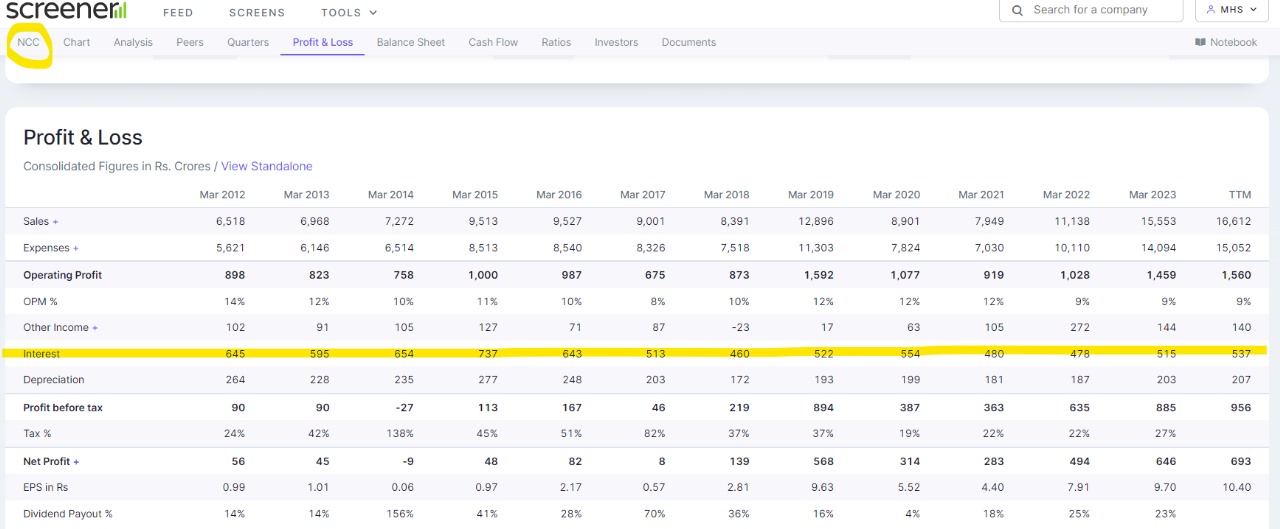

Just glanced NCC numbers : They reduced significant debt over the years, but One thing intriguing and very difficult to understand why is the interest payments almost similar after significant reduction, any idea???

Just glanced NCC numbers : They reduced significant debt over the years, but One thing intriguing and very difficult to understand why is the interest payments almost similar after significant reduction, any idea???

Intel is to pay termination free of 353M$ and then tower is now investing 300M$. ![]() Convenient.

Convenient.

If possible, you can start a series of such investment letters of some Indian Superstar investors like PMS managers, Samit Vartak, Ramdev Agarwal or Marcellus or anyone of your choice. The older the better, to get the idea of Indian markets in Past. If not investment letters then books of some famous Indian investors.

Yup acceptance ratio is 45℅ for me as well

I have researched a lot about this company as far as possible and following things I found since last 2 years

Company currently has in principle approval for 15,000 crore revenue where for

**Bombay dyeing profit margin is expected to be 75% or more.**

For a real estate company major cost is land. In this case Bombay dyeing has land for almost free of cost

Few month back I did some mathematical calculations of probable land value and revenue generation capabilities based ICC tower

I found out Bombay dyeing has probabilities to earn up to 3 lakh crore revenue from their own land parcel in next 10-20 years

Major problems will be land in name of trust so they have to face lot of legal issue before developing those land bank not easy

Wadia has 700 more acre land in th Name of other group companies and various other trust

As far as I know biggest area land holding is in Goregaon East …near arey forest area ( I am not 100% sure )

Go air liability has been pledge by 94 acre land to secure the debt

In future Bombay realty will get demerged for sure

All land parcel in name of various other group and trust will be transferred to Bombay realty

Debt free company from here on

CEO has past work ex and expertise in Realty business so textile will be their just side business

Disclosure: I don’t have any interest in Bombay dyeing but I have been studying Wadia group since last 2 year becoz I like Bombay Burmah

