Update on Tax Demand for AY 2018-19

The Commissioner of Income Tax (Appeals), has vide its order dated October 17, 2023, has considered and accepted the appeal of the Company thereby effectively rejecting all the grounds on which the Income Tax Demand of ₹122.63 Crores was made against the Company for AY18-19.

Posts in category Value Pickr

CreditAccess Grameen: Traditional MFI model, efficiently operating at scale (18-10-2023)

Syngene International (18-10-2023)

Q2FY24 results

Press Release

Syngene reports strong second quarter results:

Revenue from operations up 18.5% to Rs 910 crores,

PAT (before exceptional items) up 20% to Rs 122 crores

First half FY24 revenue from operations was up 22% to Rs 1,718 crores;

Profit after tax (before exceptional items) up 23% to Rs 215 crores

EBIDTA and PAT margins Flat

Jonathan Hunt, MD and CEO, said, “I am pleased to report a strong set of results for the second quarter and first half of the financial year, particularly in our Development and Manufacturing Services. In Development Services, we also added a new non-GMP capability center to meet market demand for agile, cost-efficient, early phase development and scale-up services. In Manufacturing, we made good progress on our long-term biologics partnership with Zoetis, as well as commissioning a state of the art, digitally-enabled Quality Control laboratory to support our growing biologics operations.

The acquisition of a multi-modal facility from Stelis Biopharma Ltd, announced last quarter,

is progressing.

Within research services, our Dedicated Centers made a steady contribution to growth and

in Discovery Services, while global demand remained generally healthy, we saw the USbased biotech segment showing signs of slowed growth year-on-year as companies adjust

to a new funding environment.

Long term sector fundamentals remain strong and we expect continued growth but at a

lower level in the second half of the year, this short-term slowing in the US biotech segment

is reflected in our latest outlook.

Overall, we reported a strong first half to the year and I am pleased with the good progress

made on our strategic priorities in both our research services and our development and

manufacturing divisions.”

Guidance

While the Company delivered strong performance in the first half, with the temporary

slowdown in US biotech funding, we expect continued growth at a lower level in the second

half of the year. Adjusting for this, against our previous guidance of high teens constant

currency growth, we now expect the revenue to grow at mid-teens on constant currency

basis.

Microsoft Word – Press release (bseindia.com)

Microsoft Word – Investor Presentation (bseindia.com)

Mudit’s Portfolio (Passively Active) (18-10-2023)

Any Particular reason to have both KEI and Polycab.

Phillips Carbon Black (18-10-2023)

PCBL Ltd Q2FY24 Concall Highlights

PCBL | CMP: INR 198 | Mcap: INR 74.76bn

Volume is expected to grow 12% to 13% over the next 4-5 years.

Capex of INR 12.8bn would bring additional revenue of INR 17bn – INR 18bn per annum going forward.

EBITDA per tonne is expected to reach INR 20,000 by FY27E.

Europe exports are expected to double in the next 2 years.

Revenue

Revenue is expected around INR 16bn to INR 17bn per quarter if crude remains stable.

Margin

Specialty chemical black margins are 2-2.5x of Tyre margins.

Volume

Volume growth is expected around 12% to 13% over the next 4 to 5 years.

Domestic sales volume stood at 82,276MT and International sales volume stood at 47,835MT in

Tyre volume stood at 79,793MT, Performance chemicals volume stood at 34,744MT, and Specialty chemicals volume stood at 15,574MT in Q2FY24.

In the Chennai facility, production volume is around 9,410MT (~50% utilization) and sales volume is around 9,008MT in Q2FY24. Overall, the Chennai facility sales volume was around 14,000MT in H1FY24.

Specialty chemical volume is expected around 50,000MT to 55,000MT in FY24. Q3FY24 volumes are expected to be better.

Capacity & Utilization

The capacity stood at 7,72,000 MTPA as of Q2FY24. The company is expected to ramp up utilization in the next 3 to 4 months. The maximum capacity achievable is around 6,25,000 MTPA (~81% utilization).

The Chennai facility is expected to reach around 80% capacity utilization in the next 3 to 4 quarters. The approvals are expected to come from Tyre manufacturers which will ramp up production.

