I have been closely tracking red tap on each and every online store as well as off-line. I see huge demand of shoes and clothes. Despite yesterday‘s results which in my opinion are not bad because festive season shifted as well as they are more than last quarter of last year. I use this opportunity to invest more in this wonderful stock. By the way fox asking for not much information available you don’t know how Mirza International works. they generally have been silent performers

Posts in category Value Pickr

Kovai Medical Center and Hospital – Health and Wealth (11-11-2023)

Very good results overall.

- 20% increase in Revenues YoY; 11% increase QoQ as well. It looks like business is back to normal at last.

- The 38-40% increase in Profits is a little deceiving, since Cash profits have only risen 7-8% (Increased Working Capital and higher Taxes)

- But the real kicker for me is the bulk repayment of long term Debt to the extent of Rs. 118 Crores. We can see the immediate impact in Finance Costs reducing from Rs. 36.53 Crores in Mar 2023 to Rs. 15.82 Crores in Sep 2023.

- For the HY ending Sep 2023, Education segment has clocked around Rs. 14 Crores in PBT. Annualized, that’s Rs. 28 Crores – which is quite the jump from last year’s Rs. 2 Crores. Per management commentary, this could be peaking out soon. We’ll have to see how much the profits will grow YoY post that. I presume around 10% at least. 15% would be good from IRR perspective (Considering the Rs. 700+ Crores Capex that was made; but some of it was for the additional beds).

- If majority of the remaining Rs. 350 Crores (Short and long term) loan is repaid as discussed by the Management, the quarterly savings in Finance costs would be around Rs. 7-8 Crores. Of course, paying off Debt also allows internal profits to accrue faster and build up a war chest for further expansion.

Interesting times for KMCH.

Abbott India: MNC pharma play on increased consumer spending (11-11-2023)

Can you please compare this with last year and last quarter figures to know the change?

Is any one studying TPL PLASTEH (11-11-2023)

Is any one studying TPL PLASTEH ?

TPL Plastech Ltd is engaged in the business of manufacturing polymer based industrial packaging products like Drums and Jerry cans. It caters to customers in industries like Chemicals, Petrochemicals, Specialty Chemicals, Plasticizers, Pharmaceutical, FMCG, Food Products etc

Permanent Magnets – Business under transformation? (10-11-2023)

