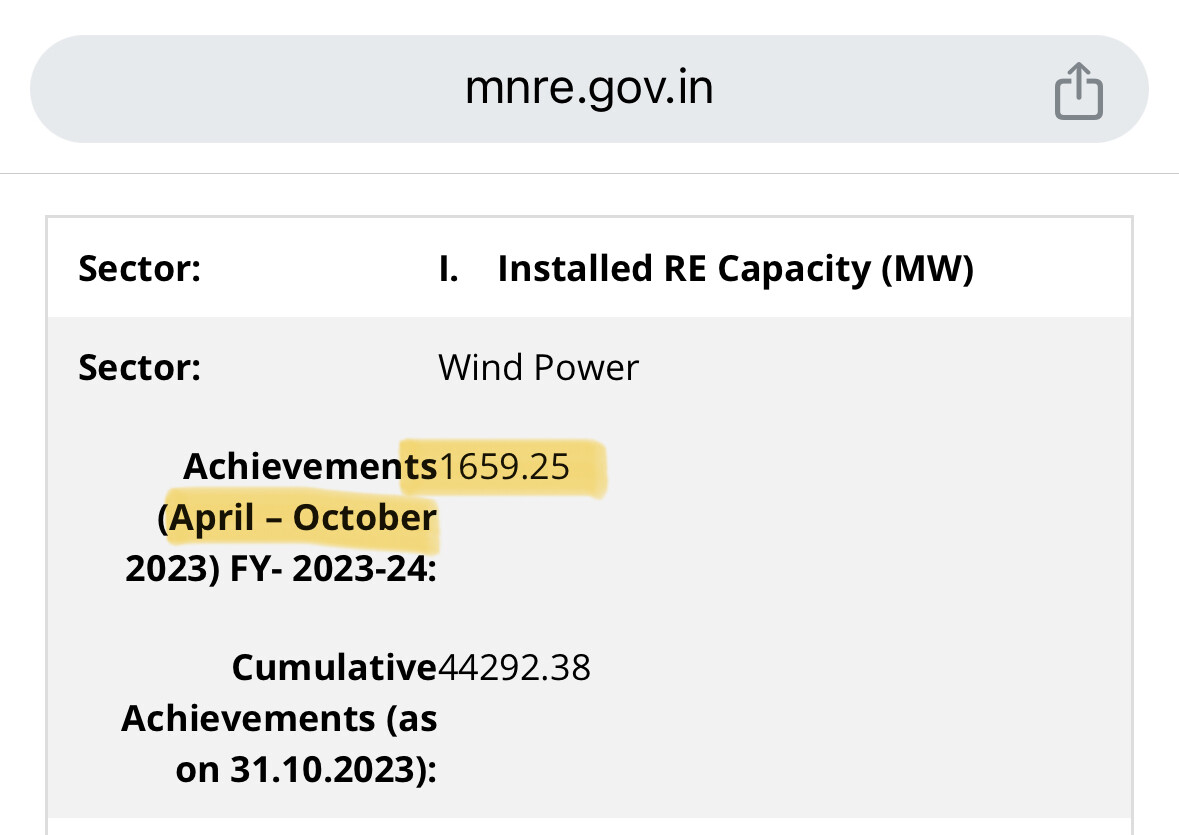

April – October: 1659

April – October: 1659

DRHP and the latest presentation are quite insightful

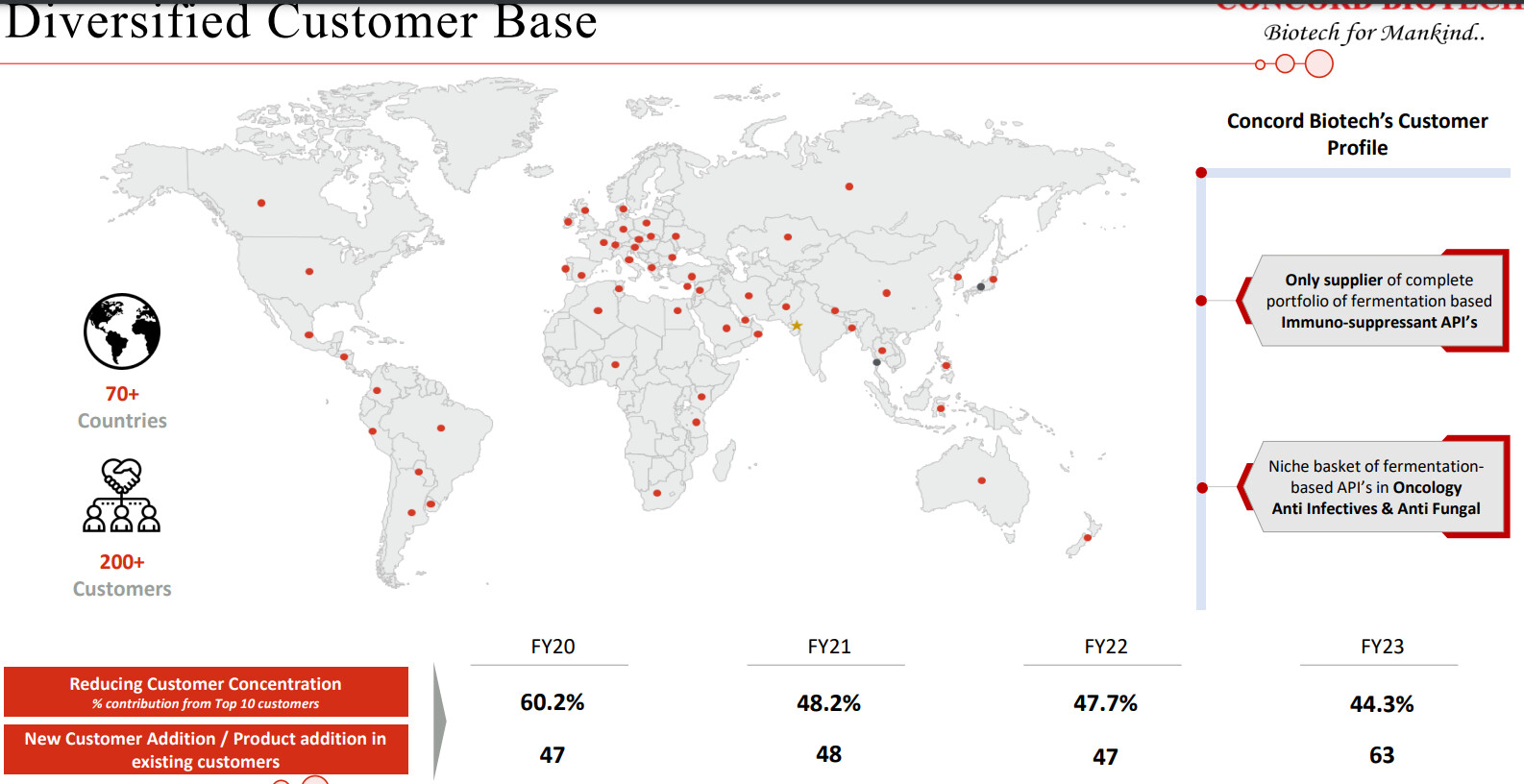

Concord has been able to crack customers in Japan, which is a big feather in their cap since entry barriers to the Japanese market are relatively higher owing to the fact that customers have high qualification criteria

IPO was 100% OFS and all of the OFS was done to give an exit to PE Investor. So, Promoters still have motivation to create value.

KTAs from Earnings Call:

| Sep 2023 | |

|---|---|

| The global API market can be broadly segmented into therapeutic areas such as anti-infective, oncology, immunosuppressants, and others. Of these immunosuppressants accounted for 7% of the market and is expected to grow by approximately 9.7% and oncology market which accounted for 19% is expected to grow at a CAGR of 19.7%. | |

