Absolutely right choice for long term

Posts in category Value Pickr

Best Agrolife – Think Big, Think Best! (23-10-2023)

Q2 result is expected to be a Super Duper for the company.

The Stock should bounce back after Q2.

Yash Pakka – (Previously Yash Paper) – Rising from ash (23-10-2023)

When is the concall??

Mahindra Logistics (23-10-2023)

Hi,

Another bad set of results at the consolidation level. Seems like situation is getting worse instead of improving.

Q2 FY24 MLL Standalone compared with Q2 FY23

• Revenue Rs. 1,136 crores as compared to Rs. 1,195 crores

• EBITDA Rs. 74 crores as compared to Rs. 64 crores

• PBT Rs. 26 crores as compared to Rs. 15 crores

• PAT Rs. 19 crores as compared to Rs 11 crores.

• EPS (Diluted) Rs.2.59 as compared to Rs 1.5

Q2 FY24 (consolidated) performance compared with Q2FY23

• Revenue Rs. 1,365 crores as compared to Rs. 1,326 crores

• EBITDA Rs. 54 crores as compared to Rs. 68 crores

• PBT Rs. (8 crores) as compared to Rs. 17 crores

• PAT loss Rs 16 crores compared to profit of Rs. 11 crores

• EPS (Diluted) Rs. (2.21) as compared to Rs. 1.69

It is quite evident that the acquisitions made by the management is backfiring. They have not been able to streamline the processes yet. EBIDTA margins have deteriorated significantly due to higher operating expenses.

If we see standalone results it is improving, and they could have been better off instead of acquiring these loss-making cheap businesses. Even there is no revenue growth also.

Senior border please suggest your views!

Disclaimer: Invested, no buy/Sell recommendation.

Thanks,

Deb

SmallCap Hunter : Trying to find the dark horses with triggers (23-10-2023)

It is said that, when valuations go into froth zone, markets/stocks look for a reason to fall, any reason, and the reasons while valid, the reactions need not be logical every time.

Broadly speaking w.r.t the markets, one can think of going along with the market, act in accordance with the market, and w.r.t specific stocks, there could be a few different scenarios, one could start taking a position, and see what happens, because the price after a fall in some stocks may very well be a good support, so there may not be more fall, not that prices will not fall more, even the bluest of the blue fall, but this is another scenario. Consolidation is another scenario. One could look at the % of falls in the specific indices, or the stocks in the watch list, for some visibility.

I think, it is hard to follow the price of a small cap, compared to a large cap, so one has to be more careful.

So, depending upon the understanding of the business, and price levels, one can come up with different scenarios and the likelihood of them happening, and take decisions.

I have positions in mid and small caps, but these are only for shorter term, so on days like today, SLs come flying, I cannot stop them, so take my views with a good amount of salt.

Kothari Petrochem Ltd~ A hidden moated small-cap company? (23-10-2023)

thanks a lot. Absolutely agree… will track this company closely!

Kothari Petrochem Ltd~ A hidden moated small-cap company? (23-10-2023)

Hey harsh, although its difficult to predict the trend of quarterly results especially for chemical companies due to uncertainty about their inventory position & pricing of raw materials (in this case base oil) & End product (i.e. PIB~ HS Code 390220). However the prices of PIB have definitely moderated in the past 3 months which might lead to an okayish quarter.

In terms of PE I completely agree with you that markets dont give good multiples to petrochemical cos, however, if you will look at its past valuation multiples it has generally traded at around 12 times ( which is the rate at which i took my position).

Now, I believe that given increase in diversification of end user base, nicheness in product with high market share thanks to the scarcity of raw materials (which it sources from Reliance & CPCB) & renewed aggression by the young promoter wherein they are developing new products & doing rapid expansions(surprisingly recording very high utilisation rates), I am fairly confident that the coming years will be much better in terms of the quality of the business as well as growth prospects & thats why it deserves a better multiple.

So to conclude, as long as business trajectory will be upwards ( unlike other petrochem cos who recorded poor results in Q1 & are actually seeing increased capacity across the industry), I believe multiples for this business might be higher in future.

It is important to note that its scale is much smaller than other petrochem players & thats why we need to see how scalable this business is… However so far, it looks decent.

E2E Networks Ltd – Listed small Cloud computing player (23-10-2023)

I think we can simplify the business model into three categories.

A . Compute resource [ CPU, Memory, Storage] provision over the cloud has lot of competition, however many MNC like HP, HPE, Dell will eventually join the game so, I would say this is a low margin proposition.

B. Compute resource, backup and services related to IP address, domain address registration etc can be a package to customer, this is an interesting space to be in because switching cost is higher if they have customers. But we don’t have data on number of such customers.

C. GPU as a Service.

This space is a very niche area and requires a lot of computing resources, having one GPU per server is of less use so, companies buy a ton of GPUs so, that customer queries get answered very quickly. E.g. Computers use GPU to simulate Weather patterns, Predict the failure of the supply chain based on orders, anomaly detection in turbines, DNA analysis, Pharma etc

So, there are two variables in the GPU equation, Training an AI model using large Data set and building an output from the model, aka Inference which is intelligent enough to predict or do the required goal in the shortest time.

With more data, the training of AI model will be good but it requires lot of trail and error as AI world is very specific to the use case. There is no standard way of doing things in AI world because data is unique.

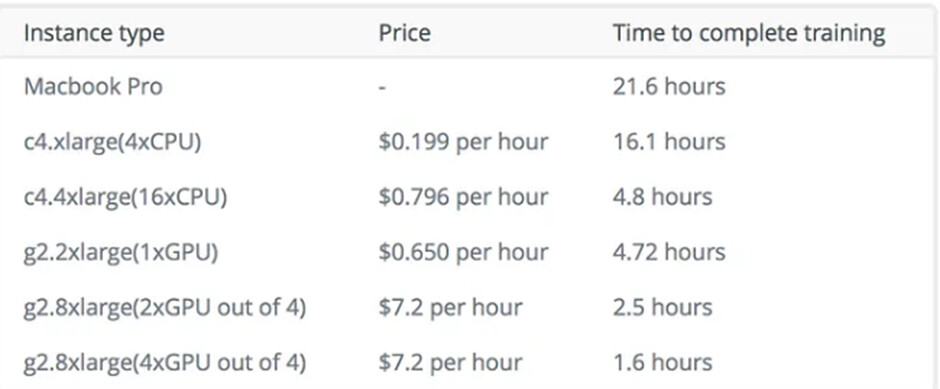

The below graph from link shows how much GPU is required for training. Now if we map it to the e2e client, what can a customer do with 1 GPU and a small machine? That too all the machines run with virtual CPU/KVM.

What can the customer achieve then?

- They can do a prototype of an AI/ML model and train the model with a limited amount of clean data.

- They can measure the model outcome but for better inference lot of data and bandwidth is required.

So, Once we have data on the below points, we can understand the exact usage of the infrastructure and the possibilities of scaling this to new frontiers.

- Client Categorization

- GPU usage with respect to clients

- Number of customers onboarded

- Retention of customers on their platform.

- Number of customers using 1 GPU vs 4 or X GPU

KPI Green- Turning Sunshine Into Cashflows (23-10-2023)

Apart from the signs of corporate governance being loose, at business front, order book growth and execution has not been upto the mark.

Q4 23 and Q1 24 saw around 80MW quarterly runrate, however Q2 was tepid.

There was a tender win from gujarat state however it was in nature of bidding and margin need to be checked.

Another order being hyped is merely an MOU with a little known company.

Request boarders to share their opinion for the quality of order book and margin going forward.