Significant jump in share price today… any specific reason?

Posts in category Value Pickr

DELHIVERY – One stop solution for shipping and parcel delivery (17-11-2023)

Based on your study, what’s the moat? How do these companies differentiate?

Mudit’s Portfolio (Passively Active) (17-11-2023)

from 1st January 2023 till today (17th nov 2023) my XIRR returns are 24.33%

Gufic BioSciences Ltd (17-11-2023)

Gufic Bio – Q2 and H1 highlights –

Q2 financials –

Sales – 215 vs 175 cr

EBITDA – 40 vs 33 cr ( margins at 18.5 vs 19 pc )

PAT – 23 vs 20 cr

Domestic business – has 8 business units with a field force of > 1000 ppl. Products cover 15 therapeutic areas

CMO business – 50+ products, one of the largest lyophillization capacities in the world

APIs – specialises in anesthetics, Anti-Fungals, Anti-Biotics

International business – exports to over 20 countries

Current facilities –

Unit -1 Navsari – makes Ampoules, Ointments, Lotions, Syrups, Lyophilised powders, PFS (pre filled syringes)

Unit -2 Navsari – Lyophilised powders, PFS

Gufic Belgaum – Oral Solids – natural products

Upcoming facilities –

Unit – 3 Indore – Lyophilization, PFS

Completion by Sep 23, revenue contribution from Q3

Penem Block – Dedicated facility for Carbapenems (lyophilised, oral solids, dual chamber bags, dry powder)

Botulinum Toxin facility at Navsari – to make Botulinum toxin API and formulations in partnership with Prime Bio, USA ( used in Pain management , Derma and Neurology )

About 50 pc of company’s revenues come from Domestic business. Critical Care + Infertility care form about 70 pc of domestic business ( 45 + 25 pc each )

About 30 pc sales are from CMO business with 10 pc sales each from Intl and API business

Company has received DGCI approval for launch of Delbavancin ( used in acute skin and bacterial infections ) in India. Seeing good traction

Company sells to 50 pc of all IVF clinics in India

Company’s SPARSH division – has been set up to do the business like a wholesaler of 92 + molecules based Injectables to over 1000 hospitals in India. Currently, this division has a field force of about 40 ppl and is doing a business of about 3-4 cr/month. Expecting a good ramp up in the Sparsh division

Also launched SeraSeal under the SPARSH division. It’s an innovative homeostatic agent aimed at stopping bleeding on contact. Finding wide acceptance

Dydrogesterone ( infertility product ) – grew 20 pc QoQ in Q2. Sales expected to double in this FY

Company conducting trials for its own HMG ( human menopausal Gonadotropin ). It increases the success rate of IVF cycles. Trials are on vs established international player’s product

Q2 growth mainly led by Domestic mkt that’s doing much better

Rs 100 cr were raised by the company via preferential allotment. The same shall be used for Debt repayment

Deterioration in working capital cycle due – CMO business pick up and launch of SPARSH division where the payments are received from MNCs / Hospitals only after 90-120 days

Disc: holding, biased, not SEBI registered

Ranvir’s Portfolio (17-11-2023)

Gufic Bio – Q2 and H1 highlights –

Q2 financials –

Sales – 215 vs 175 cr

EBITDA – 40 vs 33 cr ( margins at 18.5 vs 19 pc )

PAT – 23 vs 20 cr

Domestic business – has 8 business units with a field force of > 1000 ppl. Products cover 15 therapeutic areas

CMO business – 50+ products, one of the largest lyophillization capacities in the world

APIs – specialises in anesthetics, Anti-Fungals, Anti-Biotics

International business – exports to over 20 countries

Current facilities –

Unit -1 Navsari – makes Ampoules, Ointments, Lotions, Syrups, Lyophilised powders, PFS (pre filled syringes)

Unit -2 Navsari – Lyophilised powders, PFS

Gufic Belgaum – Oral Solids – natural products

Upcoming facilities –

Unit – 3 Indore – Lyophilization, PFS

Completion by Sep 23, revenue contribution from Q3

Penem Block – Dedicated facility for Carbapenems (lyophilised, oral solids, dual chamber bags, dry powder)

Botulinum Toxin facility at Navsari – to make Botulinum toxin API and formulations in partnership with Prime Bio, USA ( used in Pain management , Derma and Neurology )

