Idfc first bank has a very strict credit writing system in place . Mr VV has repeatedly told in his interviews that about 60% of the loan applications are rejected by the bank. Also we should not forget the excellent track record of Mr VV in building retail business in ICICI bank and Capital First. Almost all the targets set by bank at the time of merger have been met before time. Having account in the bank for the last 4 years and fully satisfied with their services. I think banks don’t prompt you to use your credit card reward points while doing online payments but this bank does. Invested since 2019.

Posts in category Value Pickr

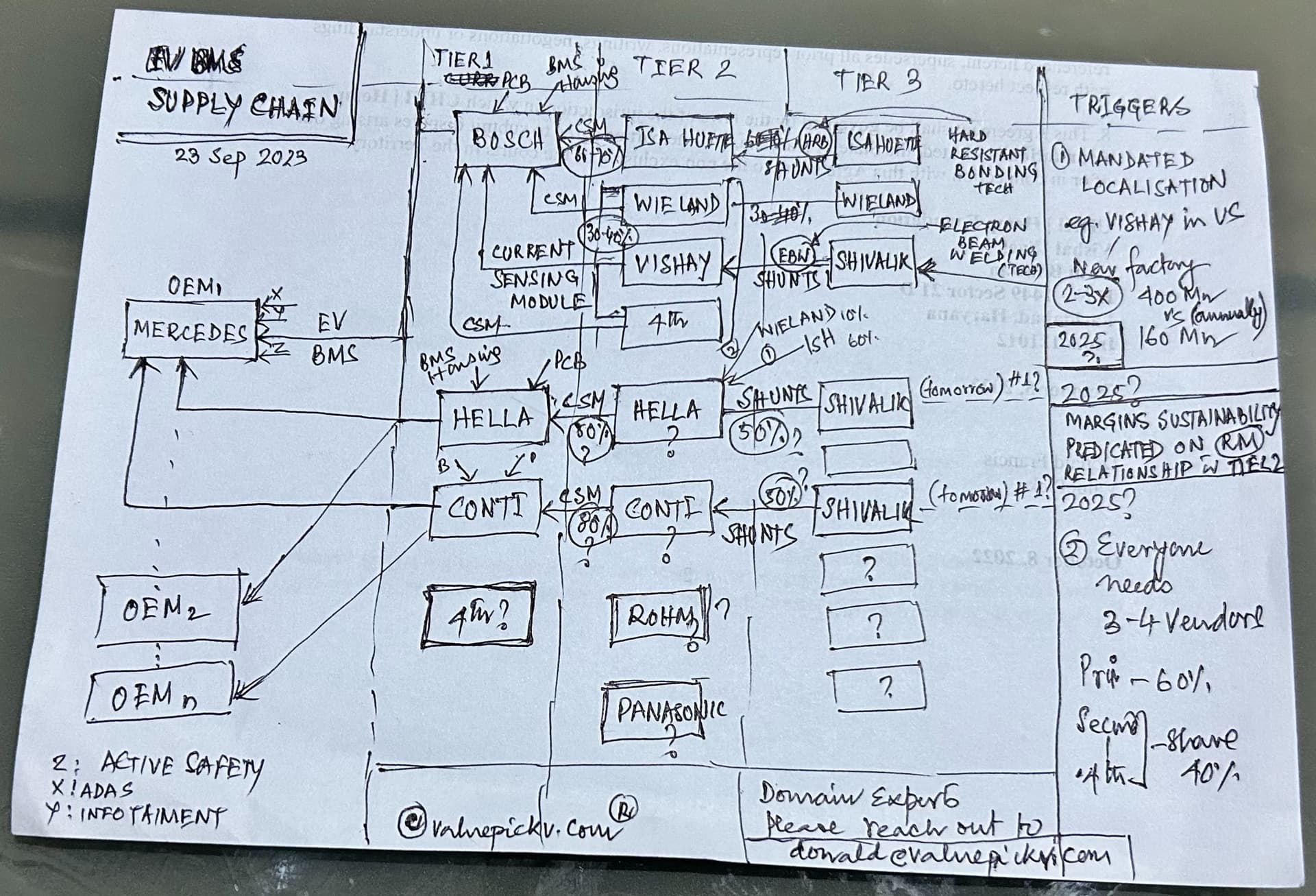

Shivalik Bimetal Controls Stock Story (23-09-2023)

To my mind, this (not so complex ![]() ) picture has it all !!

