1)Sir just one ques about the business model, do they source steel ( RM) from Tata Steel and convert them into final product and they charge for it.You mean to say contract manufacturers like pharma and electronic device industry?

2)If yes, how do they have such exorbitant margins is this normal for this industry? Like

contract manufacturing other industry ie electronics they have margins of 2%-3%

3) when the price of production rises, do they have the power to re- negotiate or they suffer margin contractions?

Thanking you Sir

Posts in category Value Pickr

BMW Industries Ltd (Steel Service center) (10-11-2023)

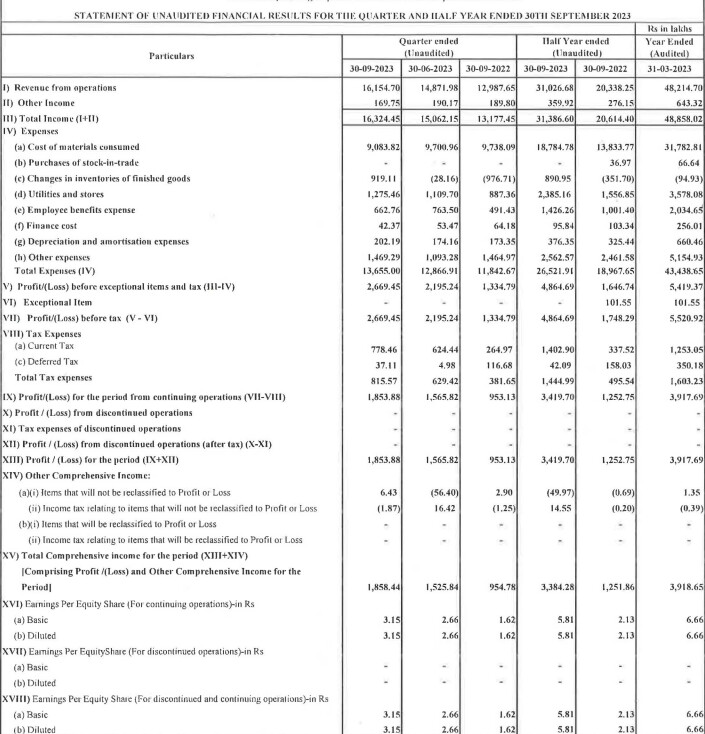

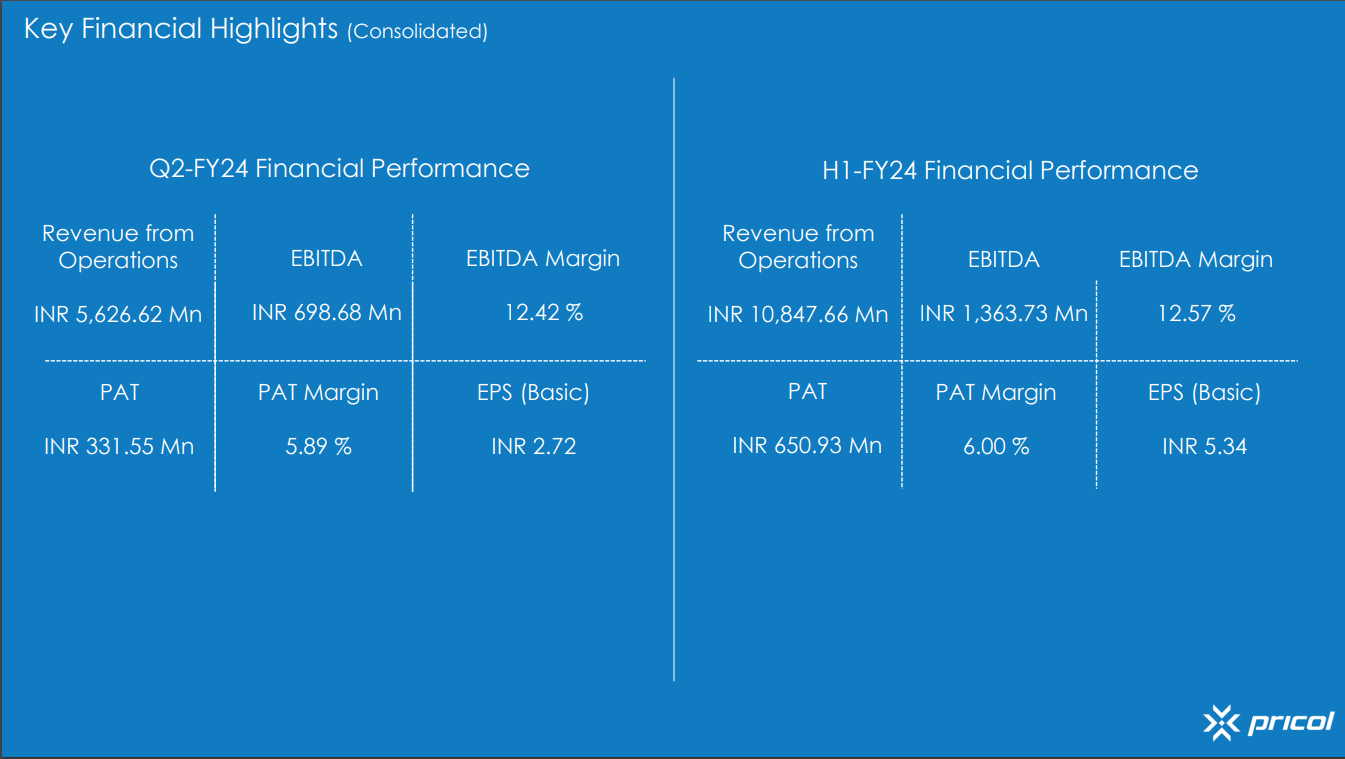

Pricol limited – OEM automotive (10-11-2023)

Pricol as released its financial results for the second quarter of the fiscal year 2023-24. Here’s a detailed summary of the information provided:

Q2-FY24 Consolidated Financial Performance:

- Revenue From Operations: In Q2-FY24, Pricol recorded revenue from operations of INR 5,626.62 million, reflecting a year-on-year (YoY) growth of 12.31%.

- EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization): The Q2-FY24 EBITDA stood at INR 698.68 million, with a YoY growth of 7.50%.

- EBITDA Margin: The EBITDA margin for Q2-FY24 was 12.42%.

- PAT (Profit After Tax): The profit after tax for Q2-FY24 amounted to INR 331.55 million.

H1-FY24 Consolidated Financial Performance:

- Revenue From Operations: In the first half of FY24 (H1-FY24), the company reported revenue from operations of INR 10,847.66 million, demonstrating a significant YoY growth of 16.02%.

- EBITDA: The EBITDA for H1-FY24 reached INR 1,363.73 million, showing a YoY growth of 12.10%.

- EBITDA Margin: The EBITDA margin for H1-FY24 was 12.57%.

- PAT: The profit after tax for H1-FY24 amounted to INR 650.93 million.

Q2-FY24 Business Highlights:

- Pricol received an award from Mitsubishi Heavy Industries Group for “Best Support” at their Supplier Conference. They were also awarded the status of “Self-Certified Supplier” for the year FY24, which signifies the company’s reliability and quality of support.

- The company was recognized with an award under the category of “Supplier Reliability Cluster Program” from TVS Motors.

- Pricol made strategic investments in Surface-mount technology (SMT) for printed circuit board (PCB) Assembly Line and Disc Brake assembly lines, highlighting their commitment to enhancing manufacturing capabilities and solutions.

Campus Activewear – betting on the India Consumption Theme (10-11-2023)

