Thanks for sharing the news.

So how this can impact Tata Invest Corporation in the coming future?

Please throw some light on this

Regards,

dr.vikas

Thanks for sharing the news.

So how this can impact Tata Invest Corporation in the coming future?

Please throw some light on this

Regards,

dr.vikas

Doing what you love is happiness and for me its investing ! What a message Sir !

Sir, I have been doing Asset Allocation & aggressive rebalancing since last 22 months and have been managing 23-24% XIRR consistently. Majorly its ETF & Index Funds rotation (Large, Mid, Small, Nasdaq, IT & Goldbees). Its peaceful , easy to track and let me be honest- keeps me happy.

Now that I have completed 1 bear and 1 bull cycle ( Bull is still on though), I am thinking of leverage in the next bear cycle. Obviously not a huge amount, but thinking of taking OD on FD or other safe instruments whereby interest rate shall be less than 10%. Overall leverage would be 30-40% and own funds would be 70-60%. Ability to hold for 5 years as have regular salaried income.

What would be your advise on the above strategy.

Right issue give pro-rata entitlement to all shareholders holding shares on record date, so per se can not be negative minority shareholder in my view. If price is 4000 and right issue is given at 10 (in same proprtion to holding to every shareholding) the ultimate share pattern remained unchanged. It is like Bonus issue which is issue at nil cost to all shareholder pro-rata.

Further, the minority shareholder who do npt have cash/or find inconveniet to subscribe in right, can sell their entitlement in stock market, which are priced normally at differences of current market price less right issue price adjusted with discount factor. So every shareholder (inclduing minority shareholder) has option to benefit from pro-rata allotment in rights.

Coming to last pointsl about increase in promoter stake, there would some shareolder who did not subscribed to right nor did sale their entitlement. In such case, board is authorised to allocate shares to other member in oversubscription ratio in pro-rata basis. So the increase in shareholding by promoter has not directly resulted as loss to minority shareholder. They may have right from open market (in which case kind of purchase at near market price) or got pro-rata allocation for their higher subscription, at same basis, as other shareholder who over-subscribed. You can ot blame managment for non-action of minority shareholder and increasing capital at lower price, at least, in this case in my view.

Discl: No investment in company. Not SEBI registered advisor. Not recommending any investment action.

SKM Promoter SHIVA KUMAR sold 100000 shares in the open market on 15/09/2023(BSE Disclosoure). Is this the indication for the end of upward curve? This is raising concerns on promoter quality. Any comments?

RBA was trading at discount becuase of this overhang of promoter sellling , may be it will catch up with the like of Devyani , Jubiliant …

Divi’s Laboratories Limited Q1 FY ’24 Earnings Conference Call Aug 19, 2023 – Rephrased Notes:

1) Performance Summary:

a) Consolidated total income of Rs. 1,859 crores for the current quarter as against the income of Rs. 2,343 crores for the corresponding quarter previous year.

b) Exports for the quarter is about 86%. Exports to Europe and US is about 67%. Product

mix for the generics to custom synthesis is 60% and 40% respectively

c) 178 cr neutraceutical revenue (ARR of ~720 Cr as against 630cr last year)

2) On Margins:

a) Gross Margin improvement (from 58% in Q4FY23 to 61% in Q1FY24) due to softening of raw material prices and change in product mix.

b) Guidance of OM reversion to pre-Covid levels (35-40%). Going forward, see an improvement in

terms of margins and a slow growth. Compounds where capacities have been improved, filings have been done, margins should grow when clearance comes for Divis’s customers.

c) Impact of high cost inventory procured during Covid leading to elevated RM cost is now over as most of the materials consumed in Q1.

d) Better equipped (compared to other API manufacturers) to deal with cyclicality of RM prices such as solvents etc as Divis have equipment available, installed to recover, reuse with the right specifications whereas not many 000000companies are equipped to do that.

3) On Growth:

a) Seeing a flattish growth because of the after effects of Covid, where first the anti-infectives grew, then the antibiotics, thereafter the life saving and lifestyle medicines. Divis primarily into the Lifestyle market in the generic space. Indicating that improvements in growth rates for generics is anticipated.

b) Customs Synthesis: Working on several projects, any of them can become a blockbuster like Molnupiravir, can’t indicate with certainty when that’s likely to happen. Peptide building block is a (re)new opportunity (obesity, anti-glycemic compounds with these synthetic liquid-phase peptide

drugs.). Only customer approval (& no regulatory approval) needed for supplying building blocks (smaller molecules, less than 500) for the peptide blocks which go into making APIs. Finds application in anti diabetic and anti obesity medicine. Renewed interest in this segment as mode of application changed from IV to Oral.

c) Enhancing capacity of carotenoid (Neutraceutical) (Unit III at Kakinada) to meet additional demand (currently operating at 90-95% utilization). Contribution expected by Q1-Q2 of FY 25. Most of carotenoid RM is made by Divis themselves. Competition is there, but demand is robust.

d) Contrast Media:

(i) MRI (Gandolinium) Contrast Media – 2bn$ market, 2-3 players. Divis will be ready with their process scale up by end of FY 24. Thereafter 1 more year for filings and commercial. Any meaningful contribution to revenue only expected in Q4 FY25.

