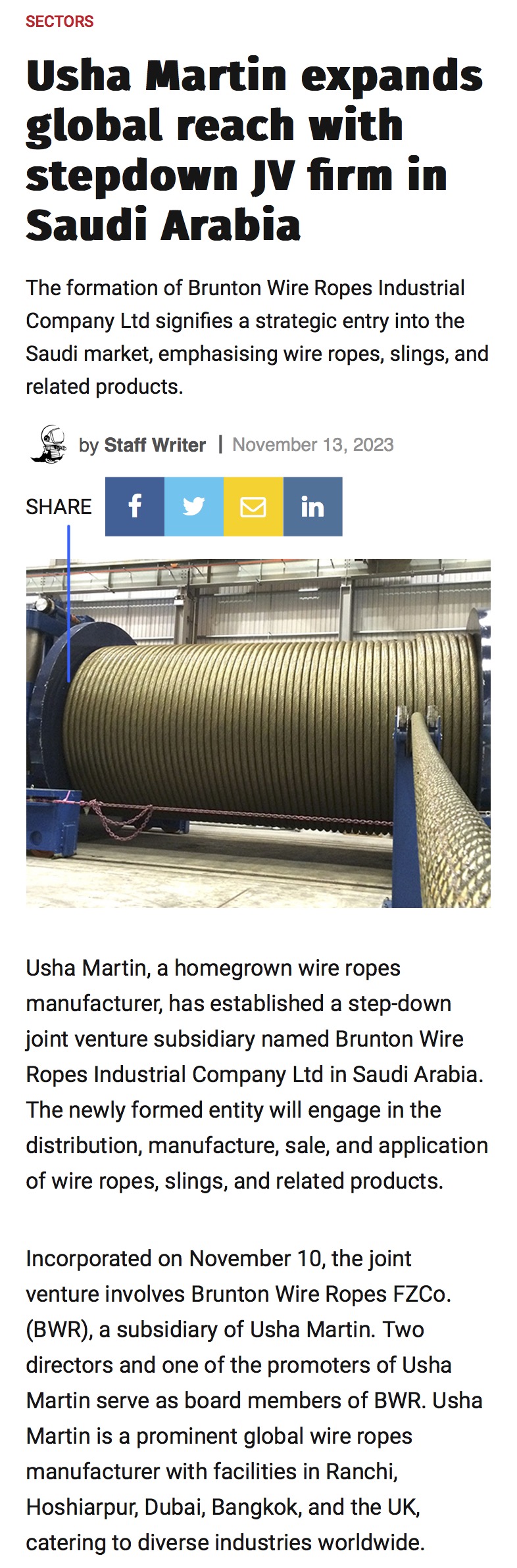

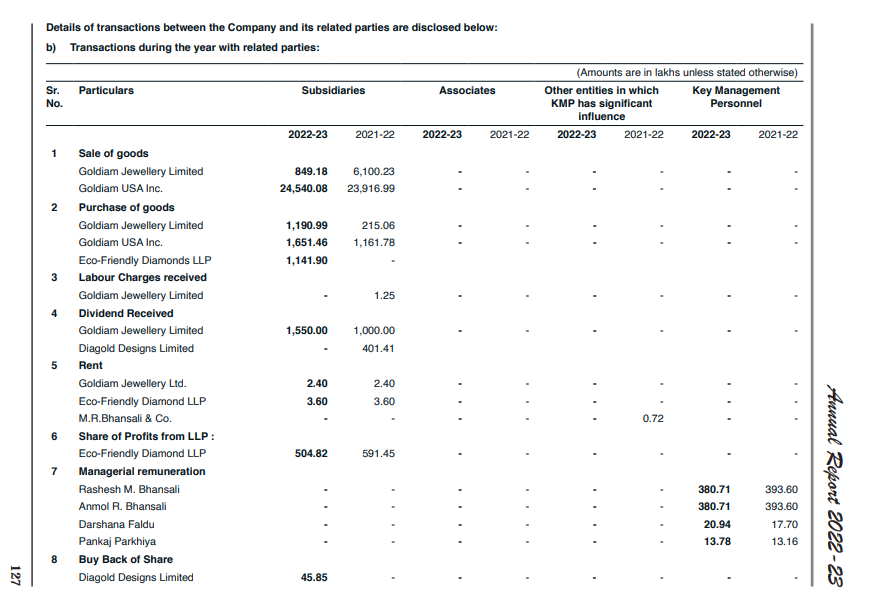

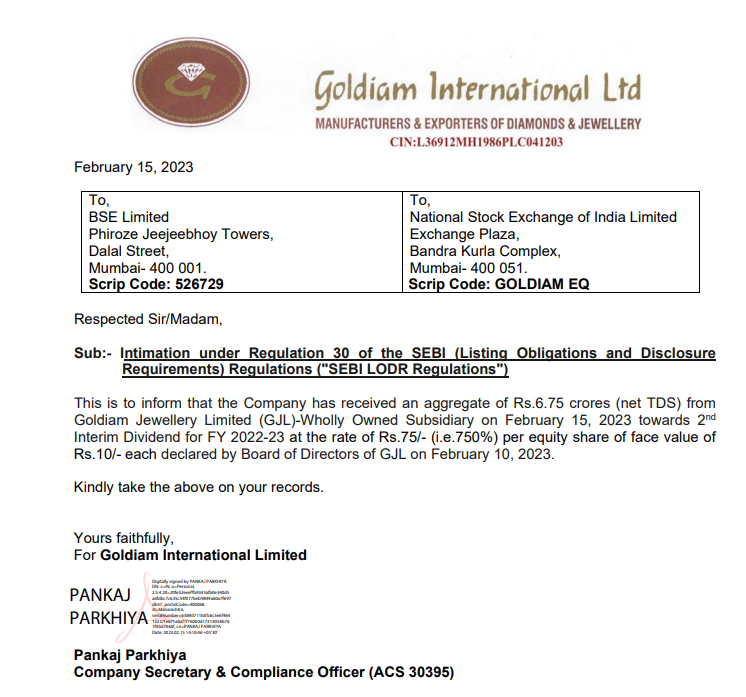

FY 22-23 total dividend received was 15.50 CR…

1 ST Dividend of 8.75 Cr and 2nd of 6.75 Cr…

So 1st dividend this year of 11.52 Cr significantly higher than last yr of 8.75 Cr…

Is this any kind of harbinger??

FY 22-23 total dividend received was 15.50 CR…

1 ST Dividend of 8.75 Cr and 2nd of 6.75 Cr…

So 1st dividend this year of 11.52 Cr significantly higher than last yr of 8.75 Cr…

Is this any kind of harbinger??

A company where the product mix is changing to a premium product with capex going on as well –

Steel Strips Wheel Ltd

Forum’s thread is very useful – Steel Strips Wheels Limited – Attractive Valuations

Hitesh Sir I came further in the book 5 rules of successful investing. I want to ask what is 10-k filing equivalent in India where I can analyse the management like how many salary bonuses they are taking?

Also I did not understand “the company capitalising it’s cash flow generating asset or expense it” (I read it multiple times though, Googled it also.)

Can you please explain this concept to me with example and how does this affect the companys prospects.

There are number of ways one could do that, because learning is not the same for everyone. One can start with the traditional way of learning through books way to have good understanding about the overall structure of the markets, businesses, concepts, as books are detailed, focused works. If you already have some idea, then you can watch videos to know how some concepts actually work. We can also get some broad understanding from reading articles which explain different concepts, or spend time in forums like VP and read what intrigues you.

Learning can be structured like learning alphabets, words, and then sentences, or we can learn in bits and pieces and try to put them together. It can be done concept by concept, or getting a broad understanding about various concepts, enough to start go forward, if we want to go forward soon, and the learning continues.

Deep understanding is the next level, as the word says, we can go deep only when he have good understanding. Can we talk to the governor of RBI right after getting a job in the bank? I am guessing not.

Business models could be different for different companies even if they are in the same industry. A company’s business model can be different if the management wants to do things differently, if the nature of the business permits.

Choose an option which suits you, there are many many ways to do this, but no matter the option, all of this takes time, if you are now. And there is always some evolution, as there are new things to learn, or we look at things in a different way as we gain experience. It will take time to settle down with a certain philosophy and process.

Here are list of books from Dr. Hitesh, if you want to go the books way.

I am in learning phase too, so take the essence of what I am saying, and choose your own way.

