What your thesis to hold Redtape even now after the demerger. I think value unlocking is already done post demerger.

Posts in category Value Pickr

The Anti-Portfolio (17-09-2023)

hi vikas …

any specific reason for not having capital goods stocks in your portfolio…

Ami Organics – Pharma Intermediates & Specialty Chemicals (17-09-2023)

In fact, it’s quite the Opposite. Just see some of the management interviews on business channels where the TV anchors are trying to guess ( informed guesses … mind u ) the kind of numbers that these contracts can bring in

The CEO keeps trying not to confirm to their informed guesses. In one of the interviews, Mr Naresh Patel even goes on to the extent and say – ” please let me refrain from spelling out the value of these contracts as I don’t company’s stock to trade at valuations that are astronomical” ( basically words to that effect )

Just my 2 cents

I am invested and biased

Portfolio for next 10-15 years – Starting now (Jan-Feb 2021) (17-09-2023)

hi blue…

very aggressive portfolio…

but don’t you think that high valuations of hbl, phantom and pulz is a concern…

Power grid – a superior alternative to Invits (17-09-2023)

Pointing it out here, that the current 11.3 percent yield might not sustain beyond FY 24.

In their Aug 7 concal, the PGINVIT management did say that maintaining INR 12 per share distribution for the year will not be possible for next year (32:30 PGInvIT).

Disclosure: invested, tracking closely as I invested mainly for the passive income ![]()

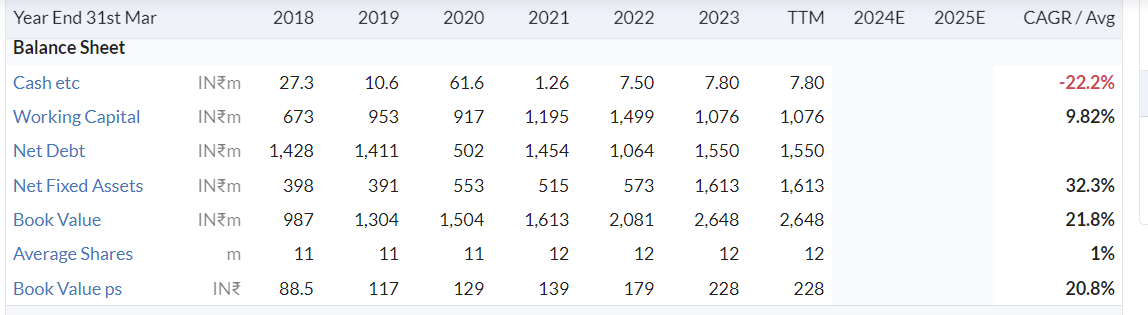

Pondy Oxide & Chemicals (17-09-2023)

Let me try and exhume this company story based on the recent development:

Lets start with the financials:

Last 5 year CAGR growth:

Revenue: 9%

Net Profit 21%

ROCE growing at 31.46%

Balance Sheet:

Present PE: 12.6

Present ROCE and ROE:20.9 and 21.4 respectively

POCL has embarked on a diversification plan with focus on Aluminum (commercial production already started) and Plastics. Significant revenue contribution is expected from these verticals. The diversification and ramp up in these verticals will be a key monitorable

Financial risk profile has been comfortable, with networth of Rs 198 crore and debt of Rs 107 crore, resulting in gearing of under 0.6 time as on March 31, 2022. Financial risk profile should remain healthy supported by stable profitability in fiscal 2023, acquisition of Harsha Exito Engineering Pvt Ltd admitted in National Company Law Tribunal route and the absence of any large, debt-funded capital expenditure (capex)

SWOT Analysis

Strengths

- Established technology with a long history of use

- Reliability and robustness of lead-acid batteries

- Cost-effectiveness compared to alternative battery technologies

Strong business risk profile

POCL enjoys a strong business risk profile, which is supported by its well-entrenched relationships with key customers, diversified procurement and supply base, moderate entry barriers and established manufacturing capabilities. Clientele comprises reputed players such as Amara Raja Batteries Ltd, Sebang Global Battery Company Ltd and Glencore International AG. Relations with these customers span over 10-15 years, ensuring steady inflow of orders.

