@harsh.beria93 Hello Harsh, Even I could not find any reference to Pneumatic nails in their AR. Also, it is a high margin product and Geekay seems much ahead of Maiden forging in its production I am wondering why would company deny the product line in their AGM and does not capture in their AR. Any insights/inputs highly appreciated

Posts in category Value Pickr

Are Beaten Down stocks worth Investing? (20-11-2023)

His lecture is an eye opener. Simple lesson? Take a deep look at the beaten down stocks. Scour the lists of 52 week lows.

Shankara Build Pro – Building Materials Organised Retail (20-11-2023)

Q2 FY 24 Short Notes:

Sales Growth and Potential:

Revenues have grown at 31% for the first half of the year.

Retail Sales grew 27% y-o-y with Same store sales growth of 23% (13% increase in number of transactions and 12% increase in average Ticket size per Transaction).

Channel and Enterprises segment has grown at 36% y-o-y with Real estate and infrastructure upcycle. Company believes this segment to grow in coming quarters and years.

Non steel Business grown by 30% y-o-y. Non steel building Materials industry is concentrated towards second half of the year. So, company expects good growth in this segment in the second half of the year.

Private Label Tiles Brand Fotia Ceramica introduced by the company.

Non steel revenue to be 25% from the current 10% in 4-5 years. Dedicated Team set up for achieving targets in the non-steel segment.

Q2 seasonally weak Quarter due to Monsoons and Floods in some areas.

Online currently does not contribute to the revenue and it is used as discovery Platform.

Concept of Store-in- Store started with Nippon Paints and may expand to other segments in future. Nippon Paints helps in Sales and marketing side.

Revenue contribution from APL Apollo products is 35-40% and volume contribution is around 40-45%. APL Apollo relatives has recently started SG Mart in the similar space but company does not feel it as competitor and APL Apollo is strategic partner for the company and that is the reason they have subscribed to the warrants.

Revenue Guidance of 25-30% for the entire year.

Company believes with the existing infrastructure they can double their turnover in next 4-5 years.

Margin Growth and Potential:

EBITDA Margins improved sequentially from Q1 by 13bps to 3.2% due to improvement in product mix within the steel category (Flat Steel and TMT grown by 60-70% while steel roofing grown by 35-40 %) and operating efficiencies.

Gross margins on Non steel Business is 10-12% and since this is the beginning expenses are high and EBITDA margin is 5-5.5%.

Company expects margins to improve with more contribution from Non steel products.

Working Capital Cycle maintained at 30 days in first half of the year.

Geography they operate and future plans:

Company is in the process of opening two new fulfilment centers, one in Maharashtra and the other one in Madhya Pradesh in the coming months. Given our established presence in the South our endeavor is to continue our cluster-based growth approach and strengthen our penetration in the Southern region by gradually expanding to other regions.

Key Monitorable to Track:

Non steel product composition in overall Sales as this is necessary for margin improvement.

Margin Improvement to check whether company is delivering on the promises.

Relationship with APL Apollo as majority of the revenues comes from selling their products.

Same Store Sales growth Rate as Retail has more margin than Channel and Enterprise Segment.

Disclosure: Invested and Biased.

Dhanuka agritech (20-11-2023)

Dhanuka Agritech Q2 concall highlights –

Sales – 618 vs 543 cr

Gross Margins @ 40.3 vs 34.1 pc – Huge Jump !!!

EBITDA – 142 vs 98 cr, Margins @ 22.9 vs 18 pc !!!

