Bankable: Personal Loans Do Not Meet Actual Family Needs, Says VP Nandakumar | BQ Prime

Posts in category Value Pickr

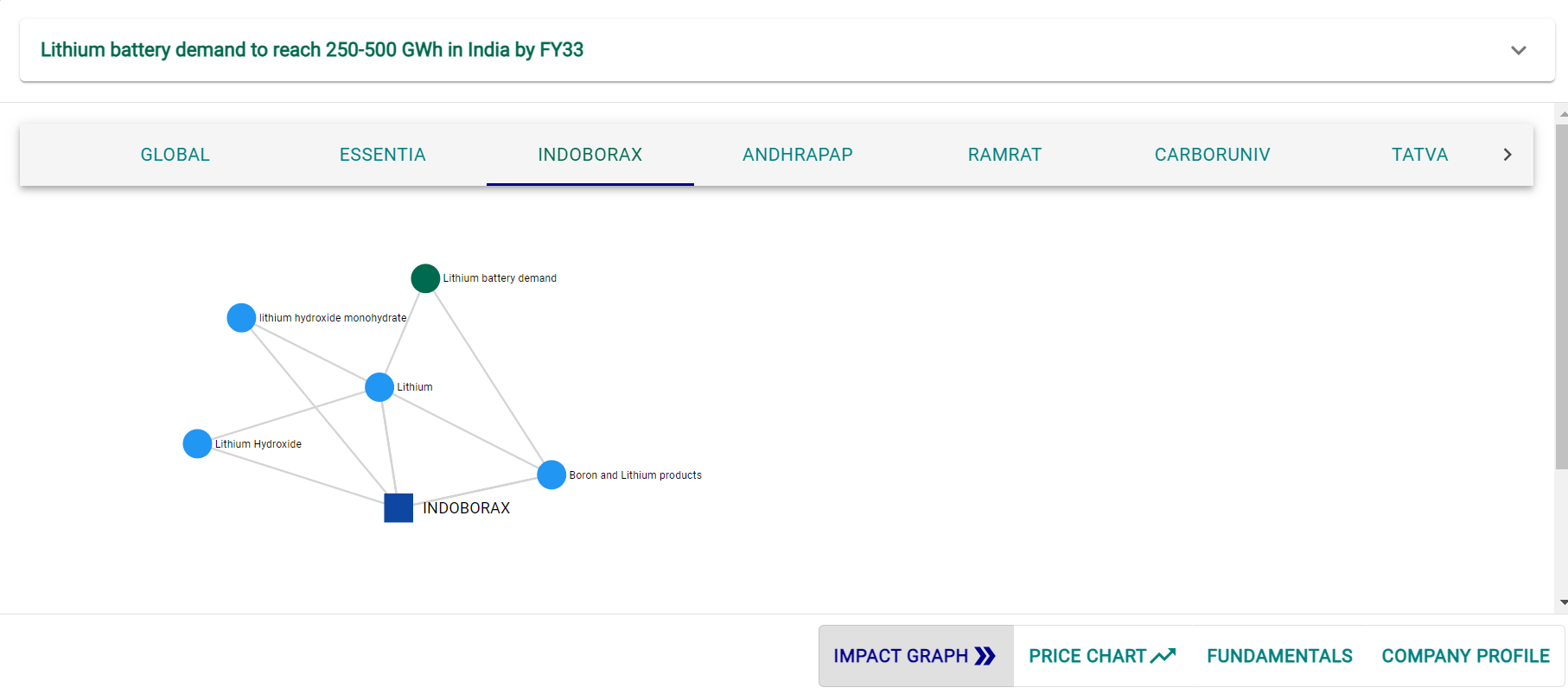

Indo Borax and Chemicals (19-10-2023)

Lithium Battery Demand Surge in India Expected to Bolster Indo Borax and Chemicals Stock

India is poised for a monumental surge in lithium battery demand, and Indo Borax & Chemicals Limited (NSE:INDOBORAX), a manufacturer and seller of boron and lithium products, stands to benefit significantly. With projections indicating that the demand for lithium batteries could reach between 250 to 500 GWh by fiscal year 2033, the company’s prospects are looking brighter than ever.