Analyst Meet Call Recording

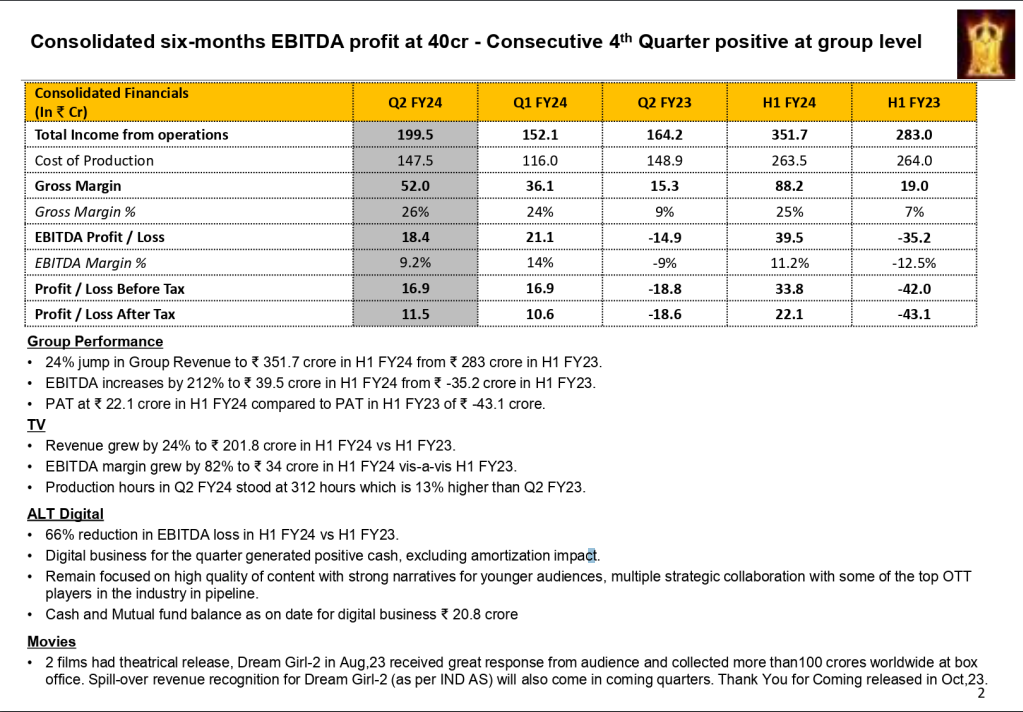

Balaji Telefilms (10-11-2023)

The provided text appears to be a financial and operational summary of a company for the first half of the fiscal year 2024. Let’s break down the key points:

- EBITDA Profit: The company achieved a consolidated EBITDA profit of 40 crore in the first half of FY24, marking a positive trend with four consecutive quarters of profit at the group level.

- Total Income from Operations: The total income from operations for the first half of FY24 amounted to 351.7 crore, showing a significant increase compared to the 283 crore in the first half of FY23.

- Cost of Production: Detailed cost figures are not provided, but they would contribute to understanding the company’s financial performance.

- Gross Margin %: The gross margin percentage is not provided, but it’s an important financial indicator that reflects the profitability of the company’s core operations.

- EBITDA Margin %: The EBITDA margin increased by 82% to 34 crore in H1 FY24 compared to H1 FY23, indicating improved profitability in the earnings before interest, taxes, depreciation, and amortization.

- Profit / Loss Before Tax: The company’s profit before tax is not explicitly mentioned in the summary.

- Group Performance: The group revenue increased by 24% to 351.7 crore in H1 FY24, with a significant improvement in EBITDA from -35.2 crore in H1 FY23 to 39.5 crore in H1 FY24. However, the profit after tax (PAT) decreased from 43.1 crore in H1 FY23 to 22.1 crore in H1 FY24.

- ALT Digital: The digital business saw a 66% reduction in EBITDA loss in H1 FY24 compared to H1 FY23. It also generated positive cash during the quarter and focused on content quality and collaborations with top OTT players.

- Movies: The company had two theatrical releases in the first half of FY24, with “Dream Girl-2” receiving a positive audience response and “Thank You for Coming” releasing in October 2023. The revenue recognition for “Dream Girl-2” is expected to continue in the coming quarters.

