Posts in category Value Pickr

Simple Investing (16-09-2023)

It was great reading about simple investing pick like Trent.

I would like to share my experience with same viewpoint.

So I started my career in markets around 2017. I am a Bachelors in financial Markets but never really explored about investing or trading. I think either you must have curiosity to explore in topics in the world or your need people around you involved in these kind of topics like Finance.

So as i started working in a broking firm i got to know what shares are how trading works and how investing works. The first company that still excites me is BATA. Bata because my family used to prefer buying leather sandals or footwears in short. So my this memory comes way back when i was in school & college. I always wear sandals from there stores because my mom used to buy that for me.

So I always had this assumption about Bata that they just sell leather footwear & sandals. Things changed when i myself saw BATA giving a fresh look and feel to there stores. The gave a separate section to men’s, women’s & Children’s. I think during 2018 or 2019ish where i saw all these changes. So they moved all old looks to new fresh color & style hiring young actors like Kirti Sanon & Kartik Aryan.

I never invested but learned lesson. With time we all must change or we will be left behind like what happened with Nokia.

My second observation was RADICO KHAITAN. I started drinking from 2017 when i joined corporate world. With time things went pretty bad i recommend “Drinking alcohol is injurious to health and your pocket” because at they end you are destroying your health & paying premium to insurance.

Its been 3 year i am haven’t touched alcohol apart from some 2 to 3 times and didn’t felt good so finally fully left drinking.

Now i want to share what i observed in this journey. When i joined the second broking firm during 2019. There i saw this company RADICO KHAITAN we were recommending this stock at 300 Levels. Not even one guy ask me about the fundamentals. Retailers want trading than investing i can see from where this is coming but when things doesn’t work one must change their strategy. Even i was not sure because i just read the companies business in one pager and checked website but kept eye because someone told me 2 industries Cigarette & Alcohol is always investable at all levels.

So i always had Radico in my mind. So when ever my friends & i used to go to get booze i used to look for brands of Radico. I got to know about Magic Movements then once i saw a bottle of JAISALMER displayed at a big Wine shop. At first i was shocked then i started reading about this company i got to know that the managements is young and they focus on there product and packaging like how there product will feel when there customer open the packaging.

So i never invested in these stock but i want to at good levels. Even the current levels are not bad but i have my own thesis. I need to get out of my mental models.

My reason to write this is to share my experience & how i discovered some companies from just a name in my watchlist.

Investing is simple you just have to observe the changes around you like Vijay Kedia Sir does recently in an interview he shared why he invested in Innovators Façade or Affordable Robotic & Automation. So these is something in underlying which supports the story. Like strong story that things are changing the affordability is changing, peoples preference is changing, people want more variety. Observing small things like this is what most retailers should focus on than running behind options & whipping out the capital

Just just took Vijay Kedia Sir name because i like the way he invests but you can choose your favorite investor or develop your way of investing.

Disc: Not Invested & Biased. Not a buy/sell recommendation. Post only for academic purposes and learning. I can be wrong in all my assessments. Not eligible to give any advice.

Hyderabad Investors Forum (16-09-2023)

Please DM me your number

Yash Pakka – (Previously Yash Paper) – Rising from ash (16-09-2023)

Coversation with “PAKKA” leaders

summary of the main talking points from board/management.

Ved Krishna, Non exdcutive vice chairman:

Focus is to achieve global scale with bagasse (sugarcane residue) and create three solutions.

We created breakthroughs in compostable, flexible packaging substrates and it is time to take the leap of faith to commercialize our offerings. The expansion was necessary given the fact that the Company had already reached around 94 percent capacity utilization during the year.

I must communicate that the cost of manufacturing compostable flexible packaging is slightly higher than the conventional alternative but as we increase capacity and make innovation-driven changes in processes and materials, we expect to become competitive. Besides, if we sell bagasse-based paper today we address realizations of around USD 1000 a tonne but if we manufacture bagasse based flexible packaging, the starting realization pay would be around USD 3000 a tonne. The delta available to us, combined with our installed capacity, should translate into an adequate re-investable surplus that kickstarts growth that is profitable and sustainable.

Jagdeep Hira, Buiseness head paper & pulp:

last year Following increased instrumentation investment, the quality of bagasse pulp improved and is widely recognized as the best in India. In the manufacture of paper, grammage and moisture variations across different batches of the same product declined nearly 80 percent; the result is that there was a sharp reduction in quality issues at the customer’s end from the second half of the last year. For compostable, capacity utilization improved to 52 percent in FY 2022-23 and is expected to improve to more than 65 percent in the current financial year. This business was under preforming last few years, expected to improve in future,

Satish Chamy Velumani, Head of compostable division:

Challenge is the cost of petrochemical based packaging enjoys large economies of scale and will always be cheaper – by a third as a quick estimate – than agro-based packaging. But the overall cost of the compostable packaging, despite being relatively expensive, would still account for a nominal share of the overall meal being ordered.

There are some other positive attributes that we have built: our brand (CHUCK) is national; the brown colour of our cutlery sends out a message of naturalness; the shape of our compostable tableware is proving to be a differentiator in a me-too marketplace.

During the current year, we expect to double revenues once again (a trend we expect to sustain for the next few years, making ours the fastest-growing business within the Company). This growth will be sustained through arrangements with more moulded fibre product converters, an asset-light way of growing our business. We also intend to commission two greenfield plants to service a total addressable Indian market of 2000 tonnes per day.

