Will the co. be having a call to discuss the Q2 results…anybody having any info?

Posts in category Value Pickr

Aptus Value Housing : Is valuation justified or just another HFC? (05-11-2023)

Aptus continued with their growth trend (28% loan book growth, 23% in disbursement, 26% in interest income and 20% in PAT). They were facing some headwinds in Tamil Nadu due to higher attrition, where growth rates came down to 13% (vs 35%+ in other states). This problem seems to be normalizing now and they plan to maintain 25% loan book growth and add 30-35 branches annually (current branch count is 250). Concall notes below.

FY24Q2

- They increased SME loan rates by 50 bps in September 2023 and NIM growth trajectory will continue in next few quarters

- There was some attrition in Tamil Nadu at branch manager level which has affected growth (13% in TN vs 35%+ in other states). This problem has reduced recently and they are confident of reviving growth rates to 25% in FY24

- Growth strategy is always to go deep into a state and when going to a new state, start with places at border of the state nearby where they already have operations, and expand in a contiguous manner

- Always recruit local people for expansion

- Borrowing cost of NBFC is 25-50 bps higher than HFC (current borrowing cost is 8.25-8.3% for HFC)

- Will maintain spread of 8.5-9%

- Intend to add 30-35 branches annually

- Total pre-closures: 8% (5.5% from customer funds + 2.5% BT-out). According to my calculations, repayment/loanbook is 16% annually in normal times (e.g. Canfin) which translates to 4% quarterly. It becomes a problem when this increases to 20%. For Aptus, current quarterly number is around 4% which is fine

Disclosure: Invested (position size here, no transactions in last-30 days)

Krsnaa Diagnostics – what is the diagnosis? (05-11-2023)

Key Highlights of Q2 FY 24:

1.anagreement for the Assam Pathology tender, a significant opportunity that

encompasses 10 Labs and 1,256 collection centers. This development

significantly enhances our presence, covering all districts of Assam.

- Mumbai Facility: 15000 Sq Ft area in Kurla, current capacity 40000 tests per day, 6000 patients per day which is scalable upto 100000 tests per day, 15000 patients per day.

on Margin subdued on current quarter

Management reply: “It is important to acknowledge our profitability margins,

were impacted in comparison to the previous quarter. This impact can be attributed to the additional costs incurred for the on boarding of teams and operation and management of our newly established centers. We anticipate a positive trajectory in margins as these centers mature over the upcoming quarters.

SG Finserve Ltd – Does it has a scalable business? (05-11-2023)

About the Company Past – Management change

SG Finserve Limited (SG Finserve), originally established in 1994, has an NBFC license and is also registered as a SEBI broker. Earlier, SG Finserve provided a wide range of services associated with Broking, Distribution, Investment Research, Online Trading, Wealth management, Investment Banking and Insurance. However, the company had ceased to do any business in the recent past. The promoters, Mr. Rahul Gupta and Mr. Rohan Gupta acquired 56.25% stake in SG Finserve on August 20, 2021, post which an open offer was made which concluded on July 22, 2022.

Company Present

-

SG Finserve, an NBFC, was started to cater to the funding requirements of the dealers of APL Apollo Tubes and vendors of APL Apollo Tubes in its first phase of growth plans.

-

In the next phase of growth, SG Finserve intends to cater to the distributor network of the dealers.

-

In Q1 of fiscal 2024, the company has disbursed Rs 4207.6 crores and collected Rs 2964.9 crores in the same period. The AUM as on June 30, 2023 was Rs 1242.7 crores.

-

The APL group will extend support to SG Finserve in terms of details around the dealer network which would form a critical component of the underwriting process as well as enforce stop supply in the event of any delay from the network of APL Apollo.

Risk mitigation Techniques in lending

Typical lending companies take collateral to reduce risks.

