My sense is (and I could be wrong here) this is likely due to Bloom Energy pushing its order delivery dates to future. Situation in US is really difficult right now due to sky high interest rates which is choking new investments by all businesses and even putting current plans on hold. If it is indeed this reason then this pain will linger for next 2-4 quarters at least if not more. Let us see how market discounts this tomorrow.

Posts in category Value Pickr

Dynamatic Technologies – Can it be Dynamite (08-11-2023)

Why are the Npm’s so bad here. Completely dependent on other income. And why is inventory and Receivables so high. Combined almost 50% of Annual Revenues are stuck here. Have never checked this company before so any ideas on these.

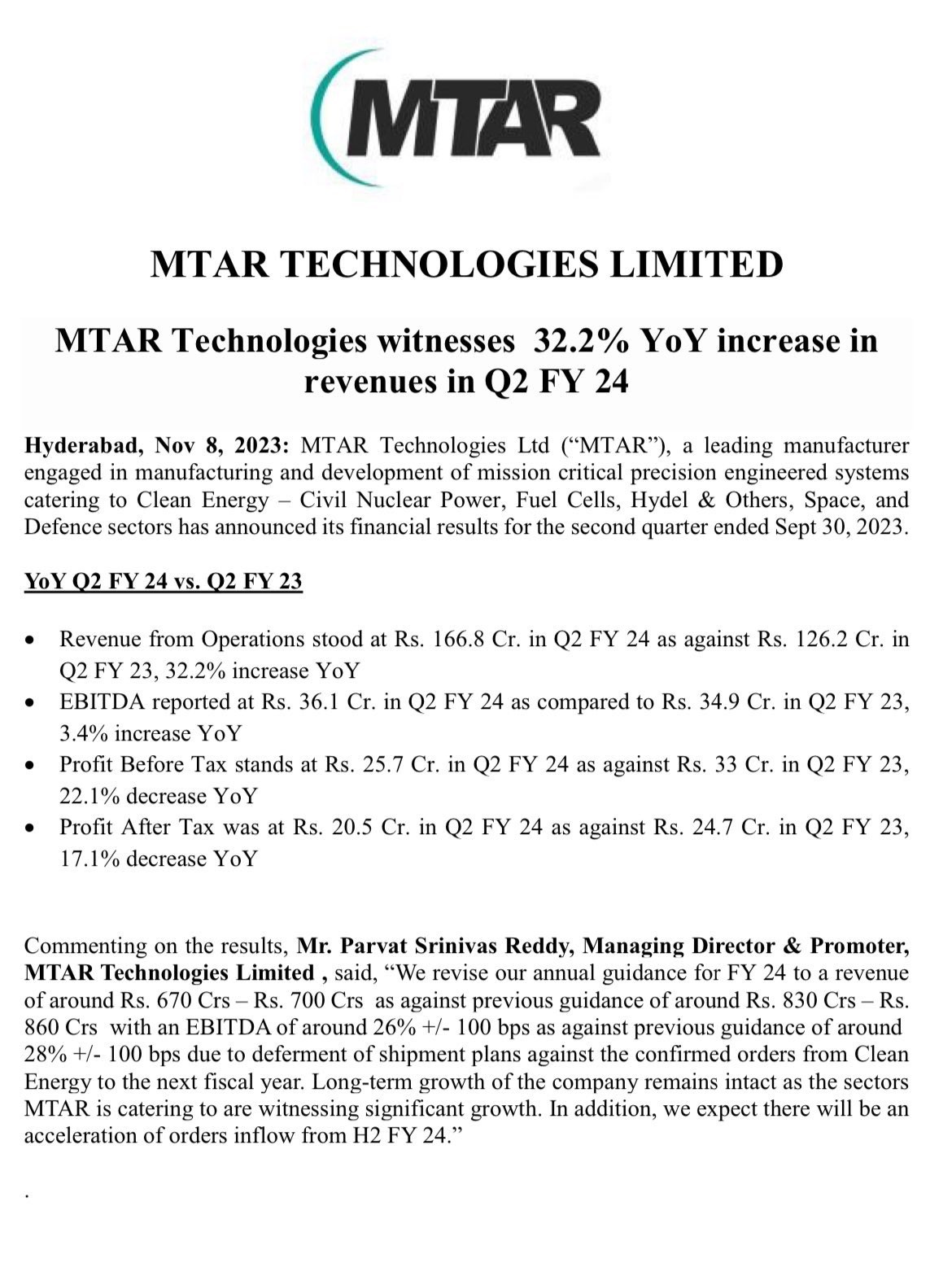

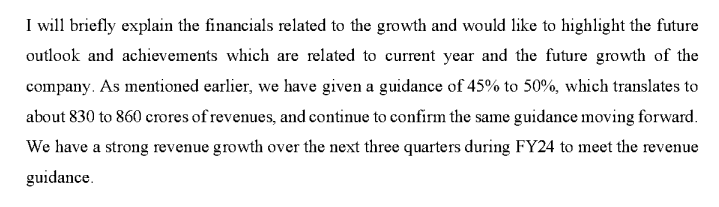

MTAR Technologies – A wager on innovation meeting economies of scale (08-11-2023)

First time since I followed MTAR from last 2 years seen revenue guidance missing this much. now 18% growth instead of 45%. Mr Reddy said this below in last Qtr concall. Not questioning company’s long term story here but little bit of faith on Mgmt is lost. I continue to hold and will add on dips.