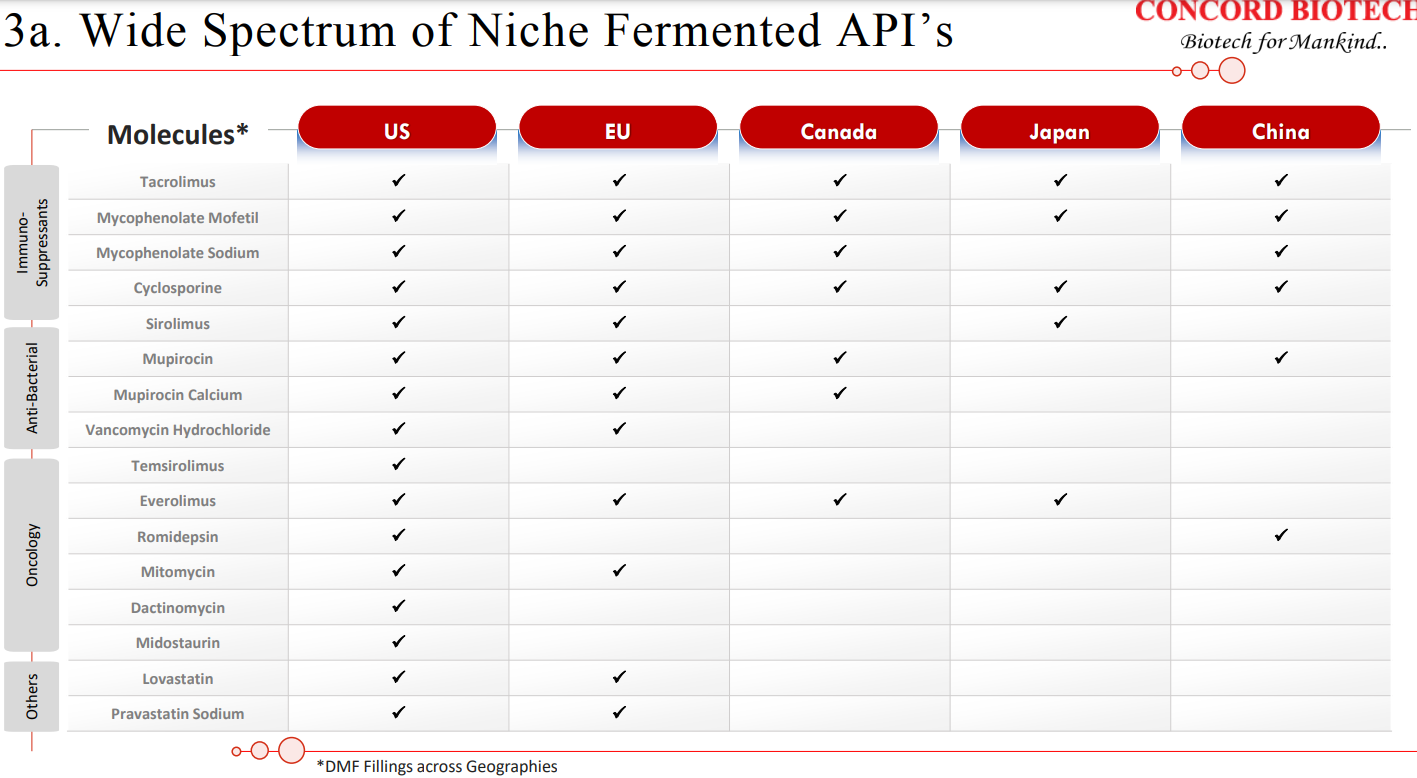

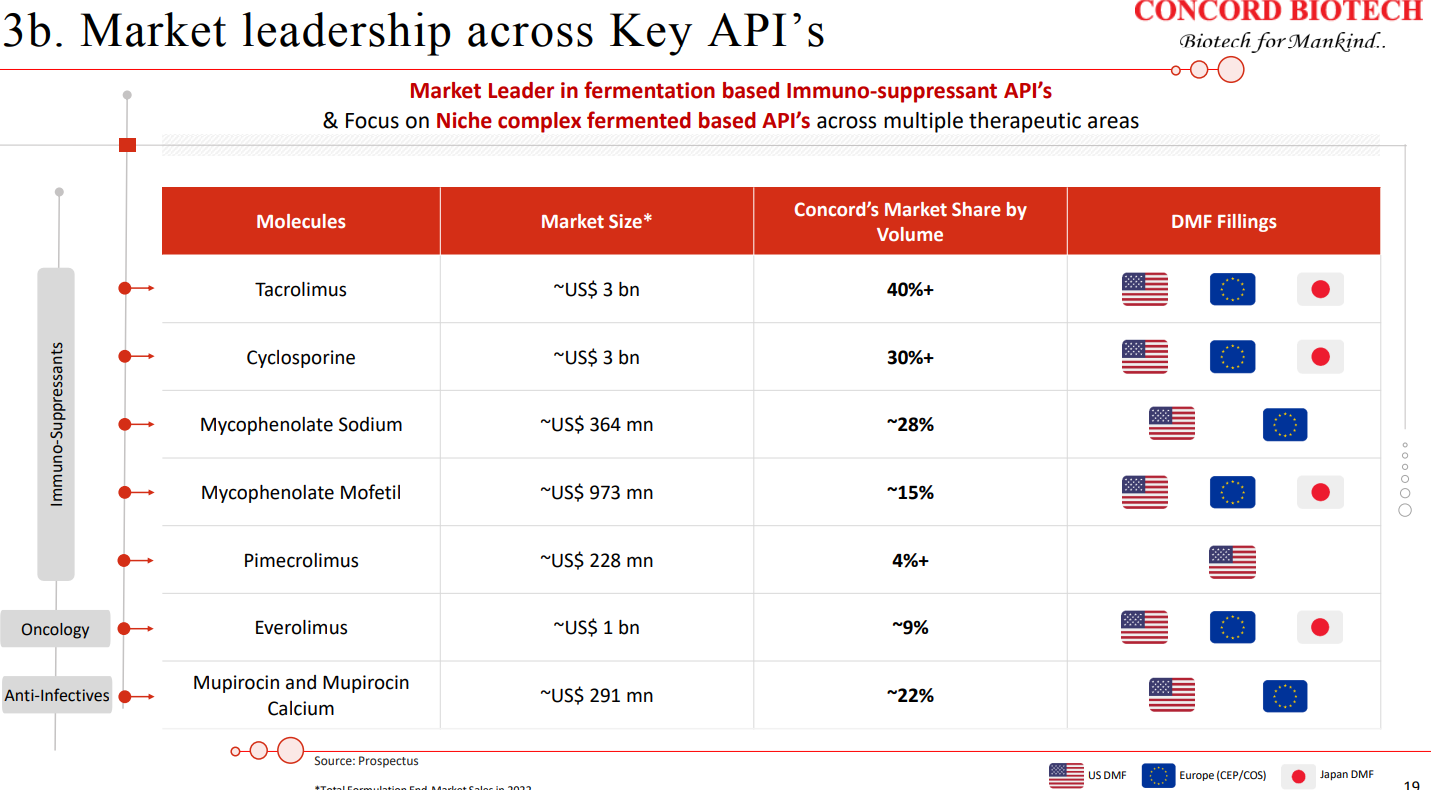

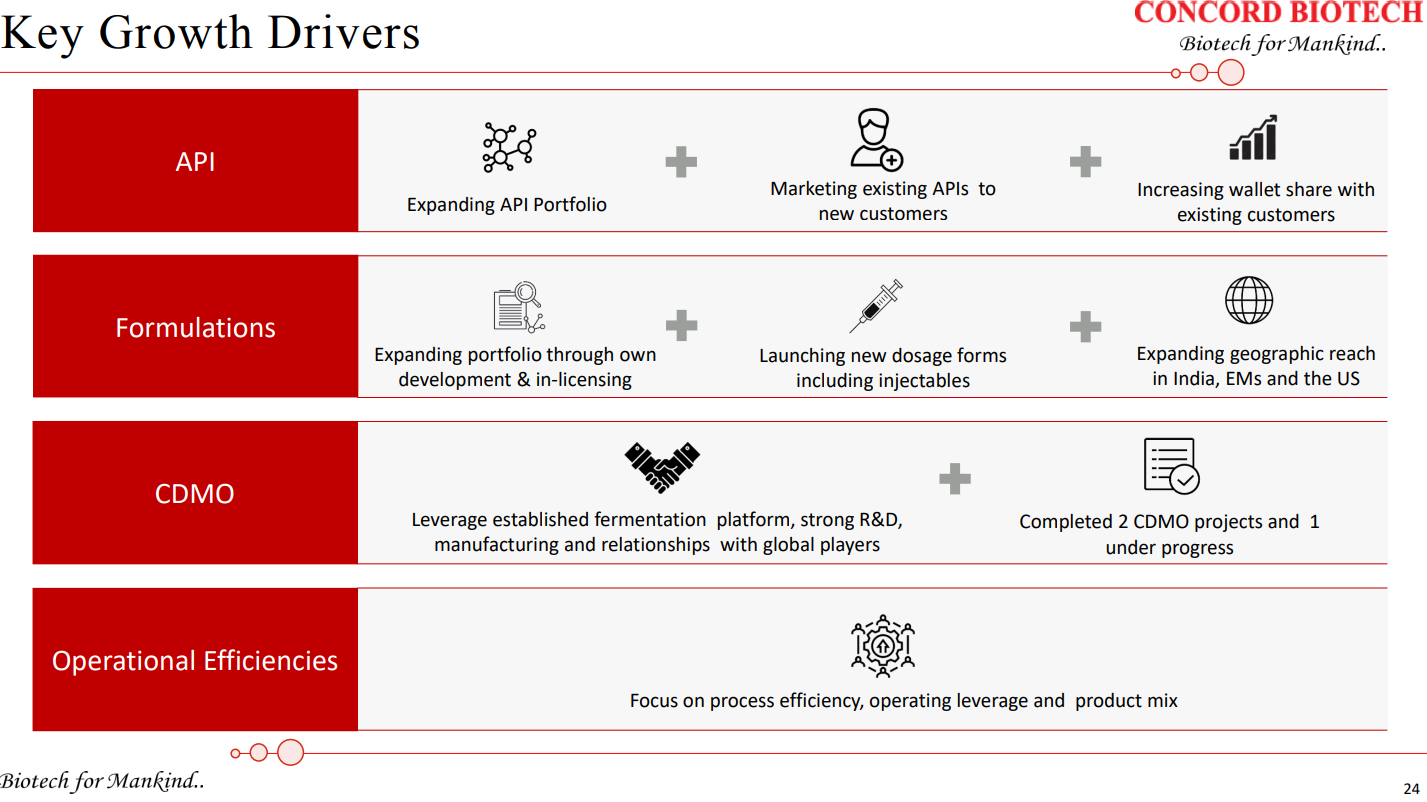

| At Concord, we are the market leaders for immunosuppressants and the only supplier in the world having complete portfolio of fermentation-based APIs for the immunosuppressants. Alongside, we have also developed our capabilities into niche fermentation-based APIs in oncology, anti-infectives, and antifungal APIs. | |

| Initially started with production of enzyme with just one manufacturing block, but with an experienced team of biotechnologists, especially in the field of fermentation. Over the years, company has made remarkable strides and currently operates approximately 41 manufacturing blocks across three manufacturing units, offering a wide range of products, spanning diverse therapeutic areas and segments. | |

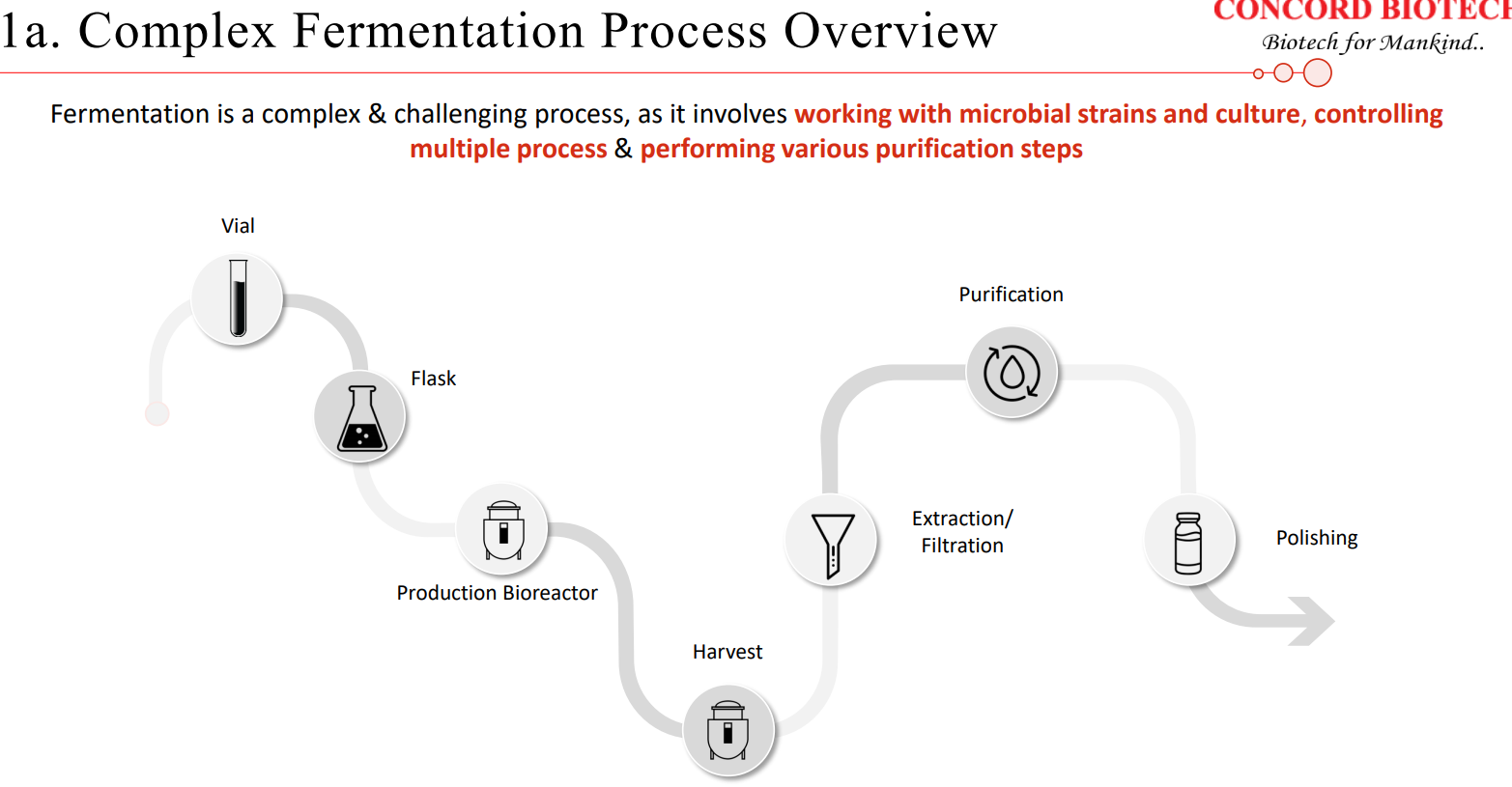

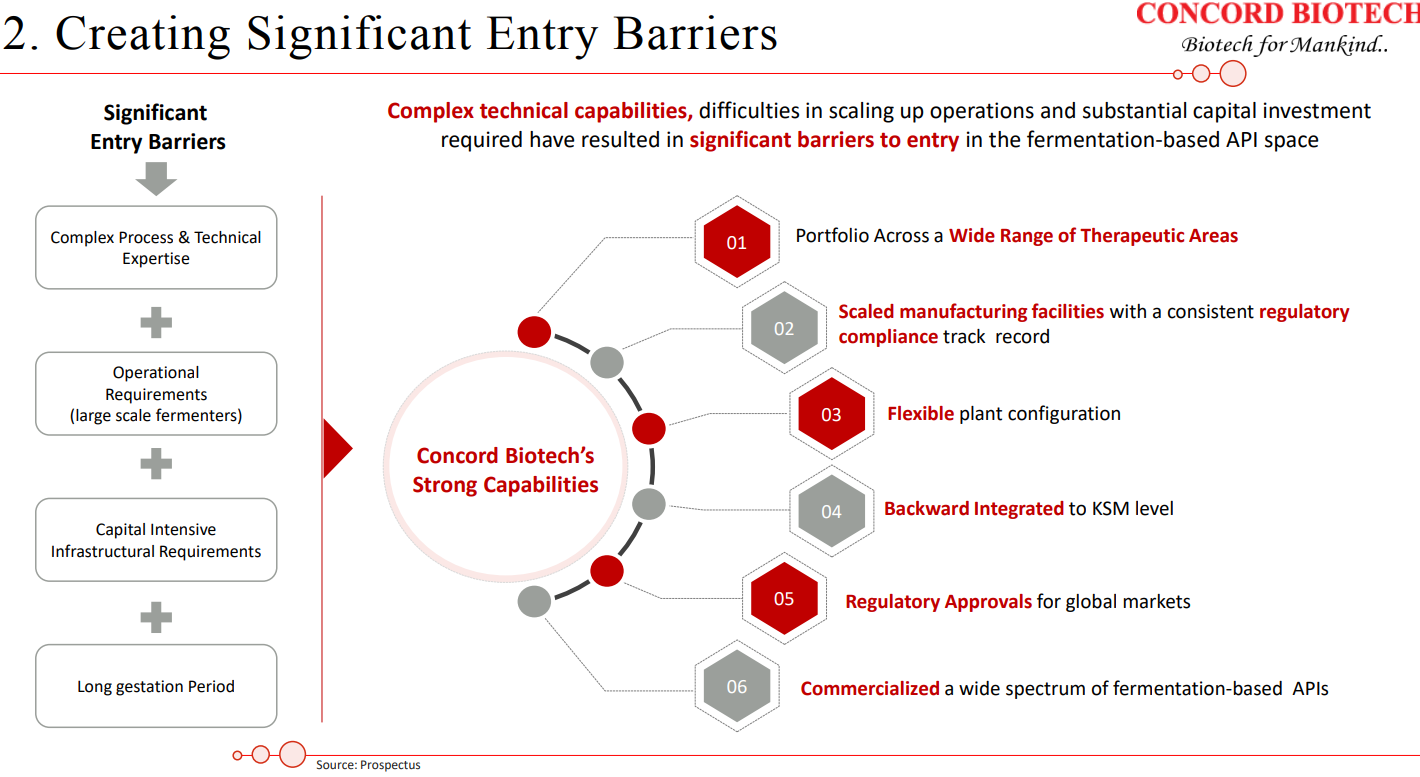

| Notably, Concord stands out on the global stage as one of the few companies that have effectively and sustainably established and expanded their capabilities in the fermentation-based API manufacturing. Furthermore, Concord proudly holds the distinction of being the only supplier of a complete production portfolio for fermentation-based immunosuppressants APIs. Fermentation as a core component of our manufacturing process presents unique challenges. It involves the intricate management of microbial strains, the precise control of multiple interconnected processes, and the execution of various purification steps. | |

| The slightest adjustment to this process can yield significant variations in the final output. As a result, this approach stands in stark contrast to chemical synthesis, requiring a highly specific, scientific, and quality-centric approach. As we expanded our market presence in the specialized fermentation-based API industry, we took a strategic step of entering into the formulation business back in 2016. Our Valthera facility was established with the purpose of producing forward integrated formulations for oral solid doses. Over time, we have successfully developed and are now manufacturing products and catering to both domestic and international markets. | |