The company also has a well-diversified supplier and procurement base, with over 270 suppliers and procurement from over 90 countries. The import of lead scrap in India is subject to licensing from the Ministry of Environment and Forest, while setting up of lead recycling plants require permissions from central and state pollution boards, which results in entry barriers for new entrants.

POCL is focusing on aluminum and plastic verticals enabling diversification. It has already started commercial production for aluminum. POCL is expected to garner revenue from aluminum and plastic verticals fiscal 2024 onwards. Also, POCL is also exploring scaling up copper vertical. The diversification and revenue contribution from these verticals will be a key monitorable.

POCL has well-established manufacturing facilities providing it logistical advantage. Its Sriperumbudur plant in Tamil Nadu is close to the Chennai port while its Chittoor plant in Andhra Pradesh is close to the Amara Raja unit. POCL has emerged as a successful bidder for Harsha Exito Engineering Pvt Ltd admitted in National Company Law Tribunal (NCLT). This provides the company with developed asset base for expansion in terms of land bank, factory building and sheds etc.

Weaknesses

- Limited energy density compared to lithium-ion batteries

- Environmental concerns related to lead content and recycling

- Relatively shorter lifespan compared to some alternative battery technologies

Stiff competition from both unorganized and organized players and susceptibility to fluctuations in raw material prices

Risks associated with change in government policies related to tightened environmental norms

Opportunities:

- Growing demand for energy storage solutions

- Increasing adoption of electric vehicles and renewable energy sources

- Government initiatives and policies promoting sustainable energy

Threats

- Competition from alternative battery technologies such as lithium-ion batteries

- Strict environmental regulations and disposal requirements

- Volatility in raw material prices

Huge demand for lead acid batteries due to growth in telecom and datacenter growth (USD 59.6 Billion by the year 2032 with a CAGR of 6.9%, globally).

Demand for rear earth material including Lithium.

Growing importance for circular economy.

OUTLOOK (based on CRISIL)

Liquidity: Adequate

Outlook Stable

POCL will continue to benefit from its established position in the lead metal, lead alloys, and other nonferrous metals businesses along with longstanding relationships with reputed customers

Year 2023 Highlight

The Company successfully established and commenced operations of an Aluminium Recycling/Melting facility at its factory in Sriperumbudur,Tamil Nadu.

In AR the company says: “To achieve our ambitious goal of reaching a Billion dollar top line by 2030, we are exploring various verticals, with some projects in the feasibility stage and others in prefeasibility stage”.

So, the company has set a goal to increase the revenue to ~8000 crore by 2030 from current 1400 crore which is aprox 27%-28% CAGR for next 7 years which is very ambitious, same thing was conformed by the management in the Q1FY23 concall, when customer asked how confident are you to achieve this based on the current growth rate of 6% to 7% for which the company responded saying they are very very confident of achieving this based on the new portfolio additions and demand of circular economy they will ensure the walk the talk!.

Observation:

Looks like the company is poised to take the advantage of power sector growth as most of it’s products such as lead (batteries), aluminum (with 50 to 55% ), copper (EVs, consumer products, solar etc), required by the power sector

