In my opinion, their revenue is impacted by new VC backed fintechs coming up. RBI stringent guidelines and VC money drying leading to lower revenues.

Disclosure: Not invested, tracking.

Posts in category Value Pickr

Apollo Finvest – Scalable business run by motivated promoters (11-11-2023)

Investing Basics – Feel free to ask the most basic questions (11-11-2023)

Greeting to all,

I just have one question

In a company where Promoter sold their 24%stake and it got bought by DII ( increased from 16% to 33% name:- Quant, Icici, Bnp paribas, goldman, mirae etc) and & FII ( increased from 3% to 10%)

How to look this transaction?

Thanks

Max Ventures – A Unique Demerger Opportunity (11-11-2023)

We Have Put In ₹1,600 Cr Of Equity In Real Estate Business: Max Estates | CNBC TV18

Max Estates will be the pure play real estate business of the Max Group, says Sahil Vachani, MD & CEO of Max Estates. Tells Reema Tendulkar, Surabhi Upadhyay & Pavitra Parekh that once fully developed, rental portfolio will be around Rs 500 cr

Campus Activewear – betting on the India Consumption Theme (11-11-2023)

I’m not an expert in understanding business but what I have understood from the concall is

- This was the worst quarter, now all next quarters will be better than this.

- Management is not bullish for the next quarters but we might see normal growth.

- Some impact was due to the festive season being shifted to the next quarter.

- Feel free to add if anything is missing or incorrect.

Something does not feel right as other footwear companies posted some positive results with some percentage of decline and not ~99% decline or ~0 profit.

Currently, the stock is at a PE of 76.7 & PB of 13.3, I don’t think it deserves this valuation for negligible growth.

Disc: Exited my entire holding on Friday, might take re-entry if it crashes a lot.

Note: This is not a buy/sell recommendation.

Krsnaa Diagnostics – what is the diagnosis? (11-11-2023)

Some Q2 highlights

- Margins: The company expects to sustain EBITDA margins between 26% to 28%, with aspirations to improve them. It was noted that margins might vary in quarters where expenses are frontloaded due to new tender wins, as initial expenses (like setting up equipment and infrastructure) do not immediately correspond with revenue. However, as volumes increase, revenue and margin are expected to improve.

- Rajasthan Tender: The revenue potential from the Rajasthan contract was revised from Rs. 150 crores to Rs. 300 crores due to the addition of 17 more districts. However, delays have pushed expected revenues from this project into the next fiscal year. Despite this, the company remains confident about its growth momentum and expects other projects to compensate for the delay in the Rajasthan revenue contribution.

- Revenue Guidance: The company is aiming for a 30% Compound Annual Growth Rate (CAGR), excluding the impact of the Rajasthan project. This growth is expected to be driven by various projects across different states. For example, projects in Assam, Odisha, Punjab, Himachal, and Maharashtra are anticipated to bridge the gap left by the delayed Rajasthan project. The company also expects significant revenue growth from new tenders in the next fiscal year, projecting about Rs. 140 crores of additional top-line revenue, potentially rising to almost Rs. 200 crores as the centers mature.

- Project Implementation and Impact on Margins: The implementation of projects like Assam labs and others may impact margins in the short term due to high initial expenses. However, from the fourth quarter onwards, these projects are expected to contribute positively to revenue and margins. The company is actively engaged in various Public-Private Partnership (PPP) projects to bolster its presence and growth. It also focuses on the B2C segment with cost-effective wellness packages to cater to diverse customer needs.

- Investments and Expenses Related to Rajasthan: The company has not made significant capital investments in the Rajasthan project. Operational expenses and basic setup work have been expensed out, with no major investments recorded on the balance sheet for this project.

- Other Operational Highlights: The Punjab tender is on track, with revenues ramping up and operational challenges resolved. The business in Punjab is primarily cash-based, different from other PPP projects. The introduction of home collection services in Punjab is expected to further increase revenues.

