Posts in category Value Pickr

Dreamfolks services limited( DFS) (04-11-2023)

People like to get things for free. They will spend their time on Cred for hours to get free points rather than do something productive and buy whatever they need using money.

I believe airport footfall and credit card customers growth are key triggers for DFS stock.

Still it does not have any moat, in the end they are just middleman.

Great articles to read on the web (04-11-2023)

https://medium.com/the-post-grad-survival-guide/the-narrative-fallacy-9bb16c81457

Views on this article?

So should we not belive success stories of companies or strategies?

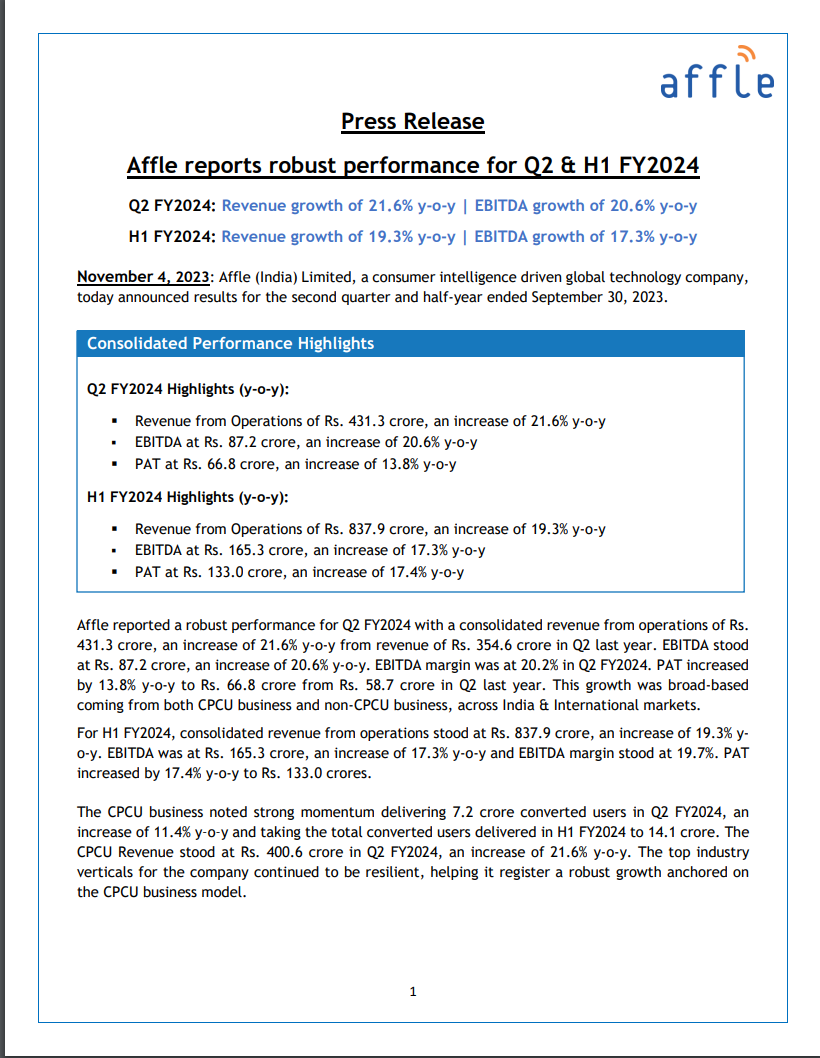

Affle India – India Mobile Internet Advertising Leader (04-11-2023)

Affle (India) Limited has reported robust financial results for the second quarter (Q2) and half-year (H1). Here are the detailed highlights:

Q2 FY2024 Performance:

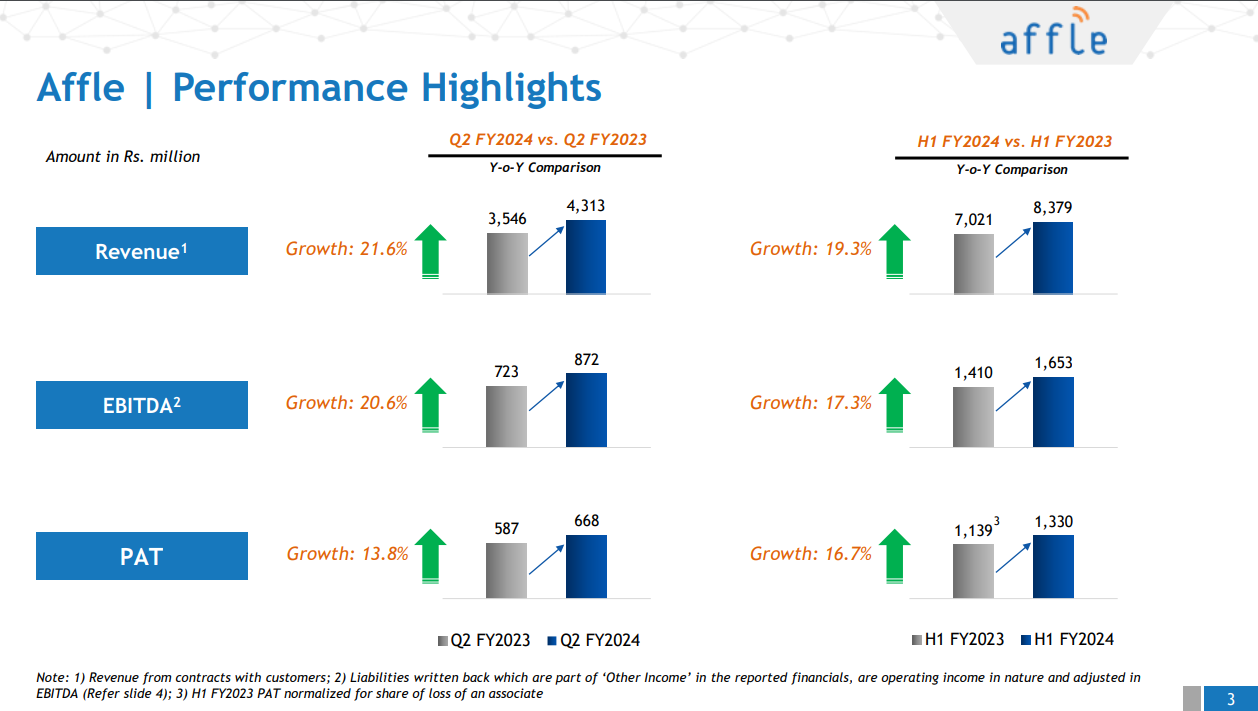

- Revenue Growth: Affle achieved a consolidated revenue from operations of INR 431.3 crore, marking a significant 21.6% year-on-year (y-o-y) increase compared to INR 354.6 crore in Q2 of the previous year. This indicates strong revenue growth.

- EBITDA Growth: The Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) for Q2 was INR 87.2 crore, showing a 20.6% y-o-y increase. The EBITDA margin was 20.2% in Q2 FY2024.

- Profit Increase: The Profit After Tax (PAT) increased by 13.8% y-o-y to INR 66.8 crore, up from INR 58.7 crore in Q2 of the previous year. This growth was driven by both CPCU business and non-CPCU business activities, spanning across India and international markets.