) picture has it all !!

Please take your time perusing this, all the clues are in.

This is why/how we think SBCL is getting to a stronger trajectory. IF Industry Tailwinds last (no inventory glut situation in near to medium term like we saw in 2018), then SBCL Competitive Position will indeed become much stronger. It will be very difficult to dislodge this business from its perch.

If we can NAIL this down – get the answers from Shivalik Mgmt (fill in the gaps, get confirmations) AND get it corroborated from domain experts in the automotive EV BMS Supply Chain, our SBCL 2023 AGM job is done!!

SBI Cards & Payment Services Limited (23-09-2023)

Hi,

Nope, long term this is a macro story. As per my opinion if you are looking at investing perspective this is a good company to hold in your portfolio. I have exited looking at chart structure. Although i am learning and there is still a lot to learn for me to share a definitive call.

Some good points for the stock:

- Good brand

- Good management

- Credit use is increasing in the market

- Only point to watch out for is rise in NPA but that would happen if the condition of the economy goes bad. Also, i think their grip is better in Tier 2 and tier 3 cities where folks are not savvy regarding credit use.

But all in all good company to hold for long term as long you keep on tracking their numbers.

SKM Egg Products – thinking out of the shell (23-09-2023)

Some of the interesting snippets from Care rating report. Also, adding the whole report at the end

[From the information on Annual report, the contribution of sales asia, africa and gulf countries likely to increase going forward]

Market cap ~ 1,000 Cr.

Link to the rating report from Care – https://www.careratings.com/upload/CompanyFiles/PR/202307140711_SKM_Egg_Products_Export_(India)_Limited.pdf

Cooling of Eggs prices in global market might mean higher competition for the company in its market. That may impact the margin. But at this point this is just my speculation. There is no word from management or any experts that I know of.

B C C Fuba India Ltd: PCB Manufacturing Nanocap (23-09-2023)