- Current Projects and Future Plans: The company is working on installing 39 CT-scan units across Maharashtra, with revenue projections expected in Fiscal 2025. Additionally, their project in Odisha has commenced operations and is poised for substantial revenue growth from the fourth quarter of Fiscal 2024.

- Private Hospital Partnerships: The company’s relationships with private hospitals and Krsnaa business associates are increasing. The contracts with private hospitals are typically long-term, similar to PPP (Public-Private Partnership) projects. The key difference is that in private hospital partnerships, Krsnaa Diagnostics pays a revenue share to the hospitals for operating out of their premises. The prices in these partnerships may be slightly higher than PPP projects to accommodate the revenue share paid to private hospitals.

- BMC Contract: Krsnaa Diagnostics has rapidly expanded under its BMC contract, operationalizing around 462 centers. The volumes they expected to complete in four years were achieved in just 6 to 9 months. The company is also expanding its Mumbai lab, and they anticipate increased revenues over time.

- Home Collection Services: BMC has mandated Krsnaa Diagnostics to start home collection services across the Mumbai region. This service allows them to charge an additional convenience fee for collecting samples from homes or other locations. The monthly revenue run-rate from these services, initially in the range of Rs. 2 crores to Rs. 2.5 crores, is expected to increase to Rs. 4 crores to Rs. 5 crores.

Borosil Limited (11-11-2023)

Q2 FY24 was in line with other listed players. Not bad and not exciting either.

De-merger of scientific division on plan for January 2024 – Can it unlock more value?

Disc:invested

Prataap Snacks Ltd – Set for a crunchy bite! (11-11-2023)

Just a brief Highlights of the call

- Demand and Inflation: The company is seeing demand pressure, especially in rural and lower-income urban markets, due to rising costs and inflation. Optimism for medium to long-term improvement was expressed, with technology like Salesforce Automation being used to drive sales growth. The expectation is that the second half of the year will be better than the first, with sustained operating margins.

- Competition and Market Share: There’s increased competition due to lower raw material prices, especially from smaller players, leading to heightened competitiveness and market share losses for major players including Prataap Snacks.

- Namkeen Category and Portfolio Performance: Namkeen has shown strong growth due to consistent efforts, aiming to increase its revenue contribution from 16% to 20-23% in the coming years. Other product categories have not shown significant performance changes. Namkeen has a slightly lower gross margin but compensates with lower freight costs due to better weight-to-volume ratio.

- Distribution and Growth Strategies: The company is expanding its reach, particularly in the Namkeen category, and aims to grow distribution by 5-7% annually. Changes in distribution are largely complete, minimizing disruptions.

- Ads and Marketing Spend: Currently, marketing spend is around 1.25% of overall revenue. There are plans to increase this next year for brand building, but for this year, it will remain in the same range.

- Margin Goals and Cost Optimization: Prataap Snacks is targeting double-digit EBITDA margin next year, having seen margin improvement over the last three quarters. Cost optimization measures include reduced sales channel costs and improved productivity in production.

- Capacity Utilization and New Facilities: Utilization is around 60-62%, with no significant change in product category contribution compared to last year. The J&K plant is expected to be operational by January 2024, and a Rajkot expansion is also planned. The company is cautious about a rapid ramp-up to 80% utilization, considering sales growth as a factor.

- Market Conditions and Future Outlook: No significant improvements in the rural market were noted around Diwali. The company reflects on its approach since the IPO, acknowledging challenges during COVID-19 and the need to adapt its product offerings. Plans are in place to cater to more urban environments with new products and categories.

- Regional Markets and Expansion: The company is focusing on the South India market, developing specific products for this region, as it’s a late entrant there. Revenue from East and South India is growing, with most revenue still coming from the West and North markets

