All defense stocks are booming, like Avantel, HBL Powe

Posts in category Value Pickr

Solar Industries Ltd (16-11-2023)

In just around four months the price seems to have almost doubled from around 3500 to 6875, PE is close to 80 now. Is there any particular reason for this significant price rise in such a short time?

Shriram Pistons & Rings Ltd (16-11-2023)

Since previous thread is closed, opening this new one. Admin may open the previous thread and merge it

Shriram Pistons & Rings Ltd (SPRL) has an exceptional lineage of Shriram Group, one of the most

reputed Industrial houses. Shriram Pistons & Rings Ltd is primarily engaged in the manufacturing of pistons, piston pins, piston rings and engine valves for various automotive companies in the domestic and export markets.

BS-6 Business

The Co. had acquired key businesses for BS-6 models in FY20 requiring the latest technology and stringent quality requirements. This also resulted in higher market share with the key OEMs in India. During FY21, the Co. had a smooth ramp up of products for BS-6 models, to the satisfaction of all its OEMs.

Marquee Clientele

The Co.’s customer base includes most of the OEMs in India like Maruti, Mahindra, Honda, Ford, Nissan, Tata, Bajaj, Hero, TVS, Yamaha, Ashok Leyland, Daimler, VE Commercial, Swaraj, and various others. [5] It also caters to global OEMs, namely Jaguar, Land Rover, JCB, BMW Motorrad, Volkswagen, Rotax, ZF Wabco, Yanmar, etc

In order to meet the Company’s vision for diversification and growth in areas other than IC Engines, the Company has been actively

working on identifying suitable opportunities to diversify its existing product portfolio

Key Business developments:

i. Acquisition of 51% stake in EMF Innovations Private Limited (“EMFI”)

The Company through its wholly owned subsidiary SPR Engenious Ltd. acquired 51% stake in the share capital (on a fully ndiluted basis) of EMFI (CIN: U29309TZ2016PTC027538), for a total consideration of INR 780.03 Mn.

EMFI is a Singapore backed electric motor design and manufacturing Company. EMFI is a young Technology company co-founded by engineering entrepreneurs with substantial R&D and operations in India and Singapore thereby providing localized cost effective e-mobility solutions to customers in India and abroad. EMFI has been leveraging on its strong power electronics & motors research base and extensive semi-automated manufacturing eco-system to deliver reliable EV Motors and Controllers for green mobility solutions and various other applications.

ii. Definitive Agreement to acquire 75% stake in Takahata Precision India Private Limited (TPIPL)

The Company through its wholly owned subsidiary SPR Engenious Ltd. has entered into definitive agreement to acquire 75% stake in the share capital (on a fully diluted basis) of TPIPL (CIN: U29220RJ2010FTC046888), at an Enterprise Value of INR 2,220 Mn. with adjustments for debt, debt like items and working capital to be calculated as on closing date subject to satisfactory completion of all conditions precedent.

TPIPL’s existing portfolio of precision moulded parts, precision metal moulds parts, assembled parts having a variety of functional products for the automotive and other Industrial applications, fits into the Company’s strategy of inorganic growth alongside de-risking its current business model.

Transition to EV: SPRL is exposed to the risks related to changes in regulations within the automotive industry, especially with regards to the transition to EVs, including the potential for acquisitions and/or higher research and development spending. The company derives a sizeable proportion of its revenue from the two-wheeler segment, which is among the first auto segments to witness higher electrification. Hence, the agency believes that an increase in the penetration of EVs could affect the company’s credit profile. To mitigate this risk, SPRL is trying to foray into EV components and is looking at inorganic route for the same. Furthermore, Ind-Ra expects the shift to EVs across auto segments to be gradual, and the risk is likely to play out only over the medium-to-long term. This remains a key rating monitorable.

Neuland Laboratories Limited – Transformation towards niche APIs? (16-11-2023)

who is the innovator? or market size for the same?

Kovai Medical Center and Hospital – Health and Wealth (16-11-2023)

Its finally great to see long term debt coming down. On top of that I was really surprised by the 12 % revenue growth in the Health care segment. I was expecting to see contribution from the 5th year of admissions in this quarter. Hope to see that next quarter. With the final year in, hope to see leverage kicking in and better margins

Ranvir’s Portfolio (16-11-2023)

Akzo Nobel Q2 concall highlights –

Sales – 956 vs 926 cr

Gross Margins @ 44.7 vs 38.4 pc

EBITDA – 142 vs 106 cr ( margins @ 14.8 vs 11.5 pc )

PAT – 94 vs 65 cr

Double digit growth in automotive coatings business led by OEM demand. Marine coatings also grew strongly on the back of strong orders from Defence. Protective coatings also grew well driven by oil and gas and power segments

Paints business impacted by subdued demand, erratic rains. Tier -2,3 towns showing good sales pick up. Premium end of the Mkt doing better than mass mkt

Company’s paints business is now on negative working Capital !!!

