If you have read my earlier posts you will realise that I am of the opinion that this will become a duo-poly like zomato, swiggy and ola, uber. Which two is what time will tell.

Posts in category Value Pickr

Zomato – Should you order? (15-10-2024)

If you have read my earlier posts you will realise that I am of the opinion that this will become a duo-poly like zomato, swiggy and ola, uber. Which two is what time will tell.

Sula vineyards – pioneers in indian wines (15-10-2024)

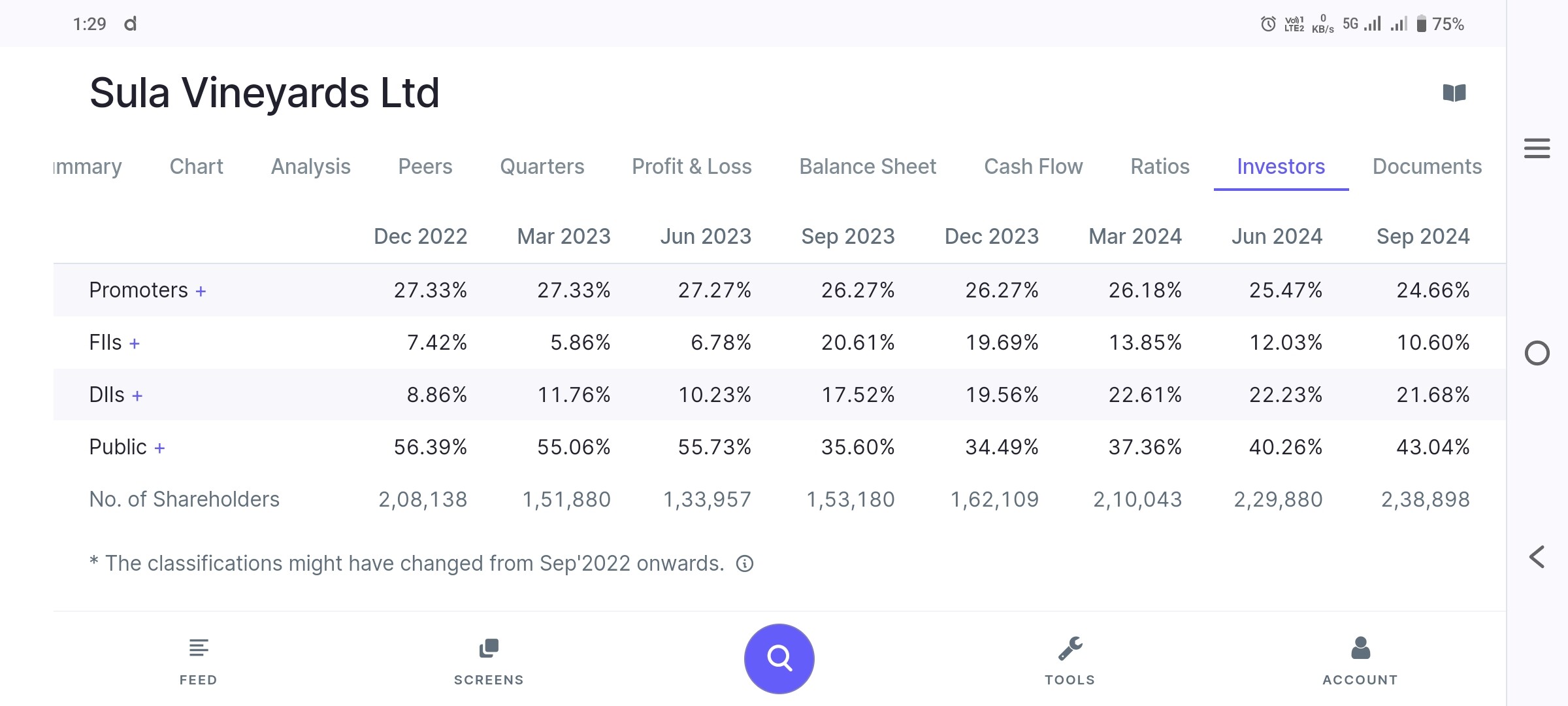

No wonder promoter holding is reducing as well.

Sula vineyards – pioneers in indian wines (15-10-2024)

No wonder promoter holding is reducing as well.

Sudarshan Chemicals – Can it colour our portfolio green? (15-10-2024)

Exports data suggests strong ~60% growth in pigments businesss in this quarter vs last year, making it one of the fastest growing chemical companies in the industry. There are discrepancies in the export data vs reported data sometimes but the trend is extremely clear. There is supply shortage.

As for acquisition, integrating a large company can be challenging but its very relieving to see that it is all coming in without debt. The mgmt has identified clear levers of cost reduction and I believe this will be an easier fruit to pluck for any inefficiently run business. Sudarshan has the most profitable business in the pigments space globally, by far and do they do seem to posses the traits of bringing down costs. As per the management, there are no contingent or pension liabilities either. So all in all , seems like a good acquisition and it positions Sudarshan as a strong #2 player in the global industrry, not too far from the leader. This has been quite a journey

Sudarshan Chemicals – Can it colour our portfolio green? (15-10-2024)

Exports data suggests strong ~60% growth in pigments businesss in this quarter vs last year, making it one of the fastest growing chemical companies in the industry. There are discrepancies in the export data vs reported data sometimes but the trend is extremely clear. There is supply shortage.

As for acquisition, integrating a large company can be challenging but its very relieving to see that it is all coming in without debt. The mgmt has identified clear levers of cost reduction and I believe this will be an easier fruit to pluck for any inefficiently run business. Sudarshan has the most profitable business in the pigments space globally, by far and do they do seem to posses the traits of bringing down costs. As per the management, there are no contingent or pension liabilities either. So all in all , seems like a good acquisition and it positions Sudarshan as a strong #2 player in the global industrry, not too far from the leader. This has been quite a journey

VP Cyclicals 2.0: Cement Industry Key Issues & Cyclicality (15-10-2024)

What is the relevance of EV/MT in cement industry? Isnt ebitda per ton a better metric? Also could someone provide a link for market share data?

VP Cyclicals 2.0: Cement Industry Key Issues & Cyclicality (15-10-2024)

What is the relevance of EV/MT in cement industry? Isnt ebitda per ton a better metric? Also could someone provide a link for market share data?

Va Tech Wabag (15-10-2024)

Wabag entry in Solar PV Sector by bagging an order worth Rs 1000 Cr

Va tech.pdf (417.8 KB)

Va Tech Wabag (15-10-2024)

Wabag entry in Solar PV Sector by bagging an order worth Rs 1000 Cr

Va tech.pdf (417.8 KB)