https://www.wagonsfund.com/our-businesses

Check out Mohnish Pabrai’s Wagon fund – invested 30%+ of Net Assets into US coal mining companies. Is there a structural shift or change in the industry that I am missing?

https://www.wagonsfund.com/our-businesses

Check out Mohnish Pabrai’s Wagon fund – invested 30%+ of Net Assets into US coal mining companies. Is there a structural shift or change in the industry that I am missing?

Krishca has released its latest analyst concall recording.

Ganesha eco(nov 2023 ppt)

On point 4, KS K GmbH is definitely selling now after expressing intention to sell for past 1 year.

I have been following Solar for a little more than a couple of years now and that percentage has remained with me, I forgot the exact source. They invested in 2 tranches, first they took a 25 percent and then a additional stake. I will try to get the source and edit this comment, if somebody else does, I will delete this.

Can you please share some source about this 31% stake , I tried to dig in but seemed they invested some amount in Skyroot with condition that they will offtake solid fuel from Subsidiary of Solar.

Was researching this after good results… But have some questions… If you can answer as very less information available…

If u can answer would be helpful…

The MTAR Technologies Ltd Q2 FY24 Earnings Conference Call discussed several key points:

MTAR Technologies Ltd Q2 FY24 Earnings Concall

Performance Overview: MTAR Technologies reported revenue of ₹166.85 crores, with a 3.4% year-on-year increase in EBITDA at ₹36.1 crores for Q2 FY24. However, there was a decrease in profit before tax and profit after tax compared to Q2 FY23.

Order Book and Growth Projections: The company anticipates a healthy order inflow in the second half of the year from new and existing customers in the clean energy, nuclear, and defense sectors. This is expected to maintain the closing order book around ₹1,400-1,500 crores. They have received around ₹80 crores of order inflows in Q2.

Clean Energy Sector – Bloom Energy: MTAR is focusing on the production of Santa Cruz block 2 hot boxes for Bloom Energy, moving from the previous Yuma model. There was a deferment of shipping plans from Bloom, impacting MTAR’s short-term growth. The company expects to ramp up production of Santa Cruz block 2 in the coming quarters. They also mentioned ongoing negotiations with Fluence for a substantial order.

Domestic Business Outlook: The company expects a significant pick-up in domestic business, particularly in the nuclear sector. They also highlighted the ongoing projects and the expected increase in revenues from these domestic ventures.

Financial Aspects: The company is working on reducing networking capital days by the end of the financial year. There was a mention of a sharp reduction in payable days due to liabilities paid for inventories purchased in previous quarters.

Guidance for FY24: MTAR aims to generate revenue of around ₹600-700 crores by the end of FY24, with an EBITDA margin of 26% ± 1%. This guidance reflects the current business scenario and the company’s strategic focus areas.

Investments and Future Plans: MTAR is investing in enhancing its product portfolio and expanding its customer base. The company is actively participating in the space and defense sectors, with a focus on import substitution opportunities like ball screws, water-lubricated bearings, and roller screws.

Challenges and Adaptability: MTAR discussed adapting to changes in technology and market demands, particularly in the clean energy sector with Bloom Energy. They emphasized their readiness to meet evolving customer requirements.

Open Invitation for Plant Visits: The management invited investors to visit their facilities to witness the company’s advancements and future project developments firsthand

Engineers India Limited Q2 FY24 earnings conference call: https://www.youtube.com/watch?v=a1slTI2dBLY

Valuation Note update (November 2023)

Disclaimer : Invested

I wrote a note on Sanghvi in July 2023 to make sense of the valuations !

The General Conclusion at the time was :

Valuations are linked to Sales (& Ebitda) which are linked to Order book

X % of Growth in the Order book would mean ~X % of Sales Growth BUT higher EBITDA Growth because of operating leverage.

Based on the above logic, at that time I had written :

“…If for the 21% Revenue Growth (order book growth based) assumption, which we estimated would bring in 35% EBITDA Growth and ~ 50% PAT Growth,

Therefore, a 50% Revenue Growth might bring in much higher EBITDA and even higher PAT Growth.

BUT Even if EBITDA & PAT Grow by 50%, and bear in mind this is seriously conservative given that Sanghvi has high operating leverage built into its business model, we’re looking at :

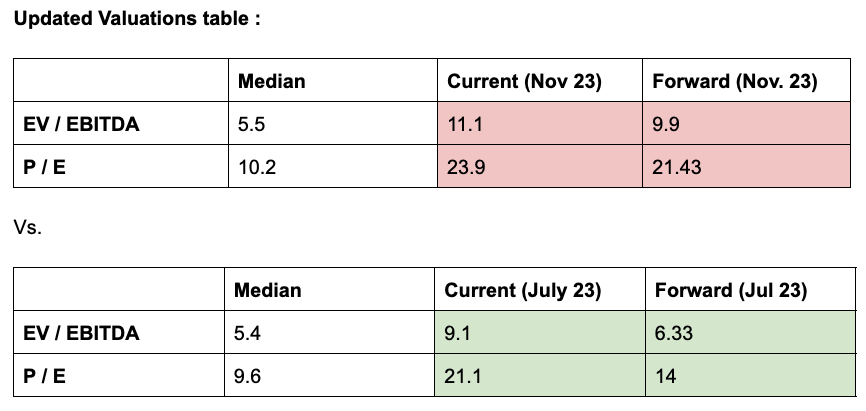

Median Current Forward (as on July 23) EV / EBITDA 5.4 9.1 6.33 P / E 9.6 21.1 14 Which, again, are not exactly mouth-watering valuations but are not as expensive optically as they seem today… “

Hindsight being 20-20, the above conclusion seems to have been mostly correct, judged not only by the Stock price movement but also judging by the more fundamental point that the Wind Energy Sector continues to grow – Big Time !

