I’m interested, Please add me to the list

Posts in category Value Pickr

Sectors with tailwinds (12-09-2023)

India has enacted a 5 year anti-dumping duty targeting specific types of Chinese #steel, as per an official government notice.

Which companies to benefit most ?

Pulz Electronics – proxy to the Indian entertainment sector (12-09-2023)

NSE has made it tougher to migrate to the main board. A few companies which did not meet the criteria were allowed to migrate (I don’t think NSE should have allowed them to) but I believe those remaining small market cap companies like Pulz will stay in SME for the next few years.

I am invested in this company primarily because it seems undervalued at less than 15 PE now and much lower PE earlier, no debt and a good growth rate. The company imports high-end audio components from Europe and assembles audio devices in their factory near Mumbai. Their products seem to have great quality. They export to South-East Asia and other countries, but India is their largest market.

One of the company’s key market is multiplexes. Now with several blockbusters in the charts this year, the demand for quality audio should increase. Pulz has an offering named AmpliX in collaboration with PVR Inox.

A few things I don’t like about the company. The company does not share information about the future such as the plan of action, the projected revenue, etc., except for a few lines in the annual report (AR). I have written to them multiple times to make presentation and/or arrange concalls, but they never respond. Personally, I believe any company that does not do concalls/presentation should not be on the main board. They have very low market share in mass markets such as home theaters although they have a few new offerings listed in the latest AR. By their presence in multiplexes, they have been able to build brand value but strong presence in mass markets is important for scaling up.

Disclosure: Invested from lower levels.

Green Hydrogen as a Fuel – Indian Companies leading the Green Revolution (12-09-2023)

Any PPA logically would contain 3 main clauses apart from other conditions :

(1) the amount of electricity to be supplied per day

(2) negotiated price per unit

(3) penalties for non-compliance.

So it has been grey area until recently. The power producer would tend to quote only for the amount of electricity it could produce in day time because of lack of Energy storage solutions for supplying in the night. Thermal power is always there to the rescue to feed the grid at night time when solar energy not available.

Thus is totally inefficient way of handling Renewable projects of high capital intensive nature as its full potential of power 24×7 is not exploited a

So no wonder all renewable energy projects failed in the past and the industry became sick…Renewable energy sources were initiated way back in 1990’s and companies like NEPC Micon , Suzlon in wind and Tata-BP solar were pioneers.

Now there is clarity in technology for renewable storage solution options namely (1) Electrolyser / Green hydrogen/ Fuel cell (2) Battery storage (3) Pumped hydro storage (4) Compressed air storage . .

And so there is clarity in Govt policy…and now it is mandatory for the power producer to instal energy storage solution ( refer link below) and PPA calls for Total power units to be supplied during day & night apart from negotiated rates and penalty etc

Sona Comstar BLW – Direct EV Play (12-09-2023)

Why promoters are selling their stake?

Seshasayee papers ltd (12-09-2023)

its giving proper valuation…because its not cyclical business

The harsh global folio! (11-09-2023)

I try to find mean reverting variables in terms of valuation, it makes the entire exercise very easy. For mature businesses with stable margins, EV/sales looks through business cycles and is a good metric.

I largely focus on free cashflow generation as a filter for accounting jugglery. By no means its perfect as companies can easily manipulate free cashflow. However, if a company returns a large part of its free cashflow to investors, its highly unlikely that they will be fudging accounts. But it can still happen.

The harsh global folio! (11-09-2023)

As of today, I have added 2 stocks to the portfolio. This reduces cash to 11%.