PAT – 102 vs 73 cr

Guidance for FY 24 – double digit revenue growth over 1700 cr ( last Yr’s revenues ), EBITDA margins for full FY at around 17 pc

Company seeing excellent demand for its new product – DECIDE (insecticide) introduced LY. Fuelled by a few more insecticide introductions, growth in Q2 was robust

Launched 02 new innovative products in Q2 –

TIZOM – Herbicide for sugarcane crop – in collaboration with Nissan Chemicals Japan

SEMACIA – broad spectrum insecticide having excellent efficacy over a range of crops

Product wise sales break up for Q2 –

Insecticides – 44 pc

Fungicides – 18 pc

Herbicides – 25 pc

Others – 13 pc

Geography wise sales break up for Q2 –

North – 24 pc

South – 31 pc

East – 11 pc

West – 34 pc

Company’s unique strengths –

Asset light model with minimal investments in Fixed assets

40 warehouses, 7000 distributors, 80000 retailers covering over 1 cr + farmers

90+ products across agrochemicals and plant growth regulators

Tech Tie-ups with leading global companies from US, Japan, EU

Robust pipeline – focus on launching margin accretive 9(3) products. To launch 8 new products in next 2 yrs

Volume growth in H1, Q2 @ 10 and 20 pc respectively

Gross margin expansion in Q2 happened because of 2 factors – better product mix, phasing out of high cost inventory

Insecticide – DECIDE did very well in Q2. It’s a versatile insecticide. It’s a 9(3) registration product used across a variety of vegetable crops ( like chillies, brinjal, tomatoes, okra etc ) against the sucking pests. Hence its Mkt potential is also big

Dahej Technicals plant got commissioned in Q2. Nil revenues in Q2. Should contribute from Q3 onwards

DEFEND – a paddy crop herbicide should do well in H2

Plus there is upcoming Chilli season in South India – which is again a good opportunity

SEMACIA, TIZOM also have good sales potential in H2

In talks / discussions with a number of international partners for CDMO business. Things should materialise sometime in future

For DECIDE and TIZOM – Dhanuka is the exclusive local partner of the innovator

New products / Innovative products – introduced by the company in last 3 yrs are doing exceedingly well. Plus the margins in these products are also better

Capacity at the company’s three formulations plant is not a constraint. Company can almost double its revenues from the existing capacities

Disc: hold a tracking position, biased, not SEBI registered

Ranvir’s Portfolio (20-11-2023)

Dhanuka Agritech Q2 concall highlights –

Sales – 618 vs 543 cr

Gross Margins @ 40.3 vs 34.1 pc – Huge Jump !!!

EBITDA – 142 vs 98 cr, Margins @ 22.9 vs 18 pc !!!

PAT – 102 vs 73 cr

Guidance for FY 24 – double digit revenue growth over 1700 cr ( last Yr’s revenues ), EBITDA margins for full FY at around 17 pc

Company seeing excellent demand for its new product – DECIDE (insecticide) introduced LY. Fuelled by a few more insecticide introductions, growth in Q2 was robust

Launched 02 new innovative products in Q2 –

TIZOM – Herbicide for sugarcane crop – in collaboration with Nissan Chemicals Japan

SEMACIA – broad spectrum insecticide having excellent efficacy over a range of crops

Product wise sales break up for Q2 –

Insecticides – 44 pc

Fungicides – 18 pc

Herbicides – 25 pc

Others – 13 pc

Geography wise sales break up for Q2 –

North – 24 pc

South – 31 pc

East – 11 pc

West – 34 pc

Company’s unique strengths –

Asset light model with minimal investments in Fixed assets

40 warehouses, 7000 distributors, 80000 retailers covering over 1 cr + farmers

90+ products across agrochemicals and plant growth regulators

Tech Tie-ups with leading global companies from US, Japan, EU

Robust pipeline – focus on launching margin accretive 9(3) products. To launch 8 new products in next 2 yrs

Volume growth in H1, Q2 @ 10 and 20 pc respectively

Gross margin expansion in Q2 happened because of 2 factors – better product mix, phasing out of high cost inventory

Insecticide – DECIDE did very well in Q2. It’s a versatile insecticide. It’s a 9(3) registration product used across a variety of vegetable crops ( like chillies, brinjal, tomatoes, okra etc ) against the sucking pests. Hence its Mkt potential is also big

