People who have invested into this stock, what is your take after yesterday’s result?

Posts in category Value Pickr

Dreamfolks services limited( DFS) (26-10-2023)

Just listened to the concall – pretty much aligns with my perspective.

A back of the hand calculation for an investment horizon of 3 years is as under.

Figures as per screener:-

Sales growth h1 fy24 = 65.56% (much less than the previous years)

PAT margin for this qtr = 6.38% (don’t think margin can go below this)

Estimated sales for fy26 = 3507.82

Estimated PAT for fy26 = 223.8

Estimated PAT CAGR = 44.73%

No major equity dilution expected.

Ttm PE at CMP = 34.64 => PEG of less than 1 which shows it is undervalued.

P.S. This is not to be construed as a buy/sell recommendation but a perspective on the valuation.

Embassy REIT: Is this “Blackstone” promoted REIT is real diamond? (26-10-2023)

@Amit2saxena @mahesh_s

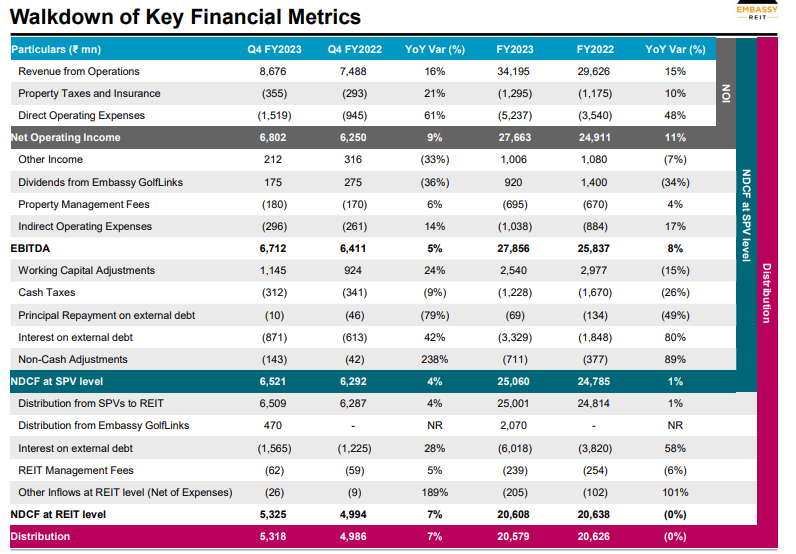

Thanks for seeking my view, although not sure how much it would be useful. I have gone through your postes and the past release of Embassy REIT for Q4FY2023. They have provided detail calculation including most of heads to derive at NCDF for Q4FY203 and FY2023.

I am enclosing same for everyone reference. I find this relatively simple to understand rather than working on my own from financial given my limited understanding. One can easily get understanding of what contribute positively and negatively in NCDFC from P&L and Cashflow .

While it may oversimply, I can not understand complex things and try to keep my life simple.

Total EBITA in P&L for FY23 is Rs 26,884.99 mn as displayed in message 259 as against Rs 27,856 Mn as shown in enclosed table. The difference is around Rs 971.44 mn can be attributed to Dividend income from Golflink being Rs 920 mn. So unexplained difference of Rs 51 mn, which is not very large given the operating matrix in my view.

Embassy REIT FY23 Reconciliation of NCDF with P&L.xlsx (9.6 KB)

Disclosure: Embassy REIT is my third largest holding in Debt portfolio and hence my view may be positively baised. I may change my allocation (increase/decrease/exit) from Embassy REIT wihtout informing forum. I am not SEBI registered investment advisor. I am not recommending any investment action. I am not CA and hence my understanding about accounting may not be correct.