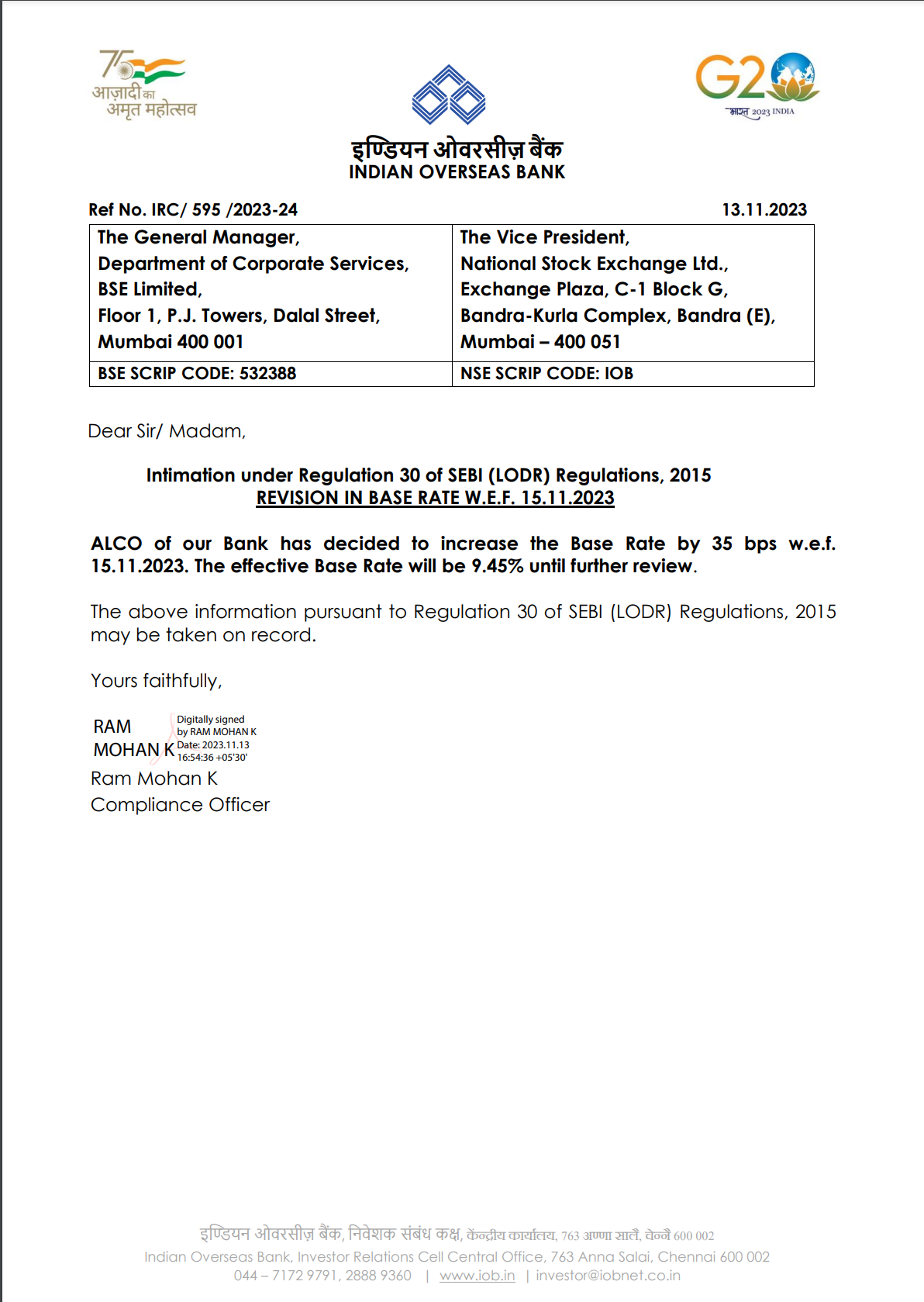

The bank’s committee, known as ALCO, has decided to increase the base interest rate by 0.35 percentage points (bps) starting from November 15, 2023. The new base interest rate will be 9.45%, and this rate will be in effect until they review it again. So, if you have a loan or deposit with this bank, the interest you earn or pay might change because of this rate increase.