Let us understand its risks

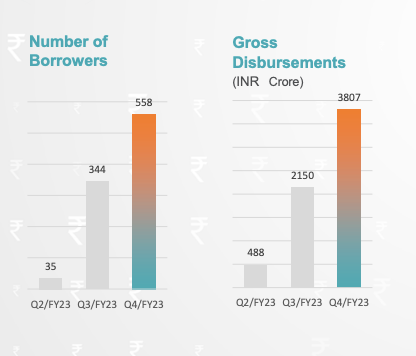

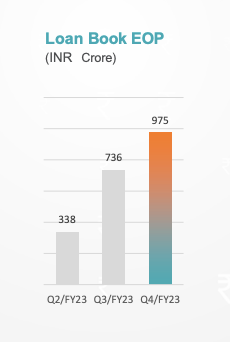

558 borrowers and 3807 Cr disbursements in a quarter. Definitely, it is huge concentration risk.

One way how they seem to be managing risk, is through reducing the duration of loan. As even after lending so much, there AUM is still near to 1000 Cr.

Other risk managing techniques taken by SG Finance →

Vendor financing – the NBFC will also provide bill discounting facilities to the creditors of APL Apollo Tubes Limited (AATL). The facilities offered will be for a tenor of upto maximum 90 days with an ROI of 11% to 15%. Here the risk mitigation resolves around the health of the AATL and no drastic increase in its payable days. Anyways, there is huge concentration risk on one company that is APL Apollo from vendor financing side but obviously they seem to be confident of their APL Apollo tubes business.

Dealer financing – AATL has a vintage of these dealers of over 3 decades and for the last decade the bad debts within AATL have remained within 0.2%(Source: Crisil credit report). Hence they seem confident of dealer financing.

Considering AATL(APL Apollo Tubes Limited) has the market dominance with 50 percent market share and is only manufacturer of certain tubes in the world(Source: Q4FY23 investor presentation). They have planned to use their dominance for recovery by stopping new supply of materials to the dealers.(Source: Crisil credit report)

Retailer financing(Not yet started it seems as per Q1FY24) – Here will be system integration and stop supply arrangements with the dealers wherein the dealers will also provide an FLDG of upto 20% for the loans given by SG Finserve. First Loss Default Guarantee(FLDG) means that initial upto 20 percent loss in loan needs to be taken by dealers who are giving the loans to the retailers.

Real Industry TAM And Growth

MSME lending is TAM is obviously huge but will they be able to manage risk same way as they are doing in case of dealers and vendors of the APL Apollo.

Total AUM potential in case of APL Apollo vendors and dealers –

Vendors –

Considering 40 payable days, payable turns = 365/40 ~ 9

Average Payable Amount = COGS/9 = 16000/9 ~ 1700

Annual AUM from the vendor invoice discounting = 1700 Cr

Considering the dealers and retailers also take the loans for similar period, hence total AUM potential = 1700*3 = 5400Cr.

Considering 1000 Cr current AUM through financing to dealers and vendors of APL Apollo, potential of 5400Cr AUM does not look big enough.

Though if it expands its business to vendors, dealers and retailers of other companies, its TAM might increase but will it be able to employ same risk mitigating techniques as it has now for its current customers?