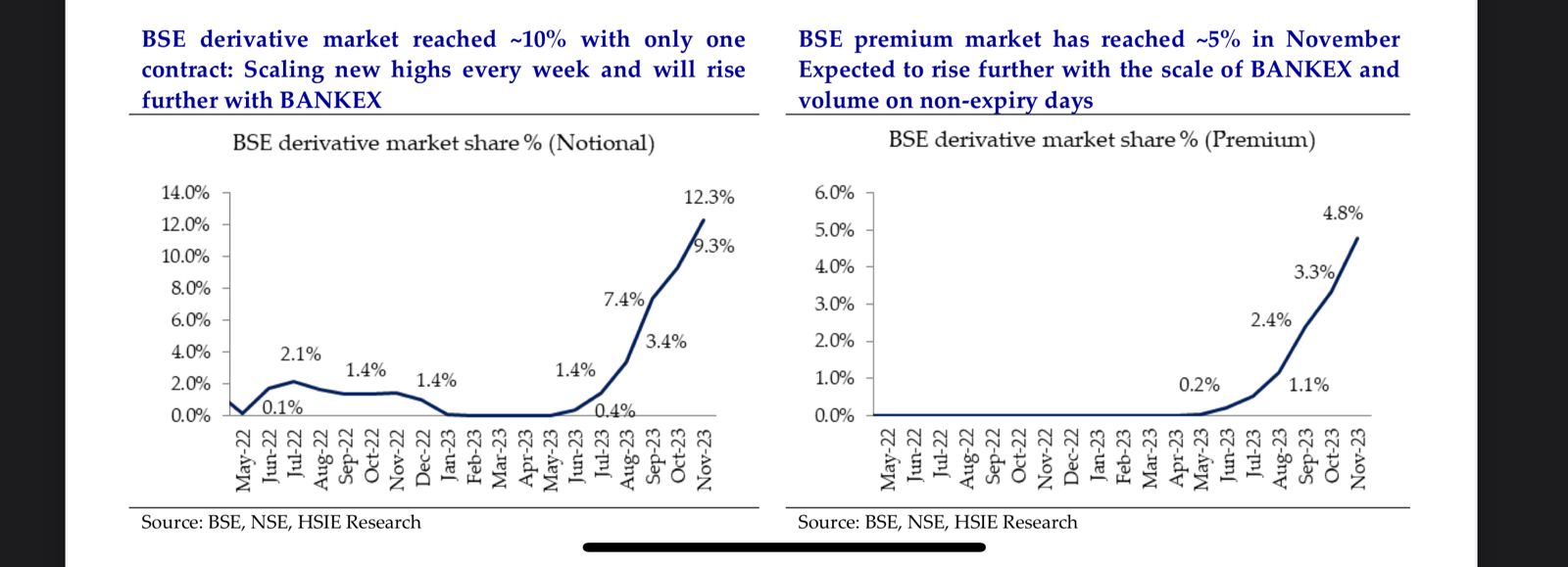

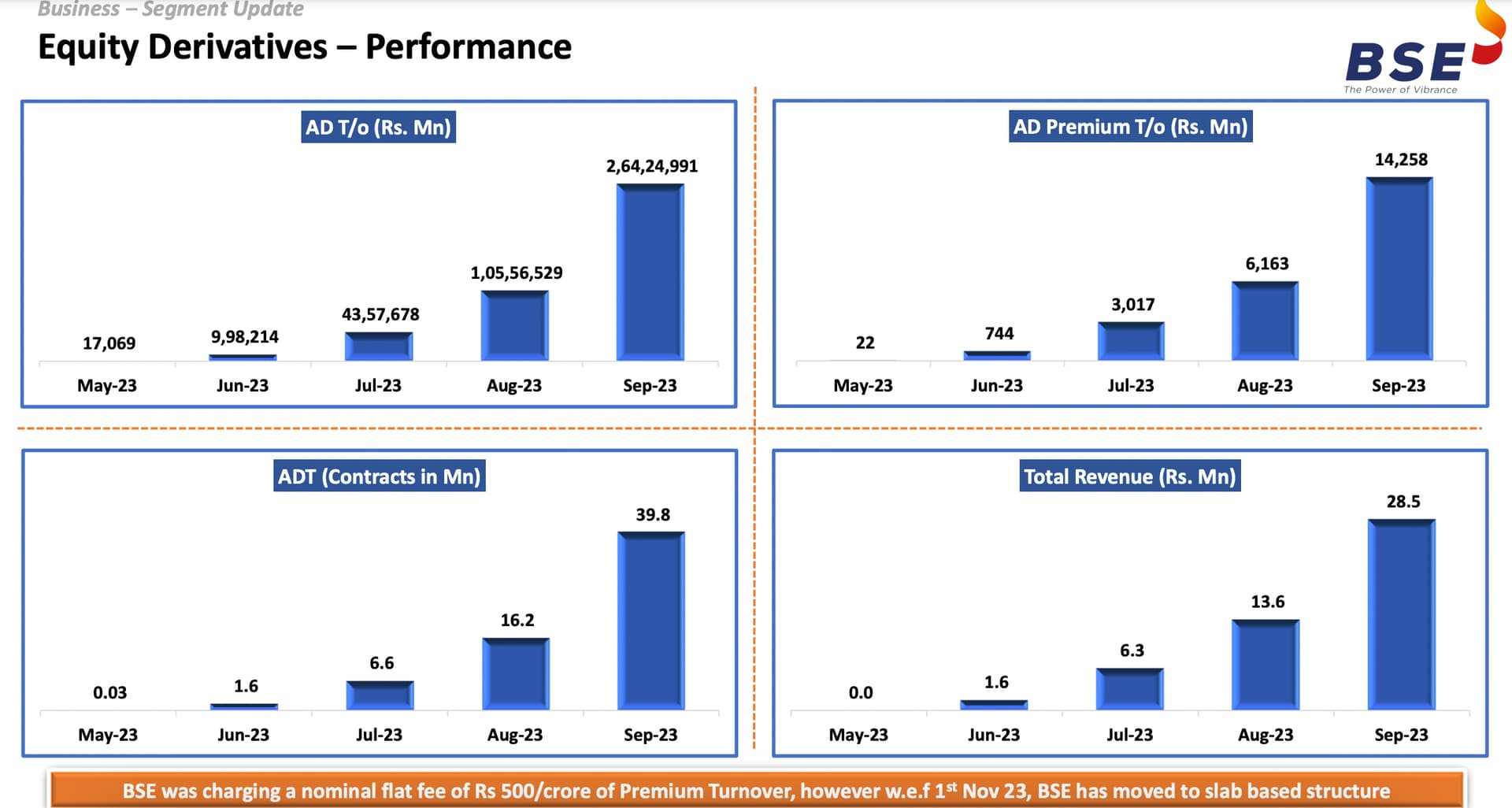

BSE (Bombay Stock Exchange)- Bet on Financialization? (11-11-2023)

Some key numbers:

- BSE’s premium turnover has reached ~5% of the industry already – again sooner than expected

- This number should double with the growth of more brokers, adoption by participants and rise of bankex

BSE (Bombay Stock Exchange)- Bet on Financialization? (11-11-2023)

Results for BSE out: Better results than the street expected mainly attributed to increased treasury (due to FNO) and better IPO book building cylce.

- Revenue up 59% YoY

- PBT up 257% YoY

Commentary from management:

- The company has been bleeding heavily in settlement charges due to which the prices were increased earlier than expected. But Sensex has achieved critical mass way before expectation which allowed them to do this

- Bankex has achieved the same volume in 4 weeks that Sensex derivatives took 12-14 weeks to achieve. Prices will be hiked in Bankex as well when critical mass is achieved but surely be done

- Due to most trading happening on expiry days the premium turnover / notional turnover remains lower than NSE. Focus will remain on increasing and developing the longer dated expiry volumes (Upto T+2 weeks) to increase liquidity and price turnover

- New products are being worked upon and eventually be released in the market; however what days still remains uncertain

- Working out things with brokers, members and NCL to further reduce down these costs as the volume in derivatives keeps increasing

a79f046f-d9d7-43e5-8434-ca1e775930ce.pdf (350.8 KB)

ea075acf-5a0c-4d20-883f-456f1109d339.pdf (3.1 MB)

Basilic Fly Studio Ltd (11-11-2023)

Appreciate you work…have you considered the aggressive revenue recognition angle?