Posts in category Value Pickr

See the bright Sun: Aditya Vision (04-11-2023)

AVL Q2 FY24 Result and Concall highlights

Amit Singh Learning page (04-11-2023)

Aditya Vision Q2 FY24 Performance

Performance in Q2

| Q2FY24 | Q2 FY23 | YoY % | |

|---|---|---|---|

| Rev | 315.6 | 260.14 | 21.3% |

| Expense | 303.28 | 245.72 | 23.4% |

| Gross Profit | 12.32 | 14.42 | -14.6% |

| GM% | 3.9% | 5.5% | 1.6% |

| PAT | 9.63 | 11.35 | -15.2% |

| PAT % | 3.05% | 4.36% | -1.3% |

No of Stores State wise (130):

Bihar – 97 stores

Jharkhand – 20 stores

Uttar Pradesh – 13 stores

-

Zero Store closure since inception

-

No Private labels are sold at Aditya Vision Store

-

Customer Service Strong Financial Management

-

Aditya Seva – One-stop solution for after-sales services.

Aditya Seva – One-stop solution for after-sales services. -

Aditya Suraksha – Allows customers to enjoy an extended warranty

-

Customer Loyalty Reward Program – Buy & Win since 2012

-

Operates on a cash-and-carry model

-

Efficient inventory management, (Inventory of Rs. ) for festive season and Q1 FY25

-

High cash reserves of Rs.

-

Avg Capex per Store is ~60 Lakhs

-

Avg period for break even of new store is 8 months.

-

Avg Working Capital per store is Rs. 2.25 Cr

-

Revenue per SqFT is ~Rs. 40,000/-.

-

Employee cost and Rent Cost at 3% of Sales.

-

Quarterly tentative Share of revenue based on FY19 to FY23 trend:

-

Q1 30% – Summer season led by marriage and AC sales

-

Q2 18% – Lowest due to monsoon and shradh

-

Q3 28% – Propelled by Festive and Marriages

-

Q4 24% – Marriage, Pre Summer sales, End of year sales by brands

-

Target to grow at 20-25% CAGR, by reinvesting cashflows at higher ROIC for next 3-5 years in hindi heartland.

-

Electricity consumption grew by 2 times in Bihar/UP/Jharkhand:

Electrical appliance ownership:

| % of house hold owning TV,Fridge,WashingMachine | AC owners | |

|---|---|---|

| UP | 15.70% | 2.40% |

| Bihar | 3.70% | 4.0% |

| Jharkhand | 6.20% | 2.1% |

| Chattisgarh | 7.90% | 0.9% |

| Odisha | 7% | 1.5% |

| WB | 4.80% | 3.4% |

Concall highlights:

-

Entire festive season has fallen in Q3 FY24, Good growth in revenue is expected. Electronic loan mela in Panchayat/ Block level for rural customers in Bihar/ UP/ Jharhand has got great response.

-

Aug and Sept sales were robust with >20% growth.

-

Bihar revenue share 81%, Jharkhand 8%, UP2% (new stores)

-

Expansion is steady opening of stores. Open 10-15 additional store 145 Store to be opened in FY24.

-

Earlier guidance of 150 Stores by FY25 end is revised to 160-165 stores. Southern in saturated market new market is the hindi heartland.

-

Inventory remain on the higher side in Q2 and Q4 as AVL does not want to face a stock out situation in Q1 and Q3 seeing the best demand during these times. Q2 inventory is at Rs. 283 Cr

-

30% stores are less than 6 months old. Going forward they will achieve the break even and add to profit.

-

ESOP of Rs. 2.5 Cr given to employees.

-

OPM has gone down by 1.2% YoY, new store opening has its impact on this %. With new stores maturing in next few quarters this will normalize.

-

Very Bullish Q3 is expected.

-

AC business has grown by 30% in H1.

-

18 Smaller store out of 130 rest are larger. Going forward larger stores are in focus for volume business.

-

Retail financing is helping big time in this store success. Plenty of money inflow from Outside Bihar is also one aspect along with improved electricity consumption.

-

Cashflow from operation has increased. Rs. 97.78 Cr Q2 FY vs Rs. 21.77 Cr. Q2 FY23.

-

Because big investors wants to buy large number of shares promoters are to sell from their share as the share is very illiquid. Post listing on NSE in FY25 this issue may get resolved when at a bigger platform it is traded.

-

No Private brand selling at AVL stores.

Omkar’s Portfolio Analysis and Discussion (04-11-2023)

I dont think any amount of time spent from my side will increase my circle of competence in following ideas. I will have to rely on – past track record and past management actions to invest in these companies which gives me some idea of risk played out. Its very difficult to predict any future growth where I dont “critically”understand core subject.

