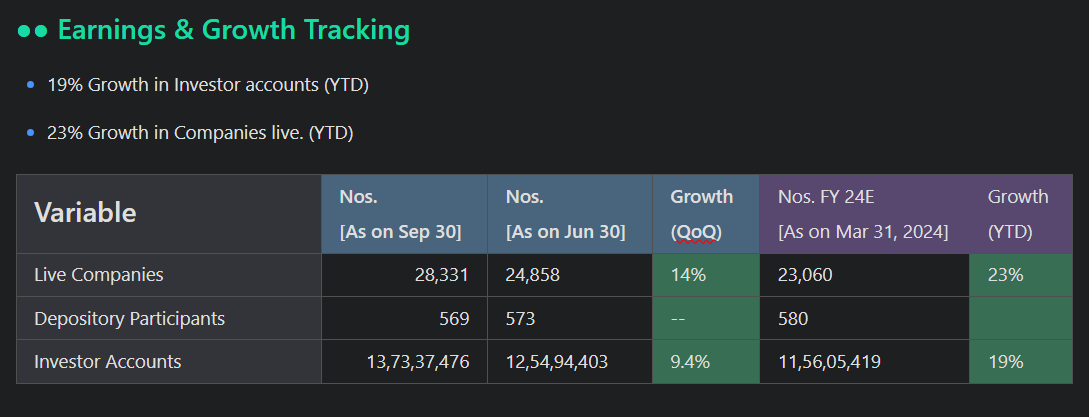

I have put this up in my notes. I will be tracking these growth variables going forward. Thank you!

I have put this up in my notes. I will be tracking these growth variables going forward. Thank you!

They’ve repeated in interviews that they’re tempted to up the guidance looking at the performance in the first 2 quarters, so it’s very likey that the 45% guidance is very conservative.

Hello, I’m new to analysing SME stocks. One query I had, is it possible to find a company with decent management and plans to scale up and then maybe actively track and hold that for several years (lets say 5yrs) that can give good returns like 20x or 30x+. As I have seen cos. with Mcap of 200-300 reach 2000Mcap in 1-2yrs. Or was this just due to the bull run. Penny for your thoughts?

Good to see management going aggressive on new fund launches with 2 NFOs. Multi Sector Rotation Fund (https://www.shriramamc.in/smurf) and Liquid Fund (https://www.shriramamc.in/liquidfund).

A new Fixed Income Fund Manager has recently joined their Investment team. (Shriram AMC Enhances Fixed Income Team with the Appointment of Mr. Sudip More as Fund Manager – APN News)

Another interesting appointment of Head of Wealth Management seen on LinkedIn (Don’t think Wealth Management biz comes under the listed AMC, but gives comfort as Shriram has accelerated the Wealth Management Biz). (Vikas Satija on LinkedIn: I’m happy to share that I’m starting a new position as Head of Wealth… | 255 comments)

One major concerning factor is that their AUM is still not growing at a faster pace. Equity AUM stands at 482cr as of Sep 2024.

As per reports, Accelya is the clear leader in terms of a 50% market share in NDC transactions (Source), and NDC is the future standard that is expected to be adopted by the airline software industry in the next 10 years because it dramatically saves operational costs and time (I don’t have growth numbers to validate this).

A parallel point to consider is that Accelya operates in an industry that has inertia built in its core, which means that its customers i.e. airline companies are loath to fix what’s not broken. Accelya has been operating in this industry for the last 20+ years and counts 200+ airlines as its customers (Source). Most likely, unless these 200+ airlines don’t significantly come across better software, they will most likely not switch to new players.

So in short, there are 2 ways to look at this:

In the best case, Accelya grows because of faster than expected adoption of NDC, increasing its revenue by 10%+ y-o-y. In this case, Accelya is not only a great dividend source, but also a potential source of capital appreciation.

Disclosure: Invested

Hi all, i have recently studied the above book related to SME stocks. It pictures the entire SME details starting from its inception (from 2012) to till july 2024. The author put his utmost effort to consolidate the complete details and its present status.

The author segregates the topic in five parts as

According to me, the clear separation itself shows how keenly he is watching the sme segments.

The author points an important metric on how to access an SME stock.

Any person who are keen to invest in SME can refer and get some valuable insights about the SME segment.

This book is available on amazon also

Hi, adding my two cents. They want to take exports business to 65% which necessarily doesn’t mean that India business is to be compromised.

Yes, promotor has alluded to the fact that in India, projects/ investments do get delayed post announcement but one can’t deny the fact, that business mix change doesn’t mean that India business isn’t a priority. New geographies are only inc the TAM for them. If India starts focusing then who knows there might be a scenario wherein they might have the possibility of market for their products in India even becoming bigger than the current status. Plus some new product developments would be one of a kind to be pushed into Indian markets.

P.S. This is my personal take and nothing against your view.

Gov beginning to mess with the rules