The recent report, titled ‘EV Batteries: Battle to control EV supply chain’ by Axis Capital, has highlighted that achieving a 250 GWh battery demand would necessitate incentives of INR 1.8 trillion over the period of fiscal years 2024 to 2028, along with an initial capital expenditure (capex) of USD 30-33 billion. This forecast is in line with India’s ambitious goals to electrify its transportation sector and reduce its carbon footprint.

So, how exactly is this bullish forecast going to positively impact Indo Borax & Chemicals Ltd’s stock price?

Increased Demand for Lithium Products : Indo Borax & Chemicals Ltd manufactures and sells lithium hydroxide monohydrate products. With the rapidly growing demand for lithium batteries in India’s electric vehicle (EV) market, the company’s lithium products are likely to be in high demand. This uptick in demand can potentially lead to increased revenues and higher profits.

Positioned for Growth : Indo Borax is already established in the Indian market and has been providing quality lithium products for years. This positions them well to capture a substantial share of the growing market, given their experience and track record.

Market Confidence : A booming industry and an established player like Indo Borax can instill confidence in investors. As they see the company benefiting from India’s electric vehicle revolution, it can attract more investment and drive up the stock price.

Favorable Regulatory Environment : As the Indian government provides incentives and support to the EV industry, it indirectly benefits companies like Indo Borax. The conducive regulatory environment can create a positive atmosphere for the company to thrive.

Strong Financial Performance:

In addition to these promising forecasts, Indo Borax boasts impressive financial credentials that make it a compelling investment opportunity.

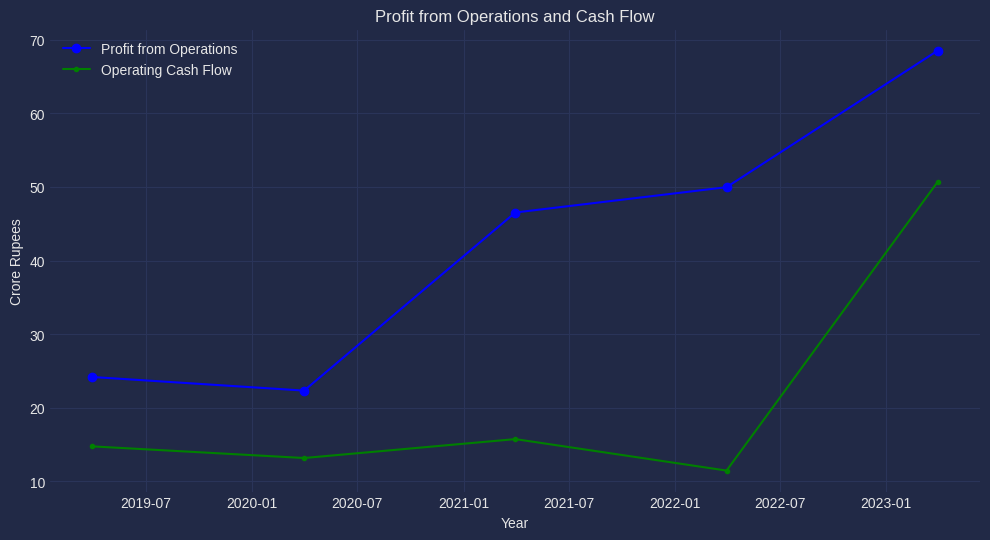

The above figure shows operating profit growth for the last 5 years.

Robust Profit Growth : Over the past five years, Indo Borax has demonstrated remarkable profit growth, with a staggering 243% increase. This equates to a compounded annual growth rate (CAGR) of 28%. Such consistent profit growth signifies a company that is efficiently utilizing its resources and generating value for its shareholders.

Strong Cash Flow Position : The company maintains a healthy cash flow position with a consistent 183% growth over the last five years and a CAGR of 23%. This strong cash flow not only ensures operational stability but also provides flexibility for investments in research, development, and expansion.