Manappuram Finance (26-10-2023)

(post deleted by author)

Kotak Mahindra Bank – Low Cost Liability Banking Franchise (26-10-2023)

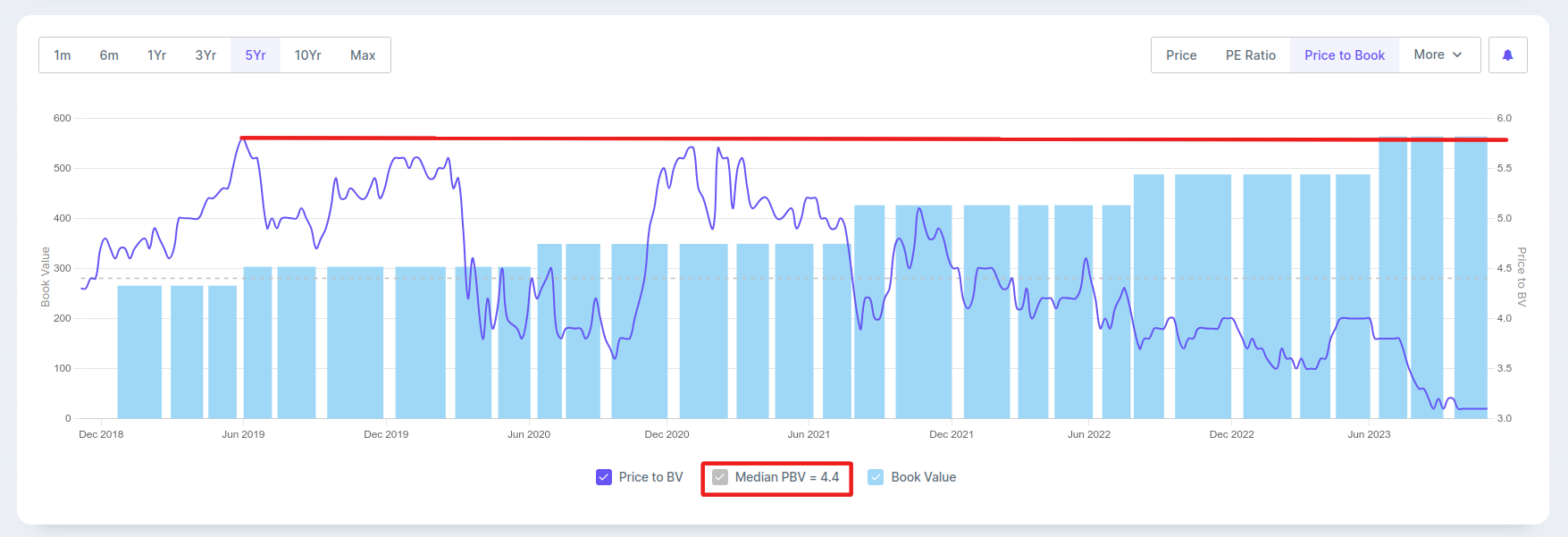

A very pertinent question is how does one assign a multiple to bank like Kotak? The bank is growing it’s book value per share at the rate of 15% yoy every quarter without fail. Also, the bank has been able to keep NNPA close to zero with advances growing at 15-20% yoy every quarter.

With Indian economy projected to grow at 6% for next decade this bank is well poised for a healthy long-term growth.

If history is any judge here are the historical multiples for the bank

Price/Book

21/oct/23 = 1769/605 = 2.9x

22/jul/23 = 1971/584 = 3.4x

21/jan/23 = 1760/540 = 3.25x

22/oct/22 = (1800/519) = 3.5x

27/apr/17 = 4.3x (900/209)

30/apr/18 = 4.5x (1222/264)

19/jul/18 = 5.1x (1400/272)

01/may/19 = 4.3x (1300/305)

22/jul/19 = 4.6x (1450/313)

Also look at the historical price to book value from the screener, median price to book is 4.4. So again the same question what price to book multiple will you assign to Kotak bank??

I think sometimes Mr. Market gives us Gold at the price of Copper and this is one of the case. Of course no one can time the market so we don’t know how long we have to hold to get some returns.

The only unsolved question from my end is, has the price to book value growth of Kotak bank slowed down, was it growing at 20% on an average between 2010 and 2020? I don’t have data for this.

Disclosure – Invested and biased.

Hitesh portfolio (26-10-2023)

We have had a brutal correction in overall markets since past few days. By now it’s become all too familiar. Whenever these corrections come about, the kind of downward force that is there takes most market participants by surprise. This has happened in the past also and is the case in most corrections.