Can you share the link, seems removed from BSE

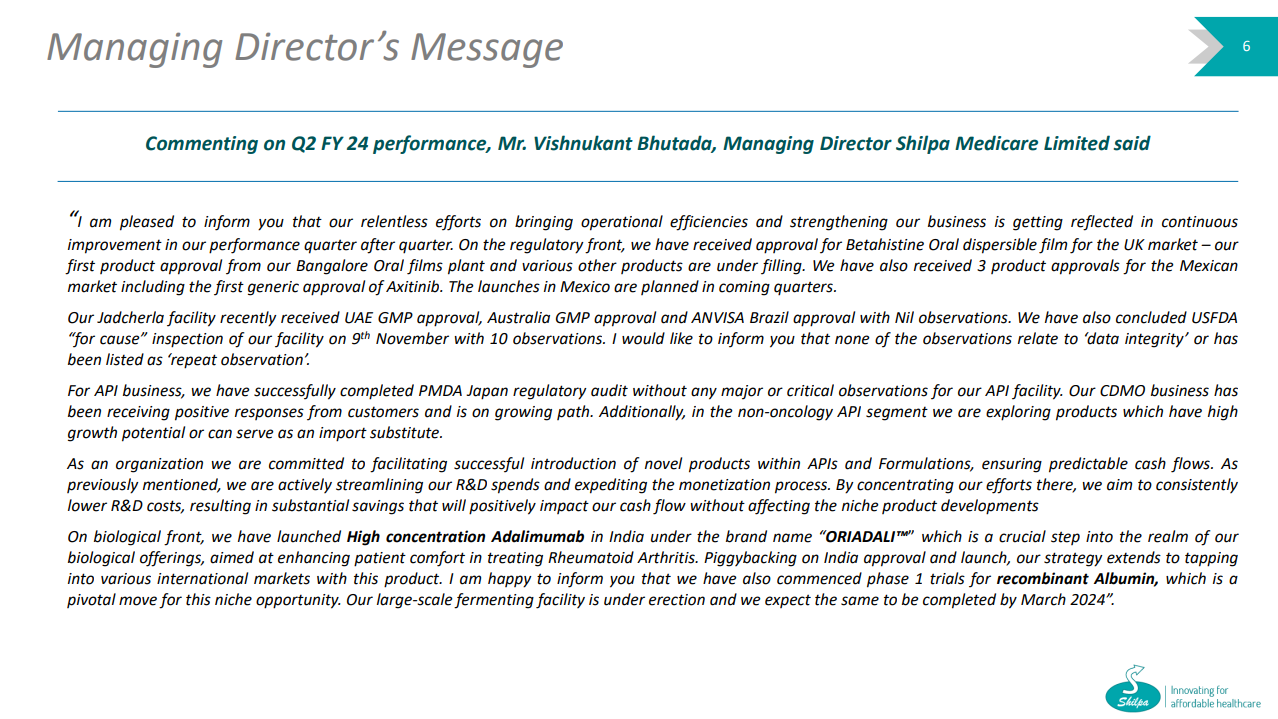

Shilpa Medicare -Racing away on the Oncology API highway! (10-11-2023)

The Managing Director reports on the company’s recent achievements, which include regulatory approvals for new products and facility inspections with positive outcomes. They emphasize efforts to streamline R&D spending for cost savings without compromising niche product development. Additionally, the company has launched a high-concentration Adalimumab product in India and initiated phase 1 trials for recombinant Albumin, signaling their expansion into biological offerings. The construction of a large-scale fermenting facility is in progress and expected to be completed by March 2024.

Operational Efficiency : The company has been focused on improving operational efficiencies and strengthening its overall business operations. These efforts have been successful, leading to continuous improvements in the company’s performance.

Quality and Compliance : The Jadcherla facility has recently received approvals from various regulatory authorities, including UAE GMP approval, Australia GMP approval, and ANVISA Brazil approval. Importantly, these approvals were granted with no observations, indicating high quality and compliance standards. The USFDA inspection, conducted “for cause,” concluded with 10 observations, but notably, none of these observations relate to ‘data integrity’ or have been listed as ‘repeat observations,’ which is a positive outcome.

API Business : In the API business, they have successfully completed a regulatory audit by PMDA Japan, with no major or critical observations for their API facility. Their Contract Development and Manufacturing Organization (CDMO) business has been well-received by customers and is on a growth trajectory. Furthermore, they are exploring products in the non-oncology API segment that have high growth potential or can serve as import substitutes.

Biological Offerings : On the biological front, the company has launched a high-concentration Adalimumab product in India under the brand name “ORIADALI™.” This product is aimed at enhancing patient comfort in treating Rheumatoid Arthritis. Leveraging the approval and launch in India, the company plans to expand into international markets with this product. They have also initiated phase 1 trials for recombinant Albumin, representing a significant step in this niche opportunity. Additionally, the construction of a large-scale fermenting facility is underway and expected to be completed by March 2024.

BMW Industries Ltd (Steel Service center) (10-11-2023)

Sir standalone represent which part of their business is this inclusive of their Bansal TMT

