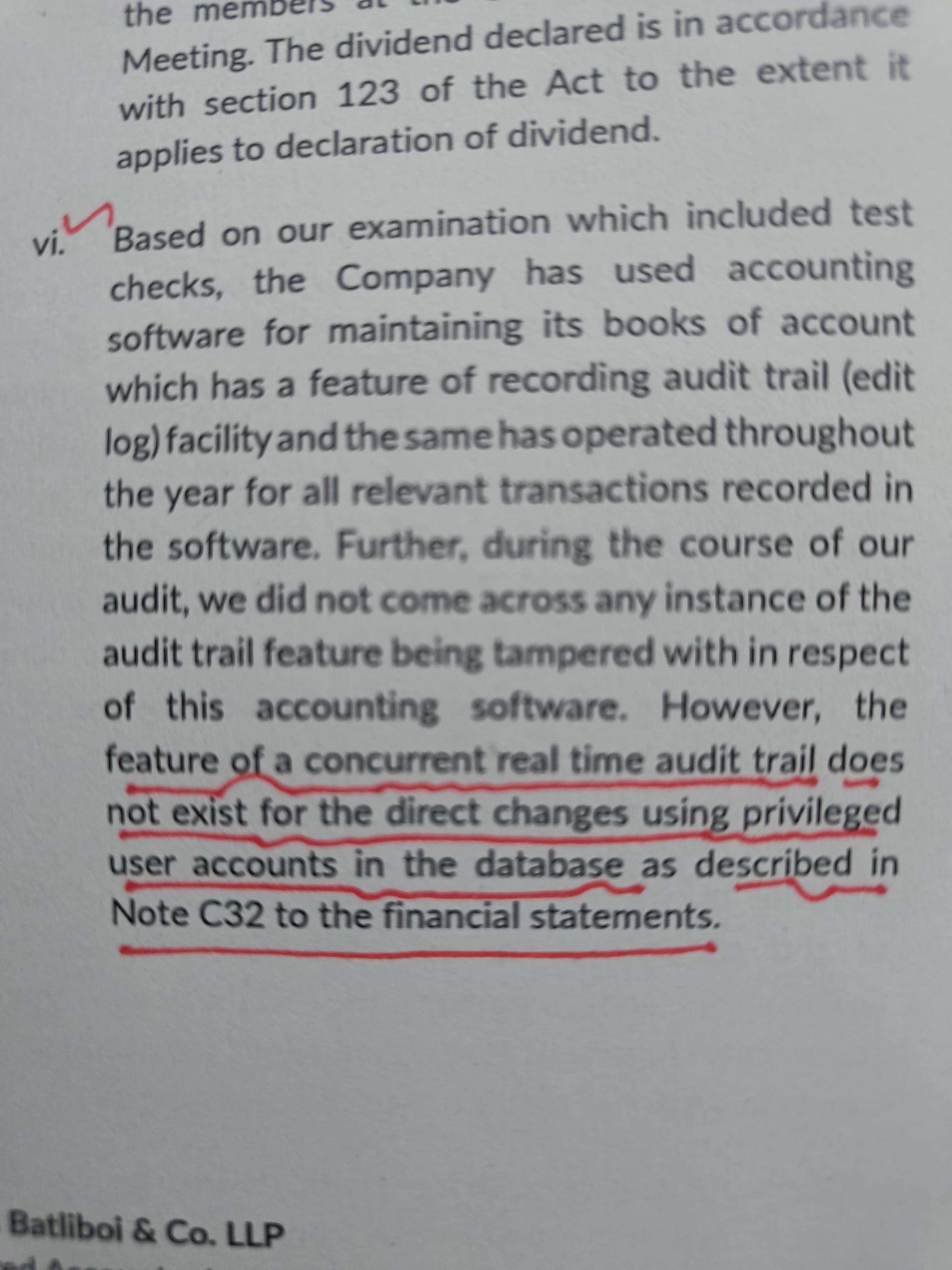

Can anyone say if this observation by Statutory Auditor is significant?

It was mentioned in Annual report FY23-24 of Apollo tyres.