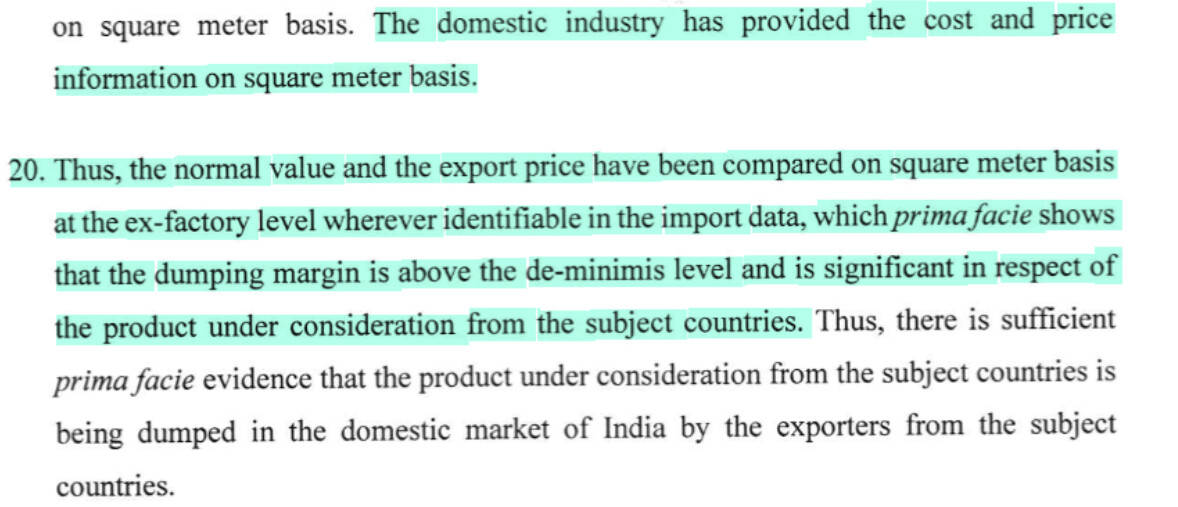

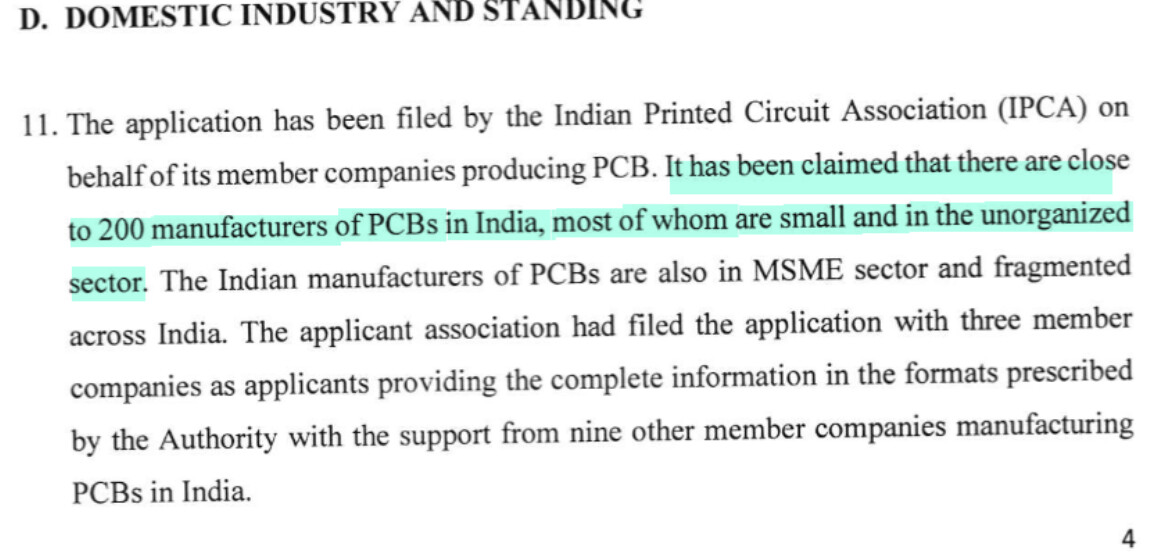

Here is latest on Anti dumping duty case status filed by IPCA(India Pcb mfgr assicoation) on behalf of PCB manaufactures in india, details for folks interested to check out are here

- Prima facie there seems to be a merit in case as evaluated at time of admission

- some more intersting data of industry size/ players in case details – 200+ small manufactuers, however top few players contribute a 25%+ share (per case doc) – indicates a fragmented industry – if we look at margin range as showon in above post its all over and will likely differentiate efficient players – would be worth investigating as to what are the drivers working for some players (e.g. one factor for Fuba seem to riding on Auto industry incldg EVs where it takes longer time to qualify and become supplier).

- Industry association for PCB mfgr has some more resources

https://www.ipcapcb.org/

While case is still ongoing and may see outcome soon, whats interesting is that players like BCC Fuba seem to be doing well (incldg AGM commentary from mgmt) irrespective of this case ADD outcome, it may create additional tailwind for industry itself if ADD were to be imposed on imports of PCB. In general clear mandate of make in india and domestic industry focus from Govt – its more likely to see favorable outcome – extent/impact to be seen.

D – same as before

Mrs Bectors Food Specialities: Can it beat the industry? (23-09-2023)

I am holding and also trying to accumulate more as my conviction increases.

Edelweiss Financial Services (23-09-2023)

Then it will be cheapest compared to its peers…As per 1st quarter results this year PAT Must around 400 Cr…

NCC: Extremely undervalued (23-09-2023)

Hi – Does anyone have any information on where this stands? Given the low promoter holding and they issuing warrants just prior to big win, want to reconfirm on corporate governance before investing. Thanks

SKM Egg Products – thinking out of the shell (23-09-2023)

During the first quarter of the FY24, there is 12% QoQ growth & 57% YoY growth with slightly better margins than those in FY23. Apart from pointing to Russia Ukraine war, the annual report points to penetration in quite a few geographies as well as launch of new products.

That being said, I am not in position to comment if FY23 or Q1’24 performance is sustainable as I am not proficient enough in understanding the global market dynamics of eggs and its derived products. If you have got hold of some information/knowledge which can point towards the probability of non-sustenance of company’s performance, that will help the investors in this community.

Vesuvius : Leader in Molten Metal Engineering (23-09-2023)

Hi @Surender, Thanks. I have not studied Vesuvius in much detail, but my guess is whatever has worked well in case of RHIM will apply equally to Vesuvius as well. Some businesses are inherently good businesses to invest in, and refractories seem to be one such. The moat is the same.