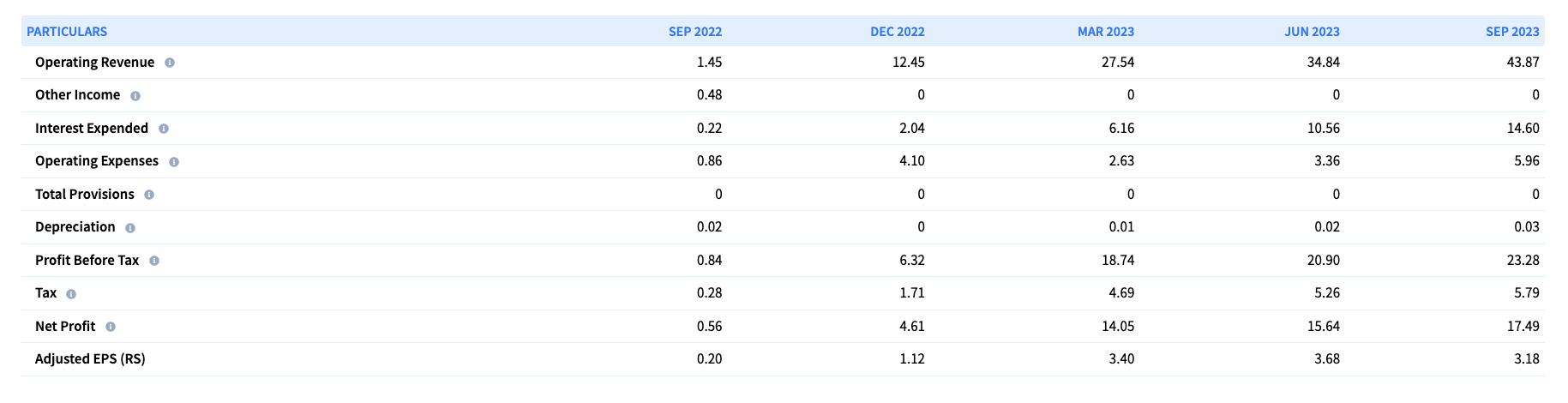

Financial Metrics

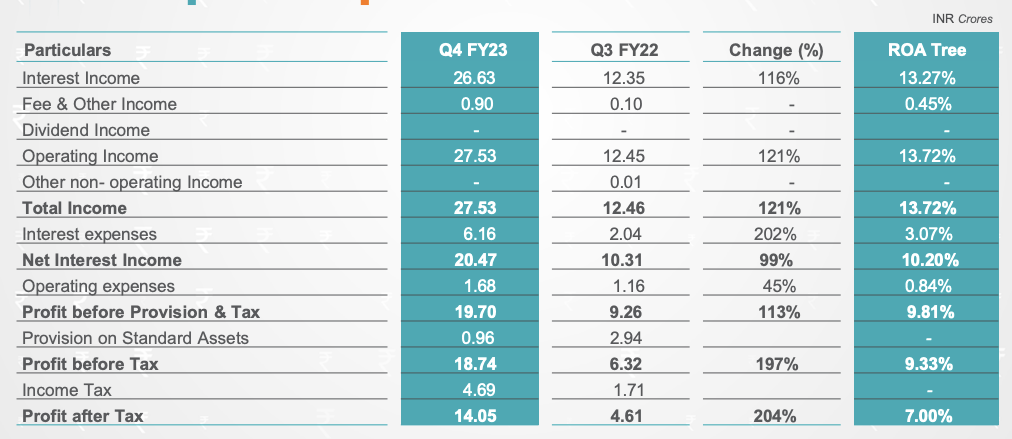

ROA Tree from Q4FY23

Current ROA(Annualised) as per Q2FY24 = 4%

They seem to be have very low gearing ratio which is understandable considering they are still testing their business which has led to low ROE.

Its current Equity is 759 Cr.

Here though again, we need to think, will it be able to scale its AUM maintaining similar risk profile to increase its ROE.

They have a good ROE potential if the scalability of the business considering the risk mitigation metrics can be ascertained as to increase the ROE they need to increase the leverage ratio(also called gearing ratio).

Source of Funds

Equity and some from banks under group entities corporate guarantee.

One interesting thing to research.

In their investor presentation they seem to show below page.

Where does these non group companies comes in the lending value chain?

Am I missing something?

I have not done the management analysis(though can be seen from APL Apollo Tubes thread). I have assumed the management is good considering APL Apollo parentage.

MOAT, Competitive analysis and Valuation comes after we can ascertain if their business is scalable which is still doubtful.

Disclosure – Not invested and please verify from your end.

Have not analysed many financial companies and hence the fundamental errors can there. Please correct if it is there.

Based majorly on CRISIL ratings.

Piramal Pharma Limited (05-11-2023)

PIRAMAL PHARMA Q2 results highlights –

Revenues – 1911 vs 1720 cr, up 11 pc

Revenues breakup –

CDMO – 1068 vs 940 cr, up 14 pc

Complex Hospital Generics (CHG) – 589 vs 562 cr, up 5 pc

India Consumer health (ICH) – 256 vs 227 cr, up 13 pc

Gross Margins @ 66 pc

EBITDA – 315 vs 219 cr, up 44 pc !!!