Thanking you

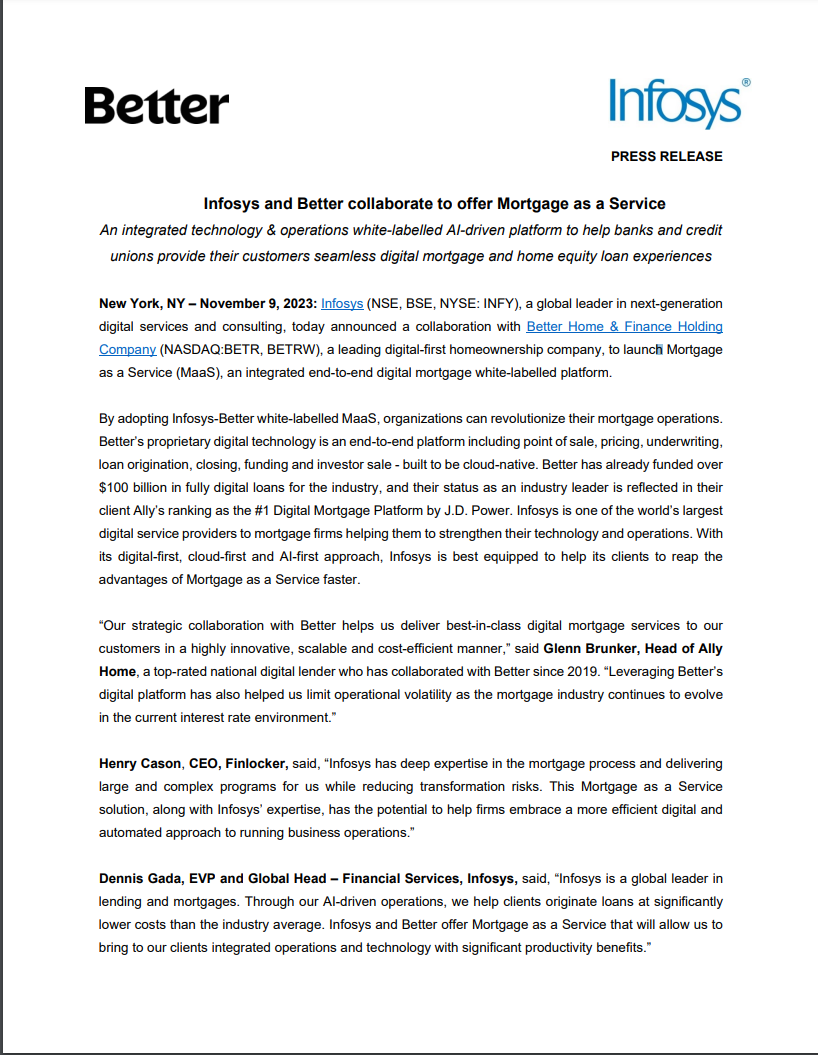

Infosys Limited – Are we getting a discount or no? (10-11-2023)

Infosys, a global leader in digital services and consulting, is partnering with Better Home & Finance Holding Company, a digital-first homeownership firm, to launch MaaS.

Mortgage Revolution: MaaS is an integrated technology and operations platform that enables banks and credit unions to provide their customers with a seamless digital mortgage and home equity loan experience. It offers an end-to-end solution for point of sale, pricing, underwriting, loan origination, closing, funding, and investor sale, all built to be cloud-native.

Benefits: The white-labeled MaaS platform by Infosys and Better aims to revolutionize mortgage operations for organizations, making them more efficient and cost-effective. Better’s proprietary technology, which has already funded over $100 billion in fully digital loans, and Infosys’ expertise in digital services combine to offer productivity benefits.

Shilpa Medicare -Racing away on the Oncology API highway! (10-11-2023)

I think, Promoters pledged shares to avail NCDs.

In Q1 call, management shared that they pledged share to avail NCDs at 12% interest for 1 year loan. They were confident that they can resolve Cashflow issue within 1 year.

With Q2 result, this statement make sense. Shilpa is one of the few Pharma company which is showing Topline and PAT growth.