Titan Company Ltd : a three decade old company (08-11-2023)

I have a question as Titan has 7% market share in the jewellery space, if I am right- when there is so huge scope for growth- why they entered in saree segment.

To be honest if people want saree , the brand name of Taniera doesnt appear.

Patel Engineering – A bet on India’s Infra growth (08-11-2023)

Q2FY24 Con-call highlights –

(+)

- Current order book – 20,000 crores.

- Received an order to work on India’s largest Hydro project.

- H2 is expected to bring better order inflow.

- The company currently handles 45% of the total hydro projects in India (Signifying dominance).

- There is tremendous potential in the sector going ahead.

- Share of tunneling projects to increase further (Better margins).

- Debt repayment is to happen throughout the next 3-4 years.

- Revenue growth guidance 15-20%.

- Expect an inflow of 150-200 crores through the Vivadh se Vishwas scheme.

- 90-95% price escalation is passed on to the clients.

- Debt reduction will consistently increase the net profit margin as interest costs reduce.

- H2 will be much stronger.

(-)

- Election year might temporarily hamper big order inflows.

- High debt remains a pinching point.

(i)

- 60% Hydro | 21% irrigation | 12% tunneling | road and others.

- 62% order inflow from PSUs | 35% state govt. | others.

Va Tech Wabag (08-11-2023)

Va Tech Wabag is to receive Rs 140 Cr which was a long pending issue

e3162352-9d89-4bbf-98e1-cb670fe004b4.pdf (1.4 MB)

PSP Projects – Construction Company (08-11-2023)

con call-November

Order Book and Order Inflow:

- PSP Projects Limited was awarded 9 projects in Q2FY24 and 14 projects in H1FY24.

- The outstanding order book as of September 30, 2023, was Rs.4,898 crore, with private projects comprising 48% and government projects comprising 52%.

- The company received an order inflow of Rs.175 crore during the quarter and Rs.934 crore during H1FY24.

- The company expects an order inflow of nearly Rs.3,000 crore in FY24.

- The company has a bid book of approximately Rs.6,500 crore.

Projects and Awards:

- The company completed 2 projects during the quarter, including a Surat Smart City Development Command Center and Adani Group’s school in Ahmedabad.

- PSP Projects Limited received awards for “Contractor of the year” and “Excellence in Construction Sector” during the quarter.

- Major projects in the bid book include AIIMS at Rewari, a museum project in Madhya Pradesh, and a commercial building in Delhi.

- The UP projects are expected to be completed by March 2024.

- The company aims to diversify its projects beyond Gujarat and has opportunities in states like Delhi and UP.

Financial Performance:

- The financial performance during Q2FY24 showed a 70% increase in revenue from operations, a 91% increase in EBITDA, and a 71% increase in net profit compared to the same period last year.

- The company expects to maintain a margin of 11% to 13%.

- The company has invested approximately Rs.165 crore in the precast facility.

- The cash and bank balance, including FDs, is approximately Rs.285 crore.

Closing Order Book:

- The order inflow for FY24 is expected to be Rs.3,000 crore.

- The closing order book is estimated to be around Rs.5,500 crore to Rs.6,000 crore.

Neuland Laboratories Limited – Transformation towards niche APIs? (08-11-2023)

Management is very conservative, however the statements given by the management reflects the positiveness of the business…

Score 10/10 in almost all parameters:

The YoY revenue growth of 43% driven by the CMS vertical is a culmination of the efforts we have put in over several years.

The EBITDA margin of 33.4% therefore is a result of not only the revenue momentum but also a shift towards high margin business. We continue to have good visibility from both businesses and

are focussed on executing according to our strategic plan.”

“The CMS business continues to grow on the back of both development and commercial projects in

line with our expectations. Even as the external funding environment is tight, our pipeline of CMS

projects is evolving as we have doubled the number of P-2 projects over the last year. We will

continue to invest in our capacities and capabilities in line with our commitment to serve customers

with agility.”

CMS segment

CMS revenues driven by commercial molecules. Significant contribution from molecules in the pipeline also

Prime segment

In Prime segment Mirtazapine and Escitalopram were the key molecules- H1FY24 Business and Financial Highlights

Specialty business

Specialty business driven by Paliperidone, Apixaban and Donepezil

Regulatory Audits US FDA inspected Unit-3 and issued EIR (Establishment Inspection Report)

Unit-I inspected by EDQM (European Directorate for the Quality of Medicines)

Free Cash Flow (FCF) generation and utilisation

Generated Free Cash Flow of Rs. 120.6 crores during H1FY24

Partly utilised to reduce debt by Rs 26.0 crores

Capex Investment of Rs 43 crores for enhancement of future overall capabilities.