Neetika Suryawanshi, CFO:

The Company is attractively placed to build around a robust Balance Sheet. At the close of the year under review, the quantum of long-term debt on the Company’s books was negligible, indicating that it was virtually debt-free. The Company’s interest cover was strong, indicating an extensive comfort in meeting lender obligations. On the other hand, we possessed INR 213.48 crores in net worth as on 31st March,2023. We believe that these fundamentals will empower us to borrow affordably and adequately for our capital expansion without stretching the Balance Sheet and without compromising the prospective earnings capacity of the Company.

Disclaimer: Invested and biased

The Anti-Portfolio (16-09-2023)

Click on the “View account value curve” in your zerodha Console dashboard page

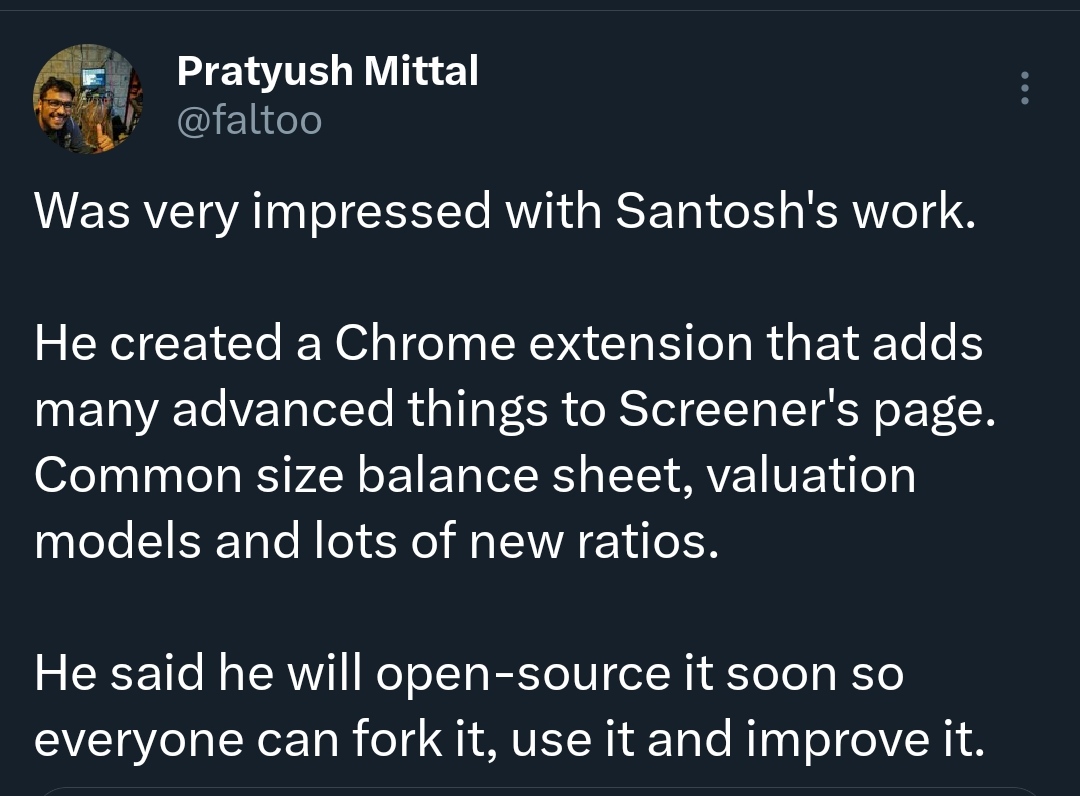

Screener.in: The destination for Intelligent Screening & Reporting in India (16-09-2023)

New Chrome extension by Santosh Badal to get more details from Screener.In

https://twitter.com/Santosh_T_Badal/status/1702766409913434477

Acknowledged by Pratyush Mittal

The Anti-Portfolio (16-09-2023)

How did you download this graph from Zerodha?

Page industries (16-09-2023)

Going commando ![]()

On serious note. You post made me think about my purchase pattern in the last year. I bought clothes 3-4 times but bought only 2 briefs. That too because I was traveling and didn’t have opportunity to wash underwear.

I obviously buy jockeys. I think they last really long. Other than the one instance I mentioned I haven’t bought new underwear in like 2 years.

Bit of faded color won’t matter for underwear, but will matter for regular clothes.

Yash Pakka – (Previously Yash Paper) – Rising from ash (16-09-2023)

Pakka ltd Annual report Highlights

408Cr revenue in FY23,94Cr EBITDA and 51Cr PAT.

76% of the revenue from domestic and rest export.

74% of revenue from paper,13% from pulp and 13% from compostable.

For people who are new to the company, in next 4-5 years Pakka ltd is taking on a huge capacity expansion in Ayodhya and Guatemala location. Turnover potential from Ayodhya after expansion will be 200 USD Million (2026-27) and from Guatemala (2027-28) will be 400 USD million. For a company with annual revenue of 500 USD Million (2022-23), this is quite ambitious ![]() .

.

Company will spend 575cr in Capex at Ayodhya site. Pakka ltd has incoporated a subsidary in USA Pakka inc, this company will raise funding for Guatemala project through equity and Debt. Parent company Equity won’t be diluted for Guatemala capacity. Main purpose of this expansion is to enter compostable packaging solutions (Wrappers/tubes used for FMCG products like chocolate and shampoo). Company will also expand existing business in paper/pulp/compostable.

Given the scale of capital expenditure company plans to spend there is substantial risk involved here. If this capex went wrong, it will strain the company balance sheet for a very long time. Company management has spend a lot of pages in this year annual report explaining the rationale/confidence in this project.

I will summarise the main talking points from board/management in next post.