Dahej Technicals plant got commissioned in Q2. Nil revenues in Q2. Should contribute from Q3 onwards

DEFEND – a paddy crop herbicide should do well in H2

Plus there is upcoming Chilli season in South India – which is again a good opportunity

SEMACIA, TIZOM also have good sales potential in H2

In talks / discussions with a number of international partners for CDMO business. Things should materialise sometime in future

For DECIDE and TIZOM – Dhanuka is the exclusive local partner of the innovator

New products / Innovative products – introduced by the company in last 3 yrs are doing exceedingly well. Plus the margins in these products are also better

Capacity at the company’s three formulations plant is not a constraint. Company can almost double its revenues from the existing capacities

Disc: hold a tracking position, biased, not SEBI registered

Skipper Ltd., (Power and Water) a moat in making? (20-11-2023)

Here are the key trackables as per my analysis of the recent con-calls:-

- The company expects margin improvement in the polymer business as volumes increase.

- The company is positive about its future outlook and expects a revenue growth of over 25% CAGR for the next three years.

- The company aims to reduce debt and improve its margin profile.

- The company’s capex plan for the year is Rs.75 Crores. (As per Aug-23 concall)

- The order book stood at Rs.5372 Crores, the highest ever in the company’s history. (As at Aug-23)

- The company secured new orders worth Rs.1215 Crores in Q1 FY2024, registering a year-on-year growth of 200%.

- Engineering segment guidance is 12% OPM and polymer segment is in double digits going ahead (As per the CNBC interview on 8th Nov 2023)

- Finance cost as a % of sales will come down each year. That is what the management is targeting. Last year in Sept 2022 it was north of 5%, this year it is 4.5%. hence the debt level should be looked at from this lens.

- Order book is executable for 15 to 24 months

Growth Drivers:-

- The domestic T&D environment is showing signs of a strong rebound.

- Skipper is leveraging the China plus one trend and witnessing a surge in global enquiries.

3.The company expects good traction in the international transmission line market.

Disc: Invested

Signature Global – Biggest Real Estate Company in NCR for Mid income and Afforable housing (20-11-2023)

Hello All,

This is my second Analysis of the stock on the forum. I hope to add some value here:

This thread is for Signature Global, recently listed Affordable and Middle income housing stock.

They are into business since almost 10 years. Their strengths are:

-

Targeted Market: Focus on Gurugram, I feel this is a great strategy, this is where they started and understand the area and market very well. They don’t plan to change their focus elsewhere.

-

Focus on Mid income: Want to serve mainly Middle income to Affordable housing only. This is very important since most of the leading real estate players want to focus on luxury and that is leading to competition in that space.

-

Low capital Intensive business model: They don’t have huge land parcels, this way the capital requirement can be kept low in the industry it is generally very high.

-

Professional team: They have hired professional CEO and CEO intends to keep running company with strong values and transparency.

-

First generation family: Chairman and founder is first generation entrepreneur which I feel adds the passion needed for business like this.

Risks Involved:

- Not much is known about founder family and how honest they are. Also no proven track record.

- Company is yet to turn profitable and this is a big concern. I hope they are able to make money sooner than later.

Investment thesis:

- When they were listed, they were just 5K Market cap company. Now if you see Godrej(almost 50 K market Cap), DLF 1.5 L Crore Market cap. I feel company will start showing huge improvements once they start showing some good numbers.

- Since their focus is on Mid size, I feel this is where real growth will be in future.

- Good Brand: With my basic research about the company and few calls here and there, I found that they have good brand and their delivery record is good.

- They are reducing their debt: This is great sign, since the launch of IPO, they reduced their debt from 1000 crore to 396 Cr.

Their sales have increased from 242 Cr in 2020 to 1554 Cr in 2023. They have already delivered 6 Million square Feet (msf) real estate, 17 msf is getting built and 27 msf is launched.