Specialty chemicals capacity stood at 92,000MT and another 20,000MT is expected to be added going forward.

Around 90,000MT rubber facility is expected to be commissioned in the next 1-2 years.

The company has commenced a 12MW captive power plant in Chennai and the total captive stood at 112MW. Another 12MW is expected to commence going forward.

Capex & Incremental Revenue

Chennai greenfield facility capex is around INR 9.5bn and incremental revenue is expected around INR 14bn. Mundra facility capex is around INR 3.3bn. Mundra facility has two phases. 1st phase capex is around INR 2bn and Incremental revenue is expected around INR 2.2bn going forward.

Maintenance capex is around INR 120mn to INR 130mn per plant which comes around INR 600mn to INR 650mn maintenance capex annually.

Patents

The company has received two patents and started manufacturing for 2 grades. The initial market potential is around 2,000MT-3,000MT and is expected to reach 6,000MT-7,000MT over the medium term. the specialty products contribution realization is around $1,200 – $1,300 per tonne.

Exports

In exports, around 70% of sales from Asia Pacific remain from other countries. The company is exporting to more than 50 countries.

Europe has larger potential and the company is focused on supply chain improvement. Europe volume is around 3% to 4% and expected to be 2x in the next 2 years.

Realization

EBITDA per tonne is around INR 18,427 in Q2FY24 and is expected to reach INR 20,000 by FY27E.

Other highlights

The company is focused on adding capacity every year.

The company is supplying battery chemicals to 2nd and 3rd generation batteries.

Tamil Nadu facility is efficient from a tax point of view.

Outlook: PCBL volume is expected to grow 12% to 13% over the next 4 to 5 years. The capex of INR 12.8bn in Chennai and Mundra facilities would bring additional revenue of INR 17bn to INR 18bn per annum going forward. Europe exports are expected to double in the next 2 years.

Companies with 20%+ growth guidance for next few years (18-10-2023)

Hi Kumar

Good compilation.

I wonder how you are following these companies. Do you have references to these forecast such as annual report, concall transcripts. I would be happy to

collaborate and track these companies and their progress.

Thanks & Regards

Bala. P

Atam Valves Ltd (AVL) (17-10-2023)

I have invested in August, 2023 and hope that management delivery what they have planned.

Companies with 20%+ growth guidance for next few years (17-10-2023)

Hi,

I am starting this thread to list companies which has provided 20%+ growth guidance for next few years. Please feel free to add to the list. We can try to keep it updating after every quarterly concall or any growth guidance update from the management.

RK Forging – 20% rev growth for next 3 years

VST Tillers – growth of 25-30%. FY 23 – Target 1000 cr revenue, FY 26 – Target 3000 cr revenue

Gravity India – growth guidance of 25% for next 2-3 years

Permanent Magnet – 20-25% growth guidance

SBCL – 20% for next 5 years

Focus Lighting – 30-40% growth for next 3-4 years

Jyoti Resin – 25% growth for next 3-4 years

Gensol engineering – Triple revenue from 400 cr to 1300 cr by FY24 and 5000 cr by FY25

Elecon Engineering – 30% growth guidance(FY 23 rev – 1530 cr, FY 24 guidance 2000 cr)

Spandana Sporty – FY23 rev 8511 cr, FY24 11500 cr, FY25 15000 cr

ACE – 25-30% growth guidance

Salzer electronics – 20-25% growth guidance FY24

Syrma SJS – 30-35% growth for FY24

Map my India – 30% revenue growth till FY26. Target to have 1000 cr rev by fy 27-28 from current 280 cr rev