When these corrections come about is anybody’s guess, and personally I have found them difficult to predict on a consistent basis.

How to negotiate them is often the big question. What I usually do is evaluate my portfolio stocks, and try to weed out the least conviction stocks, both in terms of fundamentals and technicals and try to get into new better options, or increase allocations to existing high conviction bets.

If we take a broader view on overall markets, 18880-18890 was a major top previously. In this correction we have reached those very levels. So logically based on change of polarity principles, we could get support at those levels. Nifty is close to 200 dema at around 18840. So current levels need to be watched for arrest of fall in Nifty and a possible tradeable bounce. Otherwise things can get ugly.

HBL is also in a corrective mode, and has corrected to levels of around 260 from highs of 310. This seems in line with the market correction.

@rmjp Logarithmic scale is used on very long term chart of months and years. For short to medium term, its better to go for normal price charts. While reading William O Neil’s book, (or any other book for that matter) try to focus on the overall learnings rather than getting stuck with a single point. We have to remember that this book was written decades ago, so some things may not apply to today’s markets. But if we get the overall concept described in the book, which is that of getting into stocks with both earnings and price momentum, it should serve us well.

KMC Speciality hospital (26-10-2023)

Please refer to the details of KMC capex on the recent Rating Update Pdf.

-Atmiya

PPFAS Financial Opportunities Forum (26-10-2023)

PPFAS’s view on small caps and small cap funds seems to be playing out almost flawlessly.

FYI, today is the next edition of the FOF. Focus area?

Artificial Intelligence.

Looking forward to it. If you are attending too, it will be great to catch up!

Indiabulls Housing – A compounder from here? (26-10-2023)

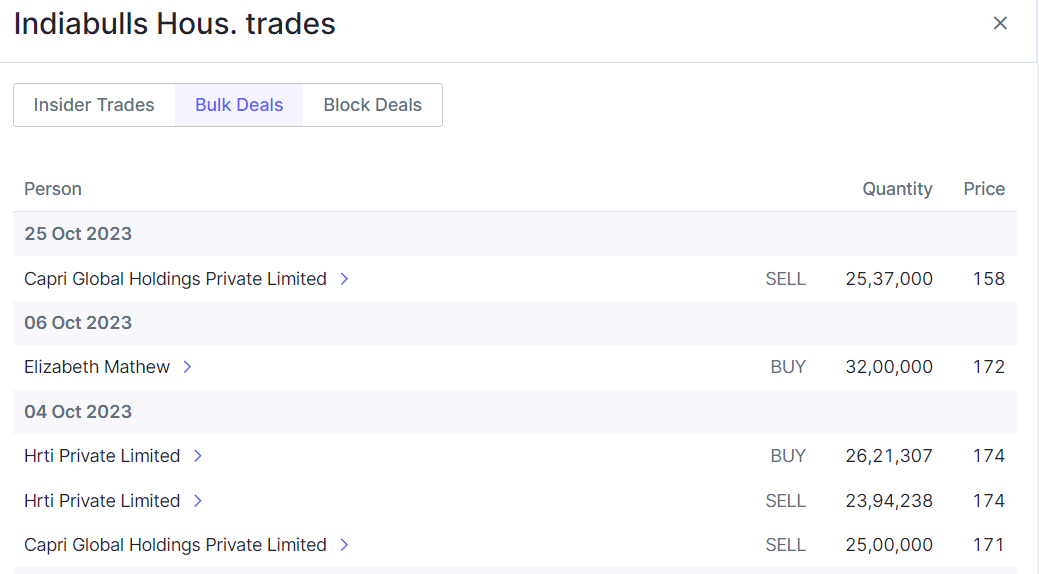

Is it possible that Capri would have shorted Indiabulls in F&O and selling in cash to create pressure?

Indostar Capital Finance Limited (26-10-2023)

Indostar sold their loans for 790 crore, which is an 86% recovery on the total loan outstanding of ₹915 crore as per the below article. Honestly I don’t know how it will be treated on the P&L statement and what impact it will have, we will get to know tomorrow.