Posts in category Value Pickr

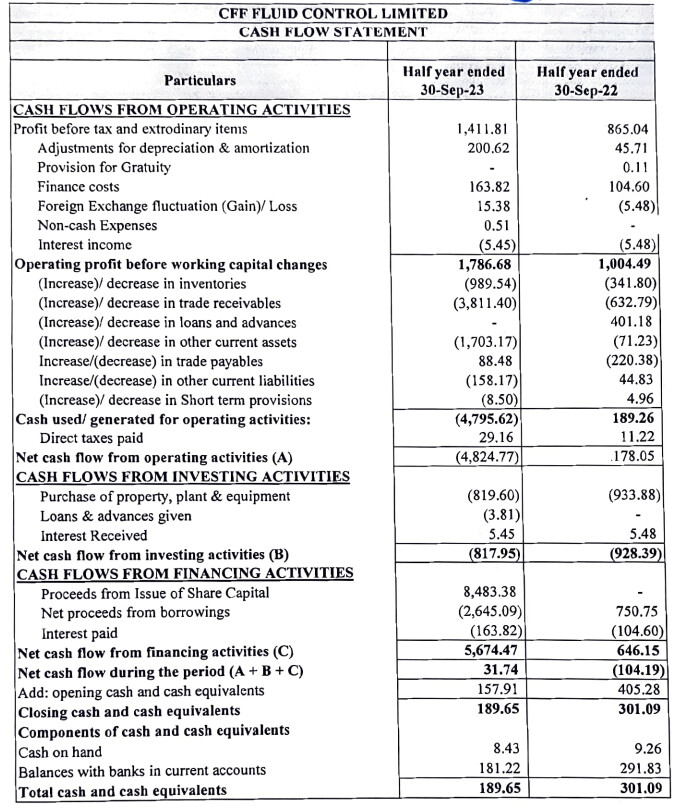

CFF Fluid Control Limited – SME (07-11-2023)

Very good results as expected.

But I feel the problem is cash flow.

Considerable increase in Inventories and majorly Trade Receivables. Cash generation is also necessary as much as Increase in Sales and Profits.

CDSL – Stock for our children (07-11-2023)

Earnings call for Central Depository Services (India) Limited, the points were discussed:

- Demat Account Growth: The management highlighted that they have seen a significant increase in the number of demat accounts, with a growth of approximately 55% in the second quarter. This surge in demat accounts is seen as a positive development for the company, contributing to its financial inclusion objectives.

- Long-term Approach: CDSL emphasized its long-term approach to business, focusing on creating a sustainable ecosystem and building the right building blocks for the future. The company’s goal is to ensure that more people have access to investing opportunities.

- Regulatory Changes: The management mentioned the regulatory changes proposed by the Ministry of Corporate Affairs (MCA) regarding unlisted public companies, which would require them to have demat accounts for their shareholders. They also emphasized that they have been ready from a technology and system point of view to accommodate these changes, with the timeline for implementation being September 2024.

- E-voting and eCAS Revenue: The company shared the breakup of e-voting and eCAS revenue for the quarter, with eCAS income at INR 7 crores and e-voting at INR 15 crores.

- Incentive Schemes: When asked about incentive schemes for private company opportunities, the management stated that they are transparent about their schemes, which are put out in the public domain. They emphasized that costs would depend on the technology infrastructure required and would be continually assessed to maintain high-quality service.

- Annual Issuer Charges: CDSL’s annual issuer charges have shown significant growth and the management discussed how this revenue was a combination of more private companies joining the ecosystem and an increase in the number of folios.

- Private Companies’ Opportunities: When asked about the proposed MCA regulations for unlisted public companies, CDSL pointed out that they are still analyzing the specifics, but the intention is to start with larger companies and expand the reforms over time.

- Expansion into Other Asset Classes: Regarding expansion into other asset classes, such as insurance, commodities, and mutual funds, the management indicated that they have created the right building blocks and are prepared for future developments in these areas.

- SEBI Charges: CDSL explained how SEBI charges are based on collections, not revenue, and that the fees are related to the previous years’ collections. They also clarified that it was challenging to predict the specific impact of IPOs on KYC income.

