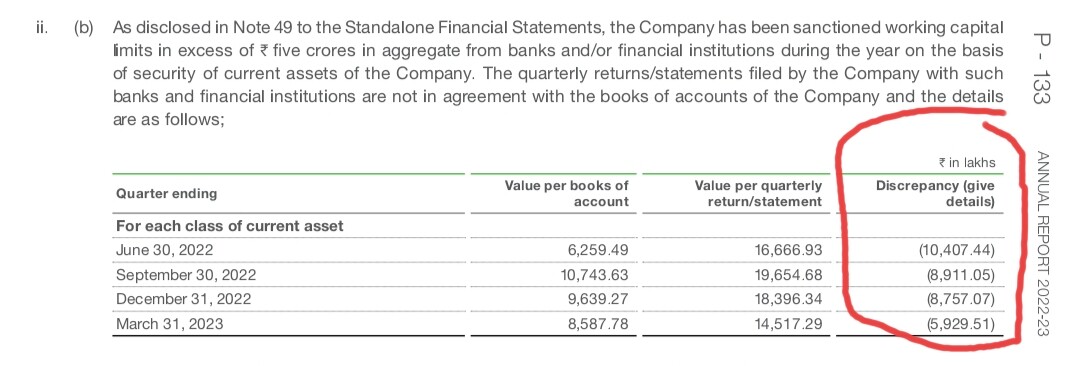

In the AR 2022-23, the statutory auditor remarked that the quarterly returns filed by the company with banks were not in agreement with the books of accounts.

Discrepancies are huge as shown below:-

Is it something serious?

In the AR 2022-23, the statutory auditor remarked that the quarterly returns filed by the company with banks were not in agreement with the books of accounts.

Discrepancies are huge as shown below:-

Is it something serious?

Can anyone solve this mystery ? ![]()

Greatly captured points!

My opinion on the business of Astec and Agrochemical businesses in general-

First and Foremost, all of us would agree on the point that agro-chemical, chemicals in general or even pharma businesses is a complex sector to understand given their thousands of variants, complex value chain, commodity driven supply-demand etc. Owing to these variables it is almost difficult to track these businesses and limited understanding is what drives extremism in this sector.

Case in point – Demand pushed up after Covid-19 and went down drastically after normalcy which led most of the chemicals related businesses to to suffer and so was the case with Astec and even the consistent playes like Atul and Aarti.

In the backdrop of this, one should be extremely cautious while investing in these businesses. It is fair to conclude that these businesses are cyclical and capital intensive. Barring few companies who are into Custom synthesis(PI,Suven,Syngene) most companies are more or less affected by their business cycles and, therefore we as retail investors should take cognizance of this and buy these co.(if one still want to) at significant MOS.

Hi @StageInvesting . I’m new to this forum . I would like to join the ZOOM Webinar.

Kindly include me.

Regards

Sri

Okay thanks we will know more in the next concall.

Thankyou for your notes

Any idea who will be the new promoter of RBA?

Totally understandable, me too find it tough to manage a portfolio and do a 9-5 job.

Thanks for the clarifications and your analysis on promoters holding.

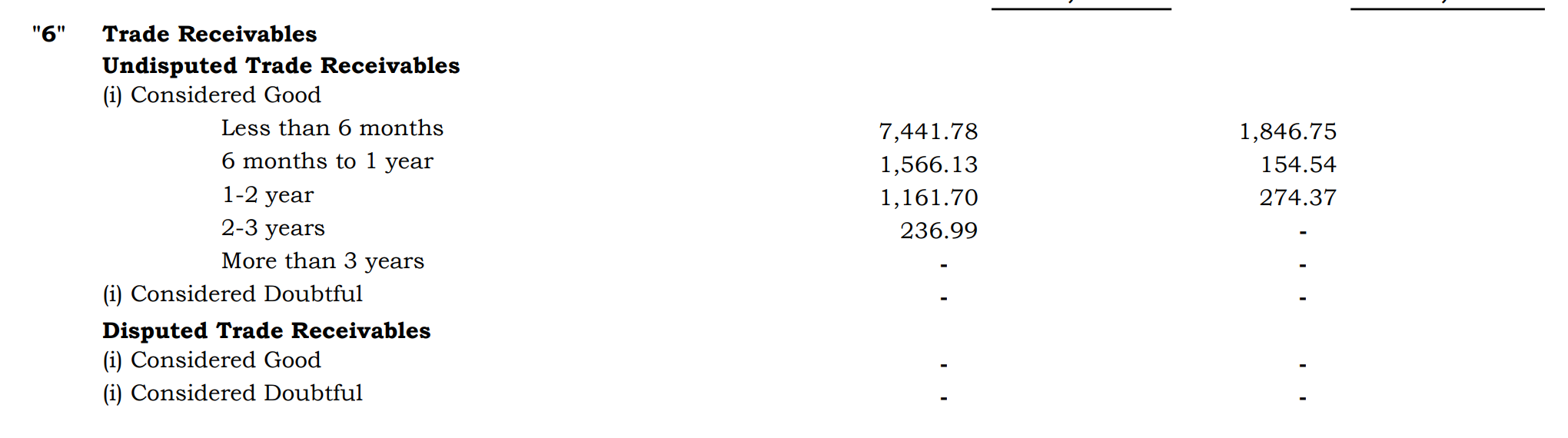

I still think their trade receivable profile isn’t promising.

Previous years trade receivables are getting carried forward.