Chemistry

For me – it is very difficult to understand any chemistry and make future predictions using it. No amount of hard work can change this position which arises out of core incompetency. Only company falls in my investment universe is Vinati Organics purely based on past track record

CDMO

From late 2020, suddenly my timeline was flooded with these 4 letters. Life was peaceful before that. I am inclined towards – easy to understand branded plays : branded generics and hospitals. So far results are ok

ER&D and small mid cap IT companies

Can not crack uniqueness in business model for different IT companies. The only way i can play IT sector is through dividend yield of large cap names. 5-6% dividend yield is my entry point

Any sun rise sector – electronic manufacturing, defence, renewables etc

Will invest in future when track record is established

Companies showing only p and l growth without commensurate cash flow growth for whatever reasons

Trying to build FOMO buffers. I am inclined to give up short term gains for the uture benefit. The problem for me is including these companies may make funnel wide open which will increase chances of getting Calital Loss candidate included along with future multi bagger candidate. Better to look at these companies in bear market

Diversified groups

Can not align with them. No regrets on missing out

Any Lenders including tier 1 banks

Cant go beyond Basket of tier 1 financials.

Change in business models or management

Will invest in future when track record is established

Special situations

Will invest in future when track record is established

Omkar’s Portfolio Analysis and Discussion (04-11-2023)

I dont think any amount of time spent from my side will increase my circle of competence in following ideas. I will have to rely on – past track record and past management actions to invest in these companies which gives me some idea of risk played out. Its very difficult to predict any future growth where I dont “critically”understand core subject.

Chemistry

For me – it is very difficult to understand any chemistry and make future predictions using it. No amount of hard work can change this position which arises out of core incompetency. Only company falls in my investment universe is Vinati Organics purely based on past track record

CDMO

From late 2020, suddenly my timeline was flooded with these 4 letters. Life was peaceful before that. I am inclined towards – easy to understand branded plays : branded generics and hospitals. So far results are ok

ER&D and small mid cap IT companies

Can not crack uniqueness in business model for different IT companies. The only way i can play IT sector is through dividend yield of large cap names. 5-6% dividend yield is my entry point

Any sun rise sector – electronic manufacturing, defence, renewables etc

Will invest in future when track record is established

Companies showing only p and l growth without commensurate cash flow growth for whatever reasons

Trying to build FOMO buffers. I am inclined to give up short term gains for the uture benefit. The problem for me is including these companies may make funnel wide open which will increase chances of getting Calital Loss candidate included along with future multi bagger candidate. Better to look at these companies in bear market

Diversified groups

Can not align with them. No regrets on missing out

Any Lenders including tier 1 banks

Cant go beyond Basket of tier 1 financials.

Change in business models or management

Will invest in future when track record is established

Special situations

Will invest in future when track record is established

Screener.in: The destination for Intelligent Screening & Reporting in India (04-11-2023)

I do find some disconnects in Screener.in… I will post here if I come across something …specific .Thx

Screener.in: The destination for Intelligent Screening & Reporting in India (04-11-2023)

I do find some disconnects in Screener.in… I will post here if I come across something …specific .Thx

Akash Portfolio (04-11-2023)

Thanks Akash, Understood. Actually I was not sure whether it would have a any adverse effect on the company profile/stock eventually if company looses the cases. By the way I also found this information in DRHP only.

Akash Portfolio (04-11-2023)

Thanks Akash, Understood. Actually I was not sure whether it would have a any adverse effect on the company profile/stock eventually if company looses the cases. By the way I also found this information in DRHP only.

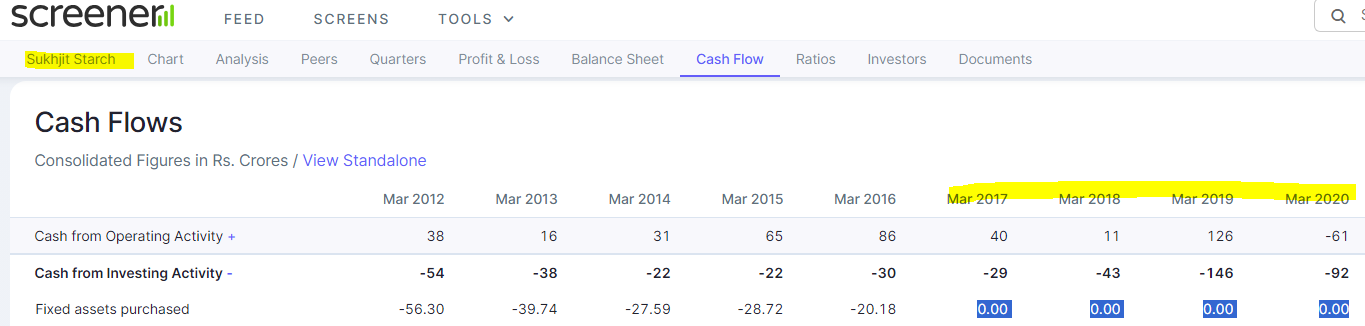

Screener.in: The destination for Intelligent Screening & Reporting in India (04-11-2023)

Thanks for the revert. Another one for your consideration:

Capex numbers are wrong for Sukhjit [Sukhjit Starch & Chemicals Ltd financial results and price chart – Screener] from FY17 to FY20: