Any updates on Dynemic Products after their poor show?

Posts in category Value Pickr

Indo Count Industries ~ Global Home Textiles Bedding Segment Leader (13-11-2023)

Indo Count Industries:

Q2FY24 Short Notes:

Product Mix:

Company’s product portfolio includes Bedsheets, Fashion, Utility and Institutional Bedding. Company Plans to increase Fashion, Utility and Institutional bedding as a proportion of the sales from 19% in FY 23 to 30%. All these are high Value-added products and will improve the Margin Profile of the company. There is significant opportunity in this segment due to China plus one Strategy as this segment was previously dominated by China.

Geography Mix:

Currently generating 70-75% of the revenues from US. Company plans to reduce this to 60%

Strategy for doing this:

FTAs with Australia and UAE has helped in reaching new customers. Also, we are getting significant inquiries from Latin America and Japan. China plus one is also helping in reaching new geographies. Potential FTAs with UK and EU will be a big boost to achieve this target.

India generated 2.5% of the Total Revenues in FY 2023. Company plans to increase this to 10% and beyond in the next 5 years. Currently, Indian Demography is positive towards consumer products. For this One Aspiration Brand Boutique Living and one Value brand Layers has been launched and company is working on B2C, D2C strategies.

Volume Growth Guidance:

Company has revised the Volume growth Guidance from 85-90 million metres to 90-100 million metres for FY24.Company said due to significant order inflows they are expecting to reach the higher end of the guidance but considering the geopolitical situation they are proving a range.

Capital Allocation Strategy:

Company has completed majority of the Capex in the last 2 years and company has no plans to do capex in the next 3 years and their plan is to enhance the capacity utilization from current 60-62% to 100%. Company’s plan is to reduce debts and make debt free. Company also invests in areas like Solar Plants to reduce the Costs.

Company is having all time High EBIDTA margins in the range of 16-18%. But, all the above efforts will not only help in sustaining the EBITDA Margins but also improve it.

Overall Positive Triggers for the Company:

Company has Significant Volume growth Opportunities.

Operating leverage Advantage due to Capacity Utilization currently at just 62%

Improving Product Mix and Cost Rationalization will help in Stable or Improving EBITDA margins.

PAT Margins will improve non-linearly as interest Cost will reduce due to reduction of debt and Depreciation will reduce as no capex was planned for next 3 years.

Disclosure: Invested and Biased

Goodluck India Ltd (13-11-2023)

Please find the Q2Fy24 concall highlights in the below document and the blog where one can follow for more such insights i.e.

GoodluckIndia Q2Fy24 concall.pdf (126.4 KB) GoodLuck India Q2Fy24 Concall – Knowledge Seeker

Radiant Cash Management Services – Asset Light Play On Cash Logistics (13-11-2023)

Sharing the latest interview by CMD Col.David Devasahayam. He mentioned that thru AceMoney acquisition, they are targeting to deploy 1 lakh micro ATMs in the next 2 years (with RBI subsidy). Rs.850 revenue per micro ATM/month = 8.5 Cr of additional revenue per month (Refer 3:14 in the video).

Targetting ₹8-9 Cr Revenue From The Recently Acquired Acemoney: Radiant Cash Mgmt Services

Adding a reference video on how micro ATMs work:

Disc: Invested

Deep Value Portfolio (13-11-2023)

The last couple of weeks has been all about … Pfc.

Finally I would say it is out of cheap valuation category.

From 26th Oct to 13th nov (roughly 2.5 weeks). Pfc is now 320 from 230!!

It’s now 1.1x book value, pe of 5.5, it’s tarting to lend in infra projects which I am not sure about. We have riden the wave on pfc from 110 (before bonus, bonus adjusted it would be 88) to 320 now with some profit booking ![]() (/diversification, in this case it worked as deworsification

(/diversification, in this case it worked as deworsification ![]() )!!

)!!

But now I feel, the time is ripe for not being overweight on pfc. No one knows where the momentum will take pfc, but atleast it is not extremely undervalued now.

DHP India Ltd – Regulators and Fittings (13-11-2023)

Hi LNB : Considering DHP is export oriented business, majorly EU & South America. And these countries are facing tough economic scenarios specially in EU (like Germany & many others). Do you think, this can be the reason for de growth in sales for DHP. I think, even the company doesnt give the bifurcated figures geography wise.

PS : Holding for more than a decade. Totally biased. Can add more or sell out.

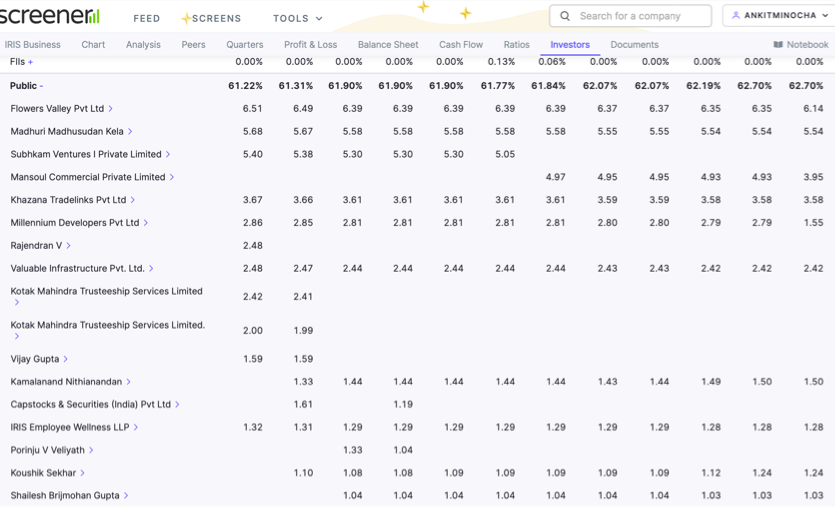

Iris Business Services – Emerging SAAS Microcap (13-11-2023)

Agree that the promoter holding aspect is a monitorable, but the promoters have indicated over the AGM that they do not wish to dilute at these valuations. In the AGM as well, the management was asked regarding a rights issue and they expressed that they do not prefer to dilute at such valuations and might explore a convertible note. AGM video below is as it is quite informative.

23rd Annual General Meeting of IRIS Business Services Limited

Regarding FII/DII holding, for a company with a market cap of ~250 Cr, I don’t think its the most relevant aspect. A simple glance at shareholders in the public space shows Madhuri Madhusudan Kela owns over 5% of the company for a long time.

Disclosure : Same as above

The Anti-Portfolio (13-11-2023)

In my view and detailed assessment, both are still undervalued. Betting heavily on both of them with a long term view.

Esab India (13-11-2023)

Very typical MNC behavior…raising royalty as soon company starts doing better… since 73.72% of the listed entity is already owned by ESAB USA (through it subsidiaries), this 2% increase in royalty is basically taking away that much money from minority shareholders…No wonder stock price got punished in the market

disclosure – invested earlier but reducing position and may decide to exit soon

Iris Business Services – Emerging SAAS Microcap (13-11-2023)

Great results in my opinion too.

What I find especially investment worthy in these SAAS businesses is the operating leverage which comes into play – YOY the growth in topline is 37% whereas in EBITDA the growth is 142%!

Mr Swaminathan had alluded to this benefit of being a SAAS growth story in the Q1 concall as well. Main contributor this time was the collect business for which the order book continues to look strong. I had also attended the concall this time where again management was very clear in certain aspects, I will share some of the details once the transcript is released.

Disclosure : Same as above