EBITDA margins @ 16 vs 13 pc ( significant improvement ). Margins in Q1 were a paltry 10 pc

PAT – 5 vs (-) 37 cr

Completed rights issue in Q2 for 1050 cr. Debt reduced by 958 cr to 3823 cr – thank GOD !!! . Need to do a lot more here in future

H2 is always better than H1 for the company. Q4 is the best

CDMO Highlights –

Have recieved 40 pc higher orders in H1 this yr vs LY. Newer orders have a good proportion of contract manufacturing of on-patent molecules

Contract manufacturing of Generic APIs – also doing well

Five of company’s CDMO facilities have successfully closed USFDA inspections since Nov 22 – Digiwal, Pithampur, Sellersville, Riverview, Lexington ( these contribute to half of CDMO revenues )

Current proportion of CDMO business involved in on-patent / NCE manufacturing / development at 44 pc vs 35 pc 2 yrs ago

CHG highlights –

Expanding capacities to meet the increasing demand for Inhalation Anesthesia products

Maintained leadership positions in Sevoflurane ( 44 pc Mkt share ) and Baclofen ( 76 pc mkt share ) in US Mkt

Have a product pipeline of 28 injectable products in various stages of development

Concluded USFDA inspection at Bethlehem facility which makes CHGs ( received 02 minor observations )

ICG –

Spent 14 pc of ICH revenues on promotions / Ads

Power brands include –

Littles – grew 19 pc in Q2

Lacto Calamine – grew 24 pc in Q2

Polycrol

Tetmosol

I-Range ( I-Pill, I- Can etc )

Power brands grew 15 pc in H1 and contributed to 42 pc of ICH sales

E- Comm grew 34 pc in Q2 and formed 14 pc of ICH sales. Have presence across 20 E-commerce platforms including own channel ( http://Wellify.in )

Have launched over 100 new products in last 3 yrs. New products launched in last 2 yrs form 20 pc of ICH business

Management comments –

Expect high teens YoY revenue growth in H2 with material EBITDA margin expansion. LY H2 EBITDA margins were around 16 odd pc !!! ( Extrapolation – suppose the revenue grows by 15 pc, EBITDA expands by 200 BPS – H2 EBITDA can be around – 810 cr. Full FY EBITDA to be around 1200 cr vs 840 cr LY – that would be a big Jump )

As innovation component increases in CDMO business going fwd, margins in CDMO business likely to expand over next 1,2,3 yrs

As ICH business crosses 1000 cr / yr revenues, margins here should grow incrementally every year. Currently, margins in single digits

Currently, road to deleveraging mapped via internal accruals. No asset monetisation lined up

Asst turns to improve substantially as revenues keep growing

Capex retirements to be also met from internal accruals

Company operates a total of 17 sites across the three businesses – helps de-risk the business. Also helps serve customer preferences

Mid 20s EBITDA margins are feasible in the medium term – Nandini Piramal

Current interest outgo @ aprox $ 44- 48 million/yr

Macro trends on biotech funding still not back to pre-COVID levels. Big Pharma spending is back

Currently, employee cost @ 27 pc of revenues. Likely to come down only when operating leverage kicks in

Medium term ROCE potential is about high teens – should be achieved as EBITDA crosses 23-24 odd pc

Innovator CDMO to outgrow generic CMO – in all probability

Disc – holding, biased, not SEBI registered

Ranvir’s Portfolio (05-11-2023)

Hi… I m still holding

Holding for a much better / improved Q2 performance

Fingers crossed

Tilaknagar Industries- Potential Turnaround Candidate (05-11-2023)

The company posted robust Q2FY24 resltus with 24%YOY growth and incresead margin of 13%

I dont know that growth prospects of brandy in india?

so,what are your views?

