Fair chances they may have more information than other small retail participants. Be patient if you are cloning them. Don’t exist due to market volatility unless they reduce stake substantially. Superstar’s stocks can fall too (20,40 even 80% if its SME ). Keep eye on bulk deals if stake is below 1% you may find buy information in bulk deals data.

Posts in category Value Pickr

Starting off with Value Pickr (02-11-2023)

Hi All,

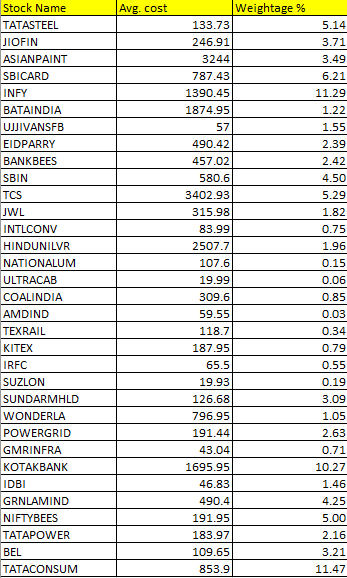

I am a Finance Professional with 15 years’ experience across various industries. I started with my investment journey 5-6 years back, however started seriously only recently as I decided to make this a full time career… My Portfolio is as below… and these stocks are subject to re-balancing.

Hope to receive feedback if any. I am still learning and some of the picks are experimental as I strongly believe you won’t learn something permanently without learning it in hard way (Means you must burn your hands first)

Open to questions

Connect me on Linkedin – linkedin.com/in/sankarmadhavan

Thanks

My portfolio – Srinidhi (02-11-2023)

Do we have a method or how you arrived at valuation of each individual stock?

I mean basically how do you “value” a stock? I know it is tough to follow a single method – If you can provide at least some thought/guidelines if would be helpful.

Thanks

Investing Basics – Feel free to ask the most basic questions (01-11-2023)

Mold Tek does not have pricing piwer. Mold tek budiness practise is that allows it to earn good margins.

When you work with like of Asian Paints or Nedtle or something and you are intermediary you do not have pricing power. They will just hung yku dry to last drop to increae their margins.

What boxes they pack, others can also pack.

What they do to pack those boxes, others casnot do easily.

This is not mold tek thread, so will not discuss further.

Disc: not invested

Infosys Limited – Are we getting a discount or no? (01-11-2023)

Notes from Infosys Q2FY24 concall.

Revenue growth is low at 2.5% YoY in constant currency terms which has slowed down due to global slowdown which includes low spending towards digital transformation and slow decision making by clients.

Except manufacturing vertical, management sees uncertainty of growth pick up on all other verticals.

Management reduced the guidance for FY 24 revenue growth to 1% to 2.5%. It was previously 1% to 3.5%.

Operating margin was 21.2% which increased by 40 bps over the last quarter. Cost optimization and better utilization led to the margin increase.

FY 24 compensation hikes are going to be rolled out from November 1st. It means Q3 and Q4 margins may be down unless utilization improvement compensates for it.

Current utilization is at 80.4% (including trainees). In past the company has managed to bring it up to ~82.5% which happened in FY22. Net headcount is negative compared to last quarter.

All in all a dull quarter apart from headroom to improve utilization slightly. Growth in NA and in BFSI are key factors to watch out for.

Peter Lynch defines a “stalwart” business as a large, mature business growing earnings at 10% to 12% with negligible debt (from his book “One Up on Wall Street”). In my opinion, this is a classic example of a business that fits in the bucket of a “Stalwart”. I feel comfortable getting into Infosys either when the growth comes back or when it falls significantly below its 10-year PE of ~25.

Just an opinion, I could be wrong.

Cheers,

Mahesh

Praveg Ltd: Play on Indian Tourism Industry! (01-11-2023)

Exactly my thoughts. Though it is unfortunate that Praveg didn’t communicate well regarding this deal, I would jump to conclusion that it is a fraudulent management, like some members did in the comments above.

- Maybe just biased because I am invested, 11% of my PF.

MCX and Financial Technologies (01-11-2023)

UBS gave an upgrade today. But why isnt it being valued at higher multiples?. BSE trades at much higher multiples

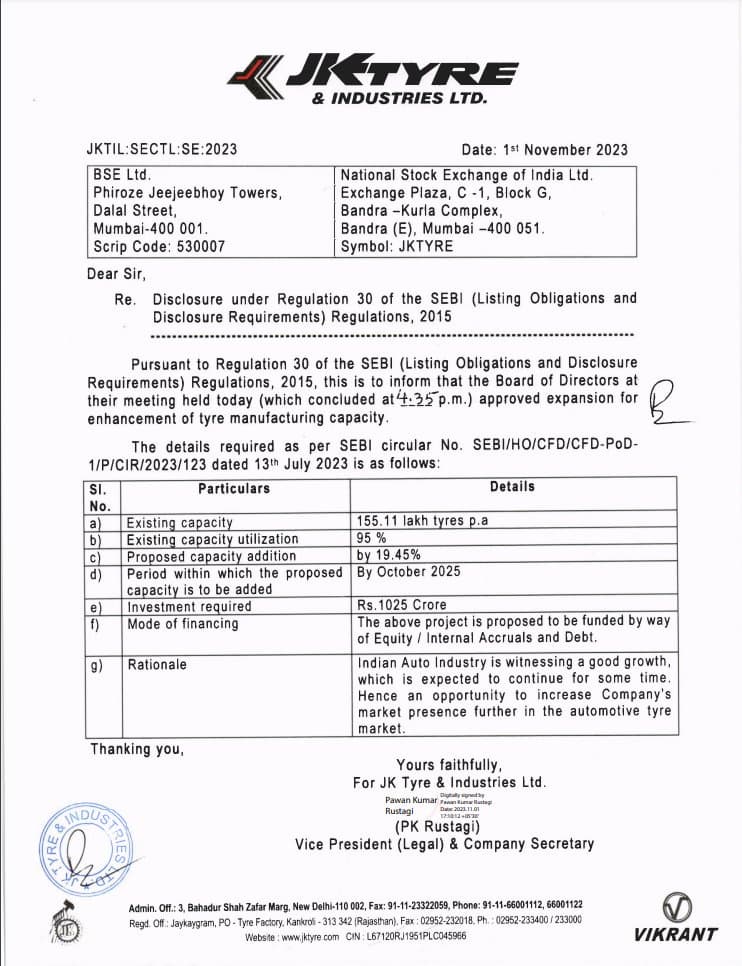

JK tyres – Catching the speed (01-11-2023)

The board has approved a plan for expanding their tyre manufacturing capacity.

These details include:

a) The company’s existing tire manufacturing capacity is 155.11 lakh tyres per year.

b) They are currently utilizing 95% of their existing capacity.

c) They plan to add 19.45% more capacity.

d) They aim to complete this capacity expansion by October 2025.

e) The investment required for this expansion is Rs. 1025 Crore f) They plan to finance this project through a combination of equity, internal accruals and debt.

g) The reason for this expansion is the growth in the Indian automotive industry, which presents an opportunity for the company to increase its market presence in the automotive tire market.

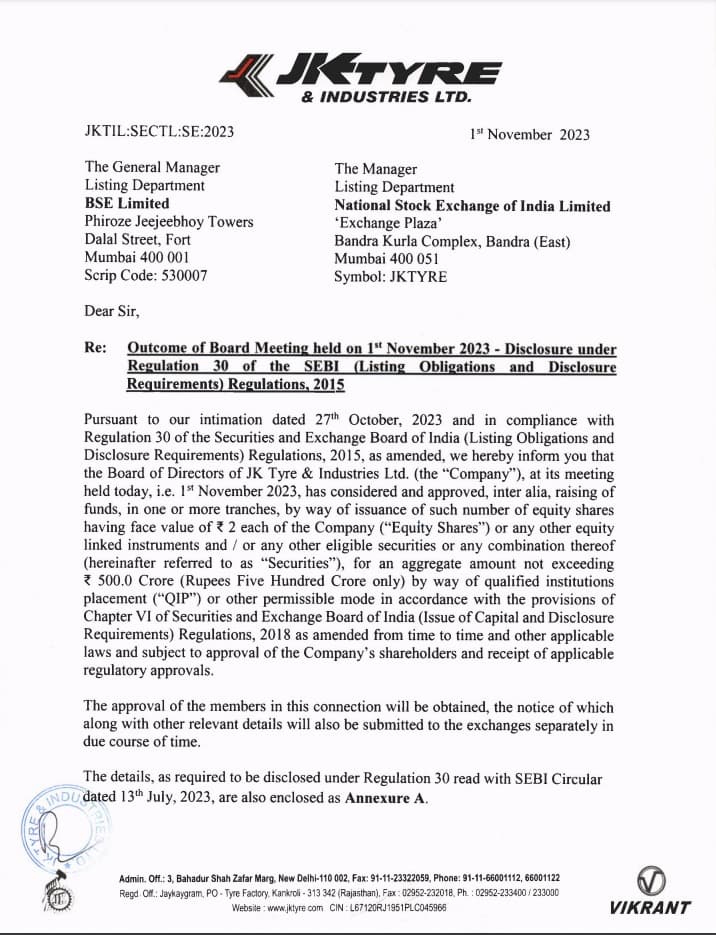

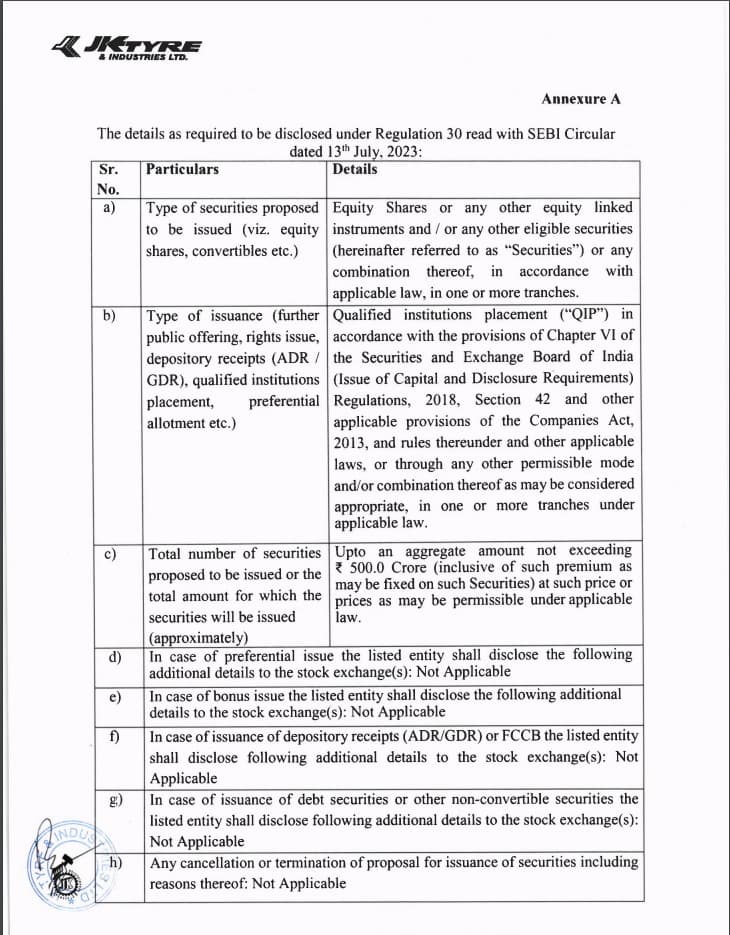

JK tyres – Catching the speed (01-11-2023)

JK Tyre and Industries – QIP

The board has decided to raise money by selling some of the company’s shares or other financial instruments. They want to raise up to Rs. 500 crore (Indian currency) through a process called “qualified institutions placement” (QIP) or other legal methods.

Sula vineyards – pioneers in indian wines (01-11-2023)

@Anubhav_Garg How does this reclassification happen? Why wasn’t it an FII from the start?