Sure Here is the link: https://www.fpi.nsdl.co.in/web/Reports/Monthly.aspx

at the time of posting this comment, this website is unreachable (don’t know why)

but keep trying later

Sure Here is the link: https://www.fpi.nsdl.co.in/web/Reports/Monthly.aspx

at the time of posting this comment, this website is unreachable (don’t know why)

but keep trying later

Saakshi Meditech and Panels Ltd

Came across this SME Machine Tools company with Market cap of Rs. 469 Cr, CMP 266, P/E of 37.9 basis FY23 numbers.

Total number of shares 1.76 Cr with promoter holding 73.6%.

They got listed on 3rd Oct on NSE platform, 1200 lot size at Rs. 150/- (Issue prize of Rs. 97).

Company is in business of making medical device, Electrical Panel, Mechanical HLA assemblies, Wiring harness, catering to Industry like, Health Care, Renewable, Aviation, Locomotive, Compressor in its 9600 SqMtr Leased premises.

They don’t own any manufacturing facility.

Indian Machine tool industry is to grow at ~10% YoY as per iMARC report.

This company is growing at ~30% YoY Sales (122 Cr in FY23 Sales). The Net Profit margin is at 10% (PAT), EBITDA at ~16%.

Company growth projection is in line with its past performance of 30% YoY. No Capex is planned as present 3 facilities in Pune are running in 1 shift only (8hrs work) with 37 Engg. They can scale up for 3 shift operation if business comes.

Their 90% business is from top 5 clients of Short term fixed price and delivery period order based:

All values in Rs. Lakhs

The above data shows that they are mainly into contract manufacturing and a dependency on getting contracts on competitive bidding basis. This works for them as a major risk.

In X Ray segment they are into Assembly of the equipment they source the components, only outer units are made, USA, China, Germany. A risk they have.

The company is having long term association with its top 5 clientele and that is the advantage they enjoy in this segment.

The peer comparison companies have similar profit margin (PAT).

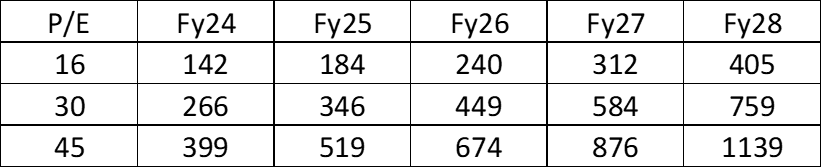

If they grow at 30% rev as projected and PAT at 10% like past performance the stock could do good for the investors. Being SME stock 6 monthly performance report is to be looked at.

Current MP Rs. 266 per share is already high and has accounted the growth of 30% for next 5 years at 16 P/E. Industry Avg PE is ~22* (Range 37 to 11).

Fwd P/E rerating can follow based on YoY performance and Expansion (Liner or Non Linear way)

Assuming 30% Sales growth and 10% PAT YoY

Disc: Not invested

(post deleted by author)

@basumallick I have done a basic forensic analysis but I have a doubt about one thing

Cumulative investments in Fixed assets from FY14 to FY23 is 1974 crores but the gross block difference from FY23 and FY13 is 1163 crores… Where is there a difference of 70% in both these amounts? Shouldn’t the difference be more or less equal to the amount spent on acquiring fixed assets?

Theme: Value Stocks:

Stock

Likhitha Infrastructure Ltd

Expleo Solutions Ltd

Greenpanel Industries Ltd

India Pesticides Ltd

Share India Securities Ltd

Sigma Solve Ltd

Theme: Value Stocks:

Stock

Likhitha Infrastructure Ltd

Expleo Solutions Ltd

Greenpanel Industries Ltd

India Pesticides Ltd

Share India Securities Ltd

Sigma Solve Ltd

Garware Hi-Tech Films Ltd (GHFL) has incurred a capex of Rs. 270 crore over the last two years. With the help of this capital

expenditure, GHFL was able to vertically integrate its business, strengthen its dealer network, launch its new product (PPF), and

increase the capacity of its current goods (SCF). Thus, ramping up of capacity provides the company with strong medium-term

growth visibility.

• GHFL has continuously increased the share of value-added products within its sales mix. Value-added products, which accounted for

48% of total sales in FY2017, increased to 80% in FY2023. This led to an improvement in its margin to 18.7% in FY2023 from 9% in

FY2017. As the company is planning to ramp up the capacity of value-added products and add new products, margins will continue

to improve going forward.

• The company has fully vertically integrated chips-to-film manufacturing facilities. These capacities are fungible and capable of

delivering customised products across a range of over 3,000 SKUs. Backward integration also helps the company’s R&D department,

as it leads to greater customization, faster time-to-market, and improved quality.

• Key risks: Sharp surge in oil price could impact margin/earnings. Sluggish demand in the automotive and real estate Industry

Garware Hi-Tech Films Ltd (GHFL) has incurred a capex of Rs. 270 crore over the last two years. With the help of this capital

expenditure, GHFL was able to vertically integrate its business, strengthen its dealer network, launch its new product (PPF), and

increase the capacity of its current goods (SCF). Thus, ramping up of capacity provides the company with strong medium-term

growth visibility.

• GHFL has continuously increased the share of value-added products within its sales mix. Value-added products, which accounted for

48% of total sales in FY2017, increased to 80% in FY2023. This led to an improvement in its margin to 18.7% in FY2023 from 9% in

FY2017. As the company is planning to ramp up the capacity of value-added products and add new products, margins will continue

to improve going forward.

• The company has fully vertically integrated chips-to-film manufacturing facilities. These capacities are fungible and capable of

delivering customised products across a range of over 3,000 SKUs. Backward integration also helps the company’s R&D department,

as it leads to greater customization, faster time-to-market, and improved quality.

• Key risks: Sharp surge in oil price could impact margin/earnings. Sluggish demand in the automotive and real estate Industry

@Ascendant thanks for doing this. Been tracking this company for a while now, after it came up on my screens a few time, and I’d submitted some questions earlier to their “compliance” as well. Obviously, no answer.

I had prepared a note on this company but decided it honestly wasn’t worth all this effort to track and assess.

Interestingly, their CFO quit recently and guess who they appointed in charge? The IT head is now CFO.

I’d also offered to travel to their Goa warehouse and see these Edge data centres in realtime.

I went through the DRHP in depth, sat an entire day on it and yes, there are some weird things going on for sure.

I join you in your disbelief of how lacking the listing process must be.

Btw, Shankar Sharma has exited BCG. And I’m sure BCG most likely has at least some core business underlying while I’m not so sure of this one.

@Ascendant thanks for doing this. Been tracking this company for a while now, after it came up on my screens a few time, and I’d submitted some questions earlier to their “compliance” as well. Obviously, no answer.

I had prepared a note on this company but decided it honestly wasn’t worth all this effort to track and assess.

Interestingly, their CFO quit recently and guess who they appointed in charge? The IT head is now CFO.

I’d also offered to travel to their Goa warehouse and see these Edge data centres in realtime.

I went through the DRHP in depth, sat an entire day on it and yes, there are some weird things going on for sure.

I join you in your disbelief of how lacking the listing process must be.

Btw, Shankar Sharma has exited BCG. And I’m sure BCG most likely has at least some core business underlying while I’m not so sure of this one.