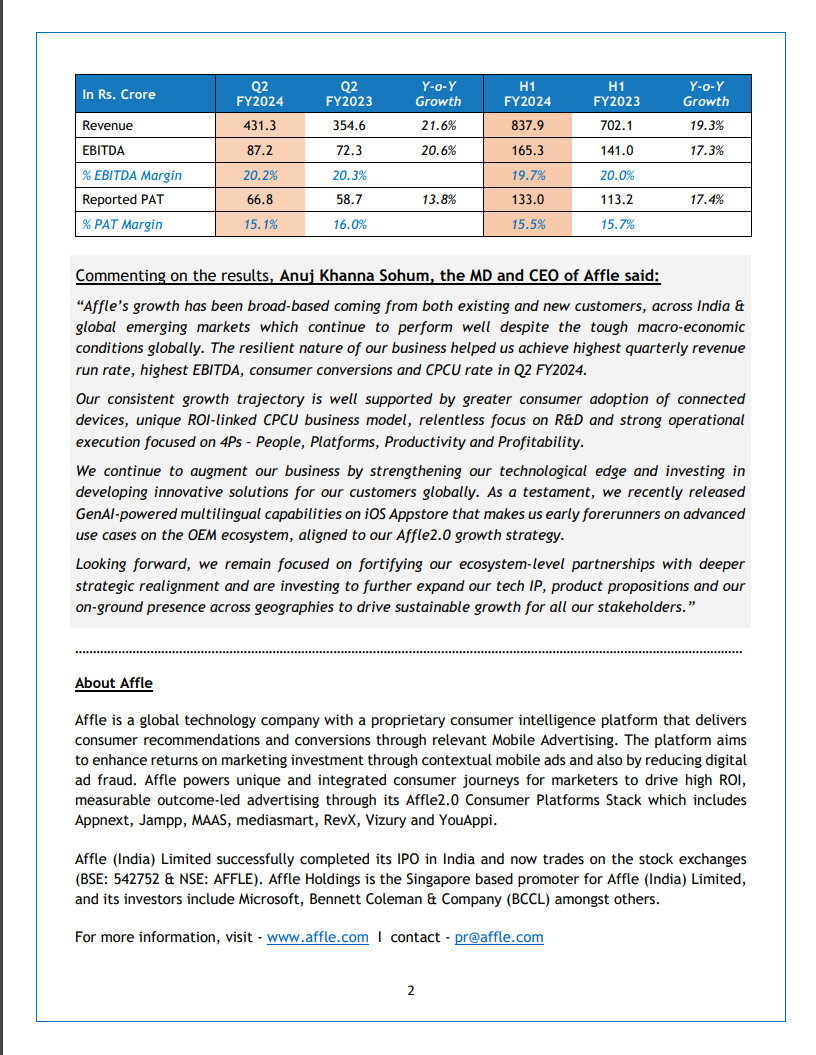

H1 FY2024 Highlights:

- Revenue Growth: For the first half of FY2024, consolidated revenue from operations amounted to INR 837.9 crore, indicating a 19.3% y-o-y increase. This demonstrates continued revenue growth.

- EBITDA Growth: EBITDA for H1 was INR 165.3 crore, marking a 17.3% y-o-y increase, with an EBITDA margin of 19.7%.

- Profit Increase: PAT for H1 increased by 17.4% y-o-y to INR 133.0 crore.

CPCU Business Momentum:

- The CPCU business showed strong momentum in Q2 FY2024, delivering 7.2 crore converted users, representing an 11.4% y-o-y increase. In H1 FY2024, the total converted users delivered reached 14.1 crore.

- The CPCU Revenue for Q2 FY2024 was INR 400.6 crore, an increase of 21.6% y-o-y. The company’s top industry verticals remained resilient, contributing to robust growth driven by the CPCU business model.

CEO’s Comments: Anuj Khanna Sohum, the MD and CEO of Affle, highlighted the company’s broad-based growth from both existing and new customers, both in India and global emerging markets, despite challenging global macro-economic conditions. He emphasized the company’s commitment to technological innovation, strengthening partnerships, and enhancing customer solutions to drive sustainable growth.

In summary, Affle (India) Limited has delivered strong financial performance in Q2 and H1 FY2024, with significant revenue and profit growth, driven by its CPCU business and a resilient business model. The company’s focus on innovation and expansion positions it for continued growth.

ValuePickr- Mumbai (04-11-2023)

Hi Folks,

It’s been a long time since this thread is inactive…!

Let’s Plan a meetup in mumbai .

andy161161 Can this be done again?

Atirek portfolio (04-11-2023)

Monthly Update

Sold goodluck India after management analysis.

I would have sold it much earlier but kept is little longer and sold it after the result near 850.

It is more about not painting the complete picture and the compensation of key members as percentage of the PAT since last three years.

Though it feels that management wants to build their business and keep putting money in the business which is good.

Their business in which they supply the tubes to the auto OEM is attractive and when they start becoming the category 1 supplier to the OEM, then obviously I might think again to buy.

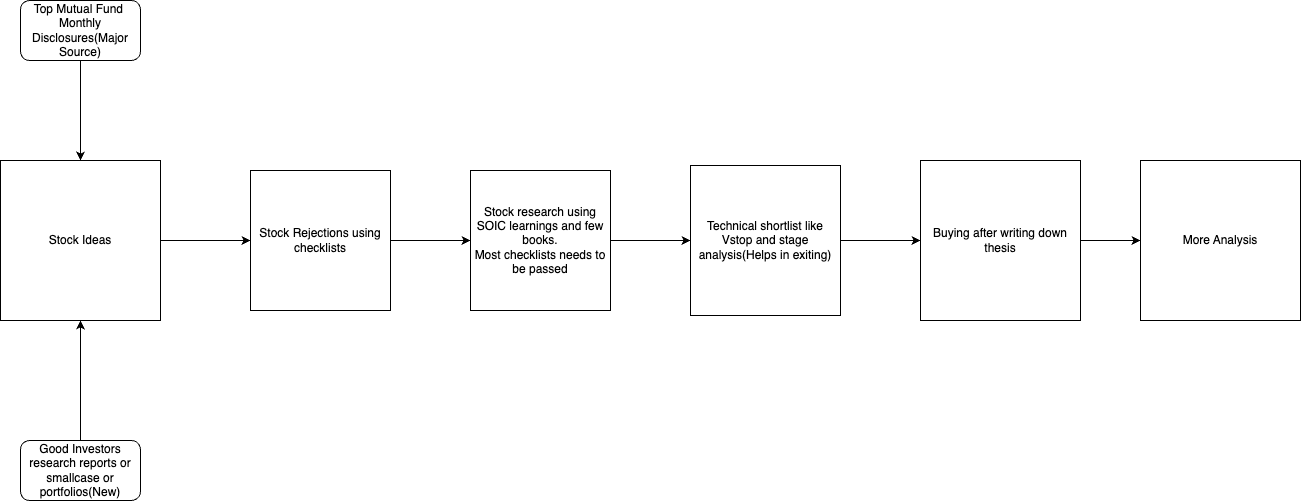

Updates in stock filtering process

Recently added another source of stock ideas.