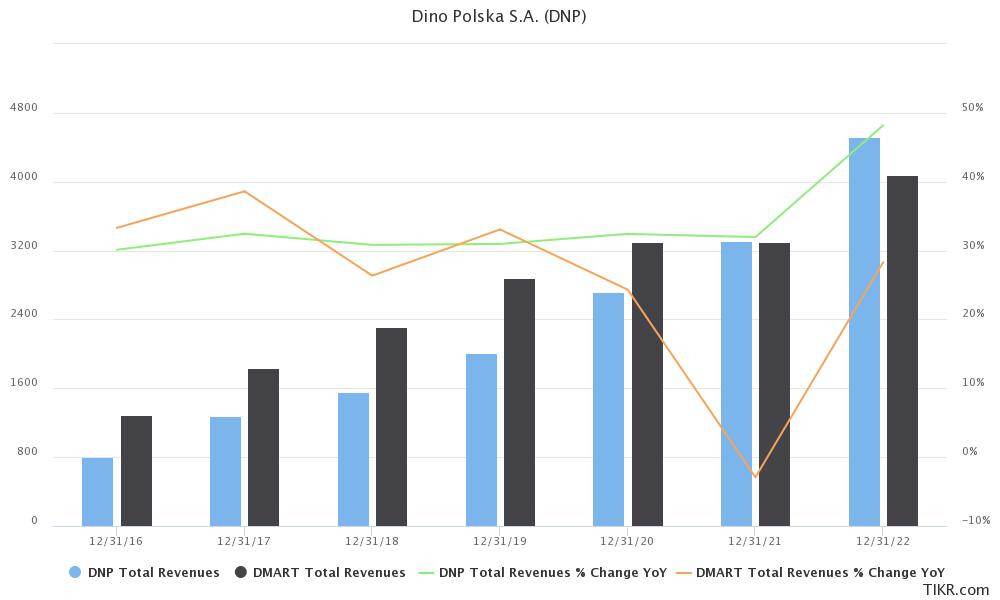

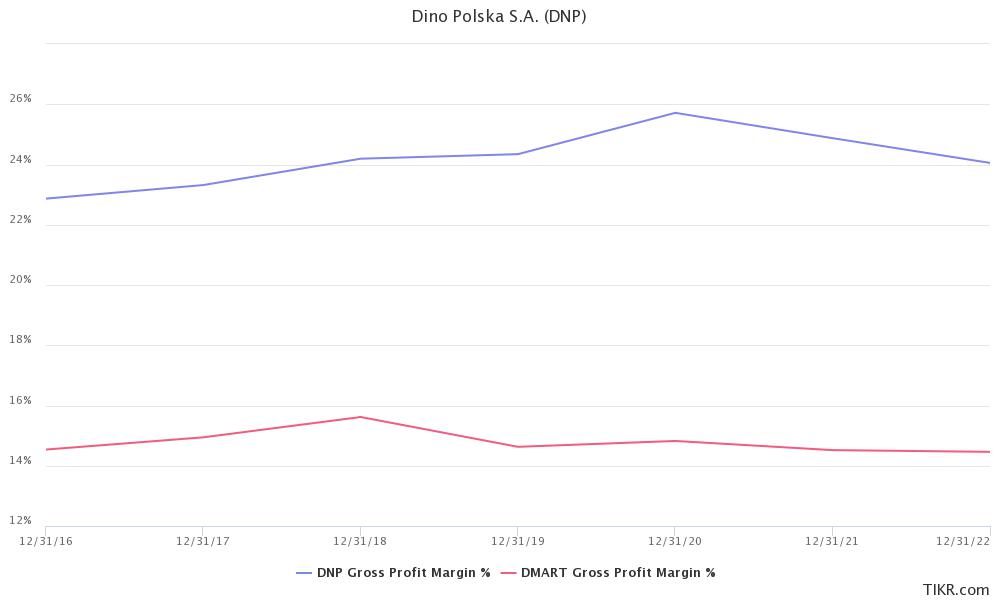

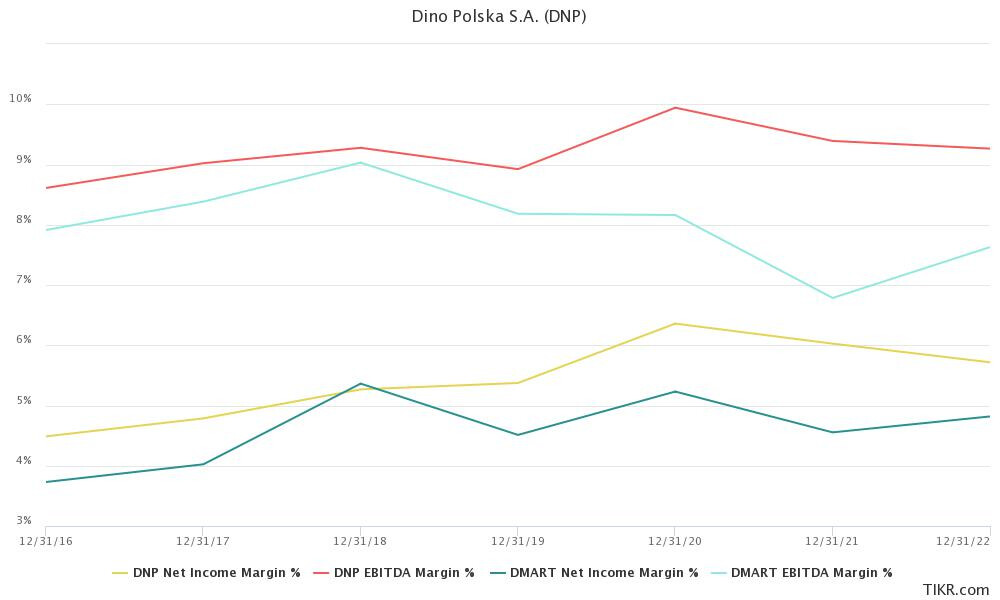

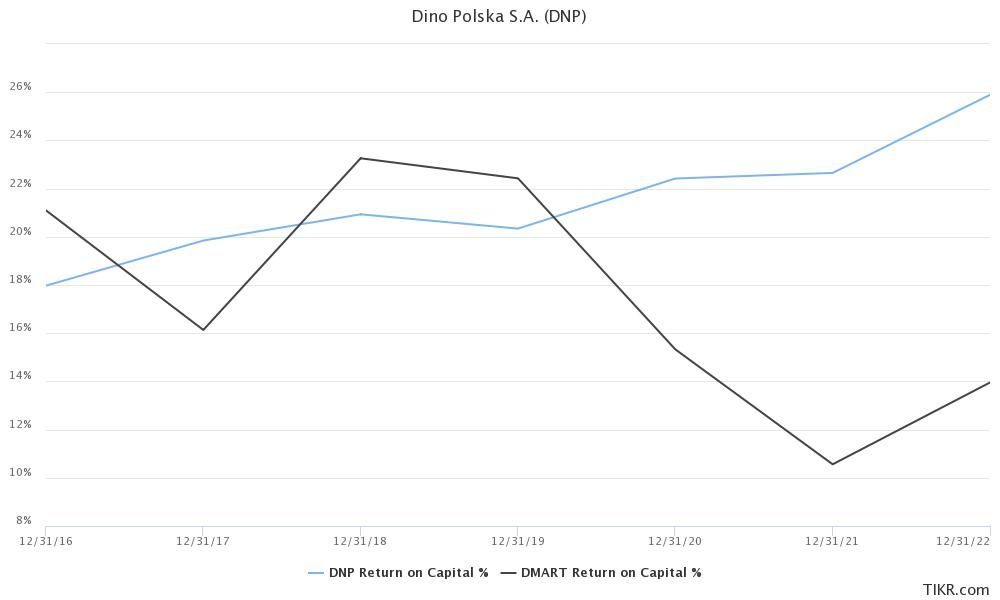