(ii) Iodine contrast media: 5 Bn $ market, 4 players including Divis

(iii) Currently in the contrast media space, major market controlled by the innovators. Innovators are connected with the instrument and supplies along with with it and thus control the market. Generic market growing rapidly in Asia and Africa markets. DIvis has generic contrast media product like Iopamidol. Thus opportunities in both generic and Custom Synthesis (innovators) in Contrast Media.

e) Not indicating any growth forecast. Company targetting 2000cr quarterly revenue with zero Covid drug sale to boost confidence in its ability to deliver.

f) Unit-3 greenfield project will initially manufacture starting materials, a few

nutraceutical APIs, advanced intermediates and complex chemistry APIs, thus freeing

up Unit-1 and Unit-2 facilities for new opportunities for custom synthesis and generic

products. Unit 1 and Unit 2 facilities are US FDA inspected.

I have been wondering for a very long time, on where to keep a log of my investing behaviour. I have done so in pocket app, google drive and many other places. Somehow all these have been scattered and difficult to locate at times. So I’m starting this thread, one to keep a track of my portfolio and other to get your feedback on my portfolio,

At the start, I’m a doctor by profession and quite passionate about investing. I’m been in the market since 2006. I have committed almost all mistakes as a market enthusiast, right from option trading, intraday, swing trading to cigarbutt long term investing. I have witnessed two major correction in my portfolio of more than 50-60%, one in 2008 and other in 2020. In 2008, I was doing what that should not be done- watching live, all the doomsday predictions on days of Lehman crisis. I had invested my dad funds and mine. On watching the news anchors prediction, I sold all my positions at 10000 levels of sensex, as those financial experts were predicting that Sensex May even go to 3000-4000 levels. Such was the panic those days and I did panic badly. One good thing was the amount involved was very small as it was start of my professional career. This 2006-2009 period gave me very valuable lesson – euphoria, infra boom, reliance hype, Lehman crisis and prolonged fall in the market unlike the covid fall. Though the fall was significant, I was inclined to do fundamental analysis as I was very much into reading most of WB, Peter lynch, Philip fisher books. With the guidance of these stalwarts, I was constantly looking for fundamentally sound companies and investing in them with the regular cash flows I get from my medical profession. Because of lack of proper direct guidance, I did learn the trick slowly but surely. I always kept part of my money invested in mutual funds as I though that it will serve as an yardstick for my direct equity portfolio.

Now after close to 16 years of investing, and bulk of investments done in the last 5 years, I’m close to being financially independent now.

I will open my portfolio positions and the rationale behind it in the next post

HBL – yes, but I am in good profit so I can hold.

Phantom – industry growing at 40-50%. lets see what happens.

Pulz – Own conviction buy after 2.5 years of observation. Quite illiquid. However, I’ve mentioned the reasons behind the buy on the company thread. Plus it is consumer discretionary sector. very niche – Audio equipment and installation. If they make a mark, it can go places. Plan is to see till it lists on main board while tracking results. Again, lets see what happens.

Note, I may sell anytime without reporting back here. fyi.

Note 2 : May turn ITDC into a basket of 2/3 real estate/infra/epc firms. Still thinking.

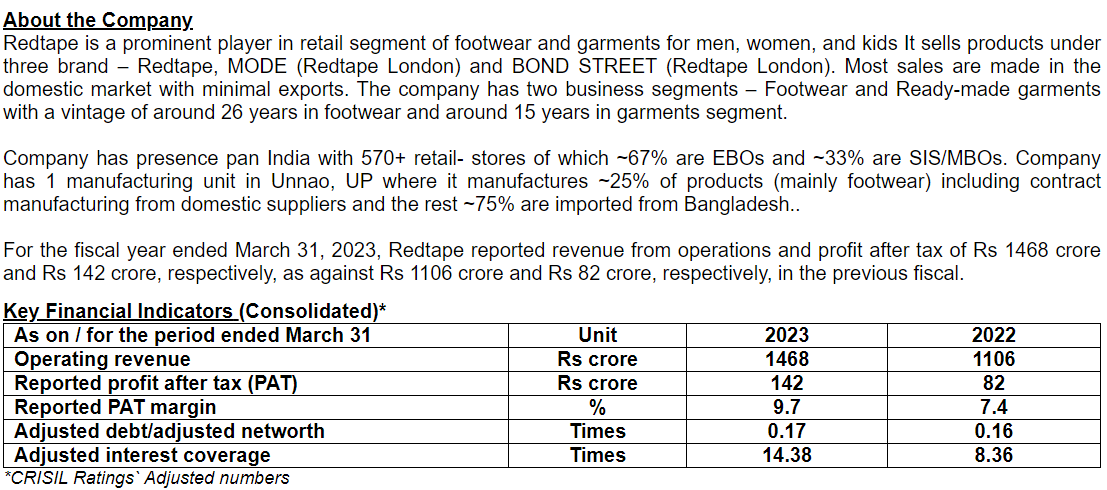

Sharing snip from credit rating Crisil.