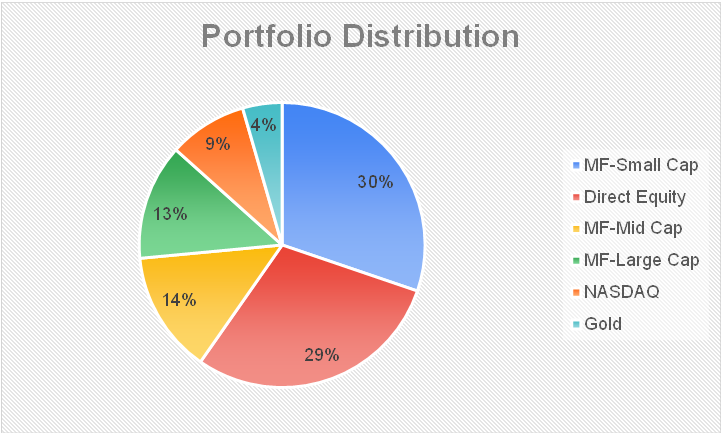

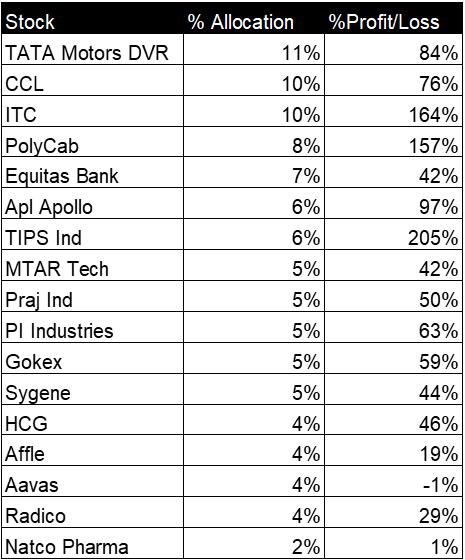

My Portfolio – Alvi (17-09-2023)

Hi all,

I began my investment journey in the midst of the COVID pandemic, with the majority of my current investments made between 2022 and 2023. Like many newcomers, I’ve been fortunate with favourable market conditions.

Currently, my portfolio consists of 30% direct equities and the rest is invested in mutual funds. The value of my direct equity holdings has increased by 60%, leading to an overall portfolio gain of 40%.

Given that I’m still in the early stages of my investment journey and have a significant portion in mutual funds, I’m inclined to take a slightly more aggressive approach with my direct equity investments.

I also have minimal exposure to Rainbow hospitals,Shivalik Bimetal, Lauras Labs, krsnaa diagnostics & Ugro Capital for tracking purposes.

Most of my current stock picks are based on online research and recommendations from channels such as SOIC(Thanks to @Worldlywiseinvestors) . I have liking for companies with MOAT and in niche sectors.My investment choices are still based on the recommendations and research of others, making them essentially “borrowed convictions.” This is the aspect I want to enhance in my investment approach.

My plan is to maintain a portfolio of 15-20 core stocks while allocating less than 1% of my portfolio to another 10 stocks for tracking purposes.

I don’t intend to inject additional capital into direct equities until I get really good with fundamentals and & build strong convictions on my picks; instead, I will continue with my SIPs in Mutual Funds.

Since I’m relatively new to the market, not inclined towards a concentrated portfolio for now. This might change as I learn more with experience.

I’d like to use this platform to document my investment journey, including my reflections and any mistakes I make along the way. I will be updating my investment thesis on each of them soon

Any suggestions or advice are welcome!

Dreamfolks services limited( DFS) (17-09-2023)

Dreamfolks (monopoly bridge between lounges and card issuing banks in India) Q1 updates –

Have signed a new agreement with Plaza premium in Q1 to expand global Lounge coverage. Provides Airport lounge access across 04 continent, operates 340 + lounges @ 70 major Intl airports

Q1 Financial Outcomes –

Sales- 266 vs 160 cr

Gross Profit- 28 vs 25 cr

EBITDA- 18 vs 19 cr ( margins @ 7 vs 12 pc )

PAT- 13 vs 13 cr ( largely flat )

Domestic : International revenue mix- 74:26

Cash on books- 83 cr

Current Mkt share in card based lounge access in India- 95 pc

Number of touch points across the Globe – 1700

Countries covered- 100+

Domestic air passenger traffic in Q1 @ 3.8 cr vs 3.2 cr YoY. India expected to be 3rd largest aviation Mkt by 2024. Current numb of airports @ 140

Dreamfolks foot fall in Q1 @ 26 lakh vs 18 lakh YoY

Number of airports to grow to 220 by 2026

Four major airports expected to come online in near future- Noida, Navi Mumbai, Lucknow, Ayodhya

No of credit cards in India were 2.9 cr in 2017. In Apr 23, this number was 8.5 cr. Expected to surpass 10 cr credit card mark by end 2024

Currently only about 35 pc of Indian credit cards have the facility of Lounge access. Here again, there is scope for growth

Current number of lounges at Indian Airports @ 58 with an area of 4 lakh sq ft. These are facing excessive demand & efforts are on to set up more lounges

Dreamfolks have 100 pc coverage of Railway lounges. Another growth area as railway Infrastructure develops