BBTC has 44.5% Stake in Bombay dyeing

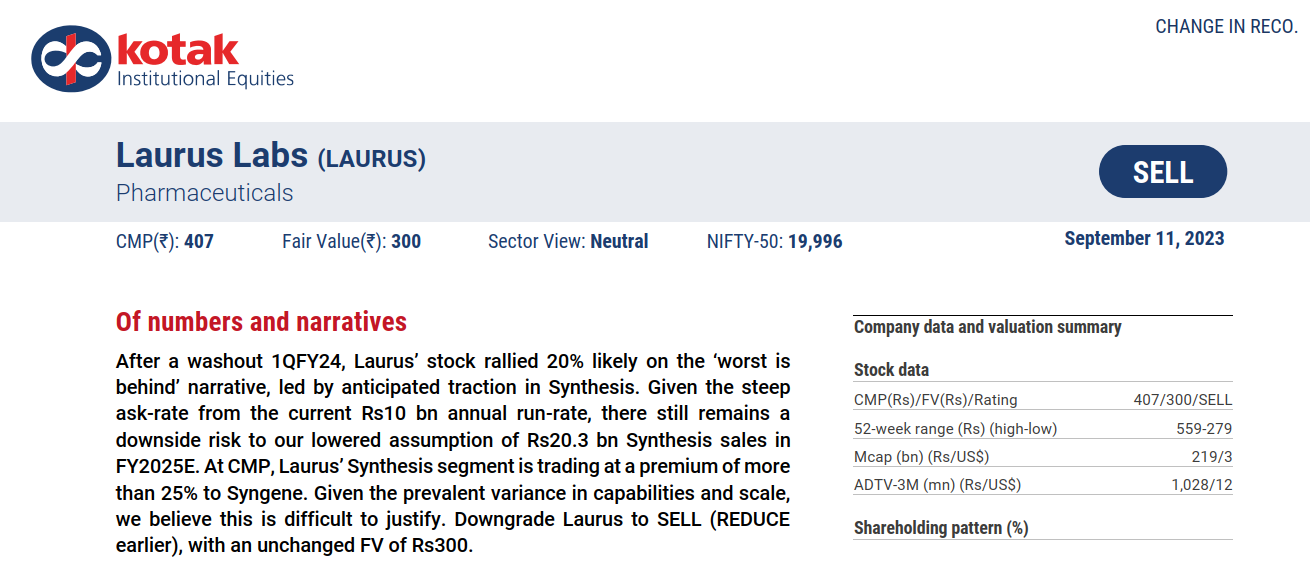

Actually Kotak has a recent similar reco too.

Update: My information is changing and so are my views. The information gained includes:

trying to be value conscious as well now

@Ruchit_Shah – What is Gokek’s value in your opinion?

Imo, this is an early start. The sector is coming from a downturn and the market trying to discount the real numbers is yet to start. Whether is it peak valuations or not, depends upon the investor’s time horizons. There are some triggers that are yet to be achieved such as FTA or even sector consolidation. Peak valuations are often made at peak margins and my understanding says that we are far from froth. Likely, the game is just starting.

West has been diversifying from China. Indian manufacturers haven’t been able to gain anything and the current numbers are not close to the potential. Gokek’s and the Ministry’s are focussed on the same geographies/params. The froth will likely be there once all the triggers are in place.

Disclaimer: I’m invested in Gokaldas Exports. Me & my family members may be invested in other stocks whose names may or may not be mentioned here. This isn’t a BUY/SELL recommendation.

Thanks for the well written post Harshitt.

I just watched their Q1FY24 earning call. I have been running a health tech start-up for 4 years now and very frequently come across various insightful data points and reports from tracxn.

Loved the analogy of tracxn being screener for VC firms (was my first thought too).

IMO one future growth driver for them (not mentioned much elsewhere) could be serious angel investors (individual/groups) who invest directly in startups/ sectors based on their research and insights via platfotms like traxcn (just like what we do today in secondary markets).

I feel we have already come a long way from mainboard stocks to SME stocks and AIF being mainstream for retail investors. Natural extension for this trend would be a way to invest in high quality/ high growth private companies/ start ups.

One more use case couple be to collab with data players of publicly listed companies (brokers, players like screener, moneycontrol, smallcase, etc.) to share some data tgrough APIs for comparing public listed companies with their private counterparts (e.g. Britannia vs Parle or Zomato vs Swiggy).

As their customer are generally crème de la crème and going ahead angels/VCs are going to grow much faster in next decade compared to the previous one. So TAM is only going to expand.

I genuinely feel that current funding winter and dull private market is the best time to research and accumulate such stocks.

YT link for Q1FY24 earning call: https://youtu.be/4AI0MJP8NTY?si=3C7vszLnXd1b13pT

PS: I have just joined VP and this is my first ever post/comment. So please excuse my assumptions/hypothetical scenarios.

Congratulations to Mr Niranjan. What you have reported on 25th July has been proved to be correct. Now it is official that the Company is selling 22 acres of land at Worli for Rs 5200 cr. At long last some concrete steps taken to monetize land assets and create shareholder value.

The stock is bound to be rerated as it has large land holdings in Mumbai, market value of which is hundred times of present market cap. The share has the potential to become another Raymond.

Mr Niranjan is requested to give other plans of the company to monetize land holdings.