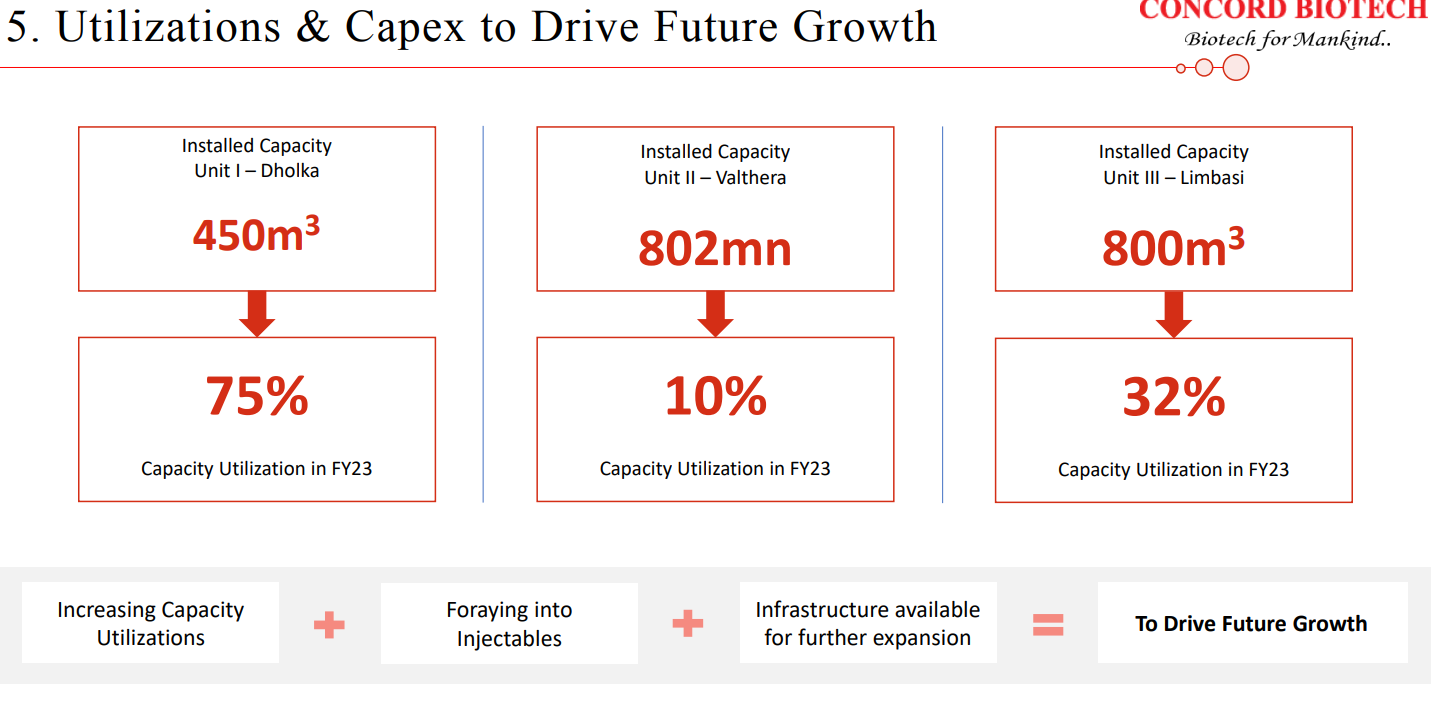

| At present, our Valthera facility boasts an impressive capacity of approximately 802 million units. Furthermore, as part of our commitment to strengthening our position in the formulation business, we are in the process of establishing an injectable facility. We anticipate that commercial production at this new facility will commence by the first quarter of the next financial year. Over the years, Concord has diligently cultivated its capabilities and an extensive range of products, positioning itself at the forefront of the competition. We have steadily expanded our customer base across global markets. | |

| This strategic approach has solidified our reputation and enabled us to make deeper inroads by attracting additional customers and further penetrating our existing client space. The production of fermentation-based API is inherently complex, making us one of the very few global suppliers capable of manufacturing a comprehensive range of products under one roof. In recent times, the industry has witnessed significant consolidation of manufacturing activities. Several companies have encountered challenges related to the growth on the back of skill shortages, lack of scalability, and a limited product portfolio. This has presented us with ample opportunities to expand our presence in various markets and geographical regions, ultimately contributing to the growth of our revenues and market shares. | |

| Our strategic focus is on further expanding our API portfolio across therapeutic areas, especially in oncology, where we currently have 6 APIs for global markets, and anti-infectives and antifungal, where we currently have 7 products. Also, we continue to invest in R&D and have a strong pipeline of products under development across therapeutic areas of Immunosuppressant, oncology, and anti-infectives, which have an addressable market size of USD 2.5 billion at the formulation level. | |

| And this will allow us to cater to the regulated markets. I’m happy to inform you that USFDA authorities inspected our Limbasi facility from 26 to 30th of June of 2023. And the inspection was successfully concluded with zero 483 observations. We now have an EIR report for the same. So with this, customers have now initiated qualification of the Limbasi facility. I would also like to highlight that we have only one manufacturing standard across our facilities, which is followed irrespective of the end markets, be it regulated or semi-regulated markets. | |

| Further, we are in the process of enhancing our capabilities in formulation manufacturing through our injectable facility. Speaking of R&D, in research and development we have set up two DSR approved R&D facilities comprising of 148 members, a significant number of whom had full doctoral qualifications. Our R&D team has showcased its proficiency in moving products, even complex ones, from the R&D stage to full commercialization. | |

| Our product selection assessment encompasses a comprehensive evaluation of factors such as the market potential, competitive dynamics, technical feasibility, and the intellectual property landscape for each prospective product. As of now, we have successfully developed and brought to market 23 fermentation-based APIs with the valuable support of our dedicated R&D team. | |

| With high quality niche products, we’ve been able to successfully add new customers across therapies and geographies over the years. We will continue with our endeavour of adding new customers and increasing in the share of wallet of our existing customers as well. To take you through our strategies going forward, our primary strategy is to continue to increase our market share and develop our portfolio of complex and niche products with high growth potential. API will continue to be the core focus of the business and we will continue to increase our wallet share among existing customers by selling them existing and new products across therapies. | |

| Also, our investments into new manufacturing capacity has enabled capabilities to grow our wallet share from existing customers. Secondly, adding new customers across different geographies with established product portfolio and with the commercialization of new products. Thirdly, increase our presence in existing formulations and add new formulations by adding geographical reach, launching new dosages, and expanding the product portfolio. | |

| And the fourth lever being the growth in the CDMO business. So, with the capacity expansion at our Limbasi facility, the China plus One strategy and given our expertise in the fermentation area, we see this as a growth opportunity for future growth in the company. And the last growth lever for us being the increased utilization of existing and new facilities by adding more customers, and products to be marketed and sold across geographies. | |

| So we have close to around eight to 10 molecules which are there in the pipeline across different segments such as the Immunosuppressants, Oncology, and anti-infectives and one would appreciate that it takes close to around six to seven years to kind of develop the molecule in the fermentation space. And there are products which are at different life cycles within the development, R&D development stage. | |

| But typically, I say that one can expect around one to two molecules that would become commercialized based on our historical trend is what I would point out. But it’ll be difficult to mention which specific product would become commercial because it will all depend upon the market dynamics about the state at which we are with respect to those molecules. | |

| So while, you know, we have been inspected by regulatory authorities, but still, this is a risk that we carry. However, we have a very strong theme of quality, QA, and QC, which ensures that quality standards are maintained on an ongoing basis. With respect to any other risk, I won’t call it a risk, but of course, any changes in the macroeconomic conditions could impact companies in the pharmaceutical space, whether it is through changes in certain raw materials or changes to certain power and fuel costs, which could affect us as it would affect any other pharmaceutical company. | |

| So as we have discussed in the past that our raw materials are usually the basic raw materials which are either agro-based or are the solvents which are typically used in the downstream recovery. And we have close to 150 to 200 raw materials that are being used for different range of products that we manufacture. So there could be an impact of seasonality on the agro-based compounds or as I mentioned due to global changes, which could affect the solvents. But then again, it may affect maybe some of the raw materials because of which there could be an impact, but it could be very, very minuscule because of it being impacting maybe one or two raw materials out of the 150 to 200 raw materials that we use. So the gross margins work in a very, very narrow band, if I would put it. And it is more about the expertise that is needed for the fermentation manufacturing, which makes the differentiation there. | |

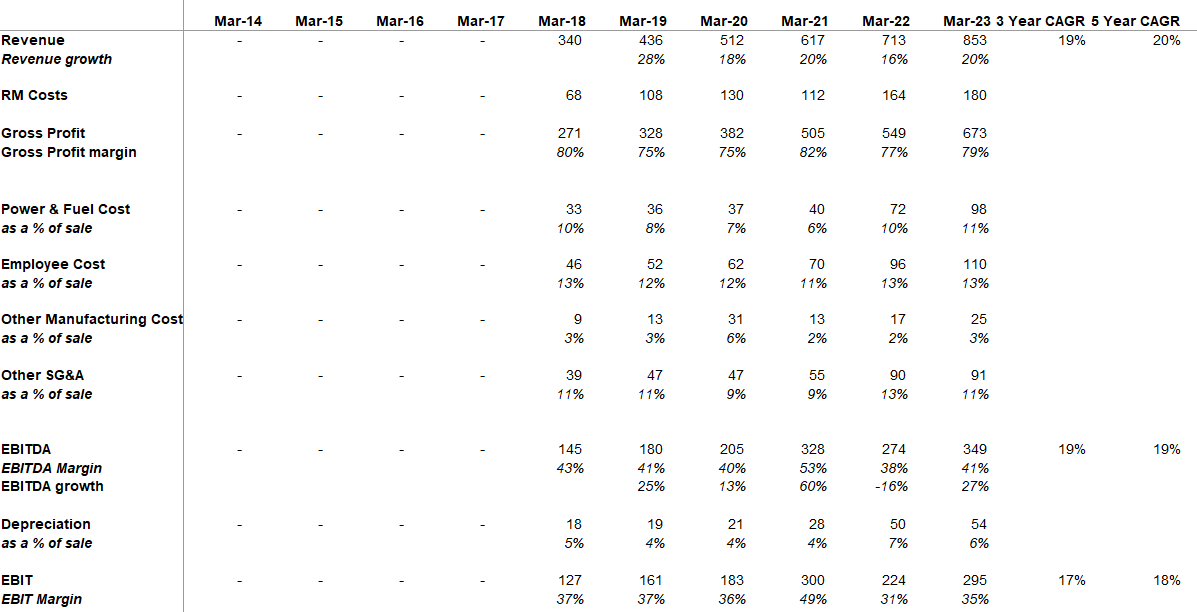

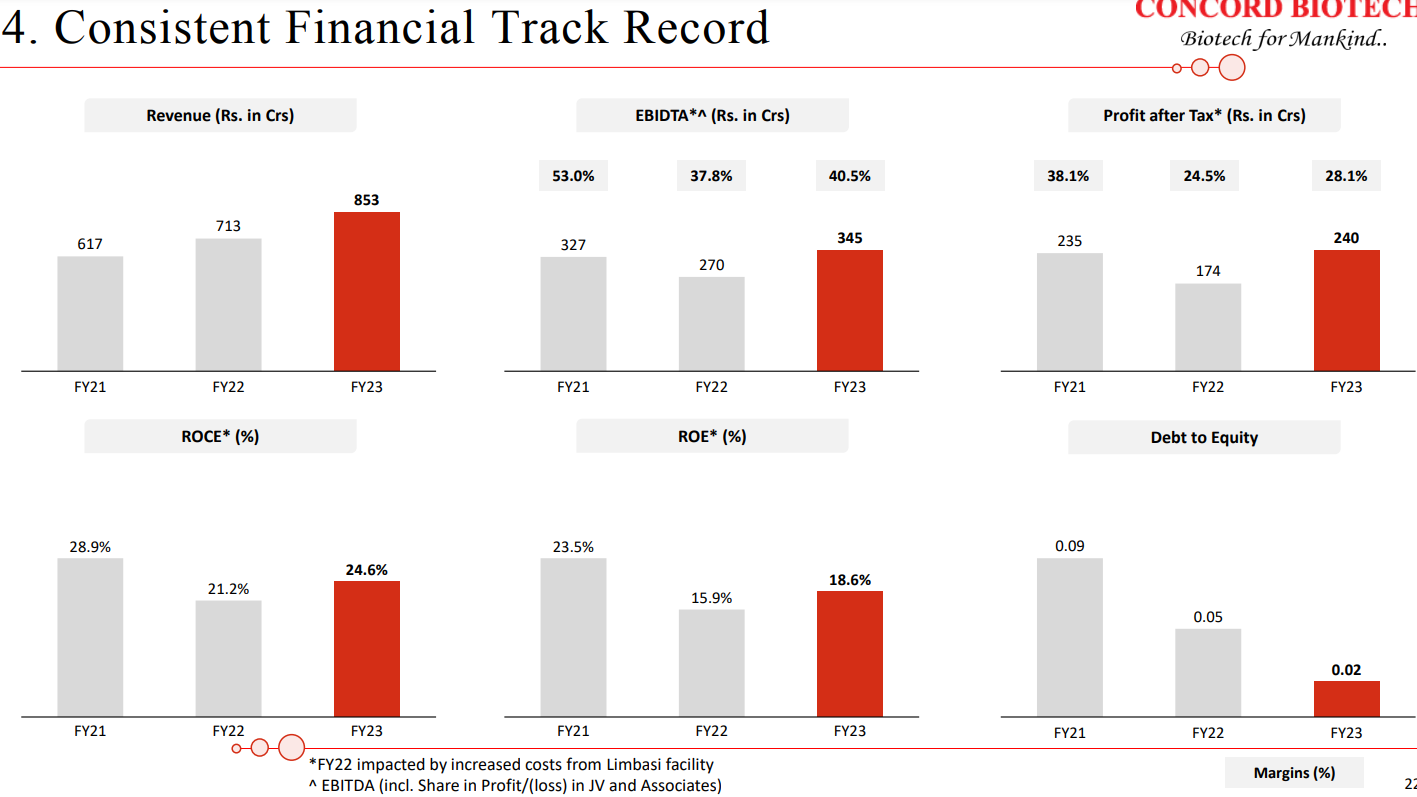

| Basically, historically, we have been growing at a CAGR of around 18% in the past for the last couple of years. In the last two years or three years, we have also built-up significant capacities with respect to the API and the formulations. And we expect to increase the capacity utilization and our growth may be better than what we have been doing in the past. So historically, we have been growing at a CAGR of around 18%, so going forward we may improve the growth per percentage. | |

| In fact, in Limbasi, we have invested around INR 400 crores of money in the capex. And with the 450-meter cube of the capacity in unit one, we are able to generate revenue of around INR 600 crores. So with an 800-meter cube of the capacity, you can begin to basically take it nearly to the level of around INR 1,500 crores, INR 1,600 crores of revenue from Limbasi facilities. | |

| Around 75% to 80% will be the right capacity utilization. | |

| So, the injectable project is running on track as we had envisaged, and we expect it to be ready by the end of this year and have commercial production by the first quarter of next year. Given that, the idea would be, the plan is to kind of first take it to the domestic market because the export market is more of a medium term to a long-term strategy for us because, by next year, we take the validation batches, put it on stability, do the dozier filing and get the approval. This is typically close to around 12 months to 18 months of time period. However, we will be going with the same integrated approach, where we have quite a few molecules, where we are the manufacturers of the API, as well as we’ll be going for the forward integration to the injectables. So you do not see many companies having that kind of fully integrated approach in some of these niche anti-infectives also, which are through fermentation. But in terms of timelines, I would say that initially we would start with the domestic supplies and then going forward, they would be, being targeted towards the export market. | |

| So CDMO is definitely an area, which is a focus to us and we now have the capacities in place, we are also building on our regulatory approvals and we have a longstanding relationship with our customers as well. So we are reaching out to customers and working with them to kind of build on the CDMO opportunity. But again, opportunities like these do take their time because customers wanting to evaluate and shift their complete manufacturing to a new site would typically be a time-consuming activity. | |

| So CDMO is definitely an area, which is a focus to us and we now have the capacities in place, we are also building on our regulatory approvals and we have a longstanding relationship with our customers as well. So we are reaching out to customers and working with them to kind of build on the CDMO opportunity. But again, opportunities like these do take their time because customers wanting to evaluate and shift their complete manufacturing to a new site would typically be a time-consuming activity. | |

| As long as it matches these criteria, which we have internally defined, we are not therapeutic diagnostic. So we would be open to look at other molecules across different therapeutic segments as well. It just happens to be that some of the molecules that we are currently under development falls within these three therapeutic segments, which is the immuno, onco, and anti-infectors, anti-fungal. But we are not therapeutic diagnosed to these. | |

| No, so I, as we pointed out that we have growth levers in place for both the API and the formulations. At the API, the new Limbasi facility which will start ramping up and at the formulation level we have ramping up of the oral solid dosage facility and the build-up of the injectable plant. So while the base will continue to grow, we expect the revenue split between the two to be somewhere around 80%- 20% as we have had in the past. So do not expect any meaningful change in the allocation between the two. | |

