Have you compared it with net web technologies. Later management looks more transparent. Any competitive Advantage of E2E vs netweb

Posts in category Value Pickr

Som Distilleries and Breweries (15-11-2023)

Why is the promoter increasing stake consistently?

I believe they plan to give higher dividends, or this guy just has a lot of disposable money.

Carysil (earlier Acrysil) – Kitchen sinks (15-11-2023)

-

The market for home improvement has been expanding rapidly in recent years

-

Well positioned to take advantage of multiple existing market opportunities

-

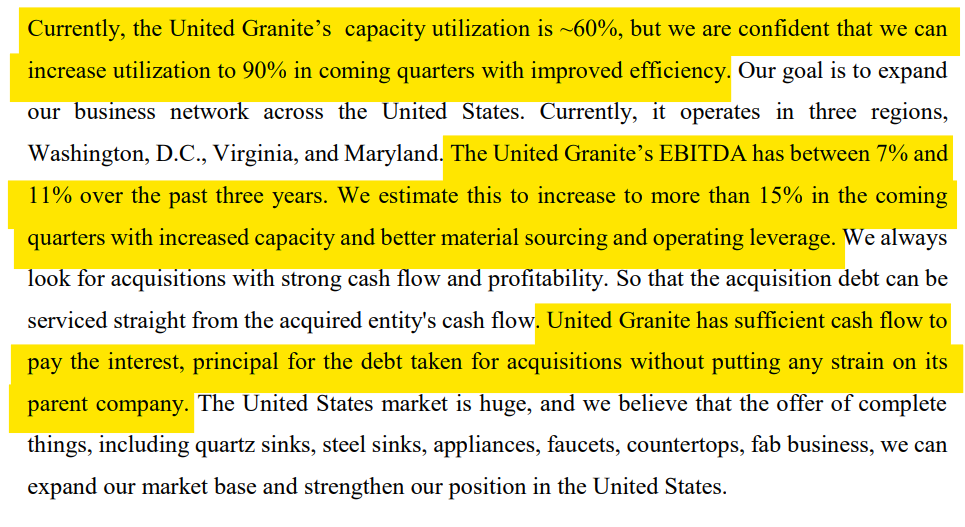

Confident to increase United Granite’s capacity utilization to 90% in the coming quarter

-

Estimate to increase United Granite’s EBITDA margin from 7% or 11% to 15% with increased capacity and better material sourcing and operating leverage

-

Increase in domestic sales starting from quarter 3

E2E Networks Ltd – Listed small Cloud computing player (15-11-2023)

Anyone having link for management concall pls share

The Anti-Portfolio (15-11-2023)

Hi vikas you doing gr8 job , i also invest in microcaps, keep 10 to 12 companies with me.

Only getting confused about MK Exim @106.5 share , after recent quarterly results. Can u pls give ur views on this conpany. My but price is 112.6 rs . Thankyou

Neuland Laboratories Limited – Transformation towards niche APIs? (15-11-2023)

Neuland gets CADIFA approval for Mirtazapine API. Don’t know how much it will contribute but should add some crores in topline and exposure to Brazil market.