Cash on Books – aprox 670 cr

Company’s good performance in smaller towns, rural areas led by distribution led gains and lower base vs larger competitors

Q3 likely to see festive tailwinds

Revenue contribution from new products launched in last 2-3 yrs currently at 10 odd pc

Company intends to jack up advertising and sales promotion expenses from 3.5 pc of revenues currently to 5 pc of revenues. Company – advertising heavily during Cricket World Cup

B2B – business has been surprising positively. B2C – remains challenging

Company’s current Mkt share in paints business is around 4.5 pc. Intend to take it beyond 6 pc in about 2 yrs by focussing more on the mass mkt where the company is still on a weaker footing

Velvet touch – premium brand continues to do well

Disc: hold a tracking position. Not SEBI registered. Biased

Himatsingka Seide (16-11-2023)

I found the management quite bullish on this concall, which is different from the usual very conservative style. They maintained their stance of ‘stable demand outlook with an upward bias’ whilst answering all questions.

- In further questioning, they sounded more bullish when guiding that capacity utilisation should reach in high 90’s before 3 years from high 60s currently. When I asked them about triggers for this on the call (below), their reasons were pretty well outlined, though obviously it still has to play out.

-

On debt, they are happy to work on it to reduce it year by year, rather than doing something like raising capital at these valuations.

-

IMO, valuations are very attractive versus peers still for the kind of business/management this is purely because of above debt. Versus the likes of Welspun/ICIL, I think Himatseide can do some good catching up on P/B P/S in case they are able to pare down this debt (even if in a longer timeframe/maybe dilution at better than current valuations over time in a favourable business environment)

-

There is significant capacity headroom here without needing Capex in case a bull cycle is coming with all the triggers in the sector (coming out of destocking, issues with Chinese cotton ban, Pakistan industry issues, potential FTAs, new products/divisions, domestic product launch). Currently capacity utilisation for them is in the high 60s.

Essentially, I invested as I thought in the next few years the R/R was favourable and there is a chance of the dual engines of earnings growth + multiples expanding in case the situation plays out for the company.

Disclosure : Invested as core PF position in self and family accounts and hence I am biased. I am not a registered SEBI advisor and this is not investment advice. I have made transactions in the last 30 days at lower levels.

