The Company has launched 2 (Two) new stores (i.e., Varamahalakshmi Silks format) at Coimbatore, Tamilnadu on 15th October 2023 & 16th October 2023.

Now Total Stores count 56.

Posts in category Value Pickr

Sai Silks (Kalamandir) – only listed player in the organized saree market (29-10-2023)

Piramal Pharma Limited (29-10-2023)

Good Result

Q2 FY2024.pdf (1.5 MB)

IDFC First Bank Limited (29-10-2023)

ROE of IDFC F Bank increase has no link with IDFC Ltd’s merger. Since IDFC’s entity shall get extinguished, it’s ROE angle doesn’t impact that of bank.

My hypothesis is : ROE of the bank shall improve going forward basis the following:

- Operational leverage kicking (26% of branches opened in last 18 months)

- Focus on Guidance of FY’25’s Cost to Income ratio target

- Run down on high cost long term borrowing

- Growing Credit Card & Wealth Management business.

Transformers has a next big transformation- Big Opportunity (29-10-2023)

Hi ValuePickr Family, My Name is Chanti Malla and working as Small techie. interested in equity research. I am a beginner and writing 1st topic in ValuePickr. Hope you will like my work.

Disclaimer : Not a SEBI register and Views are my personal. Don’t take Buy or Sell Calls on below Info and Sharing only for education or information purpose.

How Opportunity Created?

- Increasing Power demand.

- Central Government introduced Revamped Distribution Sector Scheme (RDSS)-3L+Crs for 2021 to 2026

- States upgrading Power Infra(State Discoms).

- China reduced Transformers Production.

- Not only India other countries also investing in power infra(Export Opportunity-Net Zero Emission Agreement)

List of companies are in this sector : (Source : MoneyPurse YTC Sector Video)

- Siemens

- A B B

- CG Power & Indu.

- BHEL

- Apar Inds

- Hitachi Energy

- GE T&D India

- Schneider Elect

- Volt amp Transform

- TRIL

- Bharat Bijlee

- Shilchar Tech

- Kirloskar Electric

- Indo Tech Transformers

- RTS Power Corp

- Amba Enterprise

- Star Delta Transformers

- Salzer Electronics Ltd

1st 14 Companies knows everybody and explained in different areas(YT, Forums etc)

But last 4 companies are non companies which are less then 200crs M.Cap except Salzer are came to my Rader. Seems to be long so will provide my thesis regarding these 4 companies on next my topic. Stay tune. Thank you ![]()

Jupiter Wagons Ltd (previously CEBBCO) (29-10-2023)

Q2 FY24 results Key development.

1.The capacity of existing foundry at Kolkata Unit will be increased from 2,500 metric tonnes at present to 3,000metric tonnes by the conclusion of this fiscal year. The wagon manufacturing capacity has been increased to ~700 wagons per month at present. Once the expanded capacity of foundry is made available, it is expected that production capacity will increase to 800 wagons per month.

2.A new foundry is scheduled to be established in Jabalpur over the course of next 18 months with a capacity of 2,000 tonnes, catering to both captive use and exports. This initiative is expected to yield cost savings in freight expenses.

3.Indian Railway tender for 20,000 wagons has been issued and the timeline for submission is mid of Nov,23.

4.With handover and integration activities nearing completion, it is anticipated that Stone India will initiate its operational activities in Q4FY24.

5. Electric Mobility: the vehicle is scheduled for testing in November, and we are progressing as planned for its commercial launch in the fourth quarter of this fiscal year.

PayTM (One 97 Communications Ltd) (29-10-2023)

A few notable points from the PayTM Q2 FY24 concall (E & O.E.):

-

Personal Loans: This quarter is the lowest growth Q-o-Q both in value as well as volume perspective. A couple of quarters back, we saw some early signs of stress in the PL portfolio, so we decided to go slow on it. Here, we have more than Rs 300 – 400 crores of portfolio which gets matured every month which is available for further upsell through our partners. So that is one bucket which is growing Quarter-on-Quarter and in the next two quarters we will see the renewal opportunity available to fully matured loans will be much higher than what we have seen in the last two quarters. So here you will see growth in early double digits but not like what it was in the past. (Elsewhere, he mentions 30 to 40 % is what we can expect). Ticket sizes will be a bigger contributor to growth than volume.

