So many holes in Cashflow statement for the past 2 years, are they cooking the financials?

So many holes in Cashflow statement for the past 2 years, are they cooking the financials?

So many holes in Cashflow statement for the past 2 years, are they cooking the financials?

Fundamental Valuation for HMVL makes little sense, as it belongs to a dying industry. HMVL, with its flagship Hindi newspaper is still better placed than the English dailies, but the performance has been on the way down pre-covid and has got further exacerbated during and post-Covid. The main revenue earner for the newspapers is the Ad Rev, and this is moving away to digital space. Circulation is static and they have little to no pricing power.

There are a few positives that might play out in FY24 for HMVL; 1) Reduction in newsprint prices may reduce the cash burn (losses), 2) Improved ad spends by corporates in some sectors that target the rural landscape, 3) Uptick in GoI and State Govt. ad spends in view of the upcoming general and state elections, 4) Improvement in their new digital venture subscriptions, OTT Play.

However, HMVL is still an asset play with a large cache of Investments and Cash in its pockets; against a Market Cap of ~550 cr, HMVL’s Investments, Cash and Cash Eq. are worth 1400 cr as per AR FY23.

What is missing is the catalyst to spark market participant’s interest and unfortunately the sub-par transparency and communication skills of the management doesn’t help either. If and when it plays out, it might see some upward movement towards its Intrinsic Value. Note that the stock price has increased by 42% in the last year, but this could just be the result of the general exuberance in small and micro cap stocks in the market.

Fundamental Valuation for HMVL makes little sense, as it belongs to a dying industry. HMVL, with its flagship Hindi newspaper is still better placed than the English dailies, but the performance has been on the way down pre-covid and has got further exacerbated during and post-Covid. The main revenue earner for the newspapers is the Ad Rev, and this is moving away to digital space. Circulation is static and they have little to no pricing power.

There are a few positives that might play out in FY24 for HMVL; 1) Reduction in newsprint prices may reduce the cash burn (losses), 2) Improved ad spends by corporates in some sectors that target the rural landscape, 3) Uptick in GoI and State Govt. ad spends in view of the upcoming general and state elections, 4) Improvement in their new digital venture subscriptions, OTT Play.

However, HMVL is still an asset play with a large cache of Investments and Cash in its pockets; against a Market Cap of ~550 cr, HMVL’s Investments, Cash and Cash Eq. are worth 1400 cr as per AR FY23.

What is missing is the catalyst to spark market participant’s interest and unfortunately the sub-par transparency and communication skills of the management doesn’t help either. If and when it plays out, it might see some upward movement towards its Intrinsic Value. Note that the stock price has increased by 42% in the last year, but this could just be the result of the general exuberance in small and micro cap stocks in the market.

Fundamental Valuation for HMVL makes little sense, as it belongs to a dying industry. HMVL, with its flagship Hindi newspaper is still better placed than the English dailies, but the performance has been on the way down pre-covid and has got further exacerbated during and post-Covid. The main revenue earner for the newspapers is the Ad Rev, and this is moving away to digital space. Circulation is static and they have little to no pricing power.

There are a few positives that might play out in FY24 for HMVL; 1) Reduction in newsprint prices may reduce the cash burn (losses), 2) Improved ad spends by corporates in some sectors that target the rural landscape, 3) Uptick in GoI and State Govt. ad spends in view of the upcoming general and state elections, 4) Improvement in their new digital venture subscriptions, OTT Play.

However, HMVL is still an asset play with a large cache of Investments and Cash in its pockets; against a Market Cap of ~550 cr, HMVL’s Investments, Cash and Cash Eq. are worth 1400 cr as per AR FY23.

What is missing is the catalyst to spark market participant’s interest and unfortunately the sub-par transparency and communication skills of the management doesn’t help either. If and when it plays out, it might see some upward movement towards its Intrinsic Value. Note that the stock price has increased by 42% in the last year, but this could just be the result of the general exuberance in small and micro cap stocks in the market.

Sharing notes from Q2FY24 concall of Dreamfolks:

Numbers:

Existing business updates:

Management comments about what exactly is the proprietary technology:

DFS’s platform gives the card providers (banks) the ability to manage card programs. Card providers also drive consumer analytics using this platform. DFS has invested around 5.5 crores over last 4 to 5 years to develop the technology. I still find it hard to comprehend.

New lounges or larger existing lounges (after transformation) are coming up at Hyderabad, Delhi

Railway business has been growing fast but the base is quite low to be called out separately

When asked if card providers can decide to reduce DFS’s margin, the management said they do not think card providers can/will do that. Won’t share details about card providers’ budget to offer lounge services to its customers.