With all this said, I feel if we all discuss about this company more and delve into it more, it can lead to some quality analysis and help all of us.

Note: I am already invested in this stock so my views should be very biased. Please do your due diligence before investing.

Skipper Ltd., (Power and Water) a moat in making? (20-11-2023)

In the recent con-call they have mentioned that finance cost as a % of sales on full year basis, they try to keep it down as compared to the previous year. So one quarter interest movement is not something to focus on as per them. Last year i.e FY23, it was north of 5%. This year they are targeting b/w 4% to 4.5%

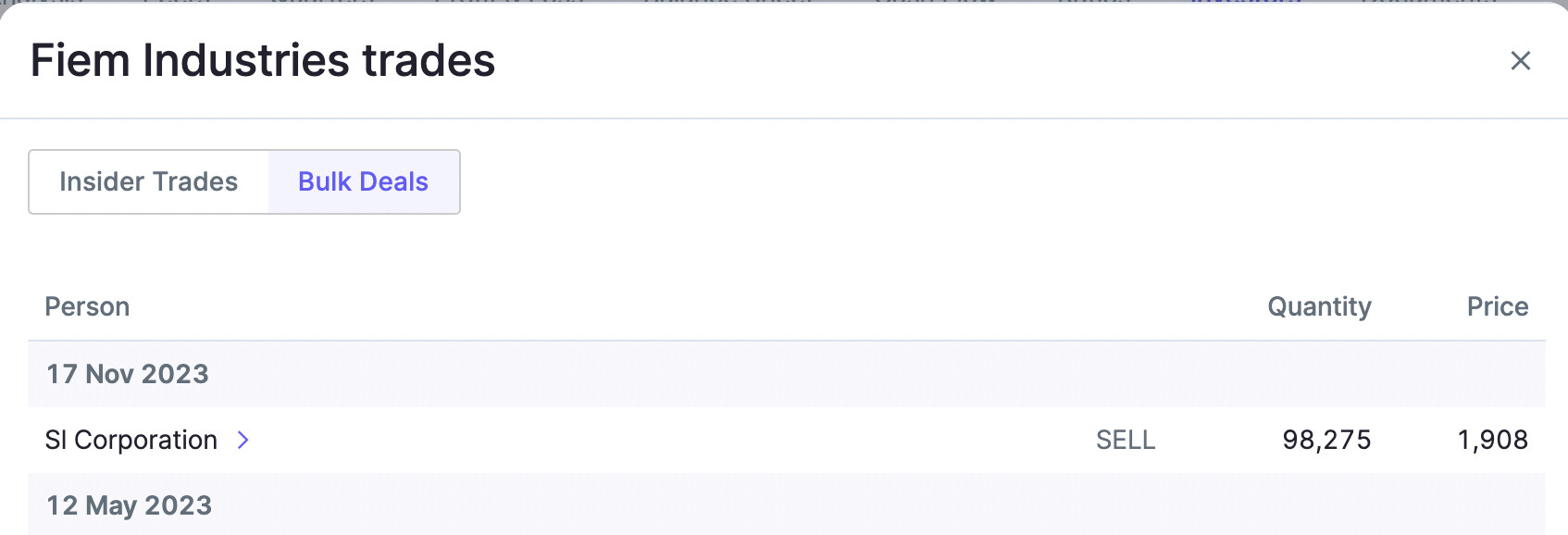

FIEM industries : auto ancillary player (20-11-2023)

Any idea, why FII are decreasing their holding continuously

Disc: Not Invested

Finkaro Unfloding The Unheard Companies with Lot’s of Potential (20-11-2023)

Here I would be Sharing Updates and Learning on the Companies which likely to be Next Multibagger in Long Run and Also Companies Which will Run On Short Run Based on Techno+Fundamental Setup,Nothing Shall hold Buy and Sell Recommendation ,Purely To Understand Rationales and Learning