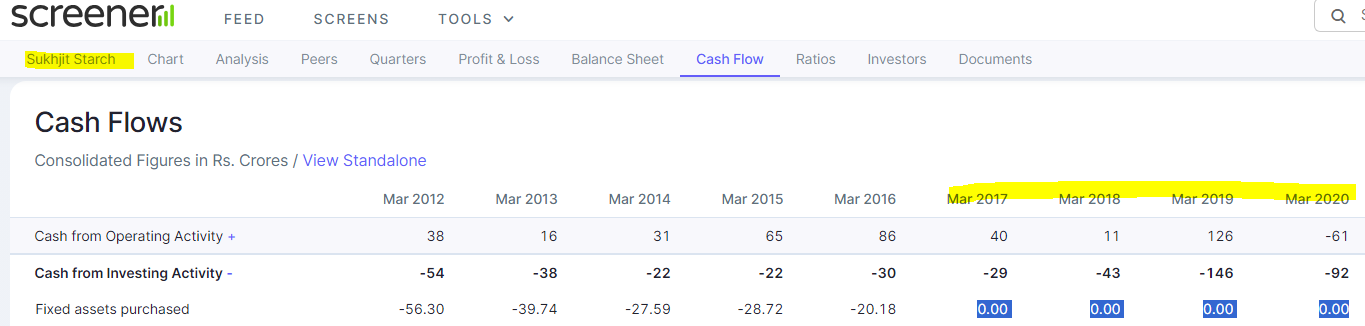

Thanks for the revert. Another one for your consideration:

Capex numbers are wrong for Sukhjit [Sukhjit Starch & Chemicals Ltd financial results and price chart – Screener] from FY17 to FY20:

Thanks for the revert. Another one for your consideration:

Capex numbers are wrong for Sukhjit [Sukhjit Starch & Chemicals Ltd financial results and price chart – Screener] from FY17 to FY20:

Fine Organics — Q2 FY’24

Fine organics posted their results for Q2 FY’24. The market did not react well after which the stock slumped by about 12-15%. This post is my take on the results. I would love to hear all of your opinions on the same.

