Where to check the activity of MF houses whether they are buying , selling smallcaps or sitting on cash?

Posts in category Value Pickr

Sterling & Wilson Solar Ltd. – Will the Sun Keep Shining? (15-10-2024)

I frankly have no idea what RIL is planning to do with them. Cant find any commentry from them in public domain. They have failed to expand margins.

Disc: Invested

Semiconductor world – CPU/GPU Wars (15-10-2024)

I would not totally agree on that, i found an interesting article about it and wrote about. however, i have used AI to make me understand certain topics.

Will surely take that into consideration. Thank you for your honest feedback.

Semiconductor world – CPU/GPU Wars (15-10-2024)

Thank you very much sir.

Yes, even i was not able to find one. will make a new thread.

Arman Financial Services Ltd (15-10-2024)

CRAR is 35%+ for both Namra and AFSL.

Collections are 95%+ which will decrease moving forward.

Leverage at 1.8x which is lowest in industry due to recent equity round.

Rating upgrade from June’24 to Aug’24.

Business cycle downturn led to reduced NIM, disbursement, collections.

Finance cost to reduce which will be beneficial to AFSL due to low leverage.

P/B ratio at low regions vs past.

Overall looks like a good entry.

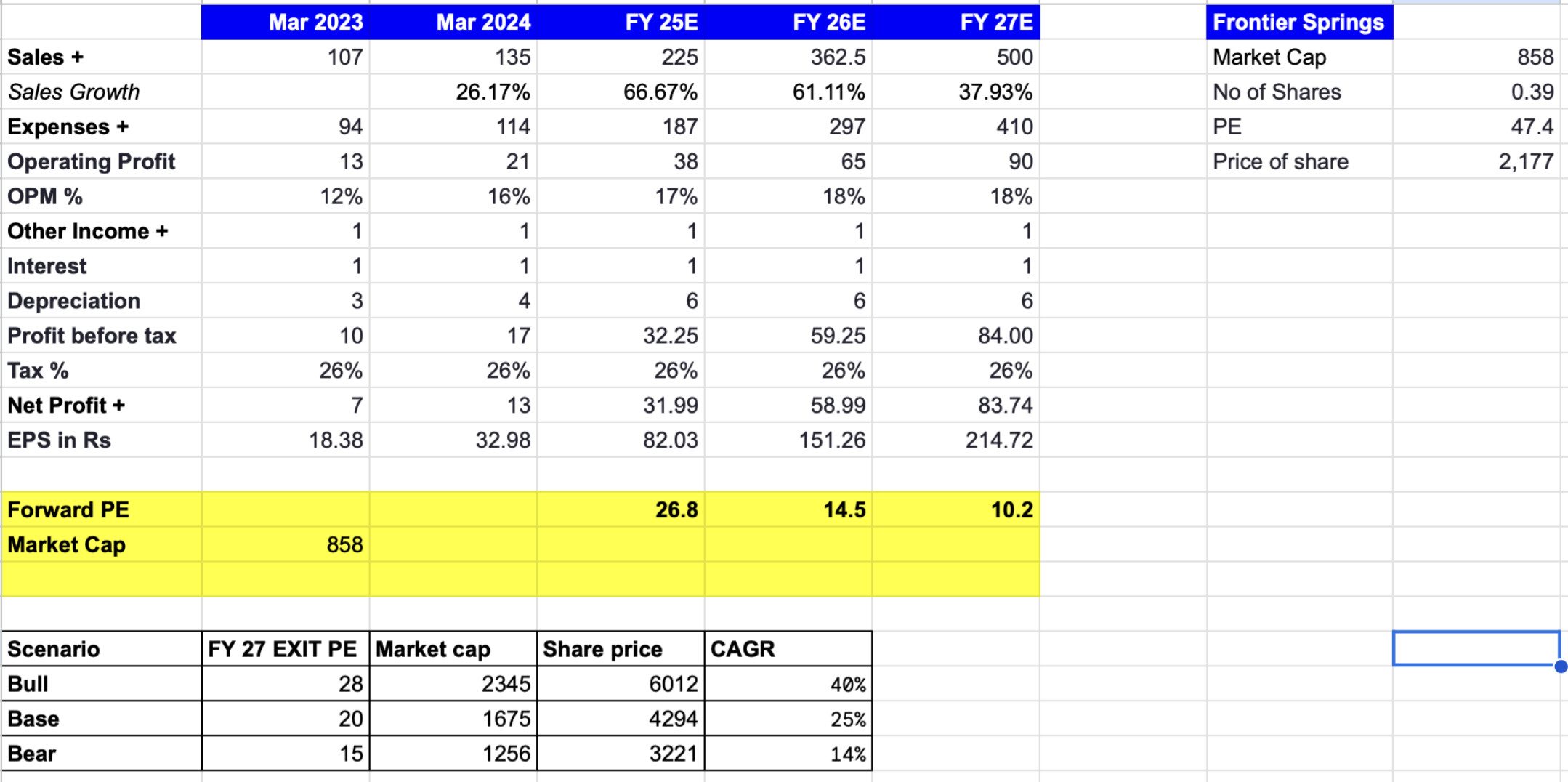

Frontier Springs – has departed, whats the next destination? (15-10-2024)

Modelled Frontier Springs as per management forecast.

Risk- Need to monitor Govt Railway Capex Spend.

Semiconductor world – CPU/GPU Wars (15-10-2024)

Seems like you used ChatGPT to generate this as it includes words like fostering, cutting-edge, significant, harness, transformative etc.

Tip: You could ask ChatGPT to use simple language and avoid complex phrases like “cutting edge,” etc.

SG Mart- Can it successfully create a marketplace? (15-10-2024)

Management guidance is to reach Rs. 18,000 Crs revenue by FY27, against that of around 3,000 Crs in FY24 (their 1st year of operation). A CAGR of 80%+.

With a 2.5% PAT margin, forward PE for FY27 at CMP (430) is ~ 7.

In FDs, interests are earned on the base we keep with the bank. No bank is going to double it up for us to earn extra bucks.

But with business it is not like that, profits can grow and when equity remain constant (as they have already raised enough money for their need), ROE will grow in future.

ValuePickr Ahmedabad (15-10-2024)

Hi, may please add me to the whatsapp group…cell no: 8700468180