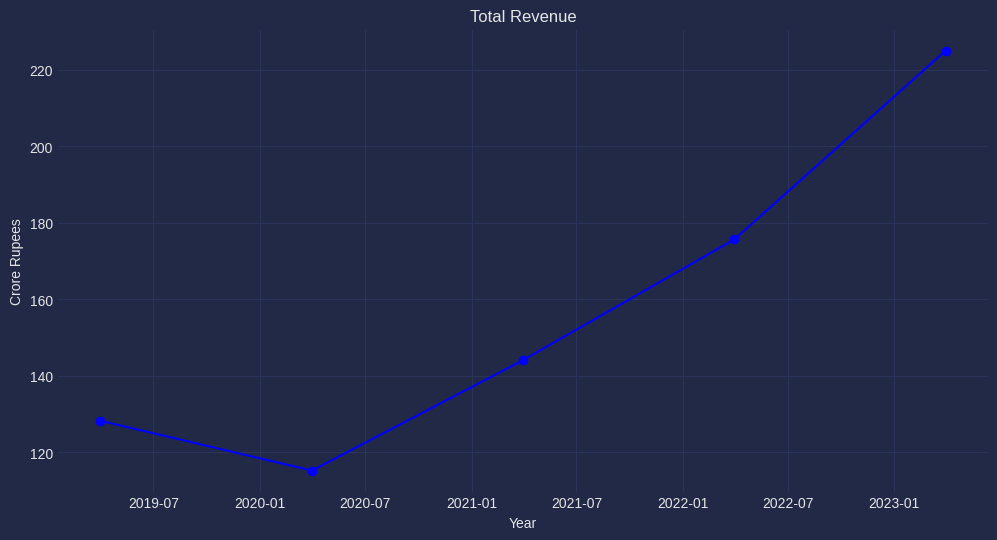

The above figure shows the revenue for the last 5 years.

Impressive Revenue Growth : Indo Borax’s revenue has surged by 75% over the past five years, demonstrating a CAGR of 11.89%. This growth highlights the company’s ability to capture market opportunities and meet the rising demand for its products effectively.

Attractive Valuation Metrics : The company’s PEG (Price/Earnings to Growth) ratio stands at 0.5, well below the typical threshold of 1. A PEG ratio below 1 suggests that the stock may be undervalued relative to its growth prospects.

Favorable Valuation Ratios : Indo Borax boasts a Price/Book (P/B) ratio of 2, which is below the industry median. Additionally, the Price/Earnings (P/E) ratio is a modest 10.7, also below the industry median. These metrics indicate that the stock may be attractively priced compared to its peers.

Debt-Free Status : The company’s debt-free status is a significant advantage in a potentially high-growth industry. It means that Indo Borax does not have substantial interest payments or debt-related risks that could hinder its growth or financial stability.

Conclusions

In conclusion, the surging lithium battery demand in India is expected to have a positive impact on Indo Borax & Chemicals Ltd. In light of Indo Borax & Chemicals Ltd’s robust financial performance and the burgeoning demand for lithium batteries in India’s electric vehicle market, the company is well-positioned to thrive. These factors, combined with a favorable regulatory environment and established market presence, bode well for the company’s future. The company is well-positioned to capitalize on this trend, potentially leading to increased revenue and growth opportunities.

Reference: Lithium battery demand to reach 250-500 GWh in India by FY33

Disclaimer: The article is not a recommendation or advice as to whether any investment is suitable for a particular investor.

EPL – Essential Packaging Company (19-10-2023)

One additional trigger will come post FY24 is that the TSA fee paid by Blackstone to the erstwhile promoter would go away and that would also lead the PBT to go up 16 cr

Essel Propack Limited Open Offer LOF_p.PDF (sebi.gov.in)

The agreement signed at the time of acq. was for five years which should end in FY24 as the acquisition happened in 2019.