-

Post Paid and Merchant Loans: Continue to see healthy growth. Merchant Loans will grow 50 to 60 %. Out of the 41 million merchants that we carry online and offline, more than 20 million merchants have signed up to accept postpaid. Not all of them obviously pay MDR. The number of merchants who are paying MDR is less than about a million.

-

Lending Partners: Added Tata Capital as another lending partner taking overall partners to 9. Shriram Finance will go live in early November. In the next two quarters, we will add another three partners, of which one or two would be banks. Jio is not a threat. We are a large platform who can originate good quality credit for more and more partners. We see any new player coming in as a collaborator rather than a competitor.

-

Overall, for Lending business: For our credit business to grow, we do not need incremental consumers on our platforms. It is better for us to penetrate the existing customer base instead of acquiring new consumers. Overall, anything between 40-50% on a blended basis over the next 2-3 years should be the growth that we should start seeing from hereon. We believe that a stable case financial services take rate is in the vicinity of 3.5% to 3.65%. We continue to add about 400,000 to 500,000 new customers who are taking credit of any kind through the Paytm platform with different partners of ours every month. We are very conservative and strict as to which kind of users or merchants get access to credit. That filter remains common irrespective of new partner or old partner and once the merchant or user passes that filter then the filter of the lender comes into play where they are looking at underwriting. We currently service more than 250 towns for personal loans and merchant credit and more than that for Paytm postpaid. This year we would be adding another 50 to 60 towns.

-

Cloud Business: This is mainly co-branded credit cards and advertising. On e-commerce side, our GMV is now Rs.2900 crores roughly which is up 39% Year-on-Year and take rates have been in the range of 5% to 6%.

-

Payments: We are serving 500 locations for Payments business and will be adding 50 to 100 towns this year. Net payment margin will remain range bound between 7 to 9 basis points. Cross-border UPI will take some more time to scale up.

-

On devices and Soundbox: Capex is majorly for devices. We have innovated on sound, cards, QR etc. and have furthermore plans and roadmap ahead. Realisation on devices is around Rs.100 on a blended basis though some high-end soundboxes may cost upto Rs.1200 per piece and card machines cost about Rs.5,000 to Rs.7,000. We will continue to increase manpower on distribution as we want to dominate the acquiring side of the business. We aspire for around 1.5 million a quarter kind of deployment rate over the next 12 to 18 months for soundbox and card machines. There is a sales force of around 35,000. We do not see this plateauing for the next 3 years. Close to about 15 to 20% of that is involved in servicing but servicing is not just going and servicing the device. It is also to do with merchandising, branding, managing what is called ‘on the shop queries’ and then obviously managing device servicing etc.

-

Operations: When somebody takes a loan on the Paytm app, our lending partner does the KYC for the customer.

-

Employee costs: For the year, ESOP costs will be similar to last year. On the sales side, employee costs will continue to grow rapidly while on the non-sales side, growth will be more muted.

-

Miscellaneous: Wealth business (e.g., broking, ETF etc) has a huge opportunity and is one of our future long-term bets. PayTM Money is a fantastic business, very high margin and if you can run it at a very low cost of customer acquisition then it is a very good business. We see a huge opportunity in Paytm Money to continue to grow trading and investing in the country and it is financially becoming much sounder than it was 2 or 3 years ago. Paytm Payment Bank had good profitability last quarter and our Gaming JV which is first games which we own 55% of that also had improved profitability last quarter. On ONDC, currently there is an invitation kind of pricing. In the long run, we would prefer a subscription-based pricing model rather than MDR model. Cash in hand is Rs.8,750 crores.

(Disc.: Invested)

PayTM (One 97 Communications Ltd) (29-10-2023)

A few notable points from the PayTM Q2 FY24 concall (E & O.E.):

-

Personal Loans: This quarter is the lowest growth Q-o-Q both in value as well as volume perspective. A couple of quarters back, we saw some early signs of stress in the PL portfolio, so we decided to go slow on it. Here, we have more than Rs 300 – 400 crores of portfolio which gets matured every month which is available for further upsell through our partners. So that is one bucket which is growing Quarter-on-Quarter and in the next two quarters we will see the renewal opportunity available to fully matured loans will be much higher than what we have seen in the last two quarters. So here you will see growth in early double digits but not like what it was in the past. (Elsewhere, he mentions 30 to 40 % is what we can expect). Ticket sizes will be a bigger contributor to growth than volume.

