@Anubhav_Garg maybe near 3750 3800

Posts in category Value Pickr

MUKAND- something is changing (15-11-2023)

Why is reliance holding 2.5% ? Are the promoters somehow related to Reliance

Premiumization — A Megatrend (15-11-2023)

If we delve deeper and take into account the holding company discount for KDDL, it still seems undervalued to me. It appears that the markets have also realized this, as evidenced by KDDL’s 37%+ rise and Ethos’ 23%+ rise in the last month. I believe that this trend will continue until the gap between Ethos and KDDL’s valuations is bridged.

Hitesh portfolio (15-11-2023)

Hitesh bhai has covered this with good examples. Let me add few points from my side –

-

In many companies, when high growth is coming and company is a small/mid cap – valuations can touch the sky because everybody wants a slice of that growth. So what I have done over the years is to do staggered selling instead of selling at one go. (e.g. Shilchar is in this mode currently)

-

One thing to remember is that business environments change (macro/geopolitics etc.). It is very difficult to grow at high rates for multiple yeas consecutively. So when businesses are trading at 40-50x PE or more, one should start looking for signs of change in business environment. If one can spot those changes, selling becomes an easy decision. (e.g. EV sector is facing slowdown due to reduced subsidies and higher auto loan interest rates. One could have spotted these things and sold out on stories like SBCL etc.)

Growth slowdown when company reached 40-50x or more has happened so many times in my observation that it is almost always a good idea to start trimming once these valuations are reached. -

Watching companies go up 50-100% once you have sold out has happened many times with me and I have felt stupid for selling out

. I think this is all part of emotion management and one has to believe in the process. One has to believe that we will find another undervalued story where one will make decent money and not let emotions take over you and make undisciplined decisions. Being disciplined this way has far more benefits over longer term rather than short term pain of missing out last bits of rally.

. I think this is all part of emotion management and one has to believe in the process. One has to believe that we will find another undervalued story where one will make decent money and not let emotions take over you and make undisciplined decisions. Being disciplined this way has far more benefits over longer term rather than short term pain of missing out last bits of rally. -

Finally the best decision of whether to sell or not sell despite slowdown comes to the amount of work someone has done fundamentally.

e.g. Selling agrochemical companies few quarters back was fairly obvious choice once it was realized that fast growth was due to inventory build up.

Selling out PVC pipe companies post stellar run around COVID was obvious choice once it was clear that PVC prices were falling and there will be inventory losses and wait-and-watch mode adopted by dealers/consumers.

If one looks at SBCL, the kind of margins and ROCE it is reporting and if one can see how it is going to be part of high growth sunrise sectors, not selling is also probably right decision if you are okay to stay put for few years of consolidation.

HBL Power broke down several technical parameters and was a sell based on that around 90. But if one had worked on fundamentals, it was clearly a candidate to not sell as best growth was in future quarters and these corrections should have been taken in stride. -

There are also few other things that result in forced selling for me – e.g. I am a concentrated investor with 80-90% of portfolio in 6-7 companies. So whenever I find a better quality, undervalued, fast growing business – I end up selling my tail or bottom ones.

Over a shorter duration, it has happened that the tail business that I have sold has gone up more and high allocation business has gone nowhere. But over medium term, these things have worked out pretty well.

This constant comparison and competition amongst businesses to be able to find place in top 6-7 means one has to consider a lot of things (BQ/MQ/Business Environment/Valuations/Differential Insights etc.) and somehow this has resulted in improved decision making.

Hope this helps.

Disc – I may buy or sell some of the companies mentioned in this post without mentioning at this forum. I am not SEBI registered analyst. Please do your own due diligence.

Premiumization — A Megatrend (15-11-2023)

Actually these are results of KDDL, the holding company of Ethos Limited. I would prefer to play the premiumisation theme with Ethos instead of KDDL

Bull therapy 101-thread for technical analysis with the fundamentals (15-11-2023)

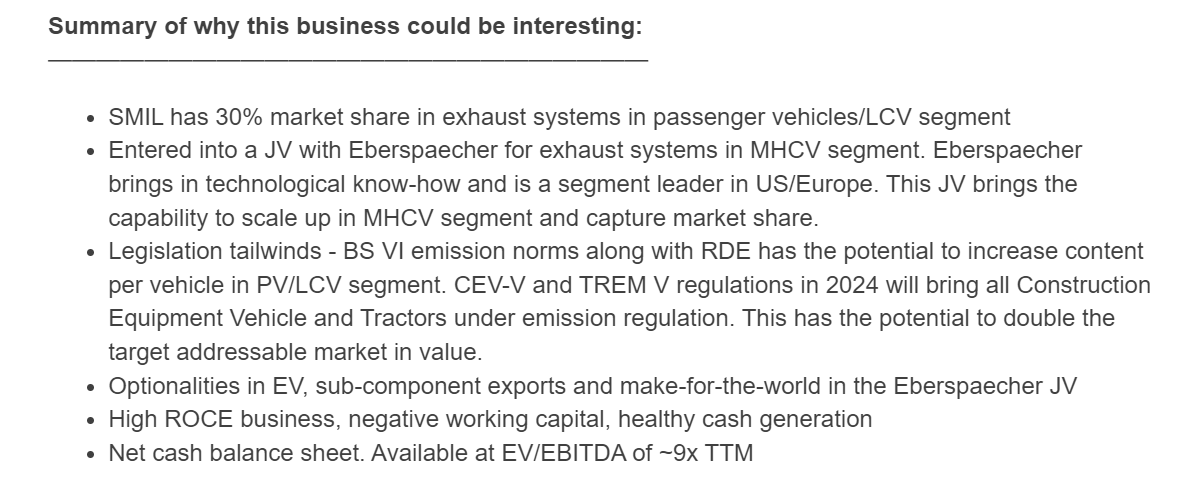

Sharda Motors, Monthly – Nice C&H breakout on the monthly. This has been a value buy for a long time but with growth in the future and not imminent. Now growth has also come in which is generally a potent combination

@manpritaurora and @nirvana_laha have done great work on the Sharda thread and I looked it back in Apr/May but gave it a pass with no immediate triggers. Now with numbers coming in and TREM V in the future, and chart setting up well, looks like its perhaps the right time.

Highlighting from the thread

Motilal Oswal Financial Services, Monthly – Getting out of the congestion zone around 1000-1100. Has done nothing in this raging bull market and has remained as a value pick.

Recent two quarters numbers are good but its not from durable streams like HFC and wealth management but from capital markets (FnO, Financialisation of savings) and Fund based activities (institutions raising capital) both of which are deeply cyclical so somewhat lower in quality IMO. But its perhaps cheaper than it deserves to trade at

Disc: Have position in Sharda Motors between 1100-1200 and MOSL around 1150.

Capacit’e Infraprojects (15-11-2023)

All impatient souls taken out today. Is there any updates on concall. Did promoters gave any byte to TV channels

Rajesh Exports: Time to examine this story seriously? (15-11-2023)

Can someone please throw light on this? Thanks

CAMS – Indirect Bet on Financialization? (15-11-2023)

So what would be the target for this stock basis the breakout on chart?