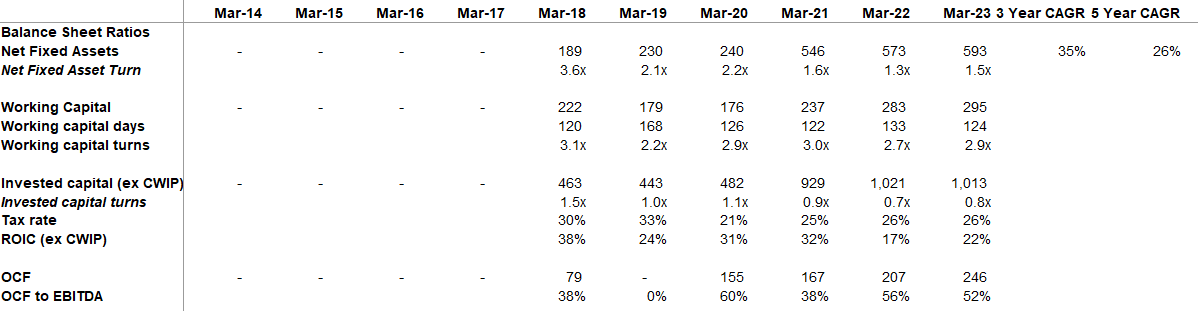

| As far as the percentage of capacity utilization is been 32% in unit 3 as of 31st of March 2023 and in formulation, it is 10% and in Dholka, it is 75% | |

| So definitely, this will boost our sales to the US as well. But again, this Limbasi facility is for global markets because as mentioned in the past that we are working on close to around 70%, 75% capacity utilization at unit one. So now that we have regulatory approvals in place, this new facility is going to be catering not only to the regulated markets, but for global markets including India and the rest of the world. And newer products that would also come in would also be commercialized at this new site. So it will definitely boost our US sales, but it would also be used to cater to global markets as well. | |

| So I would say that the products which are made through chemistry cannot be made through fermentation and products which are made through fermentation cannot be made through chemistry. So, they are two very different areas of manufacturing. However, we do see moreand-more interest coming within the fermentation space because it creates significant barriers to entry because there are not many global players in this space. So there is a good growth prospect for the fermentation but it cannot be interchanged with the chemistry APIs. | |

| So, you know, Concord holds the leadership position on several of the APIs that we manufacture. The reasons of course are that we have economies of scale, we have global regulatory approvals, strong technical expertise, and offering a basket of products. So we are the only company in the world which actually manufactures the entire range of fermentation based Immunosuppressants. So when you have these kinds of capabilities and strengths, customers look at working with companies such as ours. And that is the reason why we’ve been gaining market share year-onyear basis. And when we talk about that kind of niche, highly complex products, you typically do not see much competition coming from China. As a matter of fact, that we are commercially, we have now got approvals in China to sell our products, our APIs, which shows that, and customers are also showing interest in terms of partnering with us for the API, which kind of shows the kind of advantages and the kind of strength that we have on the API, even with respect to some of the Chinese players. And when we talk about the European counterparts, European competition, people now are talking more about the China Plus One and Europe Plus One strategy because of what is happening at the global footprint with the Russia-Ukraine war, the power costs and other things and the salaries have gone up quite significantly in Europe. And they are looking at alternate sources which are more reliable and can consistently provide them with these kinds of products. So, I think we see a lot of companies shutting down in Europe also and other parts of the world. So, we see a lot of consolidation happening in the fermentation API space. | |

| So basically around 17% of the revenue in the export, or in the total revenue comes from the US market and the balance comes from the rest of the world. | |

| In terms of cannibalization, we are not looking at disturbing the market and we are looking at value creation and opportunities within the formulation space. And that is why while we are backwardly integrated, we would look at opportunities where we can be there in the market but at the same time maintain healthy margins for us rather than going all in and destroying the value for ourselves as well as for our customers. | |

| Annual operational cost for formulation facility is ~35cr. | |

| Most of the capex has already been done as far as the growth capex was concerned. Now it’s only the operational capex which will be required to be done in the future. It will be in the range of around INR 15 crores to INR 20 crores of per annum. Yes, very little amount is required to be spent to complete the project. Majority of the amount has been spent. And yes. | |

| So you know, the prices are more or less quite similar to what you would have across the globe because, while we see limited competition on our molecules, we still are not in a monopolistic market. So when formulation companies are looking at potential suppliers. They kind of evaluate new suppliers based on which is going to supply, and give the best price. So we also have many Indian companies which are targeting the US market and they have a good amount of clarity on what the prices are there in the global markets, including in India being offered by some other manufacturers. So I would say that there is not much of a difference between what the price you offer to Indian versus that to the US. |

DRHP and the latest presentation are quite insightful

Concord has been able to crack customers in Japan, which is a big feather in their cap since entry barriers to the Japanese market are relatively higher owing to the fact that customers have high qualification criteria

IPO was 100% OFS and all of the OFS was done to give an exit to PE Investor. So, Promoters still have motivation to create value.

KTAs from Earnings Call:

| Sep 2023 | |

|---|---|

| The global API market can be broadly segmented into therapeutic areas such as anti-infective, oncology, immunosuppressants, and others. Of these immunosuppressants accounted for 7% of the market and is expected to grow by approximately 9.7% and oncology market which accounted for 19% is expected to grow at a CAGR of 19.7%. | |

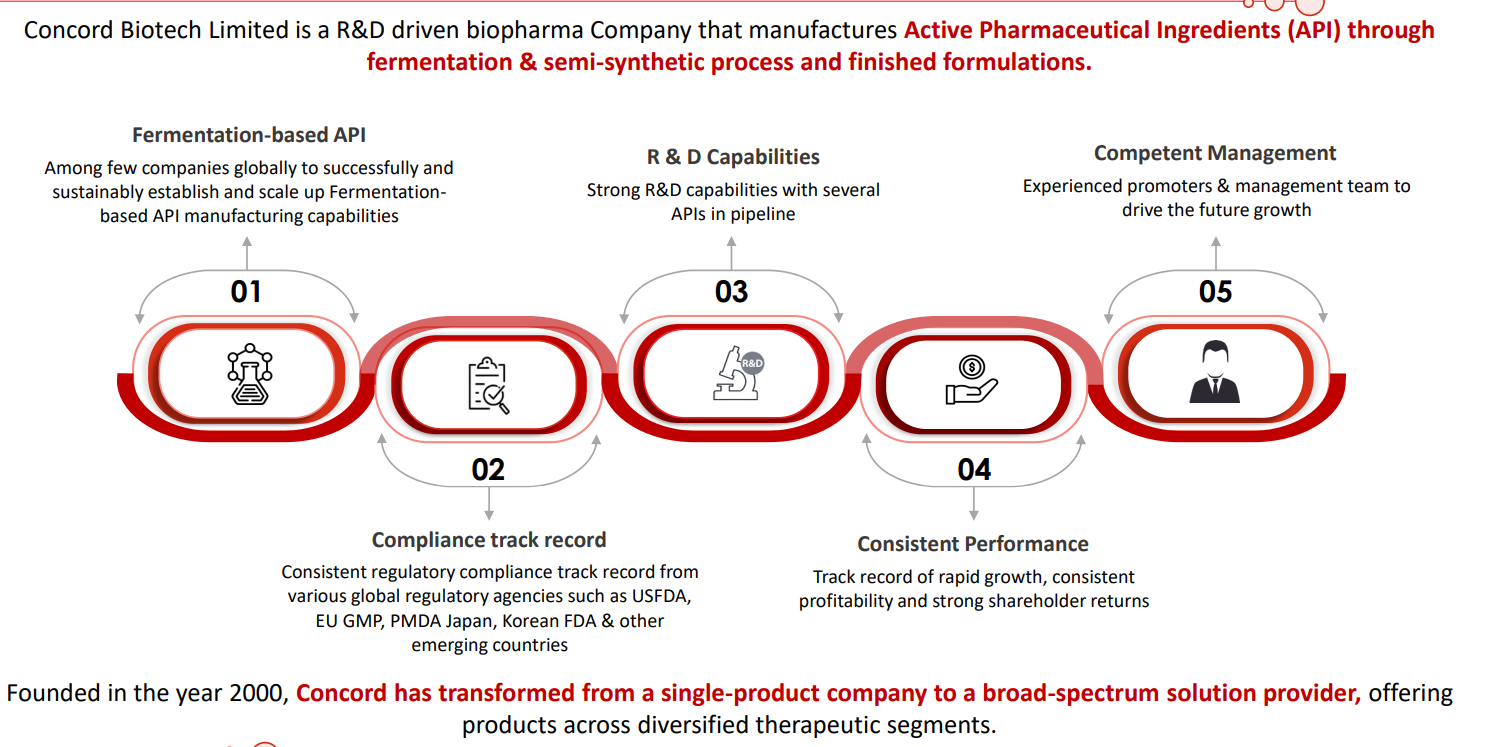

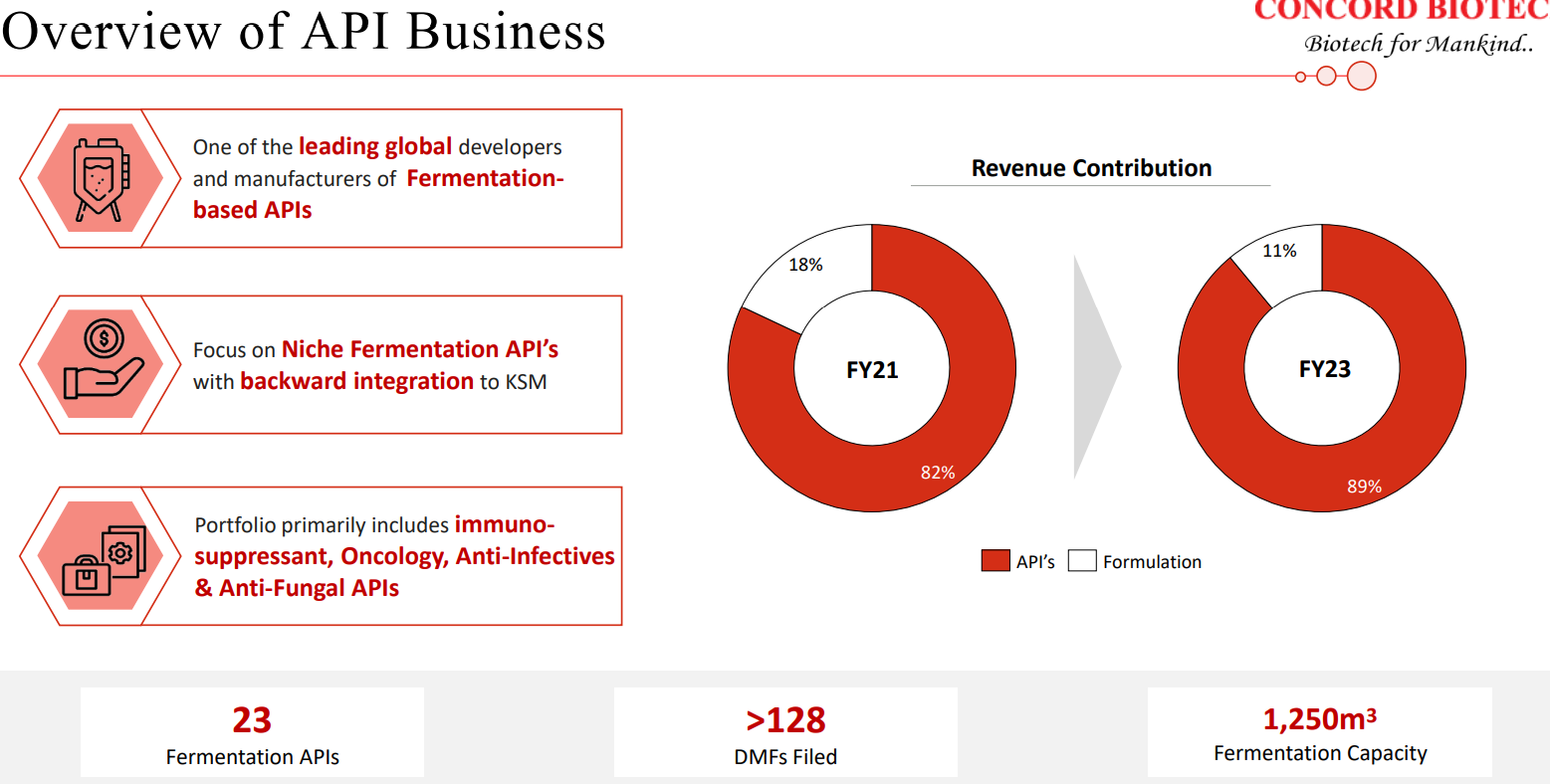

| At Concord, we are the market leaders for immunosuppressants and the only supplier in the world having complete portfolio of fermentation-based APIs for the immunosuppressants. Alongside, we have also developed our capabilities into niche fermentation-based APIs in oncology, anti-infectives, and antifungal APIs. | |