Onward Technologies – Revenue to be up by 70% by FY26

RACL Geartech – Revenue to double by FY26

Pricol – Revenue to double by FY26

Avalon – Revenue to double by FY26

Menon bearings – Revenue to double by FY26

MapMyIndia – 35-40% CAGR for next 5 years; Revenue target of 1000cr by FY27/FY28

Shivalik Bimetal – Revenue target of 4X in 6-7 years

UGRO Capital – 60-70% growth expectations in next 2-3 years

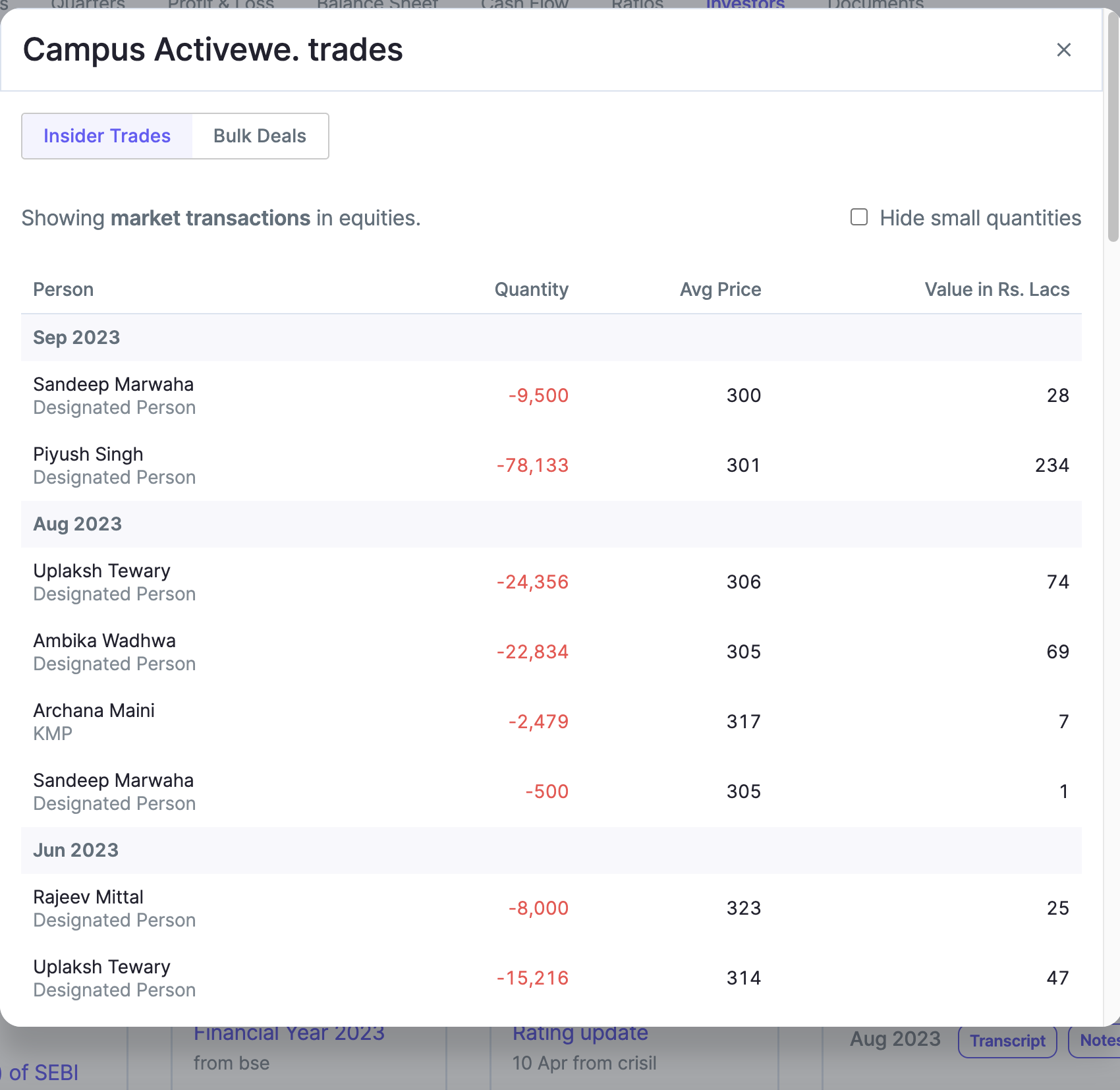

Campus Activewear – betting on the India Consumption Theme (17-10-2023)

Continuous selling & insider trades is not encouraging