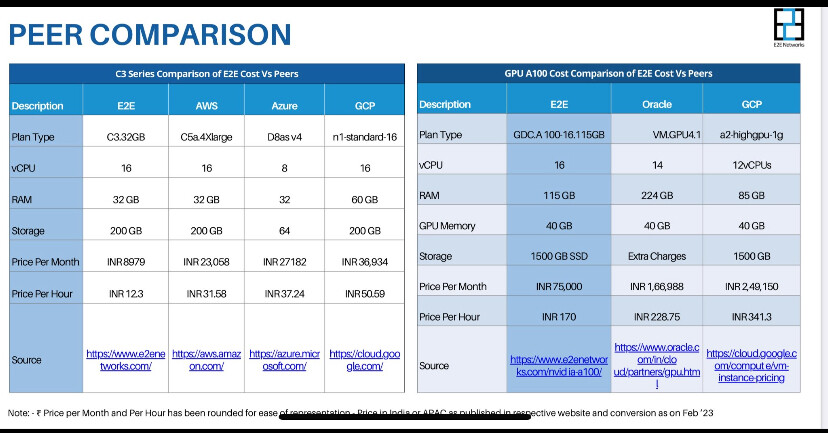

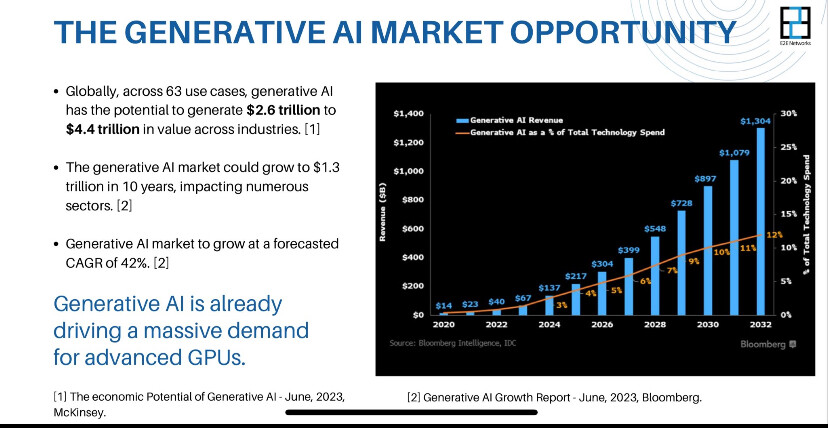

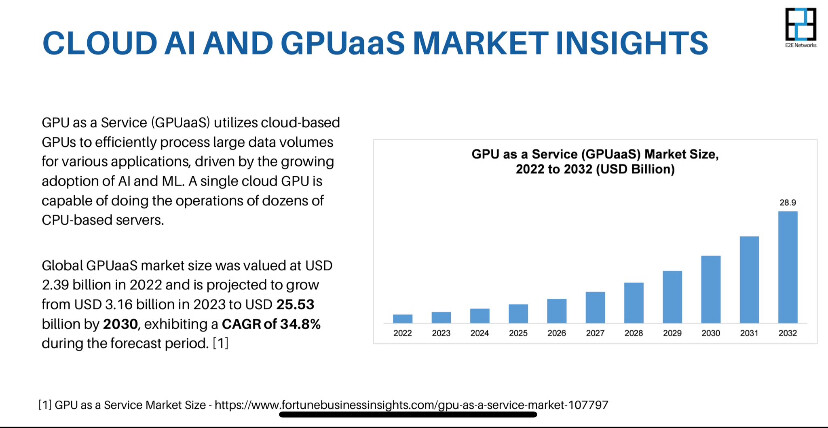

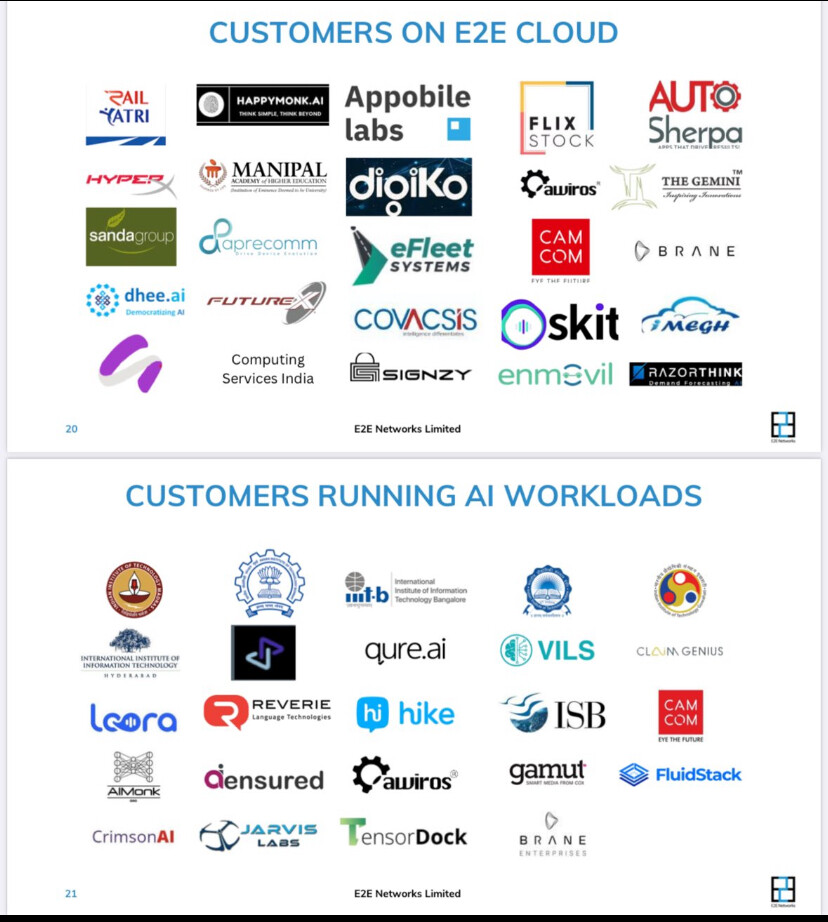

E2E Networks Ltd – Listed small Cloud computing player (16-11-2023)

This is the only Indian listed company in GPU cloud segment. Screenshots from company website is here oliw :

Please see the companies website where one can see the competitive edge what this company offer

JK Paper – Best Bet in Paper Sector? (16-11-2023)

Long term debt reduced by around 200 odd crores in the HY. Interest outgo has reduced proportionally. Crisil ratings is a good read about the capex and assets.

The company is expected to undertake yearly maintenance capex of Rs. 100-150 crore and a partially debt funded capex of Rs. ~650 crore during FY 24-26 to set up a BCTMP pulp mill, which will help in backward integration and will substitute imported pulp at Unit CPM. Despite the said capex and acquisition of Manipal Utility Packaging Solutions Pvt Ltd for a consideration of Rs. ~90 crore, expected to be funded out of cash accrual.

The company’s liquidity position remains strong, characterized by healthy unencumbered cash and bank balances of Rs. 1225 Cr (Rs. 900 Cr in Mutual Fund and Rs. 325 Cr in Bonds) as on September 2023 and average unutilized fund based limits of around Rs 163 crores (~65% of total limits of Rs 250 crores).

source: crisil ratings