Now they are opening a NBFC to finance the Company’’s Products and Consumers. Interesting Escorts Finance revoked its NBFC license earlier and has changed that AoA and Memorandum to change the line of business, Alos it was renamed to “Invigorated Business Consulting Limited”

Posts in category Value Pickr

Glenmark Life Sciences (21-09-2023)

Glenmark Pharma to sell 75% stake to Nirma @615 per share

Glenmark Pharma will retain the remaining ~7%

Nirma to make open offer

Is there any price calculation to be used for open offer (as per SEBI rules) to protect minority interest?

Journey and Portfolio of a goal-based NEEV investor (21-09-2023)

Hi Shubham,

While I won’t be able to share my personal spreadsheet (for obvious reasons), this blog post by M Pattabiraman should do justice.

Please go through this elaborate post which also has many interesting links to similar spreadsheets that effectively help one to track and measure investment performance in an autonomous way Track your mutual fund and stock investments with this Google Sheet!

Hope this helps!

Praveg Ltd: Play on Indian Tourism Industry! (21-09-2023)

It seems Praveg shareholders having rock solid conviction to hold the stocks for long time. At a time when the whole small-micro cap space is going through correction, it’s good to see Praveg is doing well. Thanks to company’s extremely positive future outlook.

Anyone who is tracking Praveg must listen to the last concall. The management is crystal clear on future planning and execution.

Though not having a strong moat, given the total addressable market size company should do extremely well in next few years. Low liquidity is a concern though. A stock split here will solve liquidity problem to an extended.

I want to deploy 15-20% of PF in this. What cons do you guys see?

Dis: Holding a tracking position.

