Is anyone tracking Emerald Finance?

Posts in category Value Pickr

Sugar Cycles: 7-8 years of losses followed by 2-3 years of super gains! (29-10-2023)

Dhampur Bio – promoters have bought shares from open market at Rs. 160. Last Nov also they had bought shares from market.

Company has increased cane crushing capacity (by 30%). As per concall they expect to crush 8% more cane this year. Extra capacity of 20% will help them crush cane faster and hence increase recovery (cane crushed in April/ May has low recovery).

They had commissioned pharma grade sugar plant few quarters back.

Ethanol they have postponed as margins in sugar will be higher for next 2 years. No capex no interest burden but higher margins through existing sugar capacity.

DBOL will be best performing sugar company this year.

Sona Comstar BLW – Direct EV Play (29-10-2023)

I am an investor myself with an avid interest in the stock market. I too found that there was no tool that helps me filter stocks based on current happenings around the world. So, I started developing this myself. Currently, I am everything, developer, marketer, CEO …

I am looking for a few folks to join my team. I need React and Python aficionados. They can also learn AI from me. Inbox me if any of you are interested.

@The_Seeker I would love to hear about your ideas/suggestions and also help you understand the interface. I hope to write a tutorial and make some YouTube videos on how to use the application soon.

“Polyplex Corporation “ Are Good Days Ahead? (29-10-2023)

In May 2023, The Promoter Group Members agreed to sell approx 24.2778% of their stake to AGP Holdco Limited (Investor) and informed that they were in the course to obtain necessary regulatory approvals. AGP Group is Dubai based Group and have several businesses including Packaging.

The consideration has been revised downwards to Rs 1,188.9 crore, compared with Rs 1,379.47 crore announced in May.

The September Shareholding pattern publshed shows that the Promoters have pledged 100% so a vital question arises how will they sell 24.3% if they have pledged full100% ?

Discl: exited and hence not tracking closely

Glenmark Life Sciences (29-10-2023)

Some highlights from the Q2 FY24 concall:

-

CDMO business: Saw slower demand this quarter in one of the molecules. But there is a lot of traction from new customers and new projects. In a year’s time, another 2 – 3 projects will be added to the basket. We have supplied validation batches. Then there is an approval cycle etc. These have a total revenue potential of Rs.150 crore.

-

Milestones achieved: Added 3 new products to our pipeline, with one high-potent API and 2 complex APIs. Working capital remained stable during H1 FY24 at 170 days. Better to stock up on inventory than run out of it, external environment is still volatile.

-

Capex: Current year’s capex is Rs.200 crore. Expansion happening in All three – Dahej, Ankleshwar and Solapur. The engineering work has started for construction of phase 1 of 200 KL in Solapur. In Ankleshwar, out of 400 KL capacity, 192 KL was added in Q4 FY23. Another 208 KL will be completed in Q4 FY24 and will quickly be utilized. Most of the capacities are fungible across customers & businesses except for 1 where the capacity is dedicated capacity for a CDMO customer.

-

Higher Employee Costs: Driven by regular increment cycles and certain talent management cost which will continue at similar levels in FY24.

-

Agreement with Glenmark: Current business will continue for a period of 5 years. We supply more than 65 APIs to Glenmark Pharma. Over 95% of it is a regulated market business. With the number of approvals that we have over multiple markets, this is a sticky business. There is non-compete with both Glenmark as well as Nirma. Pharma will have to restrict from doing the APIs that Glenmark Life Sciences is doing. And so will Nirma have to avoid doing any formulations that Glenmark Pharma is doing using Glenmark Life Sciences APIs. Glenmark Pharma has already qualified quite a few GLS APIs. That will come under the agreement, but anything new that they want to develop, that they can go ahead and develop.

-

PLI benefit: Will go away after the change in ownership. It will have 100 to 150 bps impact, which we will cover up elsewhere.