- Impairment Cost and Pledge Income: CDSL mentioned that impairment cost for the quarter was INR 3.3 crores, and pledge income was INR 4.19 crores.

- Market Share: The company’s market share in the KYC business was estimated to be around 65%.

- T+1 Settlement: The management acknowledged that SEBI was planning to implement T+1 settlement and expected SEBI to release circulars or discussion papers regarding this change in the future.

- Forward-Looking Statements: CDSL emphasized that they do not provide forward-looking statements and that many factors influence their income, making it challenging to pinpoint the exact source of growth.

Key Takeaways from the CDSL Q2 FY ’24 Conference Call:

1. Healthy Market Growth: The Indian capital markets showed robust growth in the second quarter of FY 2023-24, with increased demat accounts, total market capitalization, and daily turnover. This growth is attributed to increased participation by investors and recent industry advancements.

2. CDSL Milestones: CDSL celebrated its 25th year of operation and achieved a significant milestone of 9 crores demat accounts in July 2023. The company also received recognition for its excellence in digital execution, winning the TechCircle business transformation award.

3. Financial Performance: CDSL reported strong financial performance, with total income and net profit increasing on both a quarterly and half-yearly basis. The company’s focus remains on building value for stakeholders and strengthening the Indian digital financial ecosystem.

4. Factors Influencing IPO and Corporate Action Processing: The increase in IPO and corporate action processing is primarily market-driven. Higher numbers of IPOs in the market lead to increased processing activity. It’s difficult to provide a quantifiable breakdown of the contribution from different sources.

5. KYC KRA Business Growth: The strong performance in the KYC KRA business is attributed to buoyant market conditions, a growing number of demat accounts, and increased participation. The specific breakdown between fetch and creation is not provided.

6. Technology Costs: Technology costs are expected to remain a constant investment to support the company’s growth and infrastructure requirements. This investment is necessary to ensure CDSL can provide best-in-class performance and align with regulatory and market demands.

7. Other Expenses: Other expenses, excluding regulatory costs, increased in the second quarter, primarily due to expenses related to e-voting, consolidated account statements, and corresponding income levels. These expenses are expected to be incurred in the second quarter.

8. Private Companies Demat Opportunity: CDSL has an opportunity in dematerializing private companies registered with the Ministry of Corporate Affairs (MCA). While no specific timeline was mentioned, this represents a potential future growth area for the company.

Overall, CDSL highlighted its focus on long-term sustainability, financial inclusion, and market development while adapting to regulatory changes and preparing for future opportunities in various asset classes. The surge in demat accounts and revenue growth due to annual issuer charges and other factors were key highlights of the discussion.

Transpek Industry limited (07-11-2023)

Management had mentioned major destocking happening in Q1FY24 and this might be the spill over into Q2FY24. Need to wait for management commentary on this.

Natco Pharma: Focusing On Complex Products (07-11-2023)

I dedicated some time of my work life on FDA compliance. Generally FDA gives the observations to company first & later it is uploaded. In all faireness no company gives details of observations. They just mention # of observations which Natco has already done that.

Coming to observations, couple of observations looks serious. But it all depends on how good is their response to these observations. My personal view is that this will be an overhang for sometime and restrict its upside for sometime.

Sumedha Fiscal- A hidden gem? (07-11-2023)

Taken a small position just by because it’s price is below it’s book value and the dividend is good.

Hitesh portfolio (07-11-2023)

Hello Sir I’ve heard a lot about you.

I am a med student doing internship at Nair hospital Mumbai.

But since last 2 and a half years I am involved much more in investing and how to manage money.

I want to ask you sir how do you go about analysing a company, and as warren buffet said you should invest in business that you understand so I think that will be Pharma sector for me. So how would you go about analysing a Pharma company. How would you analyse a sector as well and their future prospects.

Others views re also welcomed.

Neuland Laboratories Limited – Transformation towards niche APIs? (07-11-2023)

https://x.com/vivekchadha1996/status/1721820705304777146?s=46

All time high revenue and margins, double the number p2 projects

Neuland Laboratories Limited – Transformation towards niche APIs? (07-11-2023)

c269f21b-fa18-4761-9130-ffc4d1a00fa6.pdf (1.3 MB)

Neuland Q2 results are good.