Pabrai fund has reduced stake in QE sep 23 by 1.87%. Can we assume that this the beginning of sale by Mr Pabrai . For him the buying price was substantially low.

Posts in category Value Pickr

CL EDUCATE – Less Down side and unlimited upside (09-11-2023)

Please study the business as a whole. There is also a martech division. And as Vineet ji pointed out above is part of the answer too

Stylam- Decent Fundamentals with Cheap Valuation (09-11-2023)

The company gave guidance that growth will slow down due to macros but margins will improve due to commodity prices stabalizing. This is actually very much in line with the guidance.

Will this Bull Market last forever? (09-11-2023)

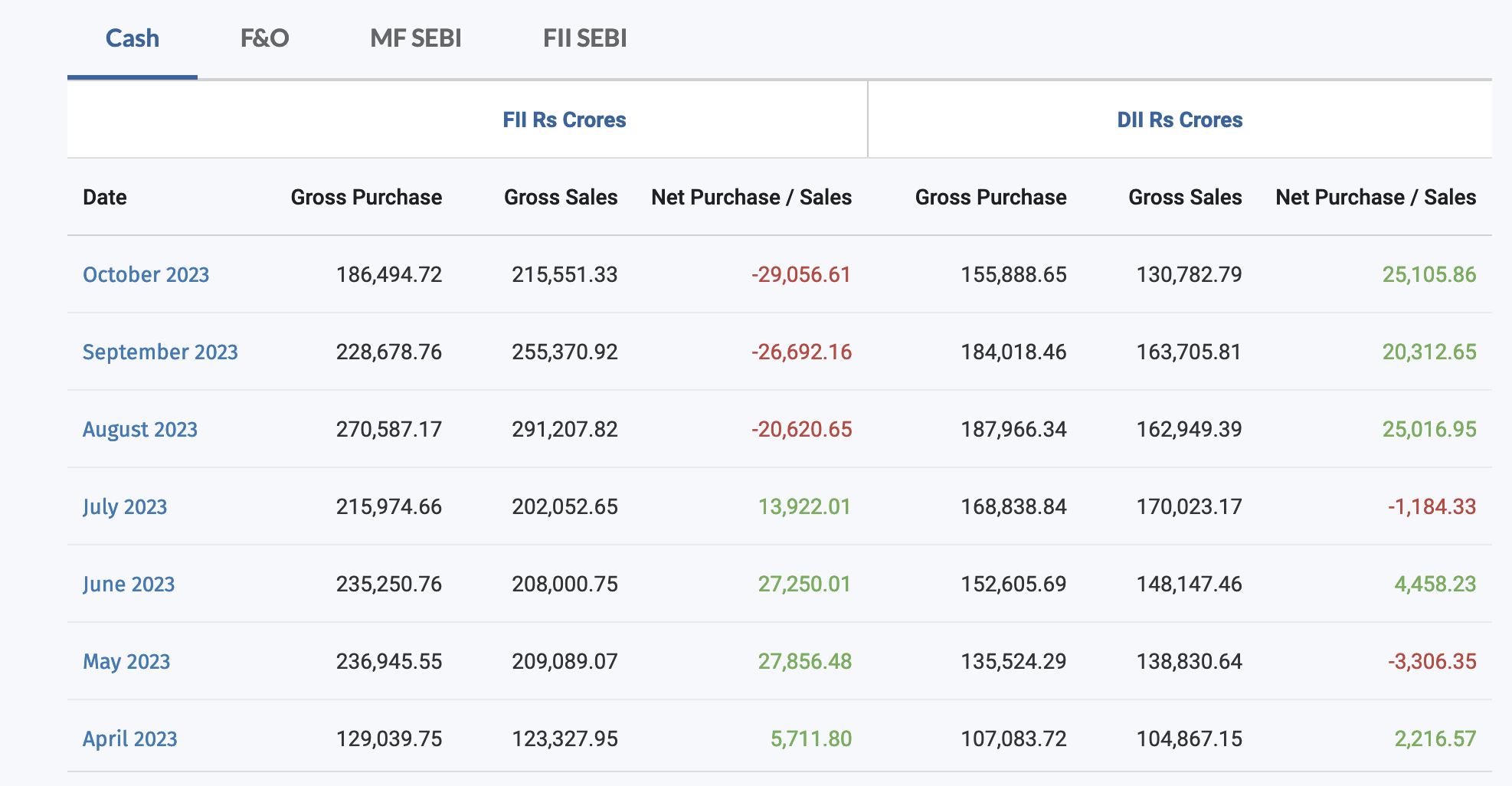

What is the source for your 2023 data?

Oh I meant FII’s selling starting this year, will edit the original post.

Garware Hi-tech films (Earlier Garware polyester) (09-11-2023)

Results are out, please go to the below link –

Almost no change in topline yoy and degrowth of 5% in bottomline.

You was right @phreakv6 their PPF line is operating at peak capacity backed by orders from US clients.

Also the company is debt free and has 350cr of cash which can utilised for expansion.

Disclosure – Invested and holding.

Megastar Foods – Food Processor from Punjab (09-11-2023)

Anyone tracking the stock ?

CL EDUCATE – Less Down side and unlimited upside (09-11-2023)

They run on franchise models where Company deals with different franchise partners.

It is through this model, they can maintain asset light model. Otherwise, it becomes opex heavy structure.

Prataap Snacks Ltd – Set for a crunchy bite! (09-11-2023)

Even Bikaji sales grew by merely 6% which has a much higher PE. Prataap Snacks stock is already very low and valuations are also reasonable. I think market is worried for a PE investor exit which becomes an overhang. That could be the reason as well

Rain Industries – An oversold de-leveraging play (09-11-2023)

The loan was taken for carbon business, however I understand your point that you expect Rain to sell Cement business to reduce debt sooner, Also the interest rate has increased form this quarter at 12.5%. we need to see how the company plan to reduce and what options they use. so far cement business was also earning profits. Since they have said there is no more capex and focus is on debt reduction that’s what we need to see in 1-2 years from now.

Jagan is a good capital allocator they have invested well when the debt had less interest rate, they should reap its benefits when market improves now… old investors should wait at least two more years to get clearer picture.

Thank you for bringing up these points,

Pricol limited – OEM automotive (09-11-2023)

Results are not that bad if we look into the tax component and the exceptional items component while comparing YoY. Personal view, invested and biased.