-

Post Paid and Merchant Loans: Continue to see healthy growth. Merchant Loans will grow 50 to 60 %. Out of the 41 million merchants that we carry online and offline, more than 20 million merchants have signed up to accept postpaid. Not all of them obviously pay MDR. The number of merchants who are paying MDR is less than about a million.

-

Lending Partners: Added Tata Capital as another lending partner taking overall partners to 9. Shriram Finance will go live in early November. In the next two quarters, we will add another three partners, of which one or two would be banks. Jio is not a threat. We are a large platform who can originate good quality credit for more and more partners. We see any new player coming in as a collaborator rather than a competitor.

-

Overall, for Lending business: For our credit business to grow, we do not need incremental consumers on our platforms. It is better for us to penetrate the existing customer base instead of acquiring new consumers. Overall, anything between 40-50% on a blended basis over the next 2-3 years should be the growth that we should start seeing from hereon. We believe that a stable case financial services take rate is in the vicinity of 3.5% to 3.65%. We continue to add about 400,000 to 500,000 new customers who are taking credit of any kind through the Paytm platform with different partners of ours every month. We are very conservative and strict as to which kind of users or merchants get access to credit. That filter remains common irrespective of new partner or old partner and once the merchant or user passes that filter then the filter of the lender comes into play where they are looking at underwriting. We currently service more than 250 towns for personal loans and merchant credit and more than that for Paytm postpaid. This year we would be adding another 50 to 60 towns.

-

Cloud Business: This is mainly co-branded credit cards and advertising. On e-commerce side, our GMV is now Rs.2900 crores roughly which is up 39% Year-on-Year and take rates have been in the range of 5% to 6%.

-

Payments: We are serving 500 locations for Payments business and will be adding 50 to 100 towns this year. Net payment margin will remain range bound between 7 to 9 basis points. Cross-border UPI will take some more time to scale up.

-

On devices and Soundbox: Capex is majorly for devices. We have innovated on sound, cards, QR etc. and have furthermore plans and roadmap ahead. Realisation on devices is around Rs.100 on a blended basis though some high-end soundboxes may cost upto Rs.1200 per piece and card machines cost about Rs.5,000 to Rs.7,000. We will continue to increase manpower on distribution as we want to dominate the acquiring side of the business. We aspire for around 1.5 million a quarter kind of deployment rate over the next 12 to 18 months for soundbox and card machines. There is a sales force of around 35,000. We do not see this plateauing for the next 3 years. Close to about 15 to 20% of that is involved in servicing but servicing is not just going and servicing the device. It is also to do with merchandising, branding, managing what is called ‘on the shop queries’ and then obviously managing device servicing etc.

-

Operations: When somebody takes a loan on the Paytm app, our lending partner does the KYC for the customer.

-

Employee costs: For the year, ESOP costs will be similar to last year. On the sales side, employee costs will continue to grow rapidly while on the non-sales side, growth will be more muted.

-

Miscellaneous: Wealth business (e.g., broking, ETF etc) has a huge opportunity and is one of our future long-term bets. PayTM Money is a fantastic business, very high margin and if you can run it at a very low cost of customer acquisition then it is a very good business. We see a huge opportunity in Paytm Money to continue to grow trading and investing in the country and it is financially becoming much sounder than it was 2 or 3 years ago. Paytm Payment Bank had good profitability last quarter and our Gaming JV which is first games which we own 55% of that also had improved profitability last quarter. On ONDC, currently there is an invitation kind of pricing. In the long run, we would prefer a subscription-based pricing model rather than MDR model. Cash in hand is Rs.8,750 crores.

(Disc.: Invested)

SmallCap Hunter : Trying to find the dark horses with triggers (29-10-2023)

Refex is not only in refrigerant filing 80% of its business comes from coal ash handling which is deep cyclical in nature every 2 or 4 month they receive order.

It will increase your Blood pressure only with LC.

Hope that helps

SmallCap Hunter : Trying to find the dark horses with triggers (29-10-2023)

Refex is not only in refrigerant filing 80% of its business comes from coal ash handling which is deep cyclical in nature every 2 or 4 month they receive order.

It will increase your Blood pressure only with LC.