Can anyone say if this observation by Statutory Auditor is significant?

It was mentioned in Annual report FY23-24 of Apollo tyres.

Any idea by when this event is scheduled?

Been a couple of months since last update here. Market has gone through its usual shakeout earlier this month and has bounced back just as it has done in the last few times. I saw people going into cash or going into banks and nifty – I think these are not so good moves.

While Nifty companies and the banks are relatively cheap, they are so for a reason. India’s growth in the last couple of years has been driven by erstwhile underperforming sectors, mostly in manufacturing and infrastructure. Nifty and Banks are focused primarily on consumption and banks have a problem with both demand and supply with demand going down due to deleveraged balance sheets and supply from higher rates causing NIMs to shrink. Its hard to say how long this will go on with equity capital being so cheap – so much so that it feels like a structural shift (I will reserve my judgement on that but so far, it does seem so).

Growth will continue to be driven by manufacturing and infra and capital goods and businesses focused towards these sectors are mostly smallcaps barring a handful of midcaps. A lot of ancillaries catering to these manufacturing and infra smallcaps are the microcaps and nanocaps universe – I think this is what we should keep in mind when someone says smallcaps/microcaps have runup too much. In the Nano/SME space there is perhaps visible manipulation and euphoria and venturing there should be done very cautiously.

Even if there is a crash, I expect a situation similar to 2018 herding to happen. However, this time herding may not be into Nifty and Banks but into smallcaps with great growth visibility. 2018 herding was driven by large fund managers. Current rally I feel is retail driven so I find it hard to believe they will get into a HDFC Bank or Reliance. Also fundamentally the way the economy is growing, i expect a lot of microcaps to become smallcaps and smallcaps to become midcaps than mid and largecaps growing bigger. It is simply not that kind of economy at present.

No changes to pf, except scaling up Strides. But there are lot of business updates which are worth looking at

Shaily, Weekly – Running sideways last 2 months. Fundamentally, the insulin opportunity could be big and there could be more where the 10 million pen order came from – discussed in the Shaily thread

Ceinsys, Weekly – Strong breakout on the weekly. It reminds me of the breakout in Shilchar from 1500 levels where it doubled in a month. Showing similar sort of strength here.

Lot of order wins taking the orderbook from 750 Cr to 1150 Cr which is phenomenal for a company with 275 Cr topline at present. Another good thing is the order size itself is going up and crossing 300 Cr+. I have discussed the moat ceinsys has in detail in the Geospatial thread. There might even be another large order of 385 Cr for which Ceinsys is the L1 bidder (explained in the thread).

The company expanded seating capacity by 200 last month and has so many open hiring positions. There is clear hunger for growth here

Wockhardt, Weekly – Gap up and circuit close on Friday and expect strong week here

WCK 5222 trials seems to be progressing well and should be completed in a few months time. Nafithromycin has got approval from CDSCO and should be in the market in a few weeks. WCK 6777 has got fast track status from fda after its phase-1 completion as per recent update. The market opportunity for Nafithro in India alone seems to be 400 Cr opportunity as per the chairman. Another good thing is the insulin opportunity as mentioned in the last post in August. There is a structural shift to biosimilars for insulin glargine driven by WHO and African countries are making this shift already (as with Algeria’s Biocare as mentioned in the Shaily thread). In developed markets as well price controls have put an upper ceiling of $35 and there’s a drive to make insulin cheaper through biosimilars. In all, the base business for Wockhardt is becoming stronger even as the NCE molecules are nearing fruition.

Strides, Weekly – This is one of my favorite chart patterns and it played out very well in VBL.

Fundamentally, this is a play on GLP-1 fill-and-finish, alongside a demerger opportunity. Stelis/Onesource is the fill-and-finish partner for Natco who has FTF on Ozempic. I would suggest going through @rupeshtatiya ‘s excellent thread on Strides, along with his recent AGM notes post. I think a 50-70% upside at least exists here from current levels conservatively.

Genesys, Monthly – Breakout and re-test. It should successfully pull away and close higher this month, hopefully.