Working Capital

Reduction in working capital cycle to 102 days in Q2FY24 as compared to 148 days in Q2FY23

The CMS business continues to grow on the back of both development and commercial projects in line with our expectations.

Even as the external funding environment is tight, our pipeline of CMS projects is evolving as we have doubled the number of P-2 projects over the last year. We will continue to invest in our capacities and capabilities in line with our commitment to serve customers with agility.

Steady shift from low margin Prime to high margin Specialty and CMS segments

• CMS business caters to Innovator customers on an exclusive basis, developing and manufacturing APIs/Intermediates in line with rigorous

customer expectations hence is highly concentrated in terms of customers

• Specialty segment works on complex products and technologies, hence has a focused approach towards select customers.

• Pre-clinical to P-3: Neuland generates revenue by process research & development as well manufacturing quantities for clinical trials

• *Pre-Reg/Reg: Phase-3 complete; Molecules filed but not yet commercial (Earlier labelled as ‘Development’)

• Commercial: Neuland generates revenues by manufacturing APIs for commercial novel molecules for innovators

• Steady trend in molecules transitioning from development stage to commercialisation resulting in increase in revenue from commercial products.

Focus Areas

29

Continue to invest in R&D capabilities and manufacturing technologies to attract more

RFPs while improving conversion rate 1

2 Lifecycle management of commercial products

3 Continue to focus on molecules in Phase II and later stages of development

4 Continue business development focus on biotech companies

5 Diversify geographic focus.

Went through the current concal 3 times to get the sense of current and future prospects. Management is crystal clear about its vision and capabilites.

Company is now debt free and started generating free cash flows. Management is conservative yet efficient in capital utilization.

Retailers shareholding has come down from 40.73% in Dec 22 to 35.08% in Sept 23 , however one good thing is that retailers are the largest shareholders… hope they will hold on for longer period to compound the benefit if Company continues to perform in this way.

Disclosure: Invested from levels of 1100 and further added today for very very long term as a coffee can investment. Views are biased.

Is Suzlon a turnaround story after FY16 (08-11-2023)

Great work and thanks for sharing your thought process.

I think most of us invested in Suzlon now have concerns on the valuations given the upper circuit it is hitting on almost every day basis!

In my personal view, in the short run (3-9 months) valuations can get in to extreme zones disconnected from the fundamentals. 4 broad a reasons for this could could be

- Stock is part of a broad narrative promising high growth

- Broad bull run in the market which results in most of us relaxing our strict valuation guidelines or throwing caution to wind and piling in the stock due to narrative and FOMO

- Operators playing with the stock

- Stock entering momentum category for traders to pile in which results in more momentum in the stock price which brings in even more traders and this becomes a self re-inforcing loop

Sometimes, these causes can play out in tandem which I think is happening right now in Suzlon.

During the covid bull run, I sold off many of stocks on concerns of overvaluation and then painfully saw them becoming multi baggers. It is this learning that has helped me stay invested this time through this over valuation zone.

Of course in the long run earning potential and price will converge…but we are here to make money and that may not necessarily always happen by sticking to our fundamental theories (especially for short 3-9 months time frame in a bull market).

Just my thoughts. Invested at lower levels and hence the risk of price crash does not worry too much at this stage and helps stay calm on valuation concerns in short run. No recommendations.

Is Suzlon a turnaround story after FY16 (08-11-2023)

Great work and thanks for sharing your thought process.

I think most of us invested in Suzlon now have concerns on the valuations given the upper circuit it is hitting on almost every day basis!

In my personal view, in the short run (3-9 months) valuations can get in to extreme zones disconnected from the fundamentals. 4 broad a reasons for this could could be

- Stock is part of a broad narrative promising high growth

- Broad bull run in the market which results in most of us relaxing our strict valuation guidelines or throwing caution to wind and piling in the stock due to narrative and FOMO

- Operators playing with the stock

- Stock entering momentum category for traders to pile in which results in more momentum in the stock price which brings in even more traders and this becomes a self re-inforcing loop

Sometimes, these causes can play out in tandem which I think is happening right now in Suzlon.

During the covid bull run, I sold off many of stocks on concerns of overvaluation and then painfully saw them becoming multi baggers. It is this learning that has helped me stay invested this time through this over valuation zone.

Of course in the long run earning potential and price will converge…but we are here to make money and that may not necessarily always happen by sticking to our fundamental theories (especially for short 3-9 months time frame in a bull market).

Just my thoughts. Invested at lower levels and hence the risk of price crash does not worry too much at this stage and helps stay calm on valuation concerns in short run. No recommendations.