Breakout

There has been a significant jump in revenue share of CMS segment from 33% in Q2 FY23 to 55% IN Q2 FY24. The company has attributed to surge in profits to shift from low margin Prime segment to high margin Speciality and CMS segments. Sustainability of margin will depend on speed of progress from P-3 & Pre-Reg./Reg. to Commercial production.

On the valuation side, the stock still looks cheap at PE of 24.8. However the big operators may cause the price to dip in short or medium term.

Primarily due to Ismt turnaround

Board meeting was held without intimation to the exchange.

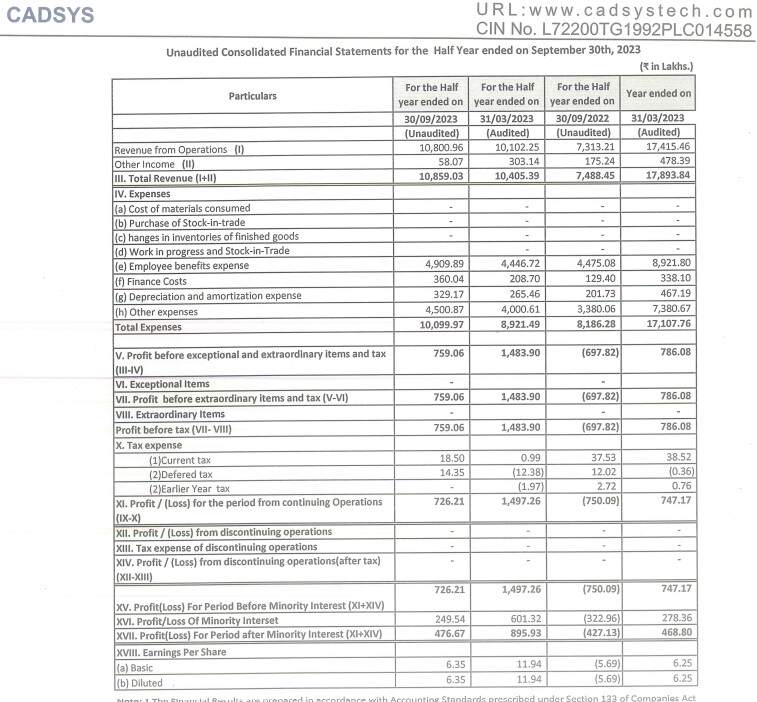

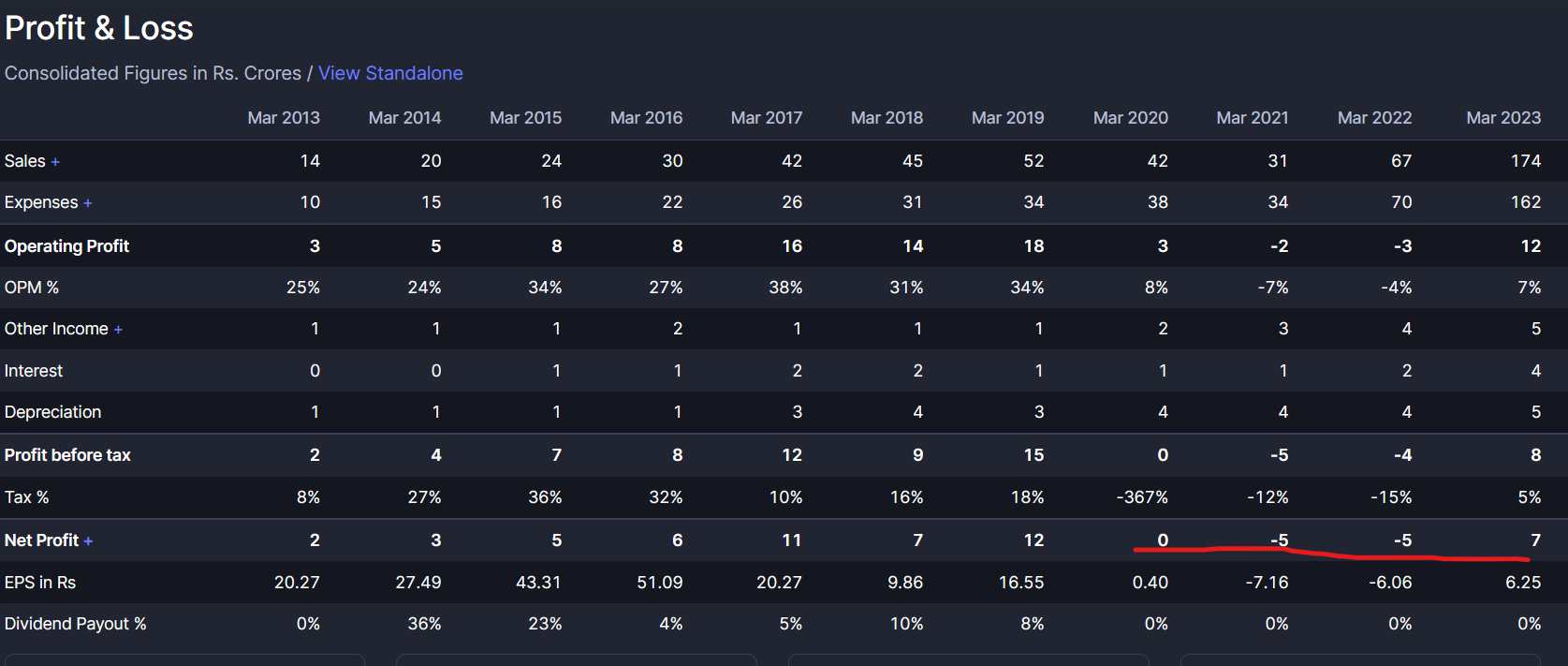

H1 Result:

PL:

Spike in all heads led to profit reduction vis-a-vis H2 FY 23. Company remained profitable and comparison YoY gives astronomical figures.

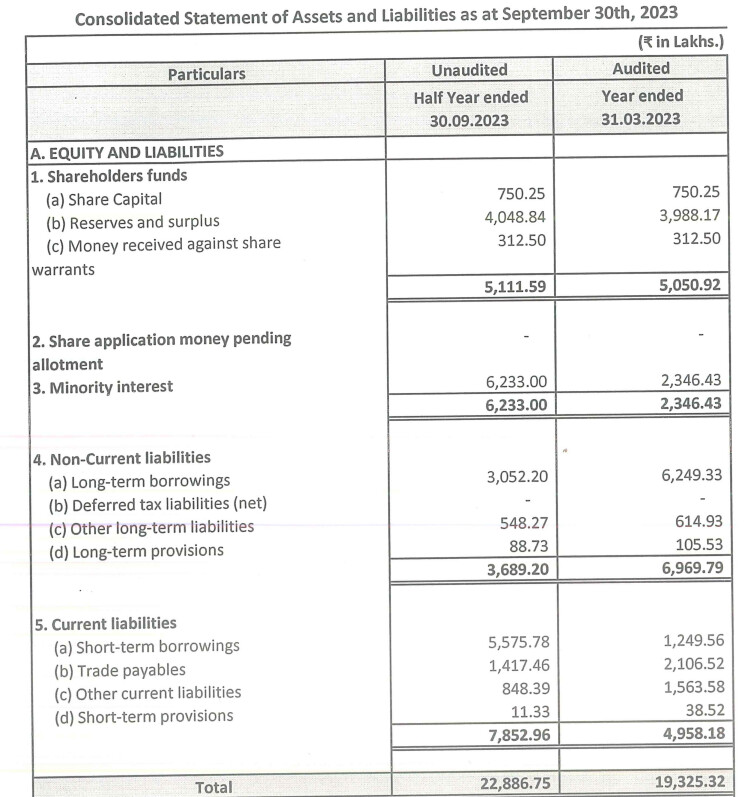

BS:

Minority Stake more than the current equity of the holding company.

Overall Debt has increased.