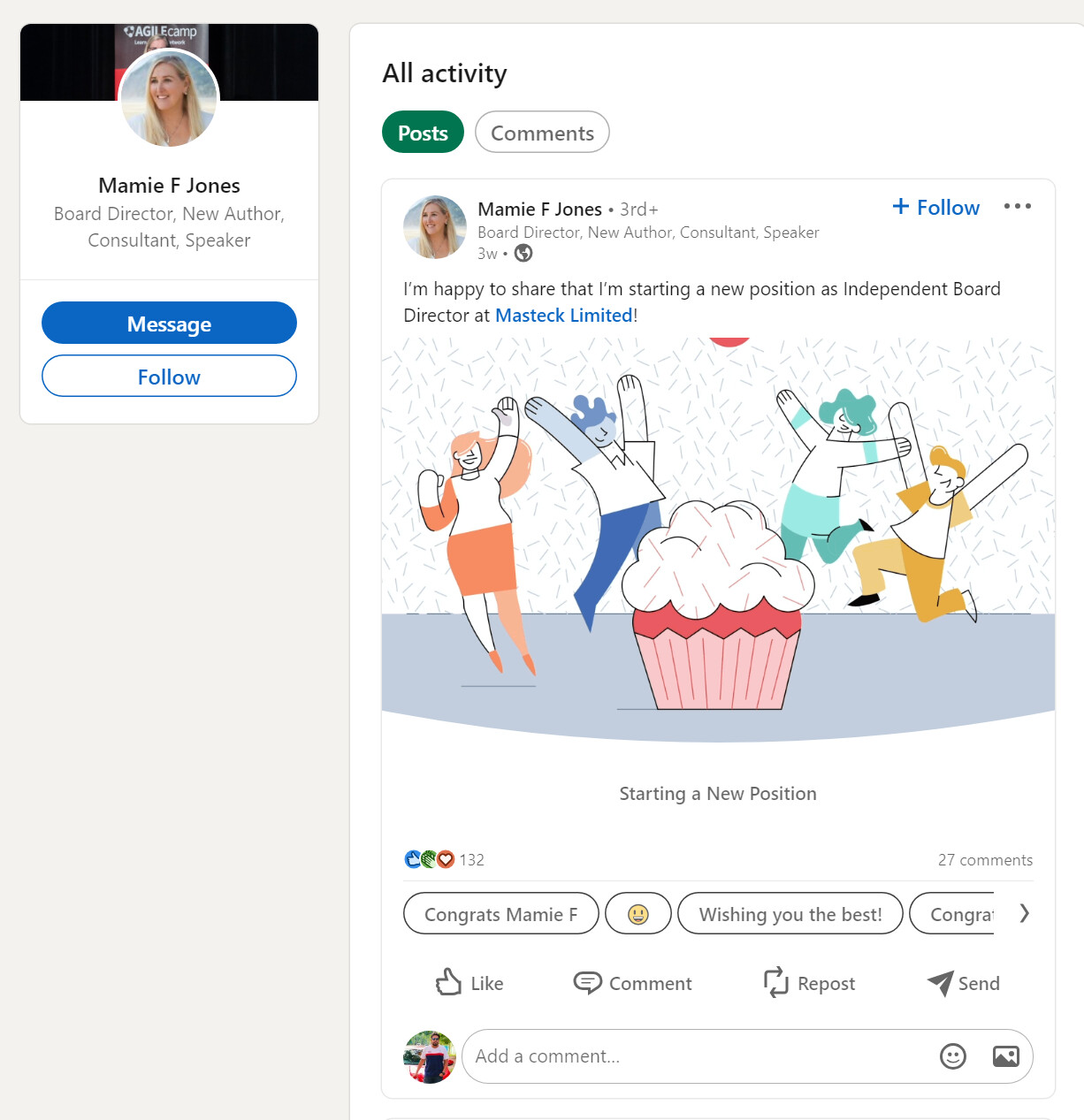

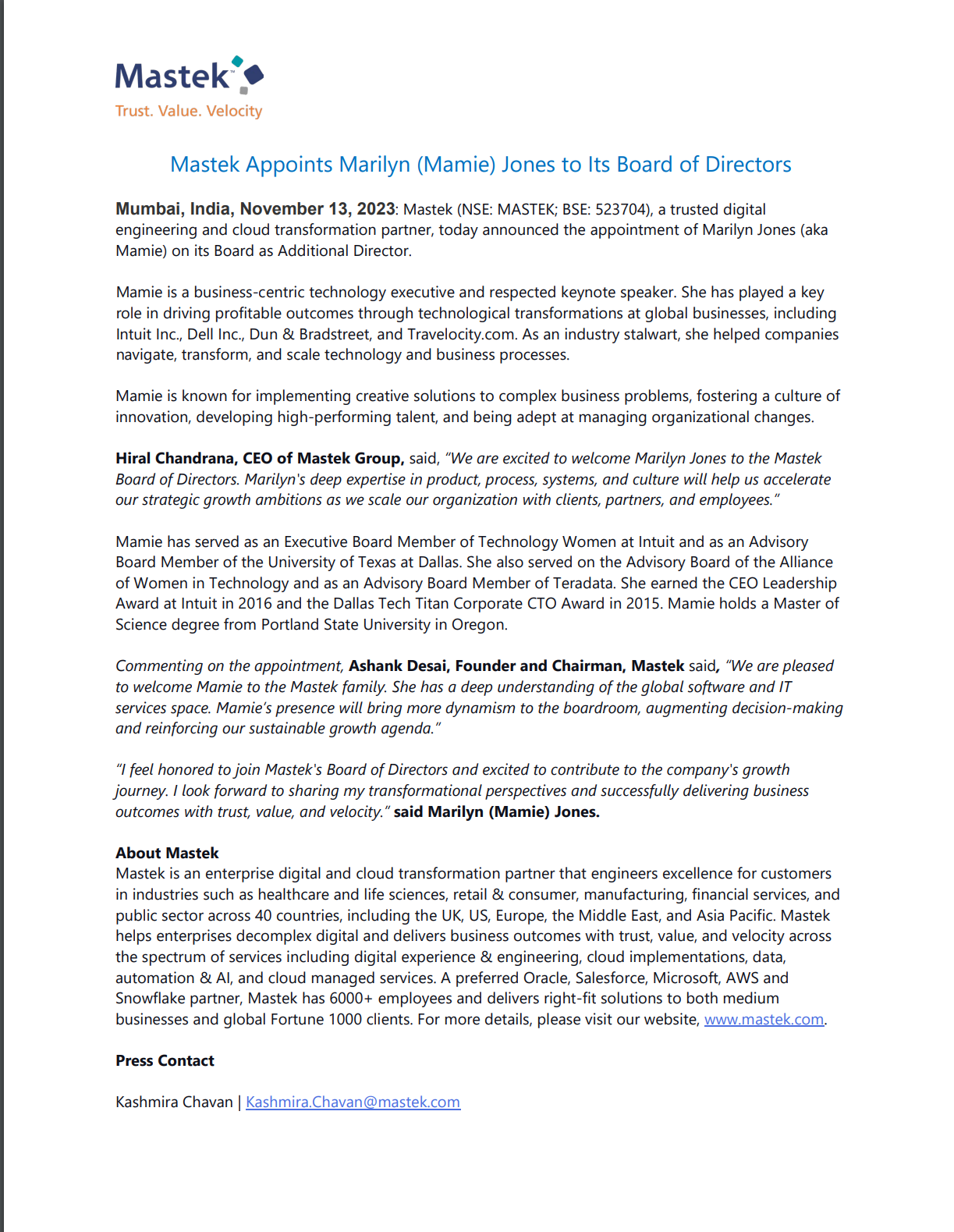

Mastek Appoints Marilyn (Mamie) Jones to Its Board of Directors

Management change-restructuring ?

Her linked profile – https://www.linkedin.com/in/mamie-f-jones-865a981/

Carysil Q2 concall highlights –

Sales – 164 vs 140 cr, up 18 pc

EBITDA – 33 vs 22 cr (up 50 pc, Margins @ 20 vs 16 pc)

Net Profit – 16 vs 9 cr

Gross Debt @ 210 cr

Sales growth led by increased orders for Quartz sinks from developed markets. UK subsidiary doing well. Additional Stainless Steel sink capacity has been commercialised. Have started building an order book for the same

Expanding dealer networks in India. Domestic business likely to be a key growth driver going forward

Exports revenues @ 129 cr, up 21 pc

Domestic revenues @ 35 cr, up 6 pc

Product wise sales mix –

Quartz sinks – 49 pc

SS sinks – 13 pc

Appliances – 11 pc

Solid surfaces – 26 pc

Quartz sink capacity @ 10 lakh sinks / yr

SS sink capacity @ 1.8 lakh sinks / yr

Kitchen appliances that company is selling under Carysil brand – Chimneys, Wine Chillers, Dish Washers, Hoods, Cook Tops, Built-in Owens, Microwave Owens

Company has also entered bath segment – to sell washbasins, facets, premium sanitary ware

Company purchases Moulds ( imported ) to manufacture over 400 SKUs ( uses over 150 Moulds )

Moulds have an avg life of 15+ yrs

Current Pan India Dealer network @ 3200+, Distributor network @ 82

Expecting domestic business growth likely to see a sharp increase from Q3 onwards. Oct 23 saw good sales volumes in Domestic Mkts

H2 sales likely to be better than H1. EBITDA margins may see some expansion due operating leverage