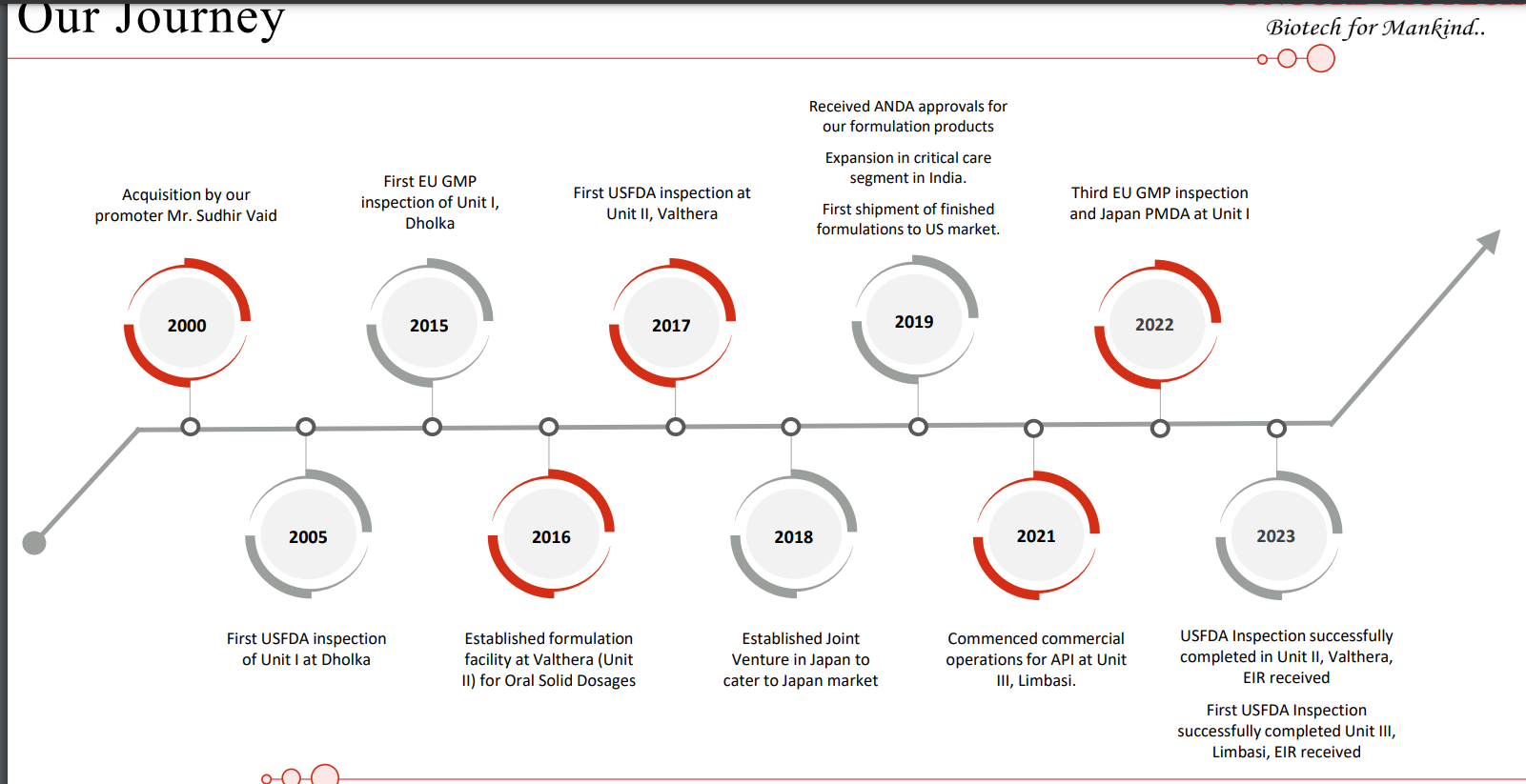

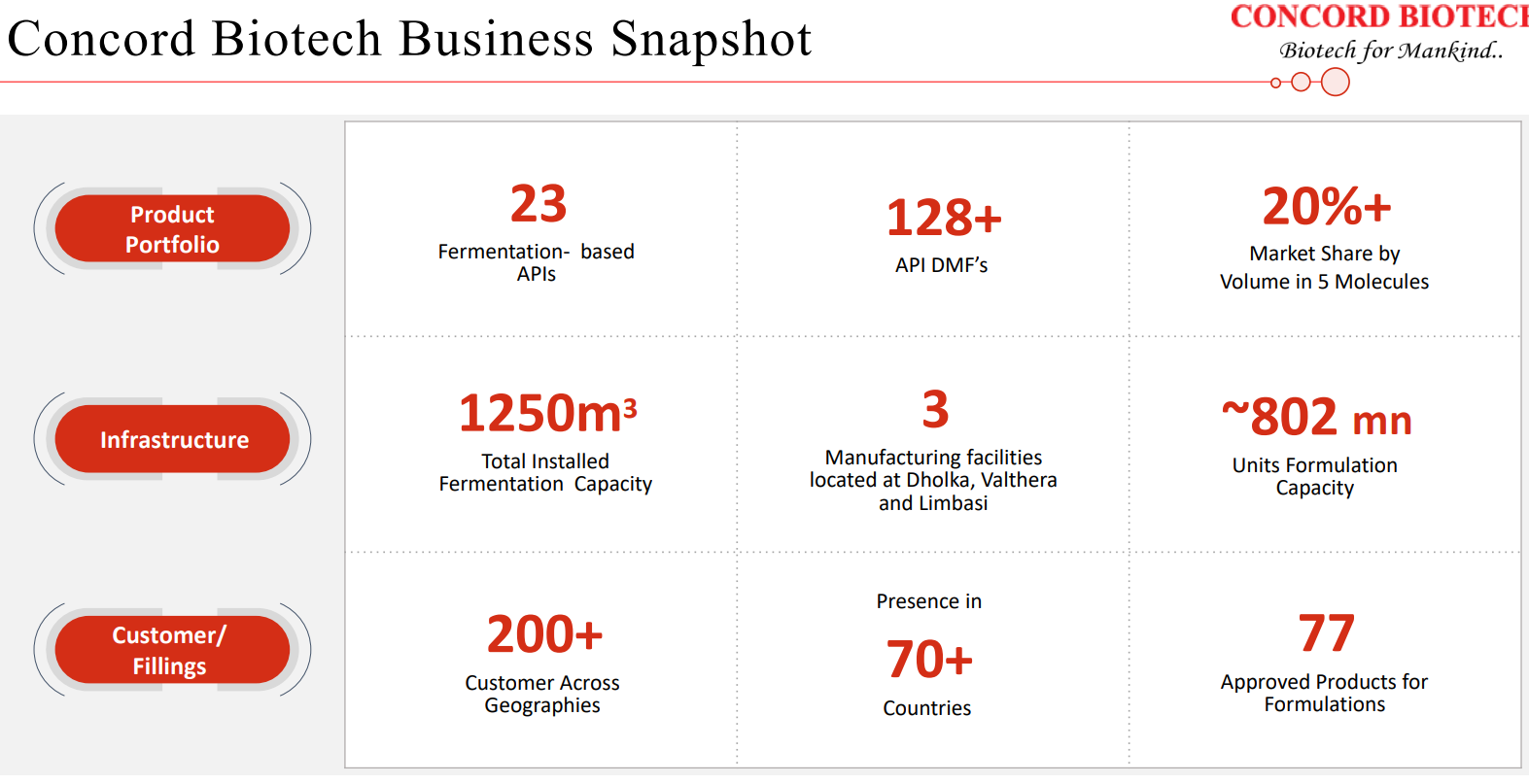

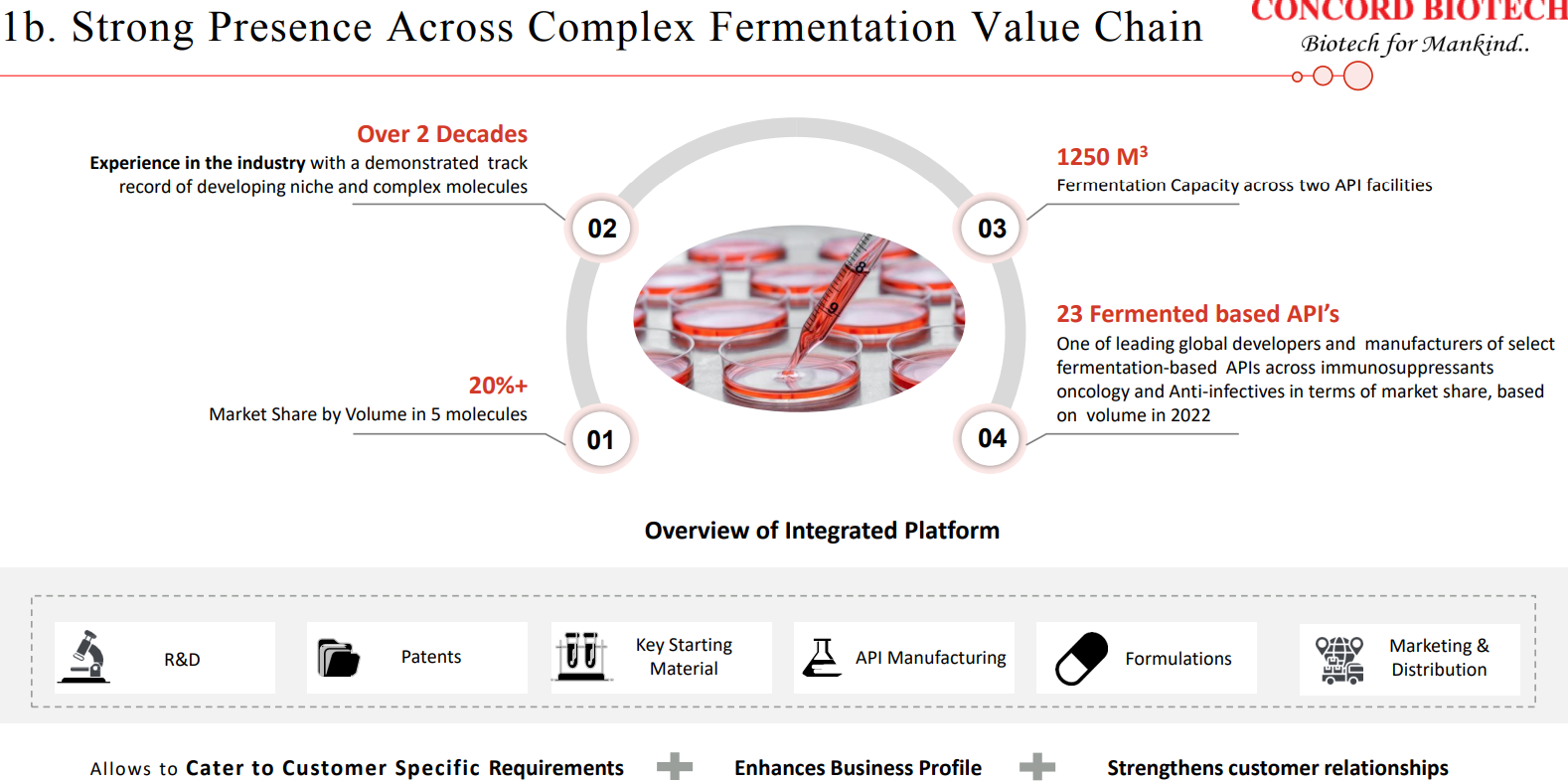

| Initially started with production of enzyme with just one manufacturing block, but with an experienced team of biotechnologists, especially in the field of fermentation. Over the years, company has made remarkable strides and currently operates approximately 41 manufacturing blocks across three manufacturing units, offering a wide range of products, spanning diverse therapeutic areas and segments. | |

| Notably, Concord stands out on the global stage as one of the few companies that have effectively and sustainably established and expanded their capabilities in the fermentation-based API manufacturing. Furthermore, Concord proudly holds the distinction of being the only supplier of a complete production portfolio for fermentation-based immunosuppressants APIs. Fermentation as a core component of our manufacturing process presents unique challenges. It involves the intricate management of microbial strains, the precise control of multiple interconnected processes, and the execution of various purification steps. | |

| The slightest adjustment to this process can yield significant variations in the final output. As a result, this approach stands in stark contrast to chemical synthesis, requiring a highly specific, scientific, and quality-centric approach. As we expanded our market presence in the specialized fermentation-based API industry, we took a strategic step of entering into the formulation business back in 2016. Our Valthera facility was established with the purpose of producing forward integrated formulations for oral solid doses. Over time, we have successfully developed and are now manufacturing products and catering to both domestic and international markets. | |

| At present, our Valthera facility boasts an impressive capacity of approximately 802 million units. Furthermore, as part of our commitment to strengthening our position in the formulation business, we are in the process of establishing an injectable facility. We anticipate that commercial production at this new facility will commence by the first quarter of the next financial year. Over the years, Concord has diligently cultivated its capabilities and an extensive range of products, positioning itself at the forefront of the competition. We have steadily expanded our customer base across global markets. | |

| This strategic approach has solidified our reputation and enabled us to make deeper inroads by attracting additional customers and further penetrating our existing client space. The production of fermentation-based API is inherently complex, making us one of the very few global suppliers capable of manufacturing a comprehensive range of products under one roof. In recent times, the industry has witnessed significant consolidation of manufacturing activities. Several companies have encountered challenges related to the growth on the back of skill shortages, lack of scalability, and a limited product portfolio. This has presented us with ample opportunities to expand our presence in various markets and geographical regions, ultimately contributing to the growth of our revenues and market shares. | |

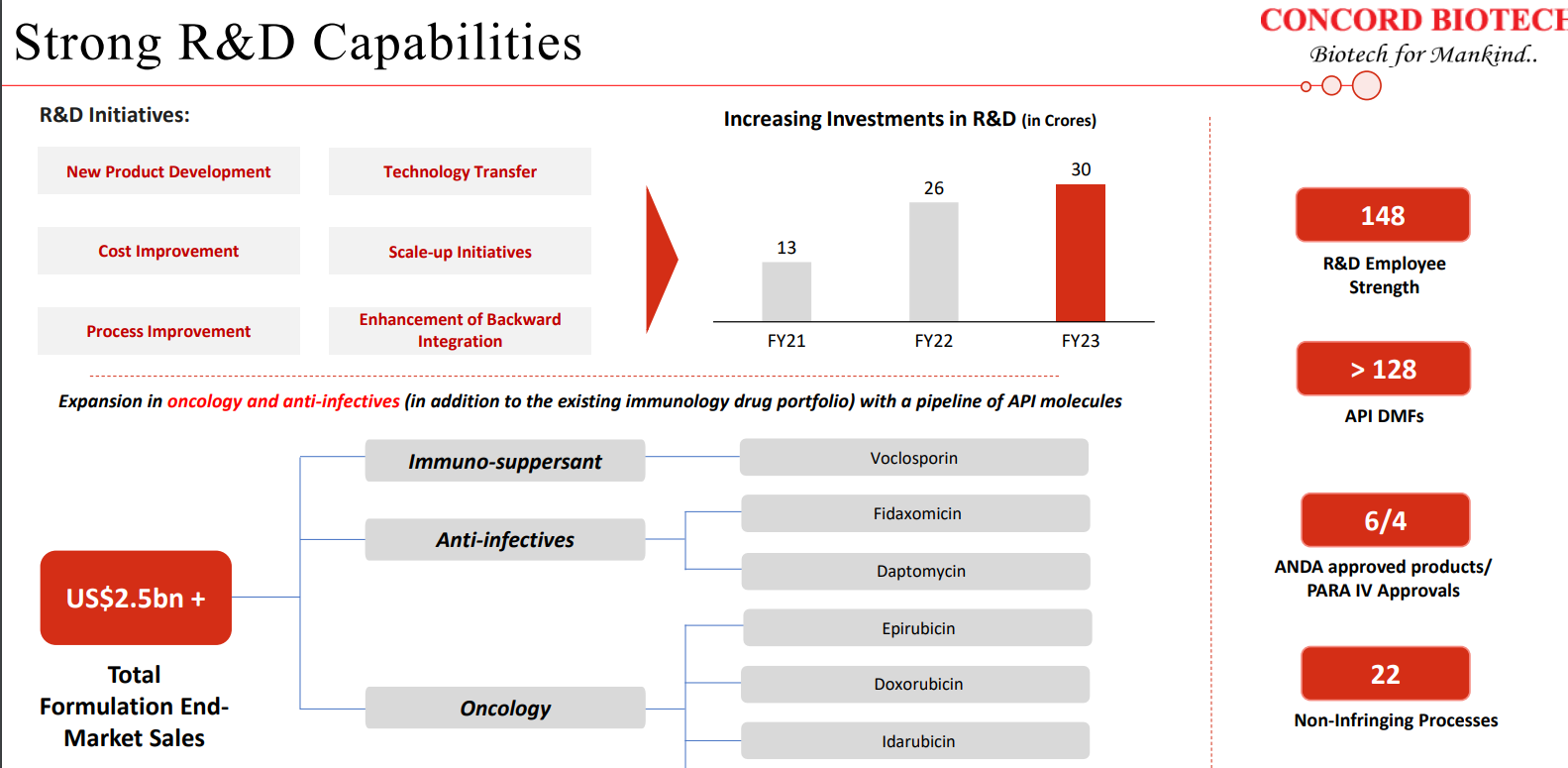

| Our strategic focus is on further expanding our API portfolio across therapeutic areas, especially in oncology, where we currently have 6 APIs for global markets, and anti-infectives and antifungal, where we currently have 7 products. Also, we continue to invest in R&D and have a strong pipeline of products under development across therapeutic areas of Immunosuppressant, oncology, and anti-infectives, which have an addressable market size of USD 2.5 billion at the formulation level. | |