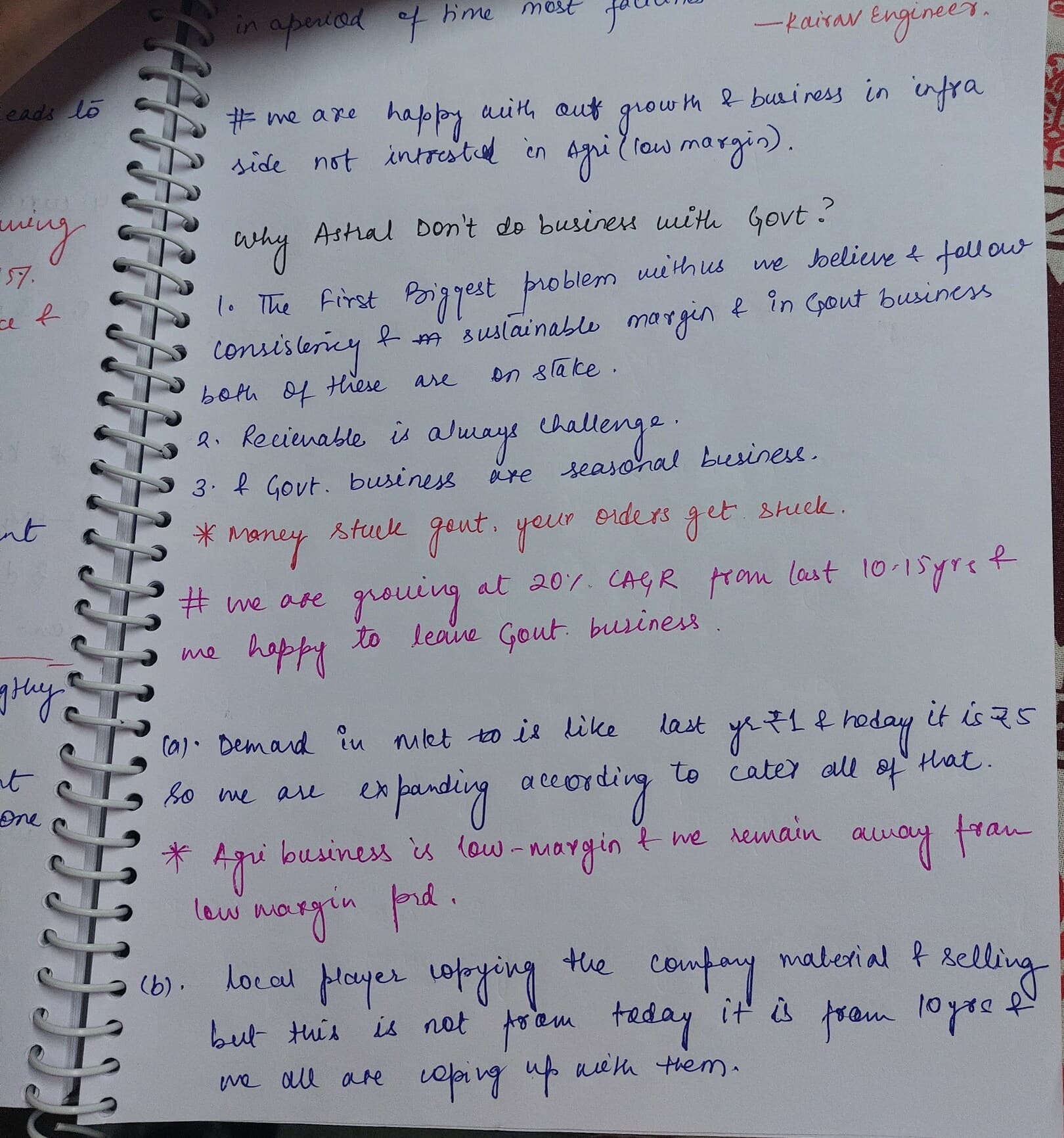

Astral Ltd. (Earlier: Astral Poly Technik Ltd.) ~ Leading Pipes & Adhesives company (21-09-2023)

Why astral not deal with government for business? from their recent con call

Hitesh portfolio (21-09-2023)

@hitesh2710 Hello sir,

Can you please share your opinion on bectors food because currently at quite high valuation but the business has a literally long way to go because they are planning out to pan out their distribution to whole country

Great articles to read on the web (21-09-2023)

Source: Trendlyne

The $100 predictions for oil prices are back. Crude oil prices touched their 10-month highs on Tuesday, as OPEC+ extended production cuts till the end of the year.

But this did not stop the Nifty 50 from hitting its all-time highs in the past week and gaining 2.5% in September, despite falling 1.2% on Wednesday. Crude oil prices increased by 6.9% over that same period – which should be a major concern for India, a net oil importer.

Investors however, are overlooking rising oil and food prices and focusing instead on India’s long-term growth. According to the World Bank, India will be the fastest-growing economy in FY24 with a 6.3% growth rate. In Q1FY24, India’s GDP [accelerated](India Q1 GDP Growth Highlights: India’s Q1 GDP growth rises to one-year high of 7.8%; RBI to maintain FY24 projection | Mint to 7.8% YoY, beating analyst expectations.

To keep growth momentum going, the Centre earmarked Rs 10 lakh crore for capital expenditure in FY24. By June end, the Centre had already spent 27.8% of the budgeted capex. As 2024 is an election year, there are plans to use at least 60% of this allocation by October.

While the government has pushed spends in the past two years, the long-awaited ramp-up in corporate capex has not happened. The private sector is cautious, hesitant to invest. Companies are sitting on their hands – the question is why.

In this week’s Analyticks,

![]() Capex Imbalance: Government drives capex surge as private sector hits the brakes

Capex Imbalance: Government drives capex surge as private sector hits the brakes

![]() Screener: Companies with highest estimated forward capex growth for FY24, and rising cash flow from operations

Screener: Companies with highest estimated forward capex growth for FY24, and rising cash flow from operations

Is weak corporate spending hurting India’s growth trajectory?

Capital expenditure (capex) is crucial for economic growth, as it helps create and improve long-term assets like buildings, equipment and infrastructure. Such spending comes from the government, businesses and households. While government capex has surged in the past few years, business investments have been lagging.

In response to a question about business capex, Finance Minister Nirmala Sitharaman had said in December 2022, “Private capex is picking up, thanks to measures such as production-linked incentive (PLI) schemes…this will drive a virtuous investment cycle in the economy.”

Despite her optimism, the share of corporate investments in total capex fell to a 19-year low in FY23.

Despite efforts to stimulate corporate spending—such as tax cuts in September 2019, increased government capex to attract private investment, and the introduction of Production Linked Incentive (PLI) schemes—we have not seen the much-hoped for boom. And it isn’t debt that is holding businesses back, since the corporate sector’s debt-to-equity ratio is at a 15-year low.

Government capex has the lion’s share, as it rises sharply in Q1FY24

Corporate capex is estimated to have fallen for the second consecutive quarter, with a projected decrease of 6.2% YoY in Q1FY24. However, the government came to the rescue – total capex is still set to rise by 7.1% YoY, thanks to a 54.1% spike in government capex, which made up for the fall in private investments.

Corporate investments contract for the second consecutive quarter in Q1FY24

Corporate investments contract for the second consecutive quarter in Q1FY24

The decline in corporate investments for two consecutive quarters has resulted in its share in total capex dropping to a 19-year low of 41.2%, compared to a pre-Covid average of 51.2%.

Share of corporate investment in total capex hits 19-year low

Share of corporate investment in total capex hits 19-year low

The government’s focus on infrastructure has raised the sector’s share of total capex from 2.5% in Q1FY17 to 11.1% in Q1FY24. Investments from private players are concentrated in a few sectors. Hetal Gandhi, director of research at Crisil Market Research and Analytics, said, “Private investment is leaning towards cement, auto, oil & gas, green technologies, and areas driven by PLI schemes.”