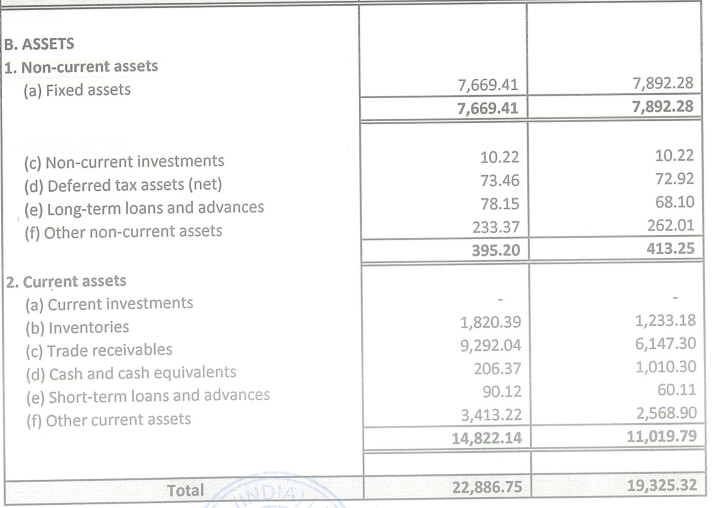

Trade Receivables are spiraling out of control.

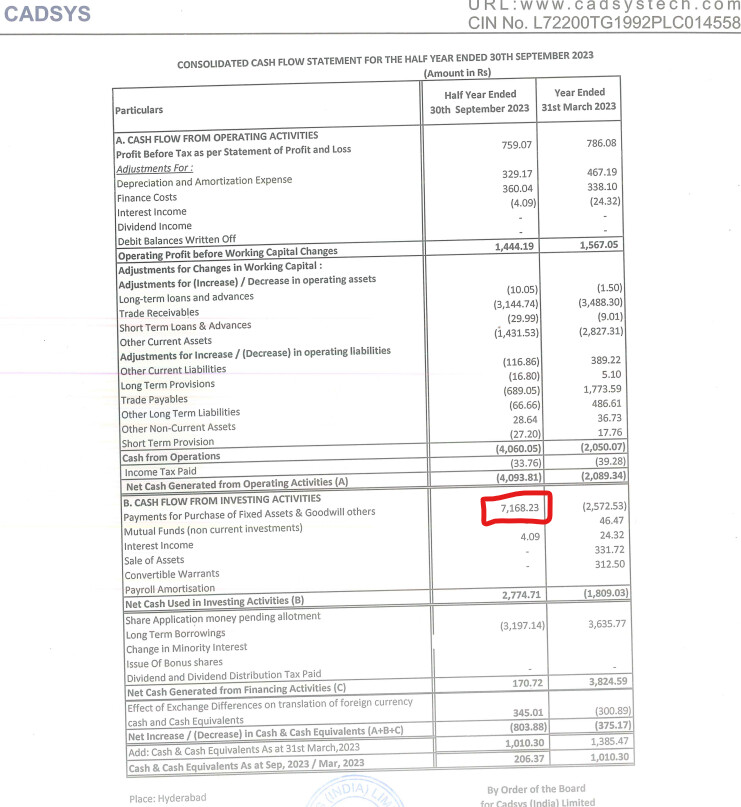

Horrible Operating cash flows, story continues from previous half.

Another matter is the Receipt from Investing Activities of Consolidated Cash Flow.

The amount invested in Apex is supposed to 30 cr, how the company arrived at this adjustment only the management knows.

More adjustment in Minority Interest to arrive in H2.

Conclusion:

Ok results with deteriorating balance sheet but increasing orders.

The company posted profit in current half which may receive positive response from the markets considering this:

Exits are always the most difficult part of investing. Few people get it right all the time.

For hardcore value investors, its often very difficult to keep holding on companies that run up fast that they have bought on very cheap vauations. I will share a few examples to illustrate this .

Very early on in 2009, in earliest part of my serious investing, I had bought TTK Prestige at the then price of 120. And in the subsequent rally it went up to 180-190… Now I had never seen big returns before with decent positions. So thinking that 50% returns in 6 months were too good to miss and I sold off. I was a newly educated investor, and markets were coming out of a big drubbing in 2009-2010. So the mindset at that time was that whatever rally was there in the market was just a pullback and we were again headed down. And the stock price went up to hit a high of 6500 in quick time. That was the first lesson for me.