Company is gaining mkt share from its competitors in the developed markets ( most competitors are from Europe ) due product quality and lower costs – this has been the key for company’s growth despite Developed mkts witnessing broad based slowdown

Inventory liquidation overhang in the developed Mkts is now over

Aim to cross 200 cr sales in domestic Mkts in FY 25

The Ikea business ( supply of SS Sinks ) will commence in Q4. Have a few more customers that are likely to buy good volumes of SS Sinks. This business is also likely to commence in Q4

Company has started its assembly operations of built in appliances in Q3. Expect to see good contribution from this segment as well in Q3

Company in advanced negotiations with big customers for bulk quantities of Quartz sinks. Things likely to materialise by Q4. This should sharply increase company’s Quartz sinks capacity utilisation

Management still maintaining its guidance of Rs 1000 cr topline by end of FY 25 with EBITDA margins of around 20 pc

Company acquired United Granite LLC in US Mkt in Q2. Currently running at 60 pc capacity. At full capacity, this can do a revenue of about 120-130 cr. Company is engaged in fabrication of Kitchen tops for retail, residential and commercial projects. Carysil is confident of turning it around

Domestic business margins should remain in the 17-18 pc kind of band

Looks like Russia-Ukraine has been a huge blessing for the company – making European competition uncompetitive

Overall – good results with bullish commentary

Disc: holding from lower levels (25 pc lower than CMP), biased, not SEBI registered

Carysil Q2 concall highlights –

Sales – 164 vs 140 cr, up 18 pc

EBITDA – 33 vs 22 cr (up 50 pc, Margins @ 20 vs 16 pc)

Net Profit – 16 vs 9 cr

Gross Debt @ 210 cr

Sales growth led by increased orders for Quartz sinks from developed markets. UK subsidiary doing well. Additional Stainless Steel sink capacity has been commercialised. Have started building an order book for the same

Expanding dealer networks in India. Domestic business likely to be a key growth driver going forward

Exports revenues @ 129 cr, up 21 pc

Domestic revenues @ 35 cr, up 6 pc

Product wise sales mix –

Quartz sinks – 49 pc

SS sinks – 13 pc

Appliances – 11 pc

Solid surfaces – 26 pc

Quartz sink capacity @ 10 lakh sinks / yr

SS sink capacity @ 1.8 lakh sinks / yr

Kitchen appliances that company is selling under Carysil brand – Chimneys, Wine Chillers, Dish Washers, Hoods, Cook Tops, Built-in Owens, Microwave Owens

Company has also entered bath segment – to sell washbasins, facets, premium sanitary ware

Company purchases Moulds ( imported ) to manufacture over 400 SKUs ( uses over 150 Moulds )

Moulds have an avg life of 15+ yrs

Current Pan India Dealer network @ 3200+, Distributor network @ 82

Expecting domestic business growth likely to see a sharp increase from Q3 onwards. Oct 23 saw good sales volumes in Domestic Mkts

H2 sales likely to be better than H1. EBITDA margins may see some expansion due operating leverage

Company is gaining mkt share from its competitors in the developed markets ( most competitors are from Europe ) due product quality and lower costs – this has been the key for company’s growth despite Developed mkts witnessing broad based slowdown

Inventory liquidation overhang in the developed Mkts is now over

Aim to cross 200 cr sales in domestic Mkts in FY 25

The Ikea business ( supply of SS Sinks ) will commence in Q4. Have a few more customers that are likely to buy good volumes of SS Sinks. This business is also likely to commence in Q4

Company has started its assembly operations of built in appliances in Q3. Expect to see good contribution from this segment as well in Q3

Company in advanced negotiations with big customers for bulk quantities of Quartz sinks. Things likely to materialise by Q4. This should sharply increase company’s Quartz sinks capacity utilisation

Management still maintaining its guidance of Rs 1000 cr topline by end of FY 25 with EBITDA margins of around 20 pc

Company acquired United Granite LLC in US Mkt in Q2. Currently running at 60 pc capacity. At full capacity, this can do a revenue of about 120-130 cr. Company is engaged in fabrication of Kitchen tops for retail, residential and commercial projects. Carysil is confident of turning it around

Domestic business margins should remain in the 17-18 pc kind of band

Looks like Russia-Ukraine has been a huge blessing for the company – making European competition uncompetitive

Overall – good results with bullish commentary

Disc: holding from lower levels (25 pc lower than CMP), biased, not SEBI registered