Reminder to myself.

- Buy stocks only in tailwinds or the tailwinds can be ascertained in upcoming quarter or two.

- Also, when a sector performs, all stocks in a sector performs.

- Everyone has different goals in life and one should focus on his path instead of diverting from it even though you might find other’s path attractive sometimes. We should always question whether following others path will help you achieve your final goal, if not then why to be in FOMO.

Dreamfolks services limited( DFS) (04-11-2023)

Plus we should remember that most lounge service are available on payment of around 1.5k. So if one is so desirous of the lounge service service he can just pay for it, without needing the services of DFS, why bother keep up with joneses and spend 1L on CC.

Screener.in: The destination for Intelligent Screening & Reporting in India (04-11-2023)

The team/mgt behind Screener.in need to be complimented for doing such a marvelous job of creating & constantly updating a tool for investors that makes access to data so much easier & number crunching almost a joy! Not to mention the time one saves by not having to visit multiple sites to access all the data & then to tabulate it. What is more, perhaps 90% of folks using the site are probably not even paying for it! In this day & age, this is somewhat unprecedented & needs to be thoroughly appreciated.

Many a time we do not value something enough if we don’t pay for it!

InfoBeans Ltd – IT Solid Growth Story (04-11-2023)

Where is the concall link??? Did anybody attended

KPIT – CASE (connected, autonomous, shared, electric) – Focused Automotive Play (04-11-2023)

KPIT

While other ER&D Companies are posting flattish Growth, KPIT stands tall in this League. I want to Emphasize here that, the Capabilities which are developed by KPIT and its recent acquisitions provide a very qualitative view of what are the intentions of the company. The management is able to sense the need of providing V&V Platform (key focus area) and also other sw solutions for the current transition from ICE to EV or Hybrid.

Being from an Automotive Industry, the way KPIT is currently positioned, it seems the company is aiming at a One Stop Solution of Sw Development using Autosar, Unit Testing, Unit Level Integration, System Testing & System level integration of all Auto components which require a Sw Driven Control.

Point here is, use of Sw in EV’s is increasing not to just provide a excellent PowerTrain like was the case with ICE, but to provide differentiated User Experience that comes from integrated software.

Major parts of EV are Software (functions, OS, Middleware), Integration, V&V, ECU’s, Sensors, Power Electronics, other electronic Components.

Having said that, Major Expenditure is towards the top braket i.e. Sw, Integration, V&V.

This decides the time to market for a Project.

Now lets take an Example of Maruti. If a Maruti car (Swift), if the company needs to build an EV Swift Car, the most important part will be to develop a Sw Model suitable for all Different ECU’s (like Motor, Drive, EDU’s, BMS etc). Even though somehow the company manages to create a Sw the major challenge lies in the integration of this Sw will all Auto Componets (ECU’s). This is were KPIT is currently focussing on, which is building a Platform for Autocompanies to have a Integration and V&V Service available to reduce the Time to market.

Next comes the SDV (Autonomous Driving). Like where Tesla is currently operating, its very difficult for other OEM’s to catch Feature quality of Tesla cars. Millions of computations per sec in a Control System. This cannot happen without excellent Intergration of Products. (One example is the

Lately they are also colaborating with Chip Manufactures which will also be a key differentiator going ahead.

Management talks about, onboarding a Cutomer and then adding value to such a extent that they become a Deep Pocket client and then using Platforms to further expand in their other Projects.

They have also started to onboard clients from OffHighway segments, CV’s which talks about being a differentiator not only in Passenger vehicles but using PV Expertise to expand into other product segments. Moreover with the compliance standards like ISO-26262 and ASPICE, Sw Development is becoming more complex and process driven. One small Failure of Hw Sw Integration can delay a project by 6-9 months. As its easy to do changes in the Sw (within a short time) but very difficult to do changes in PCB’s i.e. HW where the V&V and Integration platform will be a key differentiator.

Holding since 2 years. Biased