As @rcinvestor999 pointed out, Wind Energy Installations are increasing at a much more rapid pace compared to the last many years.

Suzlon Stock Price is a reflection of this bullishness.

Suzlon’s order book (~ 1650 MW) looks as robust as India’s Cricket WorldCup Team and I recently wrote a note on Suzlon Valuations too if you’re interested.

The Suzlon charm is such that I was at a Diwali party in Amritsar and one of my friends, who in 2014 had lost a shit ton of money in Suzlon has now made all of it back !

As luck would have it, he bought back the stock at 8 Rs/share and is holding onto it with his dear life.

He got so drunk that night he almost couldn’t speak but every once in a while, he randomly shouted SUZLONNN !!! at the top of his voice ![]()

And with that let’s come right back to Sanghvi’s current situation :

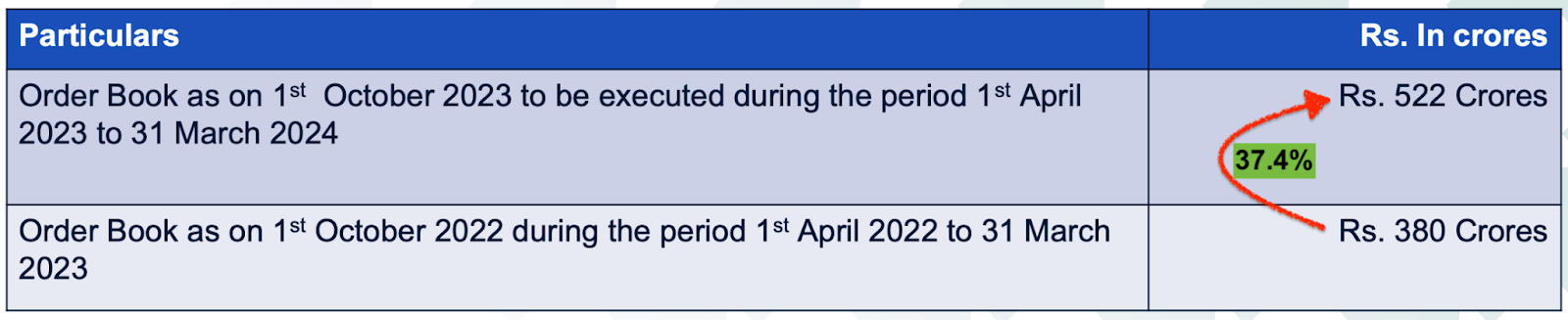

If the order book is any reflection of Sales growth, H2FY24 could see Sales growth of ~37% Vs. H2F23 Sales.

| H2FY23 Sales (Cr) | H2FY24 Sales (Cr) |

|---|---|

| 250 | 342.5 |

This means, Sanghvi can hit Total Sales of ~ 628 Cr this year if H2FY24 turns out to be in line with Order book Growth.

Let’s stay on the Conservative Side and assume growth rate in H2 FY24 Sales is ~25% Vs 37%, this means Total Sales for FY24 would be around ~ 600 Cr.

At an EBITDA margin of 60.5% (Avg of last 4 quarters), we would end up with an EBITDA of Rs. 363 Cr.

An Important point to note here is that the operating leverage angle to the story has played out fully it seems because at capacity utilization of 83-84% and OPM of 60-61%, the OPM expansion seems to be a thing of the past.

Secondly, the debt reduction and consequent outsized growth in PAT vs Sales growth is also a thing of the past. Debt has increased to ~ 336 Cr in September 23 vs ~180 Cr in March 23, which is starting to show up on the Income statement in the Interest Cost.

Therefore, going forward I think EBITDA & PAT growth will most likely not exceed Sales Growth as has been the trend for the past few quarters

Anyway, the Current EV/EBITDA based on TTM Ebitda is 11X

Therefore, on a full year basis and based on our estimated Ebitda for FY24 of 363 Cr :

EV / EBITDA comes to ~ 9.9X

Similarly, if we assumed a Net Profit Margin of ~ 27.5% (Avg of Last 4 Quarters)

Net Profit based on 600 Cr would be 165 Cr which would translate into a forward PE of 21.4X

A quick look at the above tables shows that the differential between the Current & Forward July Valuations are much higher than November valuations.

This could be because in July we were discounting full year numbers whereas as of November 23, we are discounting the numbers for the next 2 quarters.

Bottom line is that Valuations based on EV/EBITDA & P/E seem to be reflecting the bullishness in the sector and are based on the visibility provided by the order book.

Much has been factored into the stock price it seems and the order book would have to continue to get better even from this point for the stock price to do well. or multiples would need to expand.

The obvious risks also remain :

Execution Delays

Slowdown in Economy & Wind Sector and thus declining order book and consequently declining utilization

Operating leverage seems to have maxed out and if utilization declines, OPM would be hit leading to rapid decline in PAT. Remember : Operating leverage works both ways

If anyone has thoughts on the contrary or want to add something, please feel free to DM or reply here.

Thanks

Rahul