Company expanding into providing access to Restaurants, Golf Courses, Spas etc by expanding the tie up with banks for high end cards

Sharp drop in margins in Q1 due –

(a) More investments in human capital

(b) Lag in price hikes for lounge operators by Airport operator vs price increases by the Banks. Hence Q1 typically is likely to see this anomaly

(c) One time 3 X hike common areas maint charges by by Airport Operators- unlikely to recur

Points (b) and (c) adversely affected lounge operators in turn putting pressure on company’s margins

Company revising its Gross Margins guidance lower to 11-13 pc band from 14-15 pc

Have given out ESOP benefits to all the company employees to align company-employee goals

Company guiding for 60-65 pc top line growth for FY24

Margins from other services (except lounge-like Golf, Spa’s etc) are likely to be much higher but their base is too small at the moment

Presently, there r 12 railway lounges in India and company has 100 pc coverage with them

With increased Govt spending on Railways, this can also be huge growth area in Future

Have started offering differentiated services to differentiated card holders. Eg – Premium card holder may get preferential luggage transfer, better/more facilities at the lounge etc

My take-

Key monitor able is how the company is able to (or not) maintain its margins from FY 25 onwards (after a sharp fall in FY 24)

If they can do it, it can be a very good business

Basically, one has to keep a sharp look out on margin trajectory and take a call accordingly

Disc: not invested. May invest if company is able to hold onto / improve gross margins

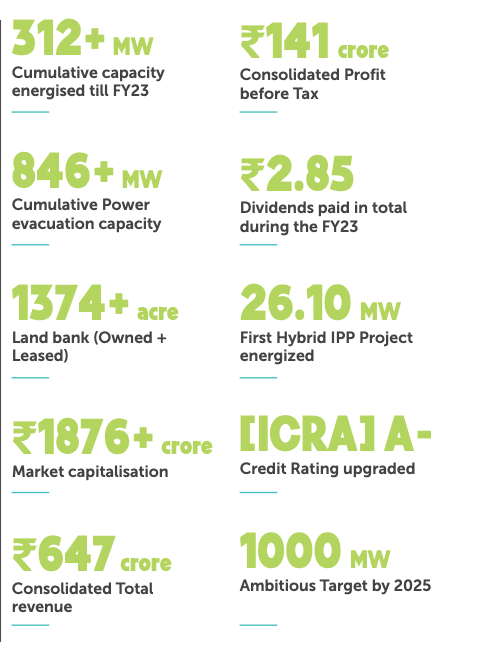

KPI Green- Turning Sunshine Into Cashflows (17-09-2023)

Extracts from Annual Report of the Company for the Financial Year 2022-23

Snippets from AR

Through bilateral Power Purchase Agreements (PPAs), we supply the

electricity produced by our solar power plants to renowned business houses.

Companies reduce their electricity costs through captive solar

plants, whose cost per unit is lessthan that from DISCOM.

Hybrid Model : We have ventured into a hybrid

model of solar and wind energy,

which helps with grid stability.

The hybrid model brings both

solar and wind energy together

to provide a more reliable,

efficient and sustainable

approach to renewable energy

generation. This model also

enables the commercial

optimisation of transmission

charges and the effective

utilisation of grid capacity. We

have added new locations and

increased our capacity from 165

MW to over 300 MW. Our aim is

to enhance this hybrid model in

the future, as it is very beneficial

when it comes to cost efficiency

or effective energy generation.

Technological Insights → Bifacial solar panels

Bifacial solar panels help us generate

electricity from both sides of the

modules by capturing sunlight from

the front and reflected light from

the rear side. They provide us with

higher energy yields, as compared

to the mono-facial panels and we

carefully plan their layout and design

to maximise the benefits

Single axis tracker →

We use single-axis trackers to

optimise the efficiency of solar

panels by maximising their exposure

to sunlight throughout the day. A

single-axis tracker is a device that

allows solar panels to follow the

trajectory of the Sun from the East

to West, as the Sun moves across

the sky. This tracking capability

enables the solar panels to maintain

an optimal angle relative to the sun,

which results in an increase in energy

generation by more than 15%

Linc Ltd: Writing the future of Bharat (17-09-2023)

Plant visit of Analyst / Investor