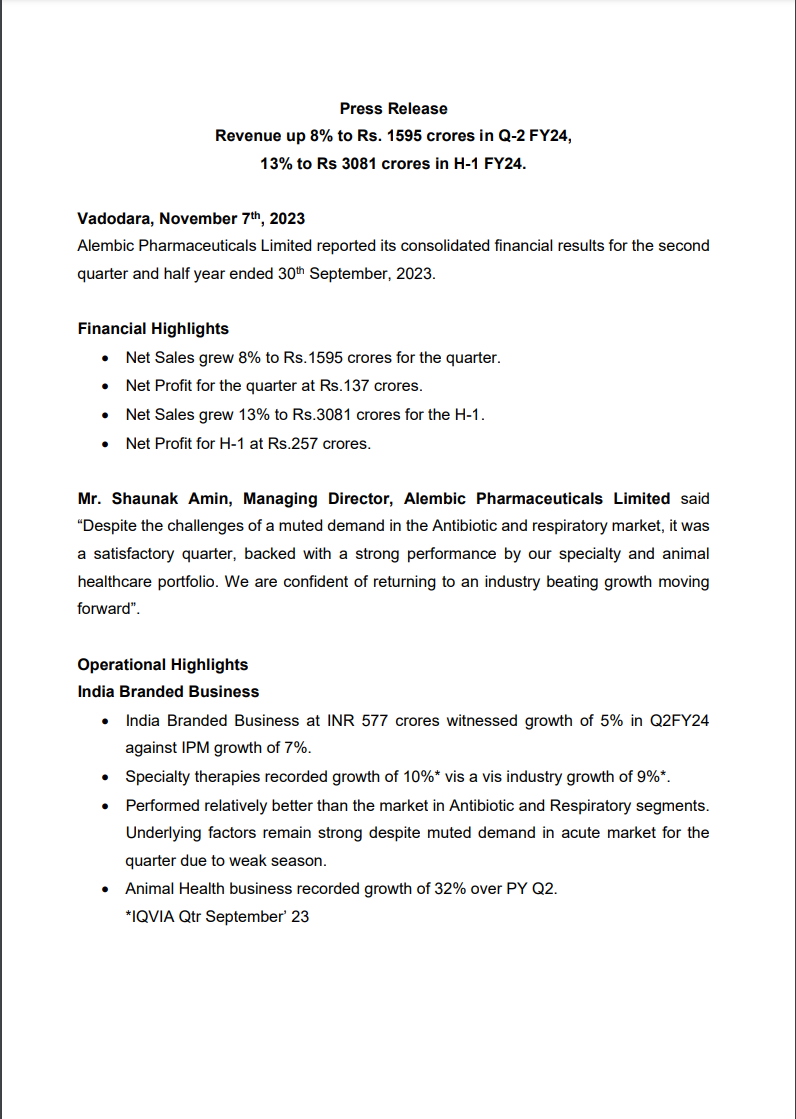

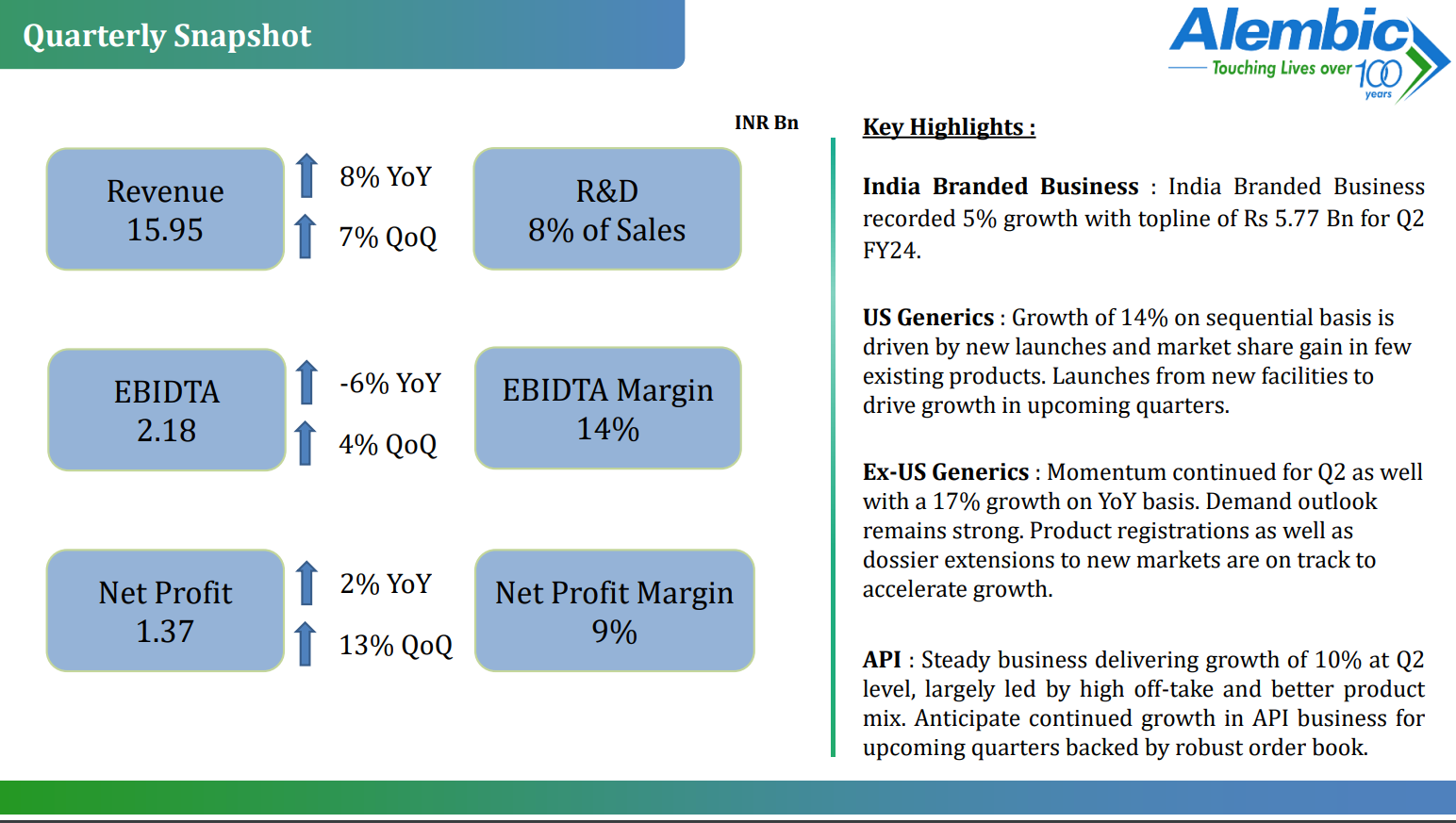

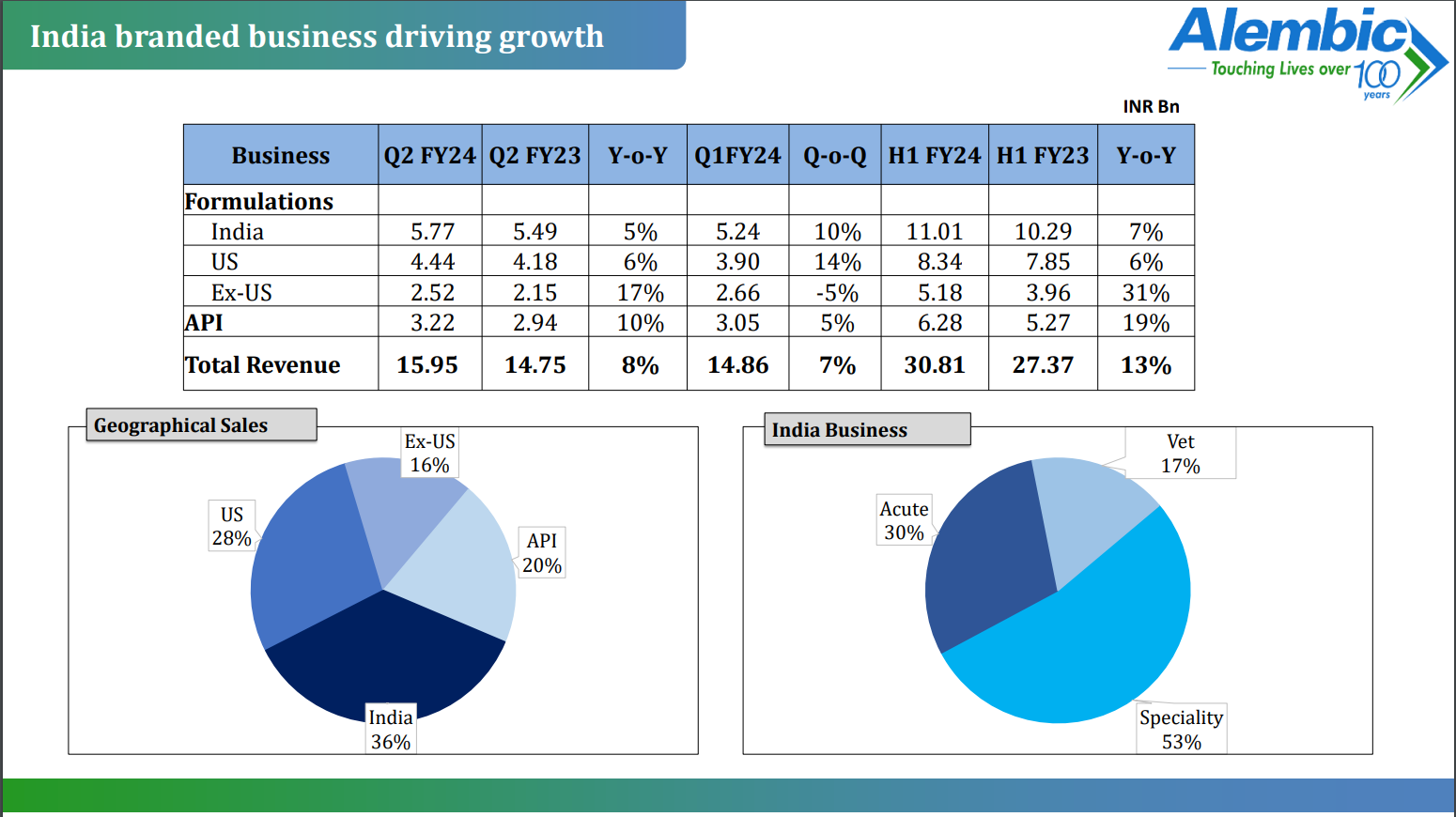

Alembic Pharma (Oral Solids ==> Injectables, Onco, Derma, Opthalmic) (10-11-2023)

Alembic Pharmaceuticals Limited, released its unaudited financial results for the second quarter and half-year ended on September 30, 2023. Here is a detailed summary of the provided information:

- Financial Results:

- Net Sales for the quarter increased by 8% to Rs. 1595 crores.