About 50 pc of company’s revenues come from Domestic business. Critical Care + Infertility care form about 70 pc of domestic business ( 45 + 25 pc each )

About 30 pc sales are from CMO business with 10 pc sales each from Intl and API business

Company has received DGCI approval for launch of Delbavancin ( used in acute skin and bacterial infections ) in India. Seeing good traction

Company sells to 50 pc of all IVF clinics in India

Company’s SPARSH division – has been set up to do the business like a wholesaler of 92 + molecules based Injectables to over 1000 hospitals in India. Currently, this division has a field force of about 40 ppl and is doing a business of about 3-4 cr/month. Expecting a good ramp up in the Sparsh division

Also launched SeraSeal under the SPARSH division. It’s an innovative homeostatic agent aimed at stopping bleeding on contact. Finding wide acceptance

Dydrogesterone ( infertility product ) – grew 20 pc QoQ in Q2. Sales expected to double in this FY

Company conducting trials for its own HMG ( human menopausal Gonadotropin ). It increases the success rate of IVF cycles. Trials are on vs established international player’s product

Q2 growth mainly led by Domestic mkt that’s doing much better

Rs 100 cr were raised by the company via preferential allotment. The same shall be used for Debt repayment

Deterioration in working capital cycle due – CMO business pick up and launch of SPARSH division where the payments are received from MNCs / Hospitals only after 90-120 days

Disc: holding, biased, not SEBI registered

Tara Chand Infralogistic Solutions Ltd (17-11-2023)

You need to put detailed risk analysis. Also need to put content on the thread. Pdf file is not preferred.

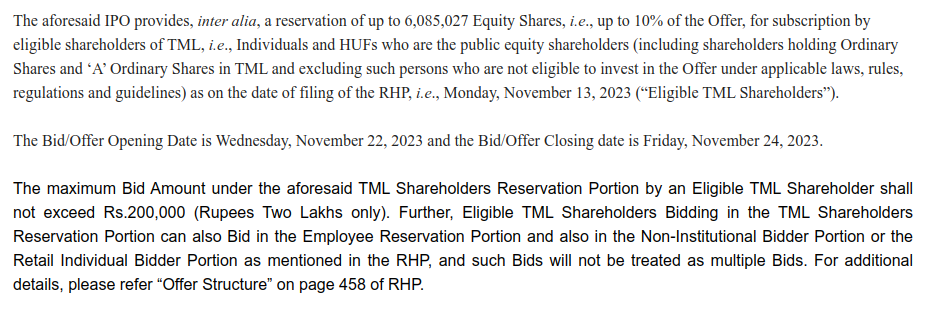

Tata Motors – DVR (17-11-2023)

At the outset, it appears to me that you get only if you bid. In bid, there is reservation and it can get in to lottery there too if bidding is more than 1x. Since 2 L ceiling is there, I think retail investors may get allotment. I did not do any calculation to check if that is reasonable or not. If some one does a calculation, please share it here.

Semiconductor world – CPU/GPU Wars (17-11-2023)

- New Microsoft Maia AI Accelerator: better than AWS, but less HBM memory than NVIDIA and AMD for large AI model training and inference

- New AMD MI300 instances for Azure: A serious challenger to NVIDIA H100

- New NVIDIA H200 instances coming: more HBM memory

- Maia is built on TSMC 5nm, and has strong TOPS and FLOPS, but was designed before the LLM explosion (it takes ~3 years to develop, fab, and test an ASIC). It is massive, with 105 B transistors (vs. 80B in H100). It cranks out 1600 TFLOPS of MXInt8 and 3200 TFLOPS of MXFP4. Its most significant deficit is that it only has 64 GB of HBM but a ton of SRAM

- Microsoft Cobalt Arm CPU for Azure: 40% faster than incumbent Ampere Altra

Investing Basics – Feel free to ask the most basic questions (17-11-2023)

Yes doctor, I gave the link I use because it also shows the number of days, profit or loss, and number of cash flows, which can be useful to gain some insights regarding the investments. Also, the user interface of the site, and the ease of giving inputs can differ too.

We can use whichever we feel like using, as the return will be the same, and if we are concerned about the data we share with sites like these, we can use Excel. I use the site.

Investing Basics – Feel free to ask the most basic questions (17-11-2023)

If you have dates and amounts, excel has inbuilt function to calculate XIRR.