(1-2 year old 2022 amount is 2.74 cr. 2023’s 2-3 year old amount is 2.37 cr)

(similar flow from 6m-1yr to 1yr-2yr …)

Apart from this, today, over 46,000 families are involved in this self-employment generating activity of

spreading health to everyone and more than 80,000 Authorized Distributors who have a presence in

more than 25 states throughout the country

And yet somehow they have 0 doubtful and 0 receivables written off.

They do MLM (46000 families), if they are selling their products to individuals at credit then they should definitely have doubtful receivables. If not, then they shouldn’t have this high receivables.

The third possibility is that most of their business comes from 80k distributors to whom they sell their products at credit.

And on the other hand, Add shop buys 146cr worth stuff from Dada organics (Pandya sir’s Proprietorship) in 2023. Trade payables stands at 35.6cr, entirely payable to Dada organics (pg 110 AR’23). => 110cr cash generated by Dada organics in AR’23.

PS: I don’t want to sound like a conspiracy theorist but err on the side of caution!

The valuations are attractive but the bet is risky.

Conclusion for me has been to stay away from the company until there is clarity on promoter selling, massive stock purchase by non promoters, new CFO and again a super high receivable which sucks away all the cash from the company and gives it to Dada organics.

I hope things get clear soon.

disc – holds tracking position.

(post deleted by author)

But the government can’t let the industry to die as most of the revenues of the state comes from Casino and casino being a sin industry would grow irrespective of taxation as per last concall commentary there won’t be impact to 80% of casino business as small players would still play and big players whose earnings is from casino would have no other option apart from going to Nepal or macau but in macau,ggr taxation is around 40% which is too high.

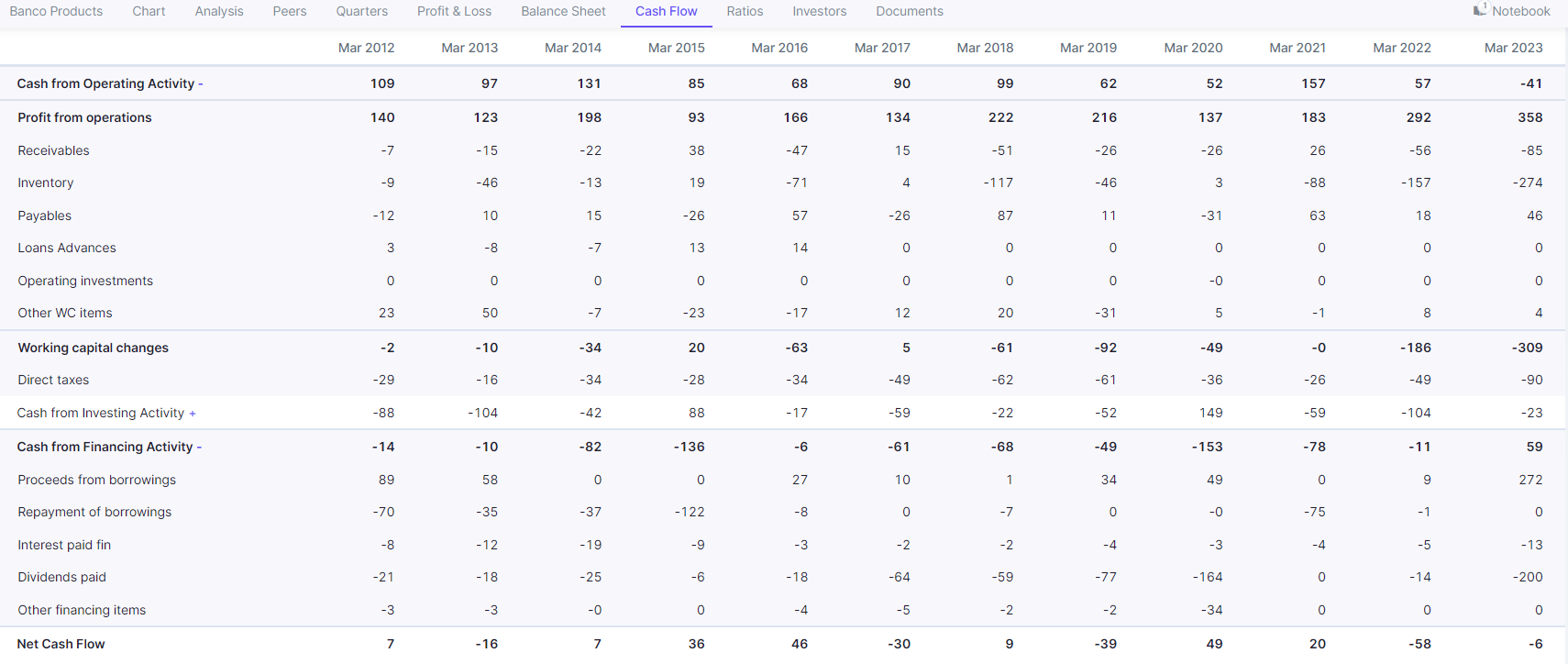

@hitesh2710 ji, thanks for your inputs on Banco earlier. It has given decent run up to around 480 levels now, however i am concerned with the built up in inventory in the firm to the extent that Operating cash flows have turned negative. Also management has borrowed (it seems on the strength of their inventory, since amounts are similar 274, 272Cr) and paid dividends(200Cr) this year. Also valuation wise it seems to be trading at the higher end now (EV 9+) however on the positive sales have grown at a healthy 12%+ for last 5 years and OPMs have also trended higherto 16%. Also FIIs have started buying into the stock. What would you advice for existing investors.