Non-lounge services like “meet and greet” have higher gross margins. Management noted that the segment is small. Once it grows to provide a 20% contribution to revenue, overall gross margins will improve. It will take another 3 to 4 years.

Newer business updates:

Risks:

Thermal insulation rubber foam

Nitrogen gas

Fire cylinder and its gas

Sandwitch panel for thermal roofing

Tyres for fork lift,spider lift,boom lift

Monorail system

Conveyor belt system

Aviation services and equipment

Reefer for cold transpiration

Give me the details with manufacturer competitive advantage and cash generating company

Q2FY24 Results: Company reported its highest-ever revenue, EBITDA, and net profit,

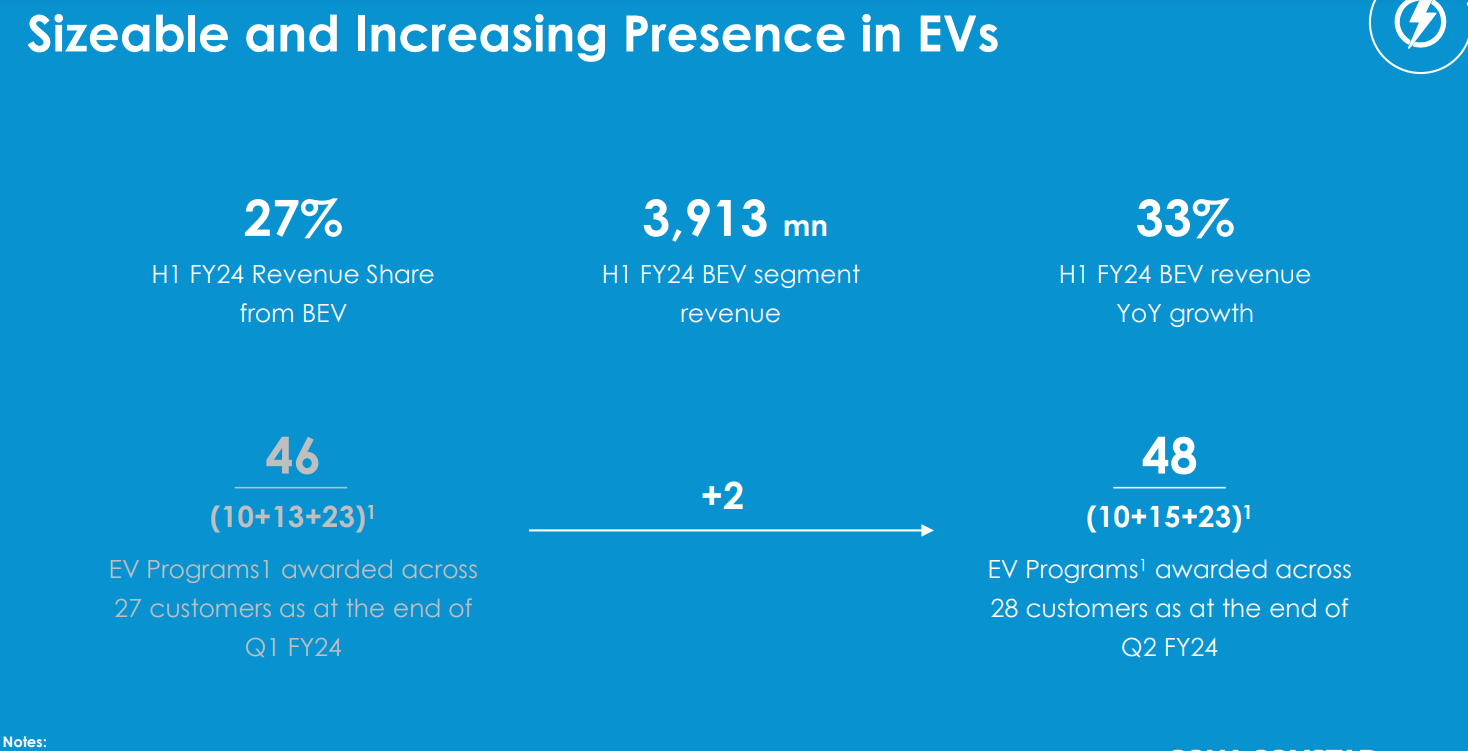

EV Business Highlights:

Concall link:

Sona BLW Precision Forgings Limited Q2 FY24 Earnings Concall

I haven’t read the article (not a subscriber). Would be grateful if someone can share a summary, especially any insights outside of the recently published Nuvama report.

@LarryWink As per your observation of historical trends by Howard Marks, smallcaps have had 2years of downtrend, but where is the rally?

I am expecting atleast a year of rally starting this year or next. Or maybe we are in the midst of a longer term rally