Phantom Digital Effects Limited (19-10-2023)

Anyone interested in studying the company can go through the post written below i.e. Phantom Digital Effects Limited – Knowledge Seeker

E2E Networks Ltd – Listed small Cloud computing player (19-10-2023)

Latest on future of Diagnostic imaging using Generative AI –

https://www.expresshealthcare.in/news/future-of-diagnostic-imaging-using-generative-ai/441050/

Shakti Pumps – solar shakti (power)! (19-10-2023)

The press release talks about empanelment which technically means their products are qualified by state govt and such sale would probably happen through the govt or if someone buys it they will get subsidy. Just wanted to understand, whether empanelment and actual orders are the same. Also the “Empanelment” is for 50,000 sets, does it mean that this is a fixed order or empanelment will stay till the quantity is procured under this scheme.

Shakti Pumps – solar shakti (power)! (19-10-2023)

The press release talks about empanelment which technically means their products are qualified by state govt and such sale would probably happen through the govt or if someone buys it they will get subsidy. Just wanted to understand, whether empanelment and actual orders are the same. Also the “Empanelment” is for 50,000 sets, does it mean that this is a fixed order or empanelment will stay till the quantity is procured under this scheme.

RPG LIFESCIENCES – Change in Governance and Performance (19-10-2023)

Excellent results by RPG.

Attaching the results and the Investor Presentation below

https://www.bseindia.com/xml-data/corpfiling/AttachLive/55744826-2434-49b7-91fd-a6bb060bb964.pdf

Invested since 600-700 levels and BIASED

RPG LIFESCIENCES – Change in Governance and Performance (19-10-2023)

Excellent results by RPG.

Attaching the results and the Investor Presentation below

https://www.bseindia.com/xml-data/corpfiling/AttachLive/55744826-2434-49b7-91fd-a6bb060bb964.pdf

Invested since 600-700 levels and BIASED

Raymond – The Complete Man (19-10-2023)

That’s a fair observation. And I’m a novice maybe I’m wrong but I’ll try to explain better what I meant by the comparison my facts may be a little off but just sharing my rationale

- Companies like Trent & Aditya Birla Fashion keep acquiring new brands and keep growing them. Trent is particularly good at it and has very high PE, AB not that much

- Trend PE is 165 & ABFRL is a loss making company, hasn’t posted a profit in the last 4 years. I don’t know how to judge if a company is fairly valued when it’s loss making and to be honest tracked it at all

- Companies like Vedant Fashion is focusing on particular segment and goes very deep in it (wedding and festivity ethnic collections like Manyavar). Margins are very high in this and hence commands high PE

- Agreed Vedant Fashion is a great company shows from their profit margins and ROCE and maybe a multibagger in the making but capital is finite and I wouldn’t be interested in Vedant Fashion at these valuations

- Raymond has a mixed business on the lifestyle vertical

a. Core textile business

b. Few own brands (Raymond, Colorplus etc) and doesn’t add anything new (or add very rarely)

c. As mentioned above, the new brand they added is Ethnix and want to grow it like Manyavar of Vedant

- In one of the interviews the CFO of Raymond mentioned that in every wedding at least 1 Raymond suit is used (Not quoting paraphrasing). That to me highlights the power of this brand. In spite of having such a strong brand they never killed it because of governance issues which also lead to too much debt and looks like both are resolved.

- Looks like management is getting aggressive in their approach they plan to get 500 new franchisee outlets. And moving from asset heavy to assets light model for expanding their footprint.

- Ethnix looks like a great expansion. Every year we hear this wedding season will be the biggest we’ve had so far and I believe this trend will go on for another decade the way our population is skewed.

Here’s a list of other branded play with their earning multiples

Redtape – 52x

Go Fashion – 82x

VIP – 84x

Indian Terrain – 57x

- When I talk about Raymonds as a fashion and premiumisation play I don’t mean to compare it with the MANYAVARs of the world and hence not looking for a 70-80x earning multiple but a reasonable 30x won’t be too much to ask for considering their brand recall and their distribution.