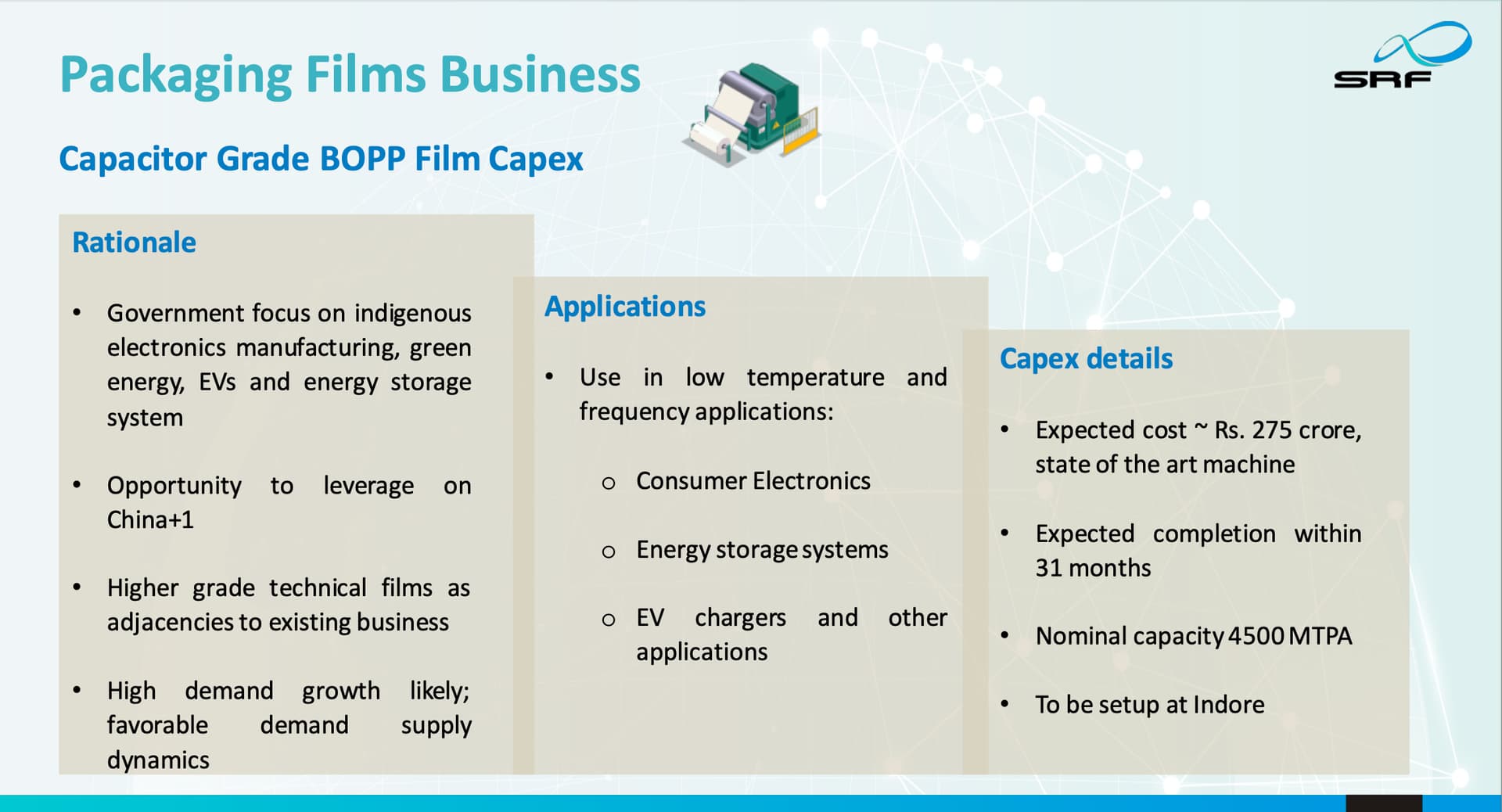

Exactly the same product as XPRO- line capacities are also same.

Nope, that was a reply given to difference between BOPP films and Capacitor grade. I attended the call live and could understand the context while listening

Exactly the same product as XPRO- line capacities are also same.