| And this will allow us to cater to the regulated markets. I’m happy to inform you that USFDA authorities inspected our Limbasi facility from 26 to 30th of June of 2023. And the inspection was successfully concluded with zero 483 observations. We now have an EIR report for the same. So with this, customers have now initiated qualification of the Limbasi facility. I would also like to highlight that we have only one manufacturing standard across our facilities, which is followed irrespective of the end markets, be it regulated or semi-regulated markets. | |

| Further, we are in the process of enhancing our capabilities in formulation manufacturing through our injectable facility. Speaking of R&D, in research and development we have set up two DSR approved R&D facilities comprising of 148 members, a significant number of whom had full doctoral qualifications. Our R&D team has showcased its proficiency in moving products, even complex ones, from the R&D stage to full commercialization. | |

| Our product selection assessment encompasses a comprehensive evaluation of factors such as the market potential, competitive dynamics, technical feasibility, and the intellectual property landscape for each prospective product. As of now, we have successfully developed and brought to market 23 fermentation-based APIs with the valuable support of our dedicated R&D team. | |

| With high quality niche products, we’ve been able to successfully add new customers across therapies and geographies over the years. We will continue with our endeavour of adding new customers and increasing in the share of wallet of our existing customers as well. To take you through our strategies going forward, our primary strategy is to continue to increase our market share and develop our portfolio of complex and niche products with high growth potential. API will continue to be the core focus of the business and we will continue to increase our wallet share among existing customers by selling them existing and new products across therapies. | |

| Also, our investments into new manufacturing capacity has enabled capabilities to grow our wallet share from existing customers. Secondly, adding new customers across different geographies with established product portfolio and with the commercialization of new products. Thirdly, increase our presence in existing formulations and add new formulations by adding geographical reach, launching new dosages, and expanding the product portfolio. | |

| And the fourth lever being the growth in the CDMO business. So, with the capacity expansion at our Limbasi facility, the China plus One strategy and given our expertise in the fermentation area, we see this as a growth opportunity for future growth in the company. And the last growth lever for us being the increased utilization of existing and new facilities by adding more customers, and products to be marketed and sold across geographies. | |

| So we have close to around eight to 10 molecules which are there in the pipeline across different segments such as the Immunosuppressants, Oncology, and anti-infectives and one would appreciate that it takes close to around six to seven years to kind of develop the molecule in the fermentation space. And there are products which are at different life cycles within the development, R&D development stage. | |

| But typically, I say that one can expect around one to two molecules that would become commercialized based on our historical trend is what I would point out. But it’ll be difficult to mention which specific product would become commercial because it will all depend upon the market dynamics about the state at which we are with respect to those molecules. | |

| So while, you know, we have been inspected by regulatory authorities, but still, this is a risk that we carry. However, we have a very strong theme of quality, QA, and QC, which ensures that quality standards are maintained on an ongoing basis. With respect to any other risk, I won’t call it a risk, but of course, any changes in the macroeconomic conditions could impact companies in the pharmaceutical space, whether it is through changes in certain raw materials or changes to certain power and fuel costs, which could affect us as it would affect any other pharmaceutical company. | |

| So as we have discussed in the past that our raw materials are usually the basic raw materials which are either agro-based or are the solvents which are typically used in the downstream recovery. And we have close to 150 to 200 raw materials that are being used for different range of products that we manufacture. So there could be an impact of seasonality on the agro-based compounds or as I mentioned due to global changes, which could affect the solvents. But then again, it may affect maybe some of the raw materials because of which there could be an impact, but it could be very, very minuscule because of it being impacting maybe one or two raw materials out of the 150 to 200 raw materials that we use. So the gross margins work in a very, very narrow band, if I would put it. And it is more about the expertise that is needed for the fermentation manufacturing, which makes the differentiation there. | |

| Basically, historically, we have been growing at a CAGR of around 18% in the past for the last couple of years. In the last two years or three years, we have also built-up significant capacities with respect to the API and the formulations. And we expect to increase the capacity utilization and our growth may be better than what we have been doing in the past. So historically, we have been growing at a CAGR of around 18%, so going forward we may improve the growth per percentage. | |

| In fact, in Limbasi, we have invested around INR 400 crores of money in the capex. And with the 450-meter cube of the capacity in unit one, we are able to generate revenue of around INR 600 crores. So with an 800-meter cube of the capacity, you can begin to basically take it nearly to the level of around INR 1,500 crores, INR 1,600 crores of revenue from Limbasi facilities. | |

| Around 75% to 80% will be the right capacity utilization. | |

| So, the injectable project is running on track as we had envisaged, and we expect it to be ready by the end of this year and have commercial production by the first quarter of next year. Given that, the idea would be, the plan is to kind of first take it to the domestic market because the export market is more of a medium term to a long-term strategy for us because, by next year, we take the validation batches, put it on stability, do the dozier filing and get the approval. This is typically close to around 12 months to 18 months of time period. However, we will be going with the same integrated approach, where we have quite a few molecules, where we are the manufacturers of the API, as well as we’ll be going for the forward integration to the injectables. So you do not see many companies having that kind of fully integrated approach in some of these niche anti-infectives also, which are through fermentation. But in terms of timelines, I would say that initially we would start with the domestic supplies and then going forward, they would be, being targeted towards the export market. | |

| So CDMO is definitely an area, which is a focus to us and we now have the capacities in place, we are also building on our regulatory approvals and we have a longstanding relationship with our customers as well. So we are reaching out to customers and working with them to kind of build on the CDMO opportunity. But again, opportunities like these do take their time because customers wanting to evaluate and shift their complete manufacturing to a new site would typically be a time-consuming activity. | |

| So CDMO is definitely an area, which is a focus to us and we now have the capacities in place, we are also building on our regulatory approvals and we have a longstanding relationship with our customers as well. So we are reaching out to customers and working with them to kind of build on the CDMO opportunity. But again, opportunities like these do take their time because customers wanting to evaluate and shift their complete manufacturing to a new site would typically be a time-consuming activity. | |

| As long as it matches these criteria, which we have internally defined, we are not therapeutic diagnostic. So we would be open to look at other molecules across different therapeutic segments as well. It just happens to be that some of the molecules that we are currently under development falls within these three therapeutic segments, which is the immuno, onco, and anti-infectors, anti-fungal. But we are not therapeutic diagnosed to these. | |

| No, so I, as we pointed out that we have growth levers in place for both the API and the formulations. At the API, the new Limbasi facility which will start ramping up and at the formulation level we have ramping up of the oral solid dosage facility and the build-up of the injectable plant. So while the base will continue to grow, we expect the revenue split between the two to be somewhere around 80%- 20% as we have had in the past. So do not expect any meaningful change in the allocation between the two. | |

| As far as the percentage of capacity utilization is been 32% in unit 3 as of 31st of March 2023 and in formulation, it is 10% and in Dholka, it is 75% | |

| So definitely, this will boost our sales to the US as well. But again, this Limbasi facility is for global markets because as mentioned in the past that we are working on close to around 70%, 75% capacity utilization at unit one. So now that we have regulatory approvals in place, this new facility is going to be catering not only to the regulated markets, but for global markets including India and the rest of the world. And newer products that would also come in would also be commercialized at this new site. So it will definitely boost our US sales, but it would also be used to cater to global markets as well. | |

| So I would say that the products which are made through chemistry cannot be made through fermentation and products which are made through fermentation cannot be made through chemistry. So, they are two very different areas of manufacturing. However, we do see moreand-more interest coming within the fermentation space because it creates significant barriers to entry because there are not many global players in this space. So there is a good growth prospect for the fermentation but it cannot be interchanged with the chemistry APIs. | |

| So, you know, Concord holds the leadership position on several of the APIs that we manufacture. The reasons of course are that we have economies of scale, we have global regulatory approvals, strong technical expertise, and offering a basket of products. So we are the only company in the world which actually manufactures the entire range of fermentation based Immunosuppressants. So when you have these kinds of capabilities and strengths, customers look at working with companies such as ours. And that is the reason why we’ve been gaining market share year-onyear basis. And when we talk about that kind of niche, highly complex products, you typically do not see much competition coming from China. As a matter of fact, that we are commercially, we have now got approvals in China to sell our products, our APIs, which shows that, and customers are also showing interest in terms of partnering with us for the API, which kind of shows the kind of advantages and the kind of strength that we have on the API, even with respect to some of the Chinese players. And when we talk about the European counterparts, European competition, people now are talking more about the China Plus One and Europe Plus One strategy because of what is happening at the global footprint with the Russia-Ukraine war, the power costs and other things and the salaries have gone up quite significantly in Europe. And they are looking at alternate sources which are more reliable and can consistently provide them with these kinds of products. So, I think we see a lot of companies shutting down in Europe also and other parts of the world. So, we see a lot of consolidation happening in the fermentation API space. | |

| So basically around 17% of the revenue in the export, or in the total revenue comes from the US market and the balance comes from the rest of the world. | |

| In terms of cannibalization, we are not looking at disturbing the market and we are looking at value creation and opportunities within the formulation space. And that is why while we are backwardly integrated, we would look at opportunities where we can be there in the market but at the same time maintain healthy margins for us rather than going all in and destroying the value for ourselves as well as for our customers. | |

| Annual operational cost for formulation facility is ~35cr. | |

| Most of the capex has already been done as far as the growth capex was concerned. Now it’s only the operational capex which will be required to be done in the future. It will be in the range of around INR 15 crores to INR 20 crores of per annum. Yes, very little amount is required to be spent to complete the project. Majority of the amount has been spent. And yes. | |

| So you know, the prices are more or less quite similar to what you would have across the globe because, while we see limited competition on our molecules, we still are not in a monopolistic market. So when formulation companies are looking at potential suppliers. They kind of evaluate new suppliers based on which is going to supply, and give the best price. So we also have many Indian companies which are targeting the US market and they have a good amount of clarity on what the prices are there in the global markets, including in India being offered by some other manufacturers. So I would say that there is not much of a difference between what the price you offer to Indian versus that to the US. |

Hello everybody, this has been a very insightful thread that has greatly helped me in understanding the business of Phantom.

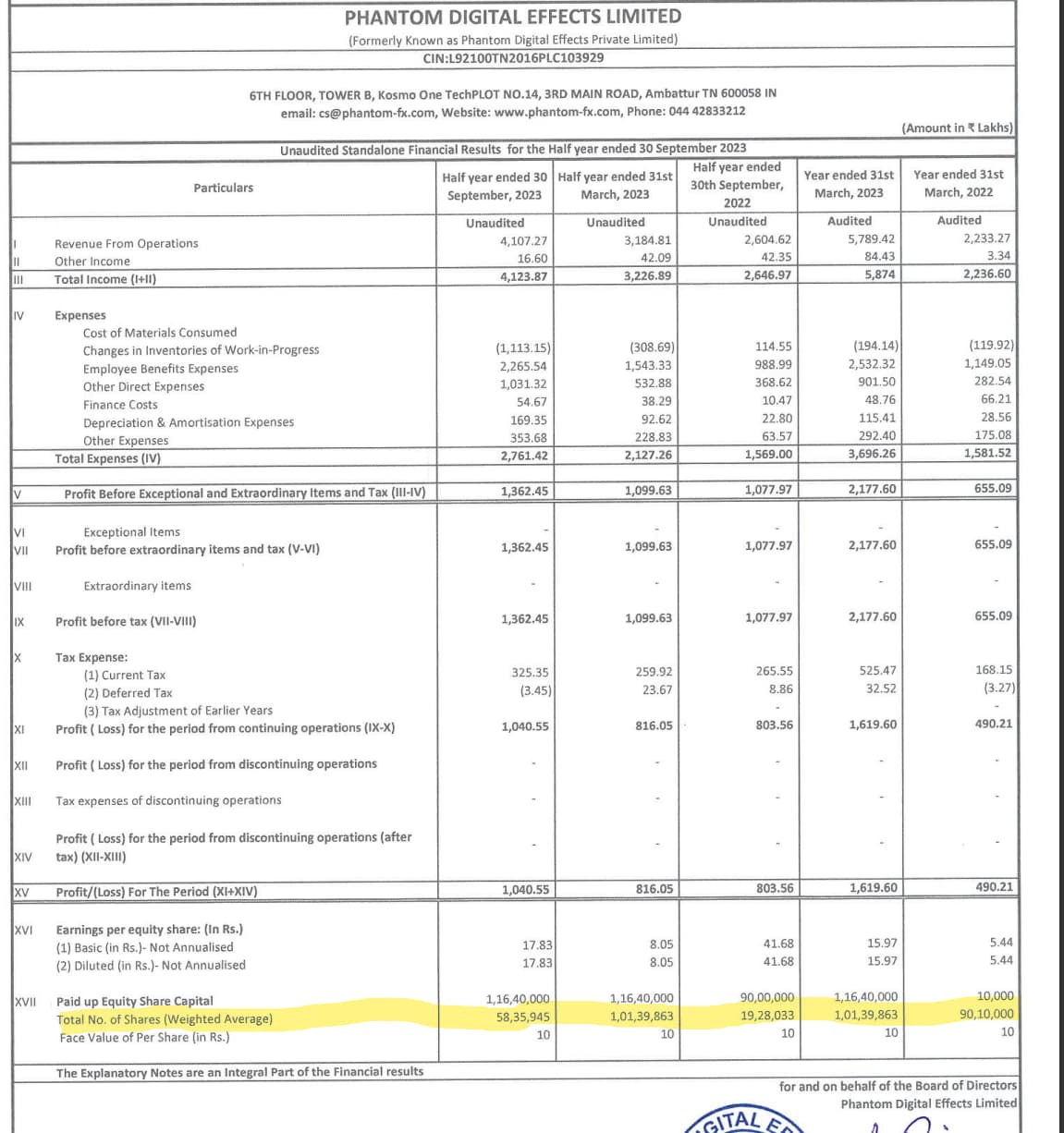

While going through the recent results, it came to my attention that the total number of shares had drastically come down.