Roads and bridges gain larger share in banks’ sanctioned project costs

Roads and bridges gain larger share in banks’ sanctioned project costs

While infrastructure companies’ aggregate cost of sanctioned projects has risen sharply, the power and construction sectors’ capex has fallen.

In Q1FY24, newly announced projects hit a five-year high at Rs 5.96 lakh crore. However, 74% of these investments came from the airlines sector, which ordered new planes by the hundreds.

Other sectors like power (10%), chemicals (8%), machinery (3%) and auto (2%) contributed relatively lower shares.

Airlines sector leads new projects announcements with huge orders

Airlines sector leads new projects announcements with huge orders

Companies are worried about high interest rates, uncertain economy

Inflation and high interest rates have got India’s private companies worried. High inflation took a significant bite out of corporate margins in FY23.

In an effort to bring down inflation, the Reserve Bank of India (RBI) raised interest rates by 250 bps to 6.5%, and has since paused further hikes. Businesses are unwilling to take on debt at these higher interest rates, and are waiting for potential rate cuts. Commenting on this recently, Satish Pai, Managing Director of Hindalco Industries, said, “Interest rates are up, which makes borrowing less attractive. So, we will work with what we have in our internal accruals, because money costs more now.”

But the recent spike in inflation in July and August means that the RBI may have to wait longer before cutting rates.

India’s CPI inflation exceeds RBI’s upper limit of 6% in August

India’s CPI inflation exceeds RBI’s upper limit of 6% in August

While private companies have strong balance sheets, inflation, uncertain global economic conditions, and high interest rates are roadblocks to anything they see as non-essential spending. Ambitious projects are more likely to be postponed.

The upcoming election in 2024 is also influencing decisions in the C-suite. Companies are cautious about policy shifts that may occur with a change in government. They will wait for clarity before committing to significant investments.

Addressing the sluggish pace of private capex, former RBI Governor C Rangarajan said, “The government has done a lot at the macro level to crowd in private investment. The next step is to evaluate each sector to see what is holding them back, and resolve the issues.”

With capacity utilisation rising, analysts believe private capex will take off

A recent, positive sign however, is the surge in India’s index of industrial production (IIP), which grew at the fastest rate in five months to 5.7% YoY in July. The mining, manufacturing and electricity sectors have shown growth compared to the same period last year.

India’s IIP tops estimates and rises 5.7% YoY in July

India’s IIP tops estimates and rises 5.7% YoY in July

The IIP rising for nine straight months indicates high demand, and increased capacity utilisation among companies.

Current capacity utilisation for Indian companies stands at 76-78%. Analysts believe that crossing the 80% threshold could trigger major capex from private companies to meet higher demand.

Any fall in inflation, followed by interest rate cuts, will also jumpstart spending and get companies back on track with their investments. ICRA estimates that the RBI may start to cut interest rates in the second half of 2024. But if corporate investments stay sluggish, it will put pressure on the government to keep capex high, increasing the fiscal deficit.

According to Chief Economic Advisor (CEA) V Anantha Nageswaran, government capital expenditure cannot continue to rise at the same pace. The private sector needs to take over as the primary driver of capital formation. India’s economy will fire up in earnest only when private firms join the capex party, and keep the growth momentum going.

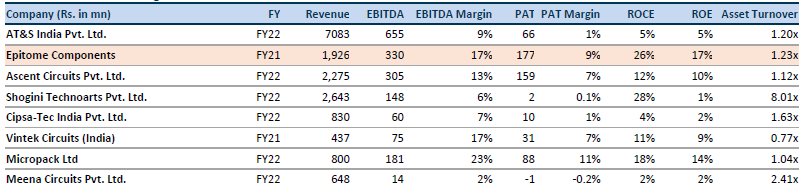

B C C Fuba India Ltd: PCB Manufacturing Nanocap (21-09-2023)

These are the margins of various companies in the industry

Techno electric engg ltd (21-09-2023)

Check power mech transcript and you will know at what rate (per MW) they got the large Adani order.

B C C Fuba India Ltd: PCB Manufacturing Nanocap (21-09-2023)

I was looking at the annual revenues of BCC Fuba. In FY19 they saw a revenue jump of almost 170% (41 Cr v/s 15 Cr in the previous year). However the operating margin was only about 1.75%. In the previous years they were making losses at the operating level. The operating margins seem to have improved in post-covid years. In FY23 it was about 10.7%.

My question is – what is the level of sustainable margins that one can expect in this industry?

I think in terms of value addition, bare PCB manufacturers do the least amount of value addition in the electronics manufacturing industry. I have seen some videos on the how bare PCBs are manufactured and it looks like there are no barriers to entry, which means there will always be competitive pressure on margins.