Nope, that was a reply given to difference between BOPP films and Capacitor grade. I attended the call live and could understand the context while listening

@Worldlywiseinvestors sir what product is then pls guide us

Thanking you

Deep Industries Limited Q2 FY ’24 Earnings Conference Call, the company provided detailed insights into its financial and operational performance. Here’s a comprehensive summary of the call:

Introduction:

Key Highlights:

Order Book and Revenue Growth:

Funding and Capital:

Dolphin Offshore:

Capex Plans:

Joint Ventures:

RAAS Segment:

Order Inflows:

Client Contribution:

Cash Flow and Investments:

Conclusion:

Overall, the call provided a comprehensive overview of Deep Industries’ financial and operational performance, order book growth, and plans for the future, including the expected contributions from Dolphin Offshore and joint ventures.

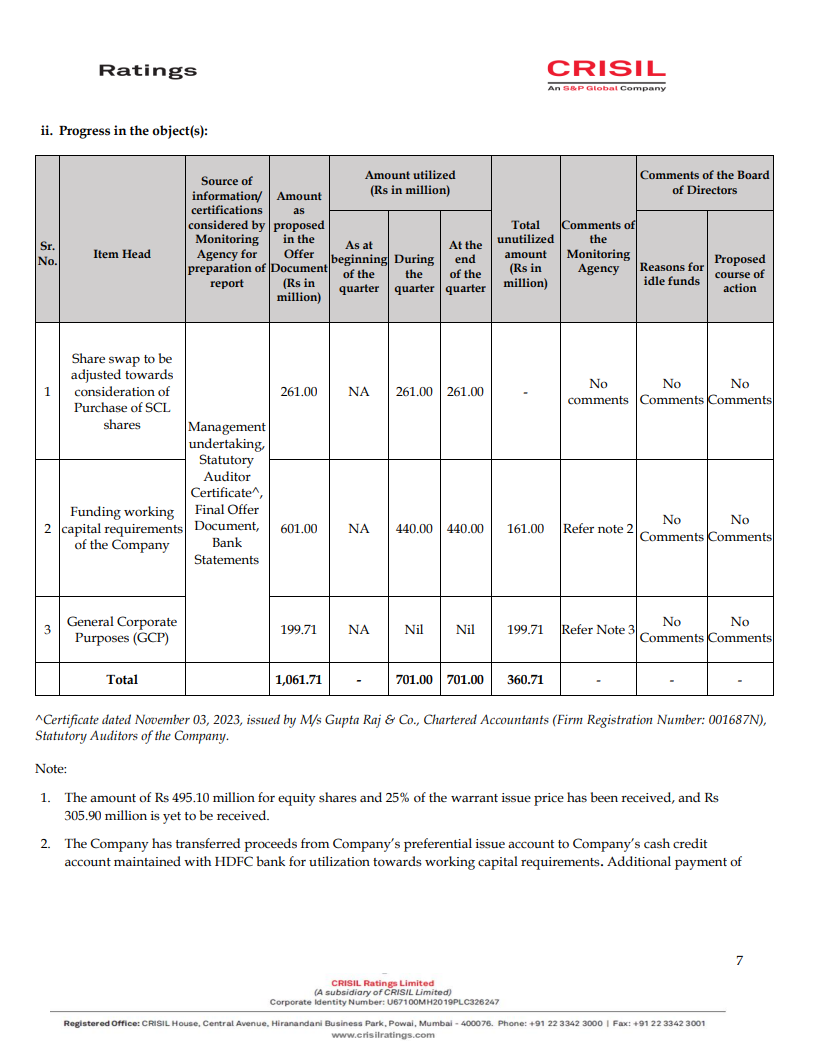

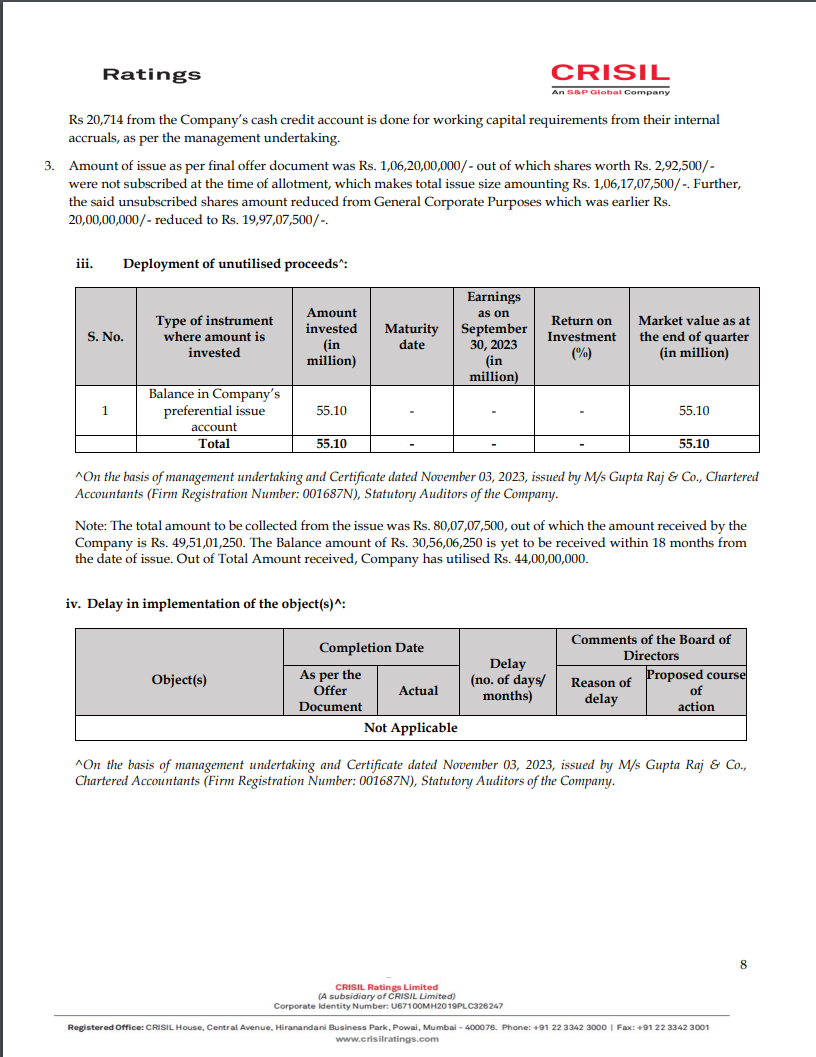

The report covers various aspects related to the utilization of issue proceeds and includes the following key points:

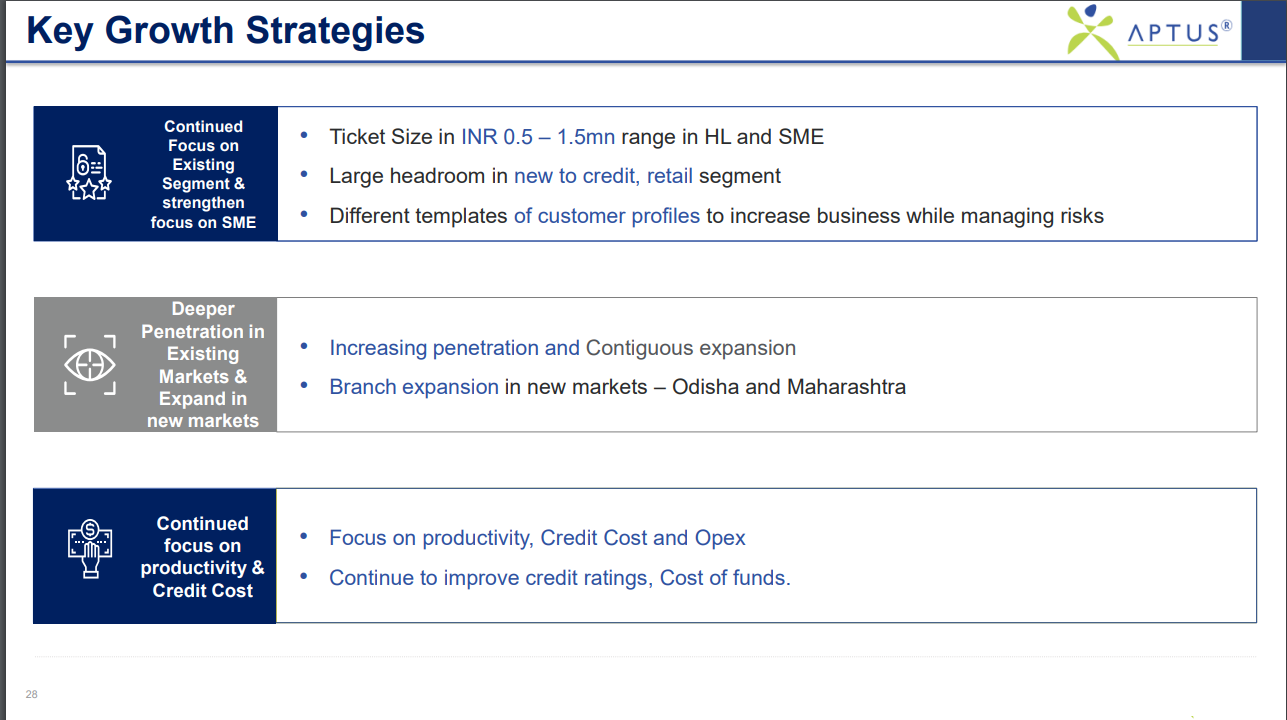

Growth Strategies

Thanks for the Q2 FY 24 summary, Harsh.

One minor correction, though. I was on the Q2 concall of Aptus and the management (Mr. P Balaji, CEO) guided for 30% AUM growth, not 25%. (Sounds optimistic, given their H1 numbers, but that’s what they guided)

Aptus has grown AUM for H1 FY 24 (Q1 + Q2) by 13% over March ’23 AUM and for them to achieve 30% AUM growth for FY24, then need to deliver 15% AUM growth in H2 (Q3 + Q4) over Sept, ’23 AUM. (Quite reasonable, given that Q3 and Q4 are seasonally a shade better)

Also, given that bulk of branch additions for FY 24 have already been done in H1 (around ~25 branches already opened in H1 out of ~35 to be opened), the guidance seems palpable.

Q2 Con call excerpt of Aptus below:

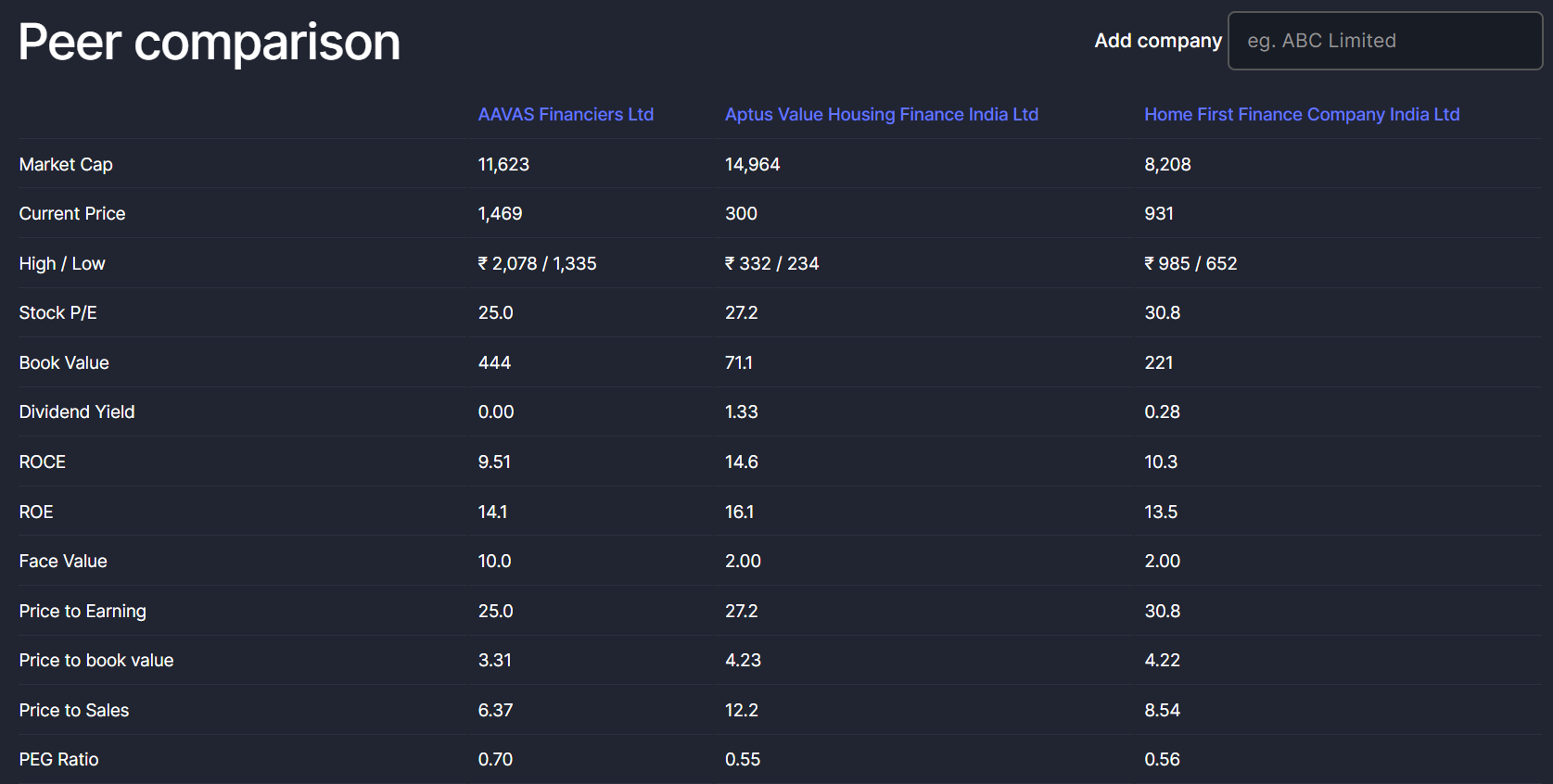

P.S. – I was also on the Q2 call of Aavas and their management has guided for 20-25% AUM growth and the management of Home First guided for 30% AUM growth for coming 2-3 years.

This is perhaps why Aavas is now trading at 3.31 times book, while Aptus and Home First are trading at 4.23 and 4.22 times book respectively.

Aside form these points, here are few aspects that are noteworthy for Aptus:

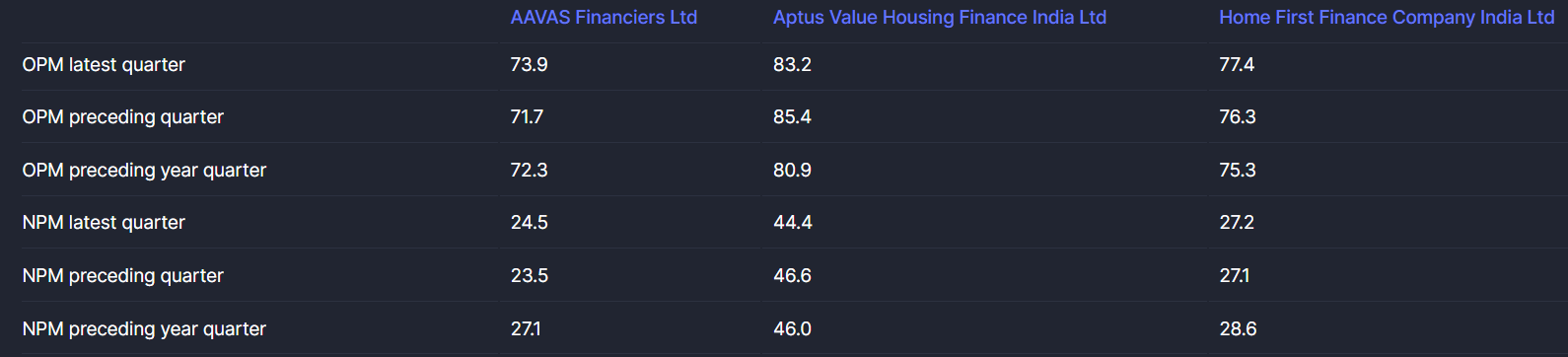

Aptus enjoys superior margins compared to Aavas and Home first due to its lower leverage (1.1 D/E) and thereby lower interest costs

Leading to almost 2x PAT margins for Aptus (44% PAT Margins for Aptus!, compared to 24% and 27% for Aavas and Home First)

Quite Naturally Aptus has high ROAs to boast, compared to its peers: (Almost 2x ROAs)

Also, such high PAT margins and ROAs for Aptus, will lead to accelerated retained earnings and book value growth for Aptus (Unless they don’t have high dividend payout rates – Right now Aptus has 20% div payout rates, Home first has 10% and Aavas pays zero dividend).

Management is quite seasoned and the market opportunity is huge. Interesting times ahead!

Disclosure: Invested. Potentially biased.

Q2 FY24 Concall Notes

I think the Q2 results and call was pretty decent. Numbers are back filling. Yet to reflect in numbers IMHO.

Some brief updates are

You can build the bear thesis.

As for the Notes given-

The company is planning to acquire a NCLT company having similar line of business.

This will lead to expansion of production capacity – beneficial for the company.