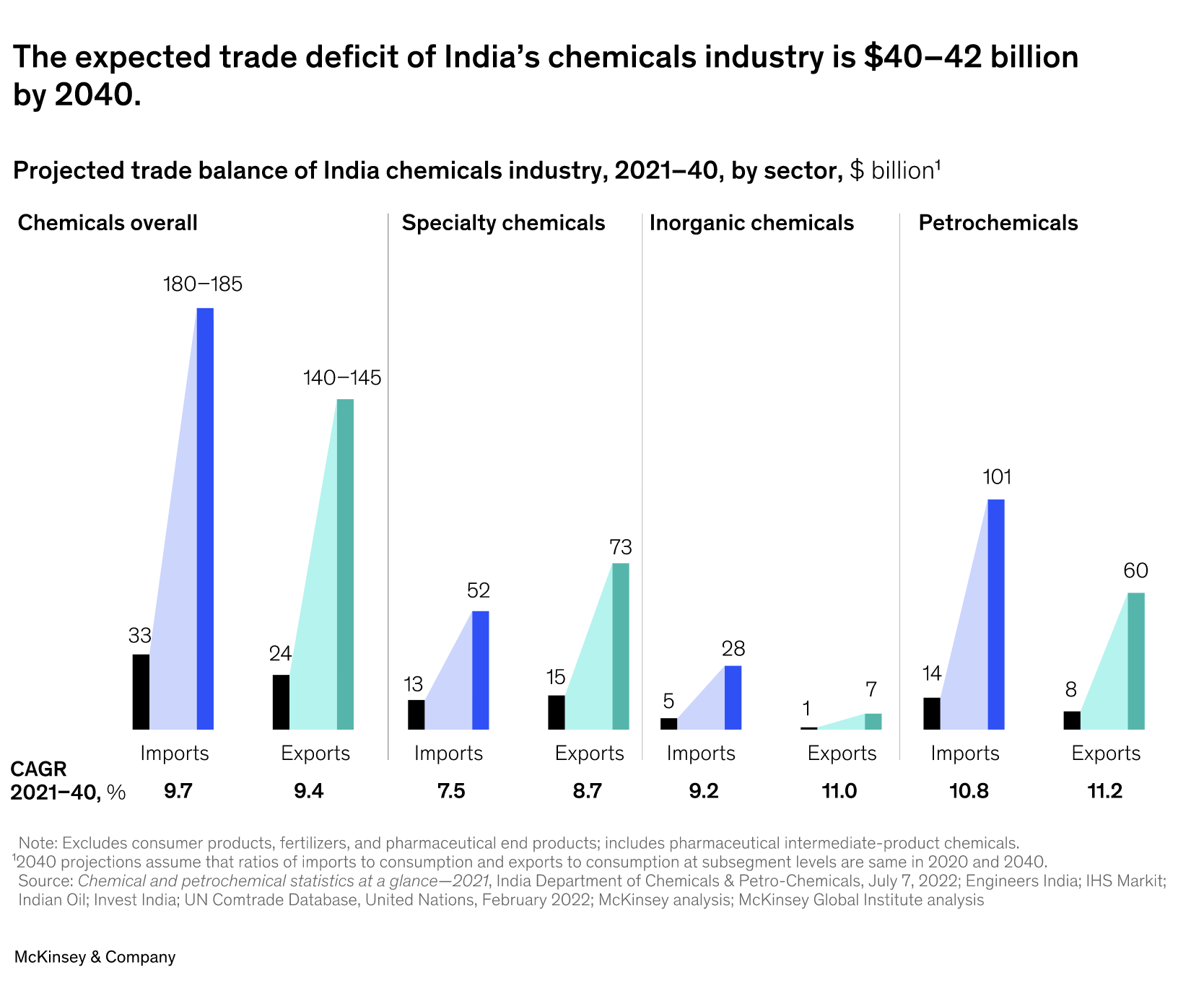

Chemical sector prospects (India):

What about the Indian Oleochemicals market?

Sectoral conclusion:

Fine organics is very well placed sector wise. Its long term growth and demand still looks to be in-tact. Export markets will be key. While this brings in more prospective business opportunities, it also adds more external factors to account for like trade barriers and policies.

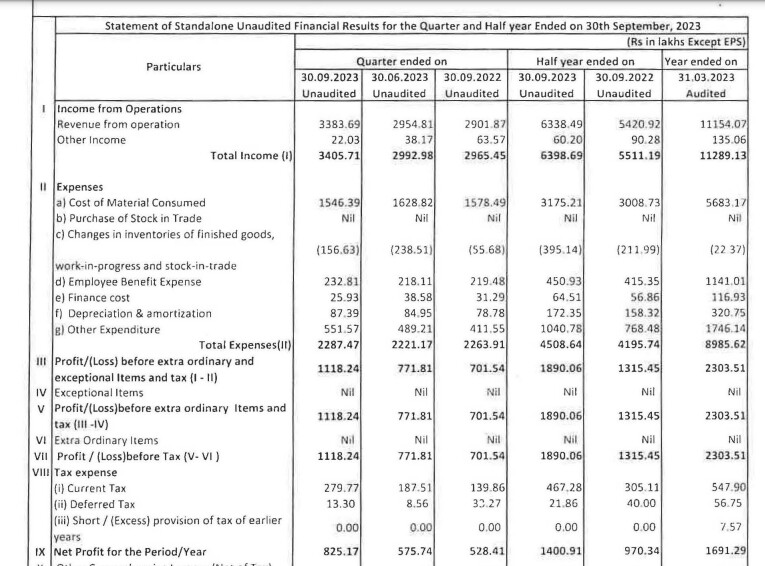

Results – Q2 FY’42

Summary (standalone):

On the face of it, the results look disappointing.

Let’s dig slightly deeper:

Over the last few months, China has been dumping stock, especially chemicals. That has predominantly happened due to low demand in their home economy. And as is well known and is well covered, that there is a lot of slowdown in the Chinese economy. And they are trying to fight that in terms of exporting more and more, especially at rock bottom prices or predatory pricing, which basically has impacted a lot of commodity players. With the aftermath of Covid and companies looking to derisk and diversify, Indian companies look attractive. But again, here, we are more skewed towards specialty chemical players. These players are much higher up the value chain vis-à-vis a commodity play which is price led. We prefer players which are higher up the value chain. Now the demand has improved in China, and when this happens the intensity of predatory pricing or dumping will recede and we expect it to happen in the coming months.

Inventory destocking: A quick glance at the financial result will quickly tell you that the company has a positive change in inventory of Rs 26Cr. Compare this to Q2 FY’23, the company had a negative change in inventory of Rs 12Cr. Chemical companies often go through stocking and destocking cycles. Stocking occurs when companies increase their inventory levels (for example anticipated demand), while destocking occurs when companies decrease their inventory levels (for example to reduce costs, decrease in demand). It looks like the destocking cycle has slowly started to end and stocking cycle has begun to take presence across the sector. It’s not a sudden process but takes a few quarters to play out.

General demand slowdown: India’s doing comparatively well but due to a general slowdown in demand globally (especially in the larger economies), export oriented sectors like chemicals are experiencing a bad cycle.

Margin contraction:Over the past 7 quarters (standalone), OPM margins have clearly contracted. With a mean quarterly OPM of 25.4%, the current quarter Q2 OPM is sitting at its lowest in the last 7 quarters at 22%. Can the margins contract more? That is a high possibility, due to the fact that even with declining input/raw material cost the company will have to pass on the benefits to its customers. But as demand starts to return we could see a reversion to mean OPM and beyond. At-least it’s good to know that we are somewhere closer to the bottom of the cycle than the top.

Market expectations for the quarter: Beaten market expectations comfortably

Capex/expansion problems: the non-availability of land for further expansion as of now is a cause of concern in the short to medium term with plants running at optimum utilisation. Only Capex due to commission in Patalganga, as mentioned earlier in the thread was expected to reach full capacity by Q4’FY24 but I could not find if any updates on the timeline. Inorganic expansion opportunities are limited.

Delay in Thailand Joint Venture (JV): However once started and functional should contribute significantly to the toppling numbers.

Valuation

PE: Currently trading at a PE of around 30. The valuation has worsened due to the bad numbers. 5 year median PE stands around 40-45, but it’s not far off. Another bad quarter and you’re headed your way there. So the company is definitely not undervalued as of now.

PEG: Currently at 0.63 which looks like the current PE is justified for now. However, the PEG has been increasing for the last few quarters definitely showing that growth is slowing down faster than the price is dropping. This could signify that the down-cycle was factored in fairly early.

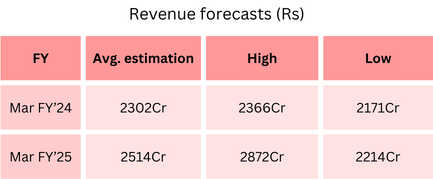

Market estimations for FY’24 and FY’25

Does not look like there is going to be a fast uptick coming immediately. The coming quarters will be key in identifying bottoming out patterns both technically and financially. Keep an eye out on the margins and PE. Hopefully you found this helpful.

Hi @Surender Few banks like CUB, Yes bank, Indusind bank were reporting their Balance in the older format on their Annual result filings. As the breakup of several line items was not available, we couldn’t update the Balance sheet.

We will be updating the same once the Annual report of the company is published.

The company has performed really well in this quarter.

In terms of margins as well as topline.

Is anyone still tracking this company?

What are your analysis on this quarter’s result?

Hey, Thanks for your suggestion. I will share the same with our team for consideration.

We do provide the Industry, BSE & NSE code as a default column on the downloaded columns for our premium users.

Hey, Our team is working on quarterly payment options as well. We will try to roll it out in the coming days. I hope this might help you in exploring the premium features.

chrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/https://www.nuvamawealth.com/ewwebimages/WebFiles/Research/7a451846-8b10-4341-93e2-b3ac96c134c5.pdf

(post deleted by author)

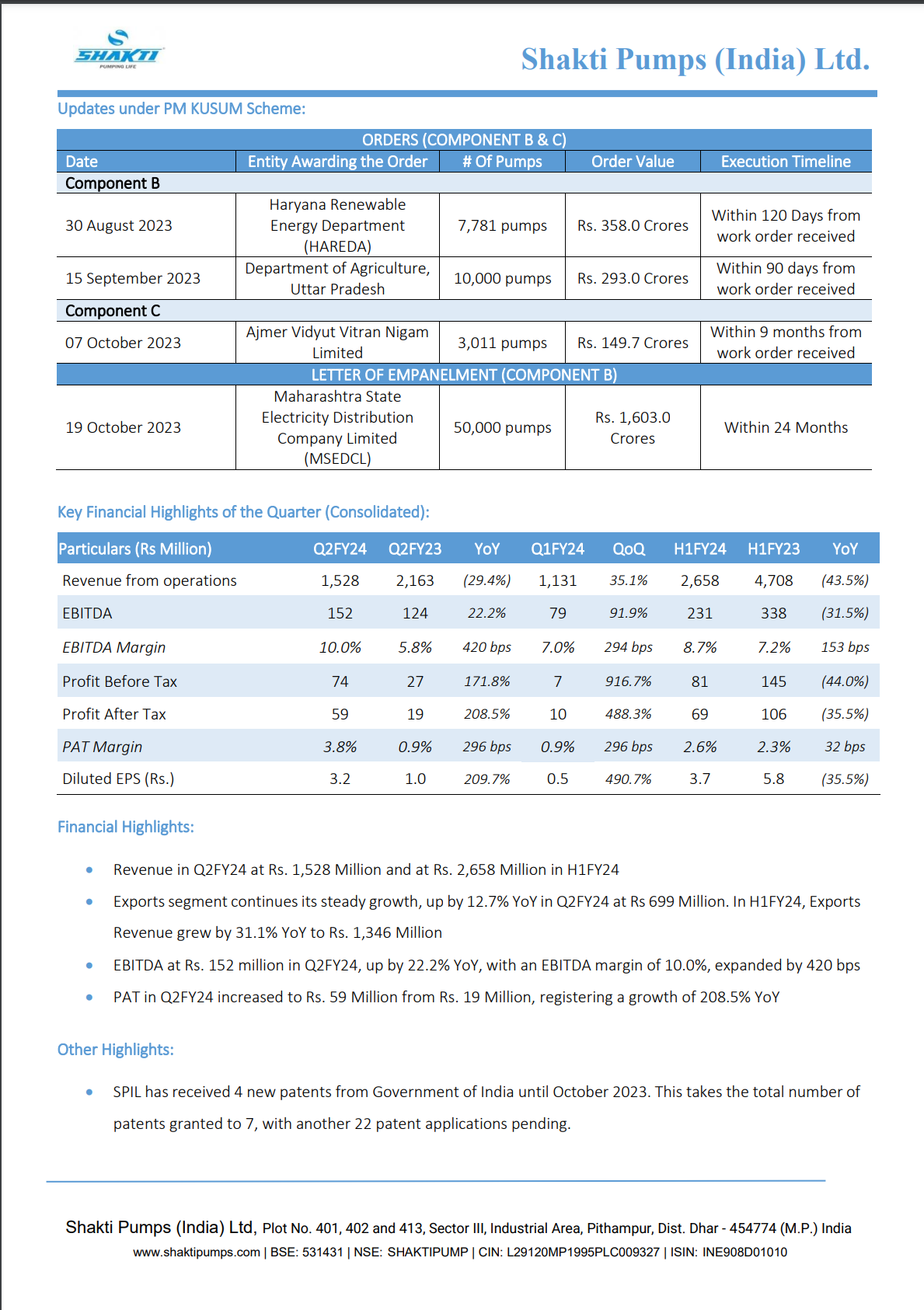

Shakti Pumps Limited, a prominent manufacturer of stainless-steel submersible pumps, pressure booster pumps, pump-motors, controllers, and inverters, released its financial results for the quarter and half-year ending on September 30, 2023. The company’s Chairman, Mr. Dinesh Patidar, highlighted the significant achievements and developments during this period in a letter addressed to the Listing Department of the National Stock Exchange of India Ltd. and the Corporate Relationship Department of BSE Limited.

The key points from the letter and the financial results are as follows:

Key Developments:

Financial Highlights:

Other Highlights:

In summary, Shakti Pumps reported a successful quarter and half-year with substantial orders under the PM KUSUM III Scheme and advancements in technology, including patents and investments in the EV industry. The company anticipates a strong business upturn in the coming months.

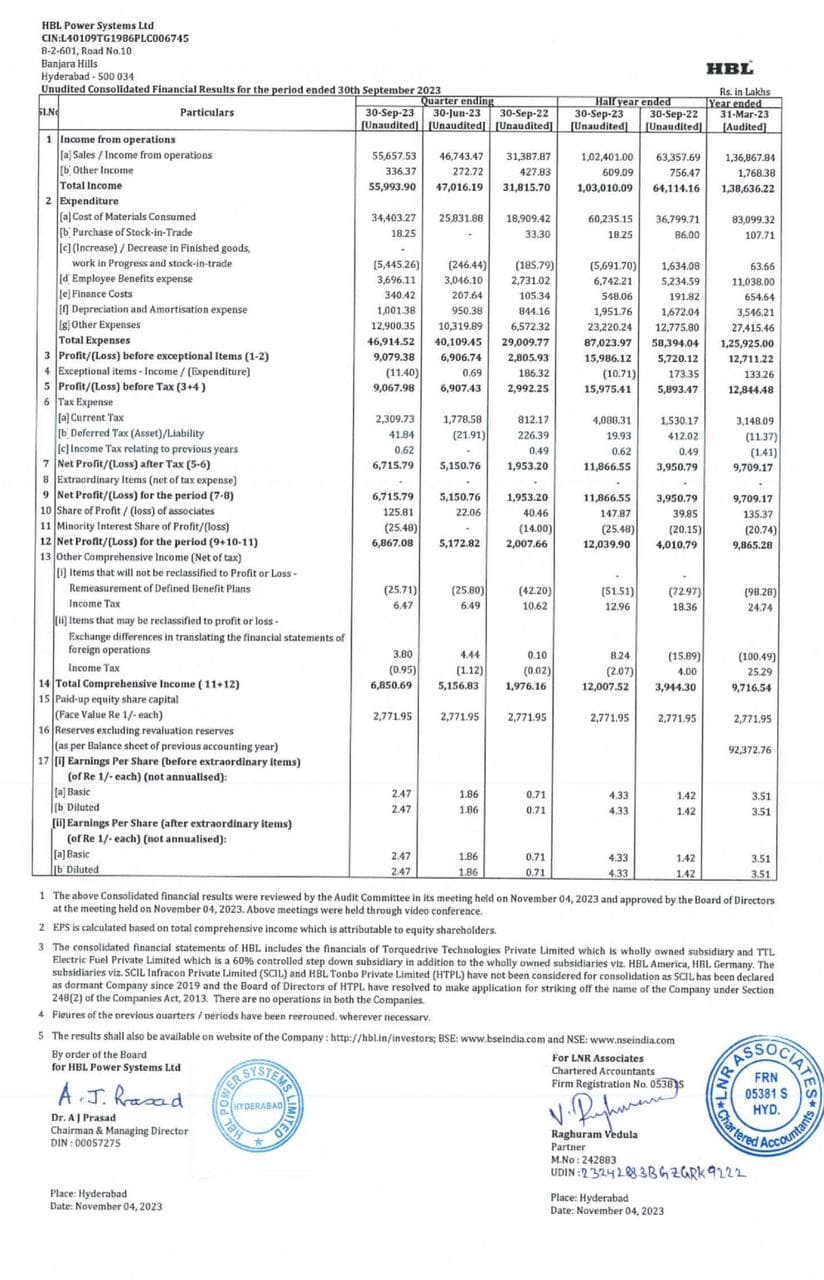

Hbl power blockbuster nos