Hope that helps

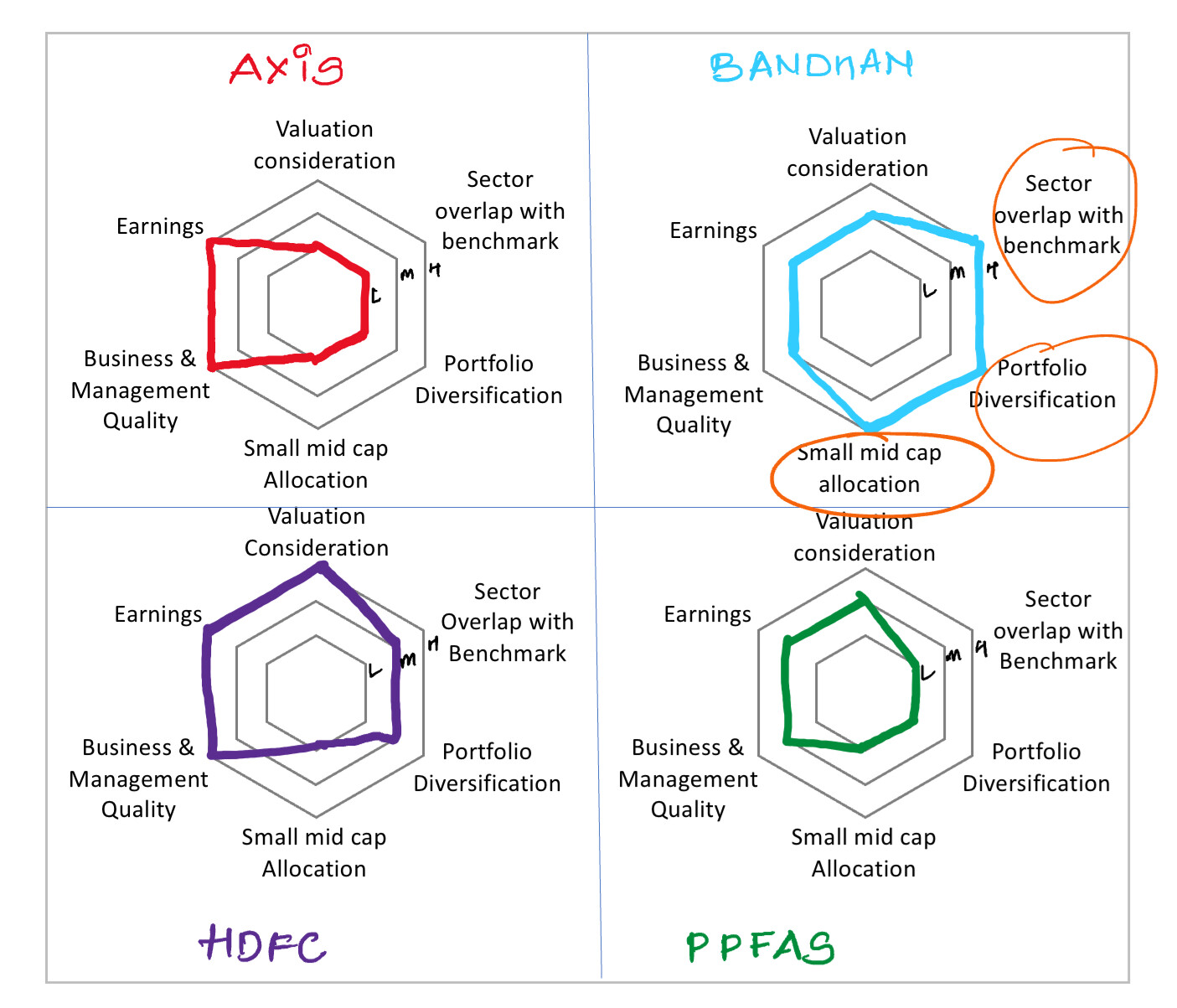

Omkar’s Portfolio Analysis and Discussion (29-10-2023)

Part 2 – What’s the best combination for the mutual fund portfolio – My take

**Part A : Why Bandhan MF is no brainer in my framework **

To keep it simple, I would like to construct a portfolio of funds which has a low beta component to provide stability during market drawdown and a high beta component to provide higher upside in a bull market. All the competition – Axis, ppfas and hdfc etc – is in the low beta part. For High beta there is no competition. As explained earlier in this thread very few fund managers cherish beta in the portfolio. A unique combination of high sector overlap with benchmark, large diversification and small mid cap heavy portfolio give High Beta characteristics to bandhan’s strategy

Part B – Which is a better low beta strategy – ppfas or Axis. To be continued…