Would be really helpul if someone could take the time out and explain what exactly might be the reason for this, and whether it is something to be weary of.

Thank you in advance.

This is your PF, and as such, except for the rationale which helps members know about your views, so that they can give their views, anti thesis I don’t think is necessary per se, unless, of course, if you have found reasons for things going wrong, which can be presented along with your thesis.

This thread may very well work like a journal to your journey, and if you update your activity as per your views, it helps you and might help others too. Work of members who are not active for years is as fresh and relevant as today’s news.

You seem to be getting lost in unnecessary details. If you are learning something new, try to learn basics first and then go into details. I suggest you read a book from first to last page on first reading without getting too deep and on subsequent readings focus on what is important.

Thanks @S.A.B for providing the links to resources.

@Sandeep_Mehta I don’t track cyient.

SRF Q2FY24 Concall:-

Specialty Chemical Business:

Flourochemical Business:-

PFTE Plant :

Pvdf some delay because of land

** fcam and fep** – pretty much online

PFB :

Coated Fabric segment – All time ever sales reported

Laminated Fabric –

Debt increased from 3250 crore in Mar 22 to 3900crore in Mar 23 because of interest rate increase and some because of Capex

Capex

Disclaimer – invested and doing SIP

The Silk Roads, Peter Frankopan, 2015 – This is a history of the world from a non-western perspective. It is mostly focused on the middle-east though as it focuses on the silk roads of trade. I found it to be an absolutely thrilling read. It is amazing how much history repeats and how much of what’s happening today from Suez blockage, oil embargos, freezing of dollar assets of a sovereign, inflation and geographic transfer of wealth has roots and precedence in the past.

The book spends substantial amount of time on the rise of Islam onward though it brushes up a bit on Greeks, Persians, Chinese and Indians before that. I wasn’t aware of all the intricacies that link the Abrahamic religions and how religious fundamentalism is sometimes at odds with the concept of nation state while at other times bolstering it, in cycles. The rise of the West is seen through all the violence and envy that led to it – without any glorification. At times the narrative is like an alien bemusedly observing the goings on

My notes –

Persians owed their success to their openness – they would adopt fashions of a defeated foe if they felt it was superior (Herodotus on why Persians were successful)

For Alexander, as for other Greeks, Europe offered no cities, culture, prestige or reward – culture, ideas and opportunities always came from the East

Alexander conquered territories and left local elites in power to administer them and hence grew fast (like an acquisitive corporation that left culture intact)

Expansion without defense was useless – so Alexander built strong fortification (borrowed from Great wall of China that kept the barbarians of the Steppes out)

Buddhists chose visual representation of the Buddha (as we know now) to keep out cult of Apollo that threatened expansion. Hence Buddha looks lot like Apollo in representation (Buddha would never have approved of this, going by what I read in “Old path, White clouds”)

Gargi Samhita reveres the Greeks for their Astronomy while calling them barbarians otherwise. Ramayana’s theme of abduction of Sita, rescue war and return (written 500-200 BC) was probably inspired by Iliad (1300 BC) and Odyssey (700 BC) where Helen of Troy’s abduction led to Trojan war and rescue. Conversely, Aeneid was probably inspired by Mahabharata

We think of globalisation as a uniquely modern phenomenon, yet 2000 years ago, it was a fact of life

“This province was a byword for grim and fruitless isolation” – Roman soldiers stationed in Britain (how brit it still sounds)

Capture of Egpyt transformed Rome’s fortunes. Abundant grain from Nile valley, made grain price tumble, boosted household spending power – interest rates plummeted from 12% to 4% and led to a surge in property prices

Silk and luxuries from the East made wealth flow from Rome to East (50% of annual mint output in trade with East). Cost of these materials were 100x because of toll collected as it traveled from East to West

As Persia soared (300 AD), Rome teetered – Rome became a victim of its own success – dwindling taxes and burgeoning costs of defending the frontiers and the fiscal deficit led to its eventual collapse

Ideas borrowed, refined and repackaged also flowed along the Silk Roads, alongside goods

Buddhist ideas and practices spread west into Central Asia (stupas in northern Pakistan) and then east through the Pamir mountains and into China (By 5th Century AD Buddhism was competing robustly with Confucianism)

Christianity spread along trade routes and hardened and radicalised Zoroastrian philosophy (by merchants from Syria to Persia – modern Iran)

Christianity though led from Rome and Constantinople (Istanbul) was born in Asia, its geographic and spiritual focus point Jerusalem, language Aramaic (semitic group), its theological backdrop and spiritual canvas Judaism – stories of floods, droughts, famines unfamiliar in Europe were shaped by Judaic influences from Egypt

Constantine converted to Christianity and brought the religion to Europe – and Roman identity and Christian identity became one – this led to disastrous consequences to Christians living in Persia as the Shah persecuted them

Persia and Rome formed a historic alliance in 395 AD to keep out the barbarian hordes from the Steppes – Christianity hence made strong inroads into Asia – bishops appointed from Persia oversaw Christians in Sri Lanka for eg. In middle ages, there were more Christians in Asia than there were in Europe (Islam was barely being both in 7th century)

Religions strongly borrowed from each other during this period – halo became a visual symbol in Hindu, Buddhist, Zoroastrian and Christian art as link between earthly and divine for eg.

Cave temples became well-established way of evoking strong spiritual messages and superiority along trade routes – Bamiyan caves in Afghanistan with Buddha statues (751 caves, most destroyed by Taliban in 2001) and Ajanta and Ellora caves

In 541, Bubonic plague wiped out entire regions – 10000 people killed each day in Constantinople (Istanbul)

Turks (nomads) rose in 6th century and became strong controlling trade routes (annoying the Chinese) – they proposed that Constantinople attack Persia with them (this infighting is what broke Rome-Persian relations). Extinguishing of Zoroastrian sacred flame effectively broke Rome-Persian relations. Turks never trusted Romans (felt Roman spoke with ten tongues) – This sounds pretty much like a modern World War

The Shah took over Jerusalem in retaliation with the help of Jews (how unlikely this sounds today) and this pissed off the Romans. Remember that by this time, Islam is not born yet (Prophet Mohammed had barely begun to receive revelations from God by 610) and Zoroastrians and Christians lived together in Persia. Now the Roman fight against the Persians was nothing less than a fight to defend the Christian faith

Romans appropriated Christianity and effectively called Persian centered Christianity as Eastern Christianity and drove them out or convert them to Roman, western Christianity (it is amazing how religion and state ideologies merged or repelled over time)

Mohammad wasn’t the only figure talking to God around this time – there were several prophets promising revelations from the angel Gabriel (remarkable similar) even as Churches started appearing around Mecca – competition for hearts, minds and souls was fierce in this region around this period

The religious wars sucked up capital and trade in the region collapsed – the Prophet preached a doomsday scenario that fell on fertile ground. Enemies of Mohammad were enemies of God he proclaimed. The conservative elite of Mecca who supported traditional polytheistic practises and beliefs (would be called “left” today) opposed this ferociously and Prophet fled to Yathrib in 622 (today’s Medina). This is year zero in Muslim calendar

The Prophet united various tribes who were deprived of the 30 pounds of Roman Gold from the now collapsed trade and gave them their own identity and faith (let there not be two religions in Arabia were his last words)

The faithful were to pray facing Jerusalem – this was corrected in 628 (proclaimed as a test) and the direction was changed to Mecca. The ka’ba was old focal point of polytheistic, pagan practises – this was appropriated into Islam to ensure continuity – this was revealed as having been set up by Ishmael, the son of Abraham the putative ancestor the 12 Arab tribes (pure genius)

Islam took advantage of the fall of Persian empire and took over territory – evangelical zeal was vital to its early success. Loot from non-believers was to be kept by the faithful. The booty was shared innovatively – early adopters were rewarded with proportionately greater share of the prizes like a pyramid system or mafia (again pure genius)

When Mohammad was cornered in Yathrib, one of his key strategies was to take the support of the Jews – followers of both religions pledged to co-operate and defend each other from Rome / Christians

Conciliatory tone in Quran – believers of Jewish and Christian faith believed in same God. Mohammad’s revelation had been revealed to Abraham and Ishmael, to Isaac and Jacob, Moses and Jesus- the prophets of Judaism and Christianity are same as those of Islam (Cohabitation was important for its early success)

Converting Christians was no the most important goal in the 7th century – keeping rival factions out was. The ones that knew most about the Prophet’s early life claimed dominance – effort was to move religion away from Mecca into Jerusalem (isolating southern Arabian traditionalists) – Shia and Sunni split happened within a generation of Prophet’s death

Christian scholars felt Islam was just a divergent interpretation of Christianity and not a new faith as it was so similar

Shipwrecks disappear from 7th century onward – a good indicator of disappearance of trade

Arab world thrived intellectually with works imported from India and from Egypt – mathematics and astrology did well. Meanwhile St. Augustine felt men want to know for the sake of knowing and curiosity was nothing more than a disease – science was defeated by faith. Christians were in intellectual backwaters

Merchants from Scandinavia – the Vikings set off on a journey south to trade with Islamic world – These men were known as “Rus” or “rhos” – the forefathers of the modern Russians

The Viking Rus’ had no cultivated fields and lived by pillaging – their captives, the ‘Slavs’, their slaves (fathers of slave trade too) – height of Roman empire needed 250-400k new slaves each year

Rus’ ruler Vladimir adopted Christianity in 988 (influenced everything from the way they dressed and traded)

In 1099, Jerusalem fell to knights of the First Crusade – Muslims were expelled from a city they controlled for centuries – Middle East was being recast to function like Western Europe (crusades were in response to inability of Christians to travel to Jerusalem – and also the lure of riches of the Arab world). Jews in Jerusalem felt it was better to be ruled by Christians than the Shia or Sunni factions

Jews were butchered in Rhineland (Germany) as the idea took over that Jews were responsible for Jesus’ crucifixion and the lands of Israel should be held by the Christians of Europe – (anti-semitism has had deeper roots in Germany)

In 1187, Saladin (of Egypt) overthrew the Crusaders and Jerusalem once again fell into Muslim hands. Joint efforts made by the kinds of England, France and Germany failed between 1189-1192

Mongols, under Genghis Khan trampled through most of the world in the 12-13th century – cultivating terrors and fears so as to use violence selectively and deliberately (most surrendered without a fight, knowing their barbarism)

Mongols, though portrayed as barbaric destroyers were far from only that – they invested heavily in infrastructure of cities they captured – Samarkand being a prime eg. or Beijing. They captured regions from Baghdad to Syria, Poland Hungary heading deep into France

The crusades established the power of the church over Europe. The crusades though failed miserably and Jerusalem was lost for good – it was all too expensive and dangerous to capture and hold it (far easier to build a Jerusalem in the English pastures)

Mongols controlled transport through the Black Sea and extracted not more than 3-5% tax – whereas taxes through Alexandra during the time were 10-30% (Mongols weren’t rent-seekers). Tolerance and careful administration backed up by military might

Russian autocracies later on were a natural byproduct of Mongol system of govt.

Black Death – spread rapidly in 1340s and took most of the population of Europe, Iran, Middle East, Egypt and Arabian peninsula. 90% of the population was wiped up in a most places

The plague redefined Europe and led to its rise – wages went up as labour was in shortage – the lower end of the social and economic spectrum rose as a result. Life expectancy went up sharply (survival of the fittest)

Rise of European art – Leonardo da Vinci, Michalangelo, Raphael owed a lot to rising disposable incomes and the availability of pigments from the east

Global financial crisis of the 15th century – aka bullion famine – arose out of Europe’s inability to pay for goods (fabrics, ceramics, spices) it brought from the east, esp. China – which was producing more than it could consume – leading to oversaturated markets, balance of payments crisis and currency devaluations (and we think these things are modern creations)

Chinese govt. (Ming dynasty) spent on the assumption that revenues will only increase so a credit crunch hit in 1420s as some of the richest parts were struggling to meet their obligations – Europe debased currency and precious metal supply wasn’t enough to go around

Global cooling in 15th century, triggered famines in Steppes and floods in China and the resulting drought had widespread ramifications – in 1453 Constantinople (Istanbul) fell in a triumph for Islam (Many Jews moved to Constantinople in this period as the new Muslim rulers welcomes them – Jews seem to have felt closer to Muslims around this period)

In a span of 6 yrs in the 1490s, Columbus crossed the Atlantic onto America and Vasco de Gama navigated around Africa on to India (both had same goals) and Europe became the fulcrum between East and West (Near, Middle and Far East definitions arose here)

Rise of the west was built on the capacity to inflict violence on a major scale. They conquered Muslim territories in Africa, converted mosques to churches and undertook slave trade under the sign of the cross

Aztecs, Incas and their silver and gold was plundered by the Spanish. Within few decades of Columbus, indigenous population fell from half a million to little more than 2000

Spain became powerhouse of the world – rise in wealth in one of the world meant demand for slaves in another part (Portuguese were hardened slave traders)

The wealth of the Americas made Europe richer than they hoped to get through the recapture of Jerusalem. Legacy of Rome and Greece was claimed with gusto by France, Germany, Austria, Spain, Portugal and England when in reality they had little to do with legacy of ancient Romans and Greeks

Portuguese reached India (da Gama) and mistook temples with Hindu Gods adorned in Gold to be Christian saints (hilarious). Venice which controlled land routes was worried Portuguese could squeeze their margins through the sea – in reality sea was treacherous (50% of ships only made and the rest sunk with precious goods)

Portuguese sought to control every port from Europe to India and ransacked, captured ports and burnt ships (one ship having indian muslims returning from Mecca was burnt by Vasco da gama) – they met their match in Ottomans who sought control as well

Ottomans ended up controlling Red Sea, Persian Gulf and the Mediterranean – coffers at Constantinople swelled and they spent it building mosques, madrassas, hospitals, bridges, warehouses and other infra in modern Turkey

Trade with Europe brought sudden influx of hard currency into India (early 16th century) – most of which was spent by Indian prices in buying purebred Persian and Arabian horses from the steppes – for prestige and social standing – not unlike oil-rich states buying Ferraris and lambos