I bought ajanta at 5-7 PE and had only newly learned to hold stocks for longer than 6-12 months. Results kept coming through and stock price kept going up, but serious re rating took about 3-4 quarters of consistent results. By that time stock had already gone up nearly 3-4 times and I had never had such returns on a decent allocation before. So seeing the stock quote at 15 PE I got scared and sold off my whole position at around 6 X kind of returns. But then it kept going up and that got me thinking, and I realised my mistake. I got a lucky break when there was some tax query related issue with Ajanta back then, and stock price corrected for a few weeks. I ended up buying whatever I sold and some more at only around 10% higher than my sell price. By that time a lot of other learned investor friends including some at VP were gung ho about the company and it was an easy decision for me. But it helped me in two ways… First is that when re rating happens, it often goes to the other pendulum of pessimism and often leads to froth and frolic. I made another 3.5 X from there and sold off, and stock went up from there another 50%, but I was satisfied with my returns and did not want to keep whipping a tired horse.

This helped in my future winners like Mayur, Canfin etc which I was able to hold in a better way, and got good returns.

Other important thing it did was get rid of anchoring bias for me. Subsequently, buying a stock which I had sold earlier even if it was at a higher price came naturally to me…

Most of the time this type of conundrums happen when a stock is bought as a value stock at cheap valuations and it then turns out into a growth stock later on. The valuations can go up from say 5-6 PE to 30-40 PE within a period of 2-3 years. This is the formula that leads to big multibaggers.

With experience and analysis of previous mistakes these types of conundrums will be gradually sorted. As long as the company keeps delivering growth numbers that beat market expectations, even lofty valuations will sustain. But many a times stock prices run up so fast that they will need to go into consolidation for a few weeks to a few months, or often a year or two, so that earnings catch up. This often leads to opportunity costs and in a very concentrated portfolio it can lead to diminshed returns. And these kind of run ups also skew the portfolio balance towards only one position and hence it needs to be trimmed to some extent.

There was a very good interview on agropages recently, I am capturing the summary below

02.11.2023 Agropages

Competitive advantage lies in technological edge

Recently operationalized “Flow chemistry” and “Azide chemistry” at commercial scale

Developed facility for high pressure oxidation involving toxic fluorinated compound and vapor phase fluorination synthesis

15 MPPs

R&D

Early-stage patented molecules, complex chemistries

FY23 R&D: 186 cr. (3% of sales)

Only integrated single-site centre encompassing chemical synthesis to biological evaluation to process development to scale-up

800+ employees including 500+ scientists, 185+ PhDs

50+ projects encompassing agrochemistry, electronic chemicals, and product lifecycle management

Non-agchem products: electronic chemicals, imaging chemicals, specialty chemicals

Making manufacturing sites zero discharge

Introduced a captive solar power project of capacity 637 KWp

Growth driven by exports underpinned by presence in knowledge space and not generics and commodities

Prominent brands: NOMINEE GOLD, AWKIRA, ROKET, OSHEEN, DINOACE, BIOVITA, KEEFUN, and HUMESOL

Reach: 3+ mn farmers in India

Disclosure: Invested (position size here, no transactions in last-30 days)

Keeping in view the molecules going commercial and capex announced recently,future growth potential is excellent. However the price seems to have gone up very fast. It is quoting around 4 times the annual sales. One should wait for correction before investing fresh money.

Disclosure … Invested .Avg price 900/-

Order Book as on 30.09.2023: Rs 8667 Crores out of which 73% of Projects and 27% related to manufacturing.

Acquisition of ISGES Titan: Expected to be completed on or before 31.03.2024.

Bio Ethanol Plant, Philippines: Commercial production on current month (waiting for clarification) expected peak revenue Rs 500-550 Cr / year.

https://x.com/vivekchadha1996/status/1724482521419956479?s=46

Key takeaways from concall, Feel Free to add more points.

Will continue to invest through sip mode!

#Biased #Invested