-

Going ahead: Demand will pick up in H2 of the year, have good visibility on both generic API and CDMO. Current year’s guidance – 28 to 29 % EBIDTA margin. But thereafter, it will stay at 30 %. Long term revenue growth will be in mid-teens. Making new business forays into oncology and iron complex. In Oncology, we have 9 molecules in the pipeline. Three have been validated already.

(Disc: Have initiated a position last week)

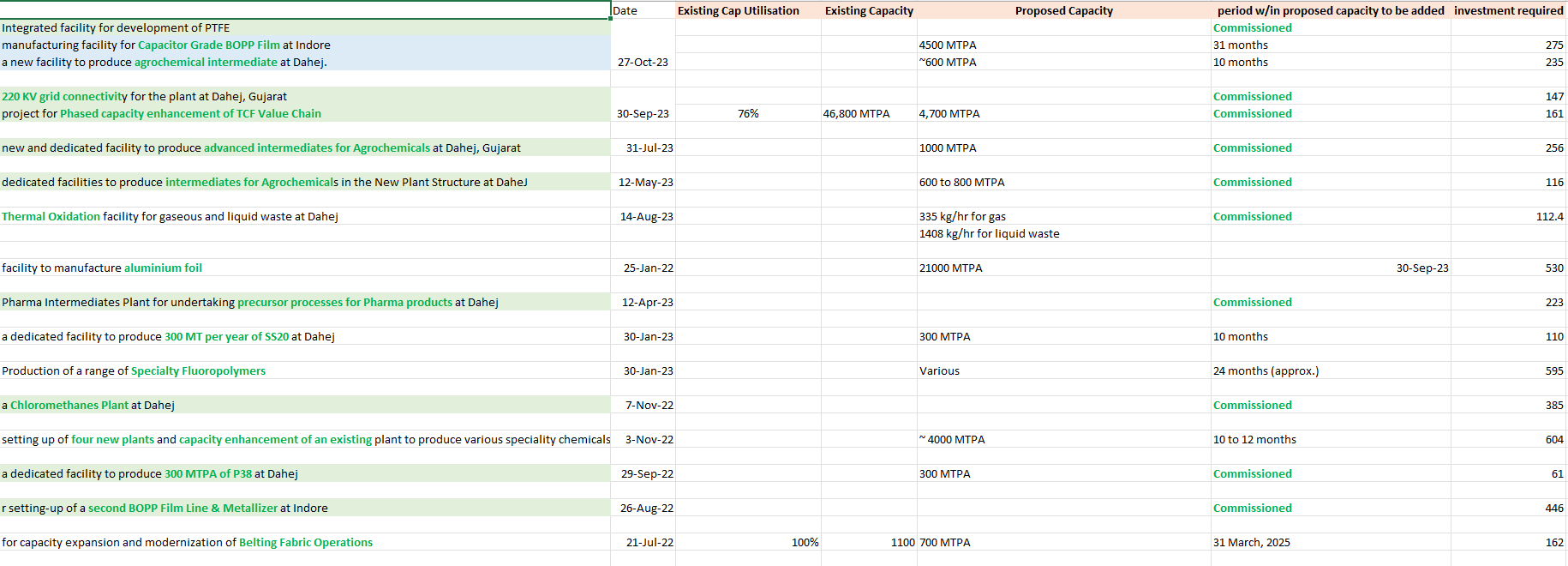

SRF Limited (29-10-2023)

Capex done from Jul 2021 till now – almost 5556 crore

most of them already commissioned or to be commissioned this year.

Price in range from Jul 2021-

Disclaimer – Invested and biased. Buying in SIP mode.

Dreamfolks services limited( DFS) (29-10-2023)

They are trying to forge a consumer behavior, so that even when rewards are minimized or withdrawn consumer habits continue.

Dreamfolks services limited( DFS) (29-10-2023)

They are trying to forge a consumer behavior, so that even when rewards are minimized or withdrawn consumer habits continue.

The harsh portfolio! (29-10-2023)

In Maiden Forgings call, however Geekay management declined it at their AGM.