Order book stands at 550 Cr. Bid pipeline is strong at 3000 Cr. Near term as well company has guided for executing substantial portion of the BMC order this year (350 Cr). H2 here should be strong

Orchid, Weekly – Multiple re-tests of previous breakout levels so needs a close above 1500 for continuation. There are lot of triggers in the next FY so things should get priced in over time. No big update here.

Small positions in Eimco, Tarachand and Garware remain and all of them have very strong tailwinds as well. I think that in general is the gist of it – if you see the 6 stocks discussed as well, they boil down to just 3 themes with tailwinds – GLP-1 (Shaily and Strides), Antibiotics (Wockhardt and Orchid) and Geospatial (Ceinsys and Genesys) – there’s a sub tailwind in insulin within this (Shaily and Wockhardt).

Apologies for the long post. Will stop here ![]()

Disc: Have positions in all as disclosed before. I am not SEBI registered and just a novice writing for clarity. Please do you own due diligence

is there any rule for remuneration resolutions which states that promoter entity cannot vote ? Weird that they did not vote on this resolution but voted on the rest of them.

Not an expert on this but I don’t think there is any rule against voting (based on a web search). I guess they decided to not vote on principle as they are an interested party.

I am not happy with this resolution also-

RESOLUTION 6: Approval for giving of loans, guarantee or security to any person in whom any

of the Director of the Company is interested under Section 185 of the Companies Act, 2013

Yes I thought this was a bad sign but then I saw the details of it in the AGM notice. It states allowing giving loan or guarantee for any loan taken specifically by M/s Kameda LT Foods (India) PL upto Rs.20 Crores, only for business activities. This seems okay to me.

Page 4 of https://www.bseindia.com/xml-data/corpfiling/AttachHis/b5baa352-2627-4167-8be6-b360ca3649bc.pdf

A Series on how parts are manufactured using CNC Machines.

I would be little cautious about Coal India ROCE going forward, as it has reduced Dividend Payout from 60% in FY22 to 42% in FY24. As a result, Reserves have increased from 36,980 to 76,567 Crores during the same period.

While this reserved profits will be certainly used for capacity expansion and expanding its Business lines, I believe that, moderation of Coal prices might have mild negative impact on Margins, Net Profits and ROCE will be under pressure.

Market may not elevate its P/B as it did during 2021 to 2024, and further re-rating in the stock could be limited. Margins are still good at about 33% and ROCE is also good at 64% but further improvement could be limited or Negative.

With reduced Dividend Yield at this Price point, I am more cautious now going forward compared to 2021 and 2022.

Disclosure: I have reduced my holding after the surge in Stock Price during 2023 and 2024, but may continue to hold it as a Dividend Stock with 4% to 5% Dividend Yield expectations. I might be wrong in my analysis as I am not a SEBI registered analyst.

Investor should be able to visualize the long term story behind the near term numbers. The validation which Neuland has got by being part of the potential block buster drug KARXT is very critical for its long term growth. The validation has come at an very opportune time when Indian companies are being looked upon as a CDMO partner and also as an alternate to Chinese companies.

Management has given conservative guidance of 20% growth for next 4 to 5 years from FY 2025-26 and FY 2024-25 has been projected as a year of consolidation. The KARXT growth was probably not factored in the estimates and projections and hence management may give some additional clarification on this .The quarterly results are going to be lumpy however the base figures are going to increase on a YOY basis.

I have discussed in my previous post also about the potential benefit of KARXT in Neuland future journey.

Disclosure : Invested for long term and views are biased.

Yes, you are right. This has also attributed to the Low Sales growth by IT sector by and large. Things should improve going forward and we may see a repeat of 2020-2022 period when Interest rates were on the downfall, off course it will be muted this time but it should have a positive impact on IT spends.

Thoughts on the latest numbers? Sales are flat. Is it an issue with the business or the slowdown in general that the management alludes to? I believe it might be an issue with the business where they are not able to grown their topline.

The wholly owned subsidiary to focus

on the retail business B2C under PM-Suryaghar (Rooftop Solar), PM-KUSUM schemes and B2C segments in RE and Emerging RE sector including EVs, Energy Storage, Green Technologies, Sustainability, Energy Efficiency,