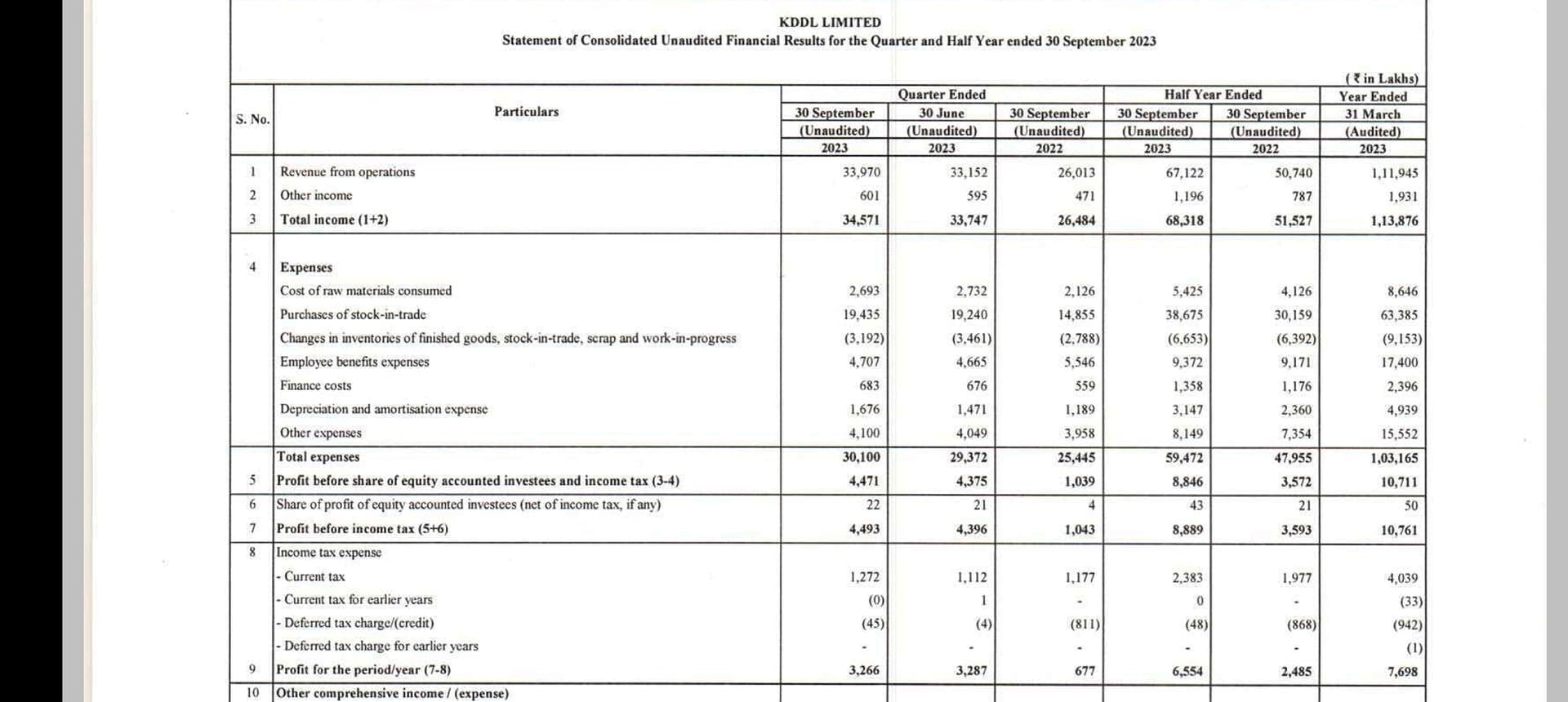

KDDL (Ethos Watches) – Scalable business model at an inflection point? (15-11-2023)

Excellent results with fantastic profit growth, disc invested no transaction since 3 months

Poly Medicure – at an inflection point! (15-11-2023)

Poly Medicure is advantage of certain MOAT.

- EU Plus strategy.: CE Certificate for Plaster device under NEW MDR.

CE Certification ensures that products meet all necessary safety, quality and standards required by EU.

Plaster device a single product but once company is habitual of such kind of certification, they will be trying to more products come under this certification (Interesting to see in future)

2.Import Substitution strategy (page 3 of 13 of Q2): further strengthening our India business as I said with two new divisions adding more people almost 100 people we will be adding during the year and out of this 100 people around 25 will be

from the clinical side will be nurses and clinical application team so we are continuing to solidify our clinical application team so that when we are launching new products, we are able to go strongly to hospitals and talk about clinical advantages of these products and most of these products will be import substitution products and they will have more higher margin compared to our existing products. So we are building that whole network and infrastructure to launch these products.

3.Banning of Unregulated products by new Laws.

- Management reply on Surplus Cash :

Himanshu Baid: So I think this is a very capex heavy industry and needs constant investment so we have to up our anti on R&D as we get into cardiology and critical care we have to increase our spending’s on R&D and bring in some new capital equipment for R&D so we have to work in that direction and this medical device industry if you look at the global industry it grows through acquisitions and

MNAs and we have done one acquisition in 2019 and I have talked about a few minutes ago that how important it is for us in terms of oncology products, and it is growing very steadily so if we find any new opportunity, we will definitely deploy our surplus crash into this new opportunities.

Tejas Networks – Product based IT business in a favored sector? (15-11-2023)

This does not seems to be a matter of concern as Tejas kitty is already full and they have to prove and deliver on their commitment of existing orders from BSNL. Also BSNL order is just playing ground for Tejas to prove to the world that they have the requisite capability to deploy end to to end network on such a large scale. Next 18 months would be critical in assessing the growth and execution trajectory and any international order wins in between. On the Italy order, they have proven their capabilities as well recently.

Additionally the “Rip and replace” campaign in US and now spreading to UK & EU will ensure that the demand will flow to India who is a trusted partner and companies like Tejas will tend to benefit.

This BSNL thing seems to be some sort of internal politics which is very much prevalent in PSU’s. So long we have the support from our Telcom minister and govt to increase domestic manufacturing of the telecom products and make it for the world then these type of news is just noise.

Happy for the learned members to share any opinions for everyone’s benefit.

Navneet Publications – a good com in education sector (15-11-2023)

While the rationale behind this investment might make sense the valuation is insane!!

500 cr valuation for a co with 7 cr revenue? And it’s rated a 3.1 on Google out of 5, so doesn’t seems like a co which has done something groundbreaking.