Ranvir’s Portfolio (05-11-2023)

PIRAMAL PHARMA Q2 results highlights –

Revenues – 1911 vs 1720 cr, up 11 pc

Revenues breakup –

CDMO – 1068 vs 940 cr, up 14 pc

Complex Hospital Generics (CHG) – 589 vs 562 cr, up 5 pc

India Consumer health (ICH) – 256 vs 227 cr, up 13 pc

Gross Margins @ 66 pc

EBITDA – 315 vs 219 cr, up 44 pc !!!

EBITDA margins @ 16 vs 13 pc ( significant improvement ). Margins in Q1 were a paltry 10 pc

PAT – 5 vs (-) 37 cr

Completed rights issue in Q2 for 1050 cr. Debt reduced by 958 cr to 3823 cr – thank GOD !!! . Need to do a lot more here in future

H2 is always better than H1 for the company. Q4 is the best

CDMO Highlights –

Have recieved 40 pc higher orders in H1 this yr vs LY. Newer orders have a good proportion of contract manufacturing of on-patent molecules

Contract manufacturing of Generic APIs – also doing well

Five of company’s CDMO facilities have successfully closed USFDA inspections since Nov 22 – Digiwal, Pithampur, Sellersville, Riverview, Lexington ( these contribute to half of CDMO revenues )

Current proportion of CDMO business involved in on-patent / NCE manufacturing / development at 44 pc vs 35 pc 2 yrs ago

CHG highlights –

Expanding capacities to meet the increasing demand for Inhalation Anesthesia products

Maintained leadership positions in Sevoflurane ( 44 pc Mkt share ) and Baclofen ( 76 pc mkt share ) in US Mkt

Have a product pipeline of 28 injectable products in various stages of development

Concluded USFDA inspection at Bethlehem facility which makes CHGs ( received 02 minor observations )

ICG –

Spent 14 pc of ICH revenues on promotions / Ads

Power brands include –

Littles – grew 19 pc in Q2

Lacto Calamine – grew 24 pc in Q2

Polycrol

Tetmosol

I-Range ( I-Pill, I- Can etc )

Power brands grew 15 pc in H1 and contributed to 42 pc of ICH sales

E- Comm grew 34 pc in Q2 and formed 14 pc of ICH sales. Have presence across 20 E-commerce platforms including own channel ( http://Wellify.in )

Have launched over 100 new products in last 3 yrs. New products launched in last 2 yrs form 20 pc of ICH business

Management comments –

Expect high teens YoY revenue growth in H2 with material EBITDA margin expansion. LY H2 EBITDA margins were around 16 odd pc !!! ( Extrapolation – suppose the revenue grows by 15 pc, EBITDA expands by 200 BPS – H2 EBITDA can be around – 810 cr. Full FY EBITDA to be around 1200 cr vs 840 cr LY – that would be a big Jump )

As innovation component increases in CDMO business going fwd, margins in CDMO business likely to expand over next 1,2,3 yrs

As ICH business crosses 1000 cr / yr revenues, margins here should grow incrementally every year. Currently, margins in single digits

Currently, road to deleveraging mapped via internal accruals. No asset monetisation lined up

Asst turns to improve substantially as revenues keep growing

Capex retirements to be also met from internal accruals

Company operates a total of 17 sites across the three businesses – helps de-risk the business. Also helps serve customer preferences

Mid 20s EBITDA margins are feasible in the medium term – Nandini Piramal

Current interest outgo @ aprox $ 44- 48 million/yr

Macro trends on biotech funding still not back to pre-COVID levels. Big Pharma spending is back

Currently, employee cost @ 27 pc of revenues. Likely to come down only when operating leverage kicks in

Medium term ROCE potential is about high teens – should be achieved as EBITDA crosses 23-24 odd pc

Innovator CDMO to outgrow generic CMO – in all probability

Disc – holding, biased, not SEBI registered

Krsnaa Diagnostics – what is the diagnosis? (05-11-2023)

Q2 FY 24 :97 Receivable Days H1FY24 (H1FY23: 87 days)

Varanium Cloud SME, the next Brightcomm Group? (05-11-2023)

I suspected that they will dupe the public with stories about forming data centres. Some news regarding this came in February although I didn’t find any Hydra web data centres in Google maps.