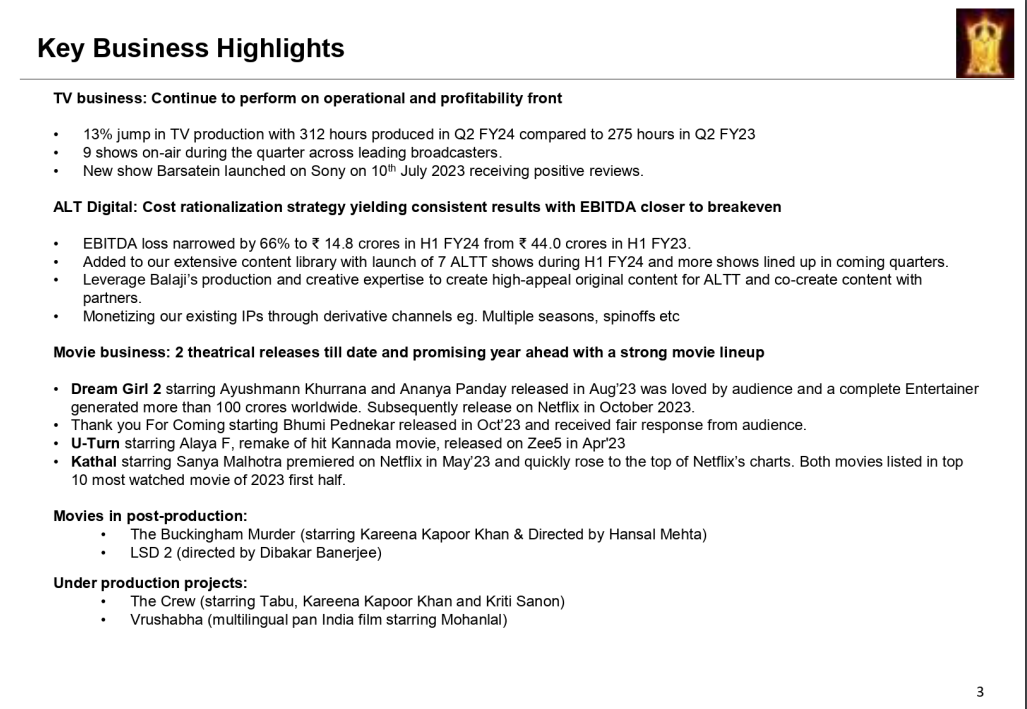

- Key Business Highlights:

- TV Business: The TV production increased by 13% in Q2 FY24, and 9 shows were on air during the quarter. A new show, “Barsatein,” received positive reviews.

- ALT Digital: Cost rationalization strategies led to a 66% reduction in EBITDA loss. The company expanded its content library and leveraged its expertise in content creation.

- Movie Business: The company had successful theatrical releases and promising upcoming movies. “Dream Girl 2” and “Thank You For Coming” were well-received.

- Movies in Post-Production and Under Production Projects: The summary mentions several movies in post-production and under production, indicating a robust pipeline of content for the future.

YM Portfolio For Long Term (10-11-2023)

IGPL Margin Reduced anyone know the reason

Balaji Telefilms (10-11-2023)

Bigger part of ‘Dream girl 2’ revenue will add to Q3

Pricol limited – OEM automotive (10-11-2023)

The results of TV motors are good. Hence their results in the next quarter should be good. We should track the EV growth esp. Of TVS to get a clearer picture of it.

Screener.in: The destination for Intelligent Screening & Reporting in India (10-11-2023)

Hi @kowshick_kk ,

Some quarterly result are not getting populated.

For such example: NIBE Ltd financial results and price chart – Screener

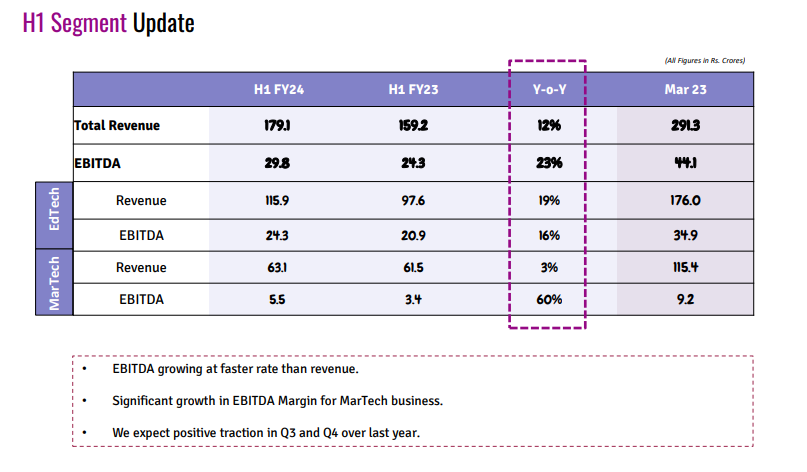

CL EDUCATE – Less Down side and unlimited upside (10-11-2023)

Please go through their latest Earning call . Edtech is generating EBITDA of ~16%.

They are organizing Investor day within next month.

@Saiyam_Jain : Please share pointers to back your statement. I might be missing something.

Kothari Petrochem Ltd~ A hidden moated small-cap company? (10-11-2023)

SUPER STRONG RESULTS BY KOTHARI PETROCHEM with EPS doubling & revenues growing by +20%

Company has reported strong Cashflows for H1 & its H1 Eps ~ FY23 EPS (which itself was at a higher base)

The company has been transitioning from traditional lower weight PIB to HR PIB, high molecular weight PIB and different grade variants from

main grade PIB products.

Further, its revenue base is diversifying with contribution from several other industries like Lubricants & masterbatches industry which itself reported strong nos this qtr (check Gulf Oil’s & Plastibends performance).

Overall, Outlook remains positive.