I was trying to collate some play store data about where the incremental interest is going on for online players vs omni channel players. This data cannot be directly correlated with sales, but this can give some indication

I was trying to collate some play store data about where the incremental interest is going on for online players vs omni channel players. This data cannot be directly correlated with sales, but this can give some indication

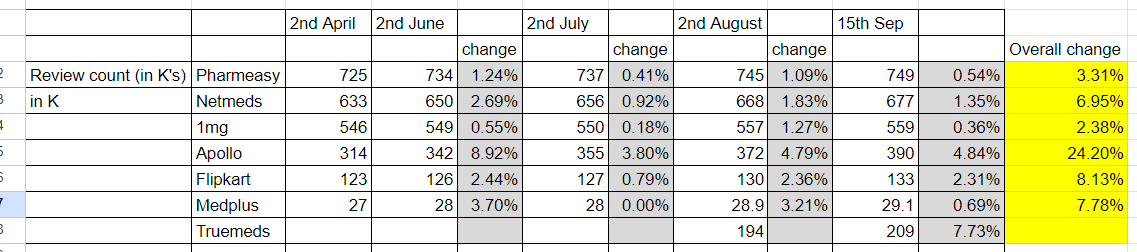

Sharing my AGM notes below:

3. APIs:

R&D/Chemistry skills

Others

Disclaimer:

I guess you are double counting 2 resorts + if you can give me access, i can add couple of things + i have high level FM i can add that also… i expect the earnings to double in 1.5 years time from here given they continue to do b2b business also…

Discl. – invested for tracking postion but will start investing after Q2 result as not much will happen till Q2 results

i did some high level calculation here… They should do 1,000 cr topline in Q2FY24 ie. 30% y-o-y growth…given the TTM PE of16x, i expect the stock to move higher by from these levels…

any thoughts?

i could not find anything on import duty about cr sheets . can you please share the source of the news ??

Nowadays(September-2023) there are news about FII buying into Vikas Ecotech through QIP…but the news articles have limitation…it only talks upto 52 week rather than the whole picture from history.

To me these news articles seem to be just a recycled PR show/ Advertisements, Since the managements doesnt evoke trust.

Disc – Not invested.

After your comments I went and saw screener this company is still up from what it was a month before. So, nothing drastic has happened, do you have any comments on why it went up 20%? If yes, it’s the same reason it has fallen.

It’s just supply and demand as other members have pointed out earlier. Your EPS logic and price doesn’t make any sense. Please provide your legitimate thesis on what the price should be and why do you think it should be, please don’t say EPS, PE and all that’s not how it works. why not that you can find on other threads.

Do you think the company can’t deliver? and why can’t it? Do you have any projections on what EPS could be for coming years and how you came about it? Any comparisons with other companies in the same sector? Are they trading at different multiples than what this company is? What are the reasons? Do you see any major roadblocks to its growth? Tell us the story and numbers of what you think the price should be. Then we can dispute or agree on that.

Why prices are up or down a few percent points (on a monthly basis, yes 17 are few when you look at longer picture) isn’t relevant to this thread.

Disc: Not invested, just following to learn.

You’ve made a valid observation regarding the D/E ratio. In my personal view, the urgency to raise funds likely stems from the D/E ratio. Despite a robust sales growth of approximately 40%, it’s noteworthy that debtor days have decreased. This suggests that there wasn’t an artificial inflation of sales figures leading up to the IPO. Given the impressive capital efficiency with a RoCE exceeding 25%, it’s reasonable to suspect a high D/E ratio, although this is purely speculative without concrete evidence.

In an ideal scenario, the advisor could have recommended securing Private equity funding to reduce the D/E ratio and consider going public after a 5-year period. This approach, in my opinion, could have helped mitigate the general skepticism often associated with SME IPOs.

As for establishing a competitive advantage, it’s likely that this will develop over time. Building a strong distribution network and establishing a recognizable brand presence are key steps in achieving this.

Which is best site to track Chemical and pharma molecule/ commodity/API ingredient prices?

Mr.Raj,

A company correcting 17% at the opening is not something to not talk about?

My previous question received ample replies and they made sense. So i went back to the dawing board with the new information. Few days later, the 17% Correction out of nowhere. You dont think its important to talk about this? One liner or not, how does a company just fall 17% if the valuations are good and acceptable?

Can you explain this Mr.Raj?

Its a Legit question. People can ignore it, but that does not rob it of its legitimacy.

Also, you did not disclose whether you are invested or not. It would help me and others understand whether your views about my questions polluting the thread could be biased. Kindly do so.

I am here to learn and ask, can you provide an answer? You seem like a veteran.

Also, i heard you, read you comment. You can delete it right away. You addressed it to me, so job done. No need to wait 24 hours.