- Net Profit for the quarter amounted to Rs. 137 crores.

- Net Sales for the first half of the fiscal year grew by 13% to Rs. 3081 crores.

- Net Profit for the first half of the fiscal year was Rs. 257 crores.

- Operational Highlights:

- Despite challenges in the antibiotic and respiratory market, Alembic Pharmaceuticals reported a satisfactory quarter, with strong performance in its specialty and animal healthcare portfolio.

- The India Branded Business witnessed 5% growth in Q2FY24, with specialty therapies growing by 10%.

- The company outperformed the market in antibiotic and respiratory segments.

- The Animal Health business recorded significant growth of 32% over the previous year’s Q2.

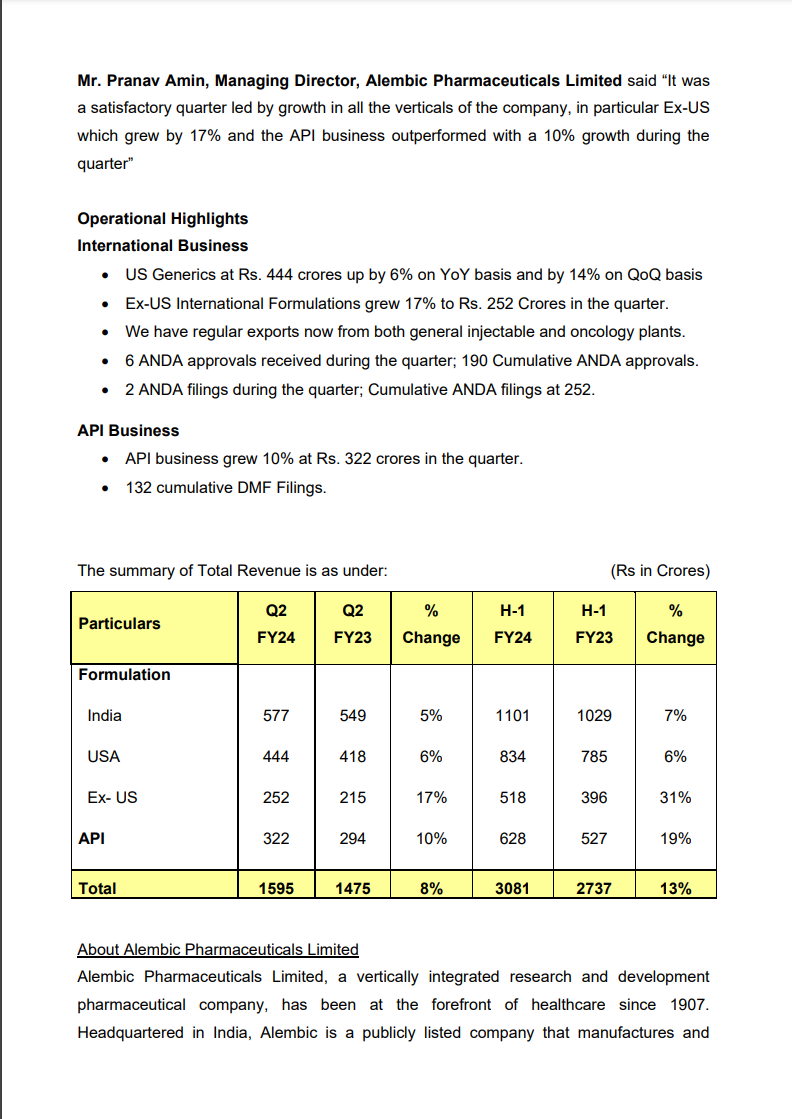

- The US Generics segment saw a 6% YoY growth and a 14% QoQ growth.

- Ex-US International Formulations experienced a 17% growth during the quarter.

- The company received 6 ANDA approvals and filed 2 ANDAs during the quarter.

- The API Business grew by 10% in the quarter, with 132 cumulative DMF filings.

- Total Revenue:

- The total revenue for the quarter was Rs. 1595 crores, an 8% increase compared to the previous year’s Q2.

- The total revenue for the first half of the fiscal year was Rs. 3081 crores, marking a 13% growth.