Posts in category Value Pickr

Ceinsys Tech-Engineering, Geospatial & IT solutions Company (14-10-2024)

After going through this thread, AR, quarterly transcript n presentation I gotta these queries

How come their attrition is so low at 1% or so?

Why we have 2 CFO resignations in a matter of an year?

Negative working capital that too with government as their major client

CEO salary is more than 10% of company’s net profit

Geospatial sector – Sunrise Opportunity (14-10-2024)

Is Ceinsys Tech still a hold for long term considering huge run up for last few days or good to book profit?

TAAL Enterprise – cheap valueations (14-10-2024)

Notes from TAAL AGM 2024

- Growth has come from existing customers as well as new customer addition. Will continue to strike a balance. Intent has been to prioritise the growth of our capabilties and share with existing customers.

- Slowdown in growth rates attributable to sluggishness in the plant engineering business. See this turning around now.

- Business split currently at 50% Product Development & Engineering, 35% Plant Engineering, Rest from Construction Engineering. Split more or less same as last year.

- Customer count ~60+.

- Margin fluctuations: due to hiring in advance of employees being placed in projects, variations in onsite/offsite employees ratio. Confident of maintaining EBITDA margins in a band of 25-30%. More likely to be closer to 30%.

- Current employee count ~600. Manage this very carefully basis the demand that we see from our customers.

- No revenue guidance, setting internal targets and track them.

- This year, the softness in the growth has been because we’ve lost a couple of customers as they have been acquired. Identify this as a problem as TAAL primarily works with the middle tier of companies which are usually promoter driven and when the companies change hands, not in their control on continuity of the business.

- Not keen on defence space – prefer predictable revenue streams and businesses without payable concerns.

- Cash on books – deliberating utilizing of cash, yet to decide on it. Understand importance of improving return metrics and will take a call on this.

- Capabilities – new areas added – auto embedded.

- Capacities – looking to add more customers in existing domains or more capacities with existing customers.

While there has been no revenue guidance, do continue to see the employee count as a proxy to establish revenue growth and margins.

| Month | Oct 2022 | Apr 2023 | Oct 2023 | Apr 2024 | Oct 2024 |

|---|---|---|---|---|---|

| Employee Count | 550 | 657 | 697 | 679 | 635 |

| Delta over 6 months | – | 19.45% | 6.09% | -2.58% | -6.48% |

The slowdown/degrowth in employee addition trends are in line with the revenue trends and margin profile trends as the lower employee costs are getting absorbed over the same revenue base recently.

Disc: Tracking. Not invested.

Ugro Capital – Opportunity To Invest in a Fintech-like Company Below Book Value (14-10-2024)

How can we acess arihant report.

Sudarshan Chemicals – Can it colour our portfolio green? (14-10-2024)

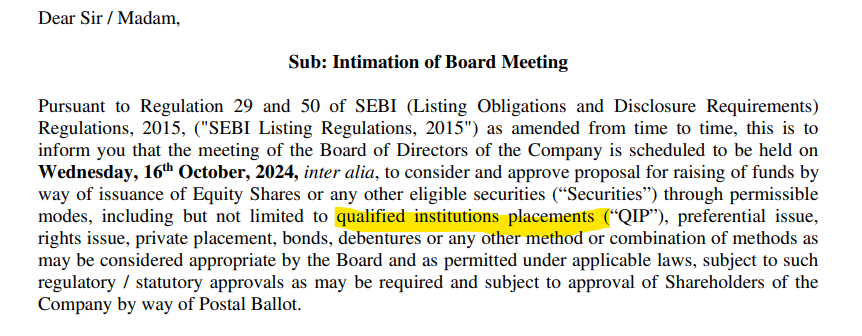

Management looking to raise funds

Vishnu Chemicals – Is Growth sustainable? (14-10-2024)

As per SEBI regulations, at least half of the board of directors shall comprise of independent directors, where the listed entity does not have a regular non-executive chairperson.

Vishnu Chemicals’ board comprises of more than 50% independent directors, which is in full compliance with the regulations. Moreover, CMD’s son as Joint MD gives clarity on succession.

As per the best international corporate governance practices, role of chairman and managing director should be split. However, most of the family owned companies in India have not done it. Also, this is more important for larger companies. While this may not be the best CG practice as per global norms, but well inline with the practical aspects in India. This is not a red flag situation.

As per the best international CG practices, shareholding should not be concentrated. However, many investment gurus give significant importance to promoters’ skin in the game with majority shareholding. In my opinion, many Indian companies with significant promoter stake have done very well at the same time there are only handful of Indian companies with dispersed shareholding having such track record.

Zomato – Should you order? (14-10-2024)

I think a profit margin of 5 percent is not optimistic. Actually a bear case profit margin would be 5 percent. An optimistic bet would be 12-15 percent. And base case 8 percent.

Shakti Pumps – solar shakti (power)! (14-10-2024)

Company hasn’t won any big orders recently and the MH order will keep exhausting. Probably the reason why the guidance of 30% increase in topline with results frontloaded in q1 and q2.

Morever, there were a few tenders of KUSUM C which they did not win. So management commentary would be vital. The PE looks optically lower if 30% topline growth target for the FY YoY is maintained.

Va Tech Wabag (14-10-2024)

i am only concerned about shareholding pattern , it is easy to manipulate by big players as public holding is more than 60%