Babur, his son Humayun and his grandson Akbar expanded the Mughal empire from Gujarat to Bengal, from Lahore in Punjab deep into central India (16th century)

1571 founding of Manila by the Spanish, enabled flow of goods from Asia to Americas through the Pacific instead of the Atlantic via Europe for the first time – changed global trade forever – route via Manila led to contraction of the Ottoman expire

Lots of American silver made its way to China through Manila for Chinese goods – China having used Silver as its currency, experienced devaluation and a serious economic and political crisis under Ming dynasty in 17th century

England (being Protestants) forged unlikely partnerships with anyone who would side with them against Catholic Europe (specifically Spain) – from Persians to Ottoman Turks. English were scavengers for whatever crumbs will come their way (16th century)

Spain’s inability to control military spending led to it failing to meet its obligations 4 times in the 16th century (not very different from US now)

Competition and military conflict were endemic to Europe. Its art was forged by violence and its not surprise the greatest genocide in history had its origins in Europe

Qur’an about legacies – a Muslim woman could be expected to be looked after better than her European peer, since she would inherit her share of wealth. This led to redistribution of wealth (and inhibited growth), unlike in Europe which led to large income inequality (and growth)

East India Company behaved like a quasi arm of the state – a position, even a lowly one in it was the way to riches. Elihu Yale started a writer but returned with large quantities of diamonds, precious jewels and 5 tons of spices – the donation from this loot led to renaming of the collegiate of Connecticut as “Yale university” (disgusting)

While European mainland squabbled over everything and spent heavily on military, England protected by its waters, spent very little and became very prosperous

The wealth led them to gentlemanly pursuits of fencing and dancing and choosing tailors. Willian Pitt, the governor of Madras brought back a large diamond (Pitt diamond), bought a country estate and a parliamentary seat with it

East India company shifted from a mercantile power to an occupying power – shift to drug-dealing (Opium in China) and racketeering was hence seamless. Robert Clive became the richest man in the world helping himself to the treasury at Bengal, even as a third of the population dies in the Bengal famine in 1770

The loss of manpower in Bengal from the famine, led to devastating loss of life and productivity and EIC shares plunged prompting a run on it, pushing it to brink of bankruptcy and bringing the intercontinental financial system to its knees

EIC was too big to fail and was to be bailed out with American tax – when Britain raised taxes on tea – it led to Boston tea party and ultimately to American independence and Britain lost America as a result (it would do anything to retain India though)

Britain had weakened throughout the 19th century as Russia posed a threat to Britain’s control of Asia (through its relentless expansion into Central Asia) and Britain gambled away its entire fortune on the outcome of WW-I as a result

Napoleon was also plotting to conquer Egypt and also to dislodge British from India in 18th century (rumoured to have written to Tipu) – so when Napoleon attacked Russia, British sided with Russians (enemy of enemy is a friend, even if he is also enemy?), much to the chagrin of Persians (who were wary of Russian expansion) – World wars have been common even before they have been called as one

Russia stretched not just towards Near East and Europe but towards North America, across the Bering Sea (Alaska) in the east – hence Britain wanted to limit Russia around 1820s. They were also worried Russia was pushing Persia to invade Herat (Afghan) to pave a way into India, the British crown jewel – hence Britain intervened in Afghanistan. Chechen terrorists were also funded by British.

To dismember Russia, Britain even handed over Crimea and Caucasus region to Ottomans. Crimean war was fought between Russian Tsar and the allied forces – Ottomans, Brits, French (all 20th and 21st century wars have deep roots in the centuries prior. Current Crimean annexation by Russia is merely payback for loss in the Crimean war)

Trans-Siberian Railway was Russia’s own Silk road and connected with Chinese Eastern railway – trade boomed between 1895-1914 with Russo-China bank (strong history of past co-op between the two, as today)

Opium wars – wars between China and Britain (and France) to gain access to free trade that led to century of humiliation for Chinese (and ceding of Hong Kong)

Britain wanted to divert the attention of Russia towards Europe (so it could maintain its eastern stronghold) – France was meanwhile threatened by German economic growth (1970s) – so France worked to build an alliance with Russia in 1890s (grossly simplifying as I understand it)

Britain’s ultimate nightmare scenario in 20th century was an alliance between Russia and Germany (Britain and France were very worried by German growth)

Germany was hated in popular culture in 1914 as books about German spies and German plans to take over Europe were commonplace (driven by British and French envy?)

Britain wanted to align with Germany to counter Russia and wanted to align with France to counter Germany in a nightmarish game of chess where all possible moves were bad ones (and led to WW-I)

WW-I – The story in public consciousness is that of German aggression fought by Allies in a just war when it was one of envy. The redress and reparations demanded from Germany by Britain was exploited by a skilled demagogue that laid the seeds for WW-II

Britain went from being the world’s largest creditor to being its largest debtor post WW-I (victors only in name). This led to a large redistribution of wealth – discovery of Americas led to wealth flowing from America to Europe – now it flowed in reverse as war bankrupted the old world and enriched America

When Anglo-Persian Oil (BP) company was setup (1909) – It was felt that the British cannot say what they mean and they Persian did not always mean what they said – so what Brits saw as a contract was merely an expression of intentions to the Persians (hilarious)

Knox D’Arcy’s concession (to drill for oil in Persia) is as significant as Columbus discovery of America (both led to large scale expropriation of wealth)

Sykes-Picot line – French would keep Syria and Lebanon and British Mesopotamia, Palestine and Suez (Southern Israel, Palestine, Jordan, Southern Iraq). Brits got Suez Canal, Haifa port and oil fields in Persia and Middle East (Laid seeds for all future wars in the region)

Britain installed reliable strongmen who would serve their interests well in 1915 (Power of Iranian religious fundamentalists rise from this)

Balfour Declaration – Concerned with the rising levels of Jewish immigration into London, Britain wanted to establish Palestine as the home of the Jewish people (seeds for current Israel – Palestine war). Jews from Europe migrated to Palestine. Lord Rothschild played a strong part in this (hence the West’s protection of Israel to this day!)

Women from Kyrgyz, Turkmen, Ukrainian and Azerbaijani republics had voting rights before women in the UK did

Creation of Iraq was a hodgepodge made of former Ottoman provinces profoundly different in history, religion and geography – Basra (towards India and Gulf), Baghdad (towards Persia) and Mosul (towards Syria and Turkey) – this helped Brits shape the land to suit its needs

Tehran considered America as more British than the British – worshippers of gold and stranglers of the weak (when Standard Oil got a 50 yr concession). America literally took over from the Brits when the latter was too weak financially to carry on its imperialism after WW-I

“Complete independence is never given – always taken” – Iraq’s view of dealing with the British control In early 20th century

Britain gave assurance to Poland to assist it if Germany invaded it after German occupation of Czechoslovakia in 1939. Hitler played an ace when he stuck an alliance with Soviet Union and both of them invaded Poland – all this despite trade collapsing from 50% to 5% imports from Germany to Soviet Union after Hitler got elected (he hated the Soviets)

Ukraine was the bread basket Germany eyed, after having been locked out of food and fuel in WW-I (Hitler’s obsession) – Ribbentrop-Molotiv pact let them access to Ukraine wheat and Russian oil to fuel their WW-II ambitions (Stalin was fueling Hitler’s war)

Britain and France were caught cold by German-Soviet co-op. Britain’s oil interests in Iran and Iraq were severely threatened

Hitler’s harking back to semi-mythical golden age playbook and purification was adopted by Persia too when it changed its name to Iran and purified its language of certain words (strange how this playbook still continues to be played everywhere still)

When Stalin starting reneging on deals made on wheat and oil, Hitler lost it and invaded Soviet Union (dressed up as an ideological battle of course – to eliminate Bolshevism). He saw Soviet Union as producer (Ukraine and Caucasus) and consumer (Belarus and Baltics) – he wanted to cut Ukraine off and take its produce for feeding his massive army (Kiev was taken in < 6 months)

British rule in India was often cited by Nazis on how large-scale domination could be accomplished by a few people

Britain and US sought to strengthen the Soviet Union against Hitler (an alliance unimaginable today). To get armaments into the Soviet Union, the only way to take control of Iran – so BBC Persian radio service falsely accused the Shah of removing Crown Jewels from the capital (BBC’s long history of manipulation)

Plans for “phased withdrawal” from India to protect Muslim minorities was rejected by London as too costly and too lengthy

Britain sabotaged ships headed to Palestine with 4000 Jews (holocaust survivors) so that they could maintain friendly relations with the Arabs and retain Haifa port and keep Suez secure

After WW-II Stalin’s role in the war’s genesis (alliance with Hitler) was quickly forgotten and replaced with story of triumph and destiny – Communism was all set to sweep the world as Islam had done in the 7th century (Stalin blamed WW-II on modern monopolistic capitalism)

Early 50s America funnelled “aid” to Iran (which it helped destabilise) to create a client state by propping by regime (and regime changes) – continuing Britain’s imperialism. “Oil in this region is the greatest single prize in all history” (report to US state dept.)

Oil in Persia was British, Bahrain and Saudi was US’s while Iraq and Kuwait would be shared between the two (Roosevelt’s plan)

Fear of Soviets and Communist influence is what made the west renegotiate revenue share with Arabs in favour of local rulers and governments (Why US hates communists so much)

Brit solvency depended on Iran not going commie. When Mossadegh was chosen as PM, he passed a law nationalising Anglo-Iranian (with support from Ayatollah Kashani, a populist cleric). Britain imported embargo on Iranian oil (origin of oil embargo perhaps). When this didn’t work, they set to work with CIA for a regime change (a repeat-use playbook)

Mossadegh is the spiritual father of Ayatollah Khomeini, Saddam Hussein, Osama bin Laden and the Taliban

Posturing about democracy while sanctioning and orchestrating for regime changes made for strange bedfellows

In 1956, Egypt’s Nasser (taking up where Mossadegh left) scuttled ships and barges in the Suez canal and effectively close it causing serious dislocations in commodity movements, esp. oil to Western Europe (Covid Suez blockage has good precedent). This led to rise in Arab nationalism

If cheap Middle East oil was denied to British, our gold reserves would disappear in 2 years and sterling would disintegrate and we wont be able to pay for defence (senior Brit diplomat after Suez blockage). Eventually Britain had to turn to IMF for assistance

Israel became a focal point for Arab nationalists to rally around, just as Crusaders had found in the Holy land hundreds of years earlier (dont be surprised if Middle-east unites against Israel today as well)

Iran was funded with US military aid and soft loans from the US to short up defence against Communism – Iran’s military spending rose from $293 million to $7…3 billion in just 15 yrs – as a result Iran had one of the largest army and air force in the world

Forming of OPEC for the first time took care of the producer interests from the west’s interests of providing cheap and plentiful oil to their domestic markets

USSR supplied 3/4ths of all armaments New Delhi procured from abroad in the ‘60s. Soviets cultivated Iraq and India and also several others. MiG-27 and MiG-29 manufacturing licenses were given to India while being denied to Chinese (Soviets have history of being friendly to India)

Iran’s revenues rose 8x and, in a decade in the ‘70s, govt. revenues rose 30x. Iraq’s was 50x between ‘72 and ‘80 from $575m to $26b (we know 70s as the decade of inflation – thats from the western perspective)

Yom Kippur war (’73) had Arab world united, almost like a caliphate against Israel (led by Saudis). Costs per barrel tripled overnight as oil was weaponised (prompted US to invest in electric cars, renewable solar and wind power)

Middle East alone accounted for 50% of global arms imports in the ‘70s. Iran alone it went up 10x leading to ‘78 (all the oil money was spent on defence). Since it was good business, no hurdles were put up

Iranian revolution led to the overthrowing of the Shah by Ayatollah Khomeini. US lost its ability to keep an eye on USSR from its Iranian listening bases which drove the US towards co-operation with Chinese military and intelligence for the same (and a subsequent rise of China economically)

USSR got access to military secrets from the Iranian US embassy as US left the country in a hurry without shredding docs when it was shutdown by the Ayatollah (Iranian revolution benefitted the USSR hugely)

US announced an embargo on Iran oil in ‘79 to keep Khomeini in check and froze $12b of Iran assets (exactly what it did post to Russia post invasion of Ukraine). Embargo was anyway useless as oil always found its way around it and reached US (Same is true today with Russian oil)

By end of the ‘80s, Iran, Iraq and Afghanistan lay in the balance – Saddam Hussein rose up in Iraq thanks to the big bet by US as a counter to Iran. Iran needed spares for its US arms which it got through Israel – much as the Ayatollah despised jews, Israel hated Saddam more and was partners with Iran (how strange this is today). US played all sides (not strange at all)

China resisted USSR’s expansion and trained its Uighur Muslims to become Mujahidin and supplied Afghanistan with arms to defend itself against USSR (Uighur radicalisation was again a failed Chinese ploy as it came to regret it later)

Saddam was shocked in ‘86 when US had sold arms to Iran (called it a stab in the back). All the mistrust Middle East has towards US comes from decades of poor US policies in the region

In ‘91 when Gorbachev resigned as President of Soviet Union and announced dissolution of USSR into 15 independent states, the cold war was won by US

When Osama bombed US embassies in Tanzania and Kenya and Taliban refused to give him up, US undertook strikes that killed Afghan civilians and hardened anti-US stance in the region. Afghans insisted that the US speak to Saudi to cut off Osama’s funding (which US refused to do)

9/11 changed the way US engaged with the world as a whole. They wanted new regimes in Afghanistan, Iran and Iraq. Engagement in Iraq and Afghanistan alone is estimated to have cost the US $6 trillion or 20% rise in US debt between 2011 and 2012 (seeing GFC as one of making of the banks is very narrow-minded – everything goes back much further)

Use of energy, resources and pipelines as economics, diplomatic and political weapons would be the order of the 21st century as Kremlin backed Gazprom controlled most of energy to Europe (Putin’s PhD was on this)

I haven’t gained this much useful perspective on the goings on from anything else I have read in the past. History wasn’t a subject I particularly liked in school (I was a math and sci guy). I feel some things should be read when we are ready and not forced down. If you are curious about the world today and want something that’s epic in scope, this is the book to go for as my notes barely do justice. 11/10

Here is the answer.

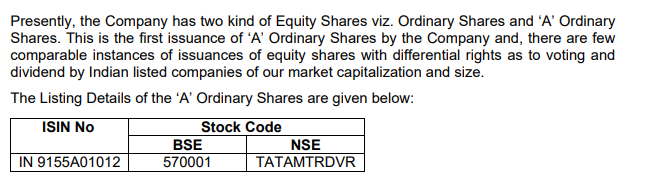

“A” Ordinary shares are nothing bus DVR

So DVR holders are eligible in 10% reserved category.

Thanks, updated. Is Anti thesis mandatory? I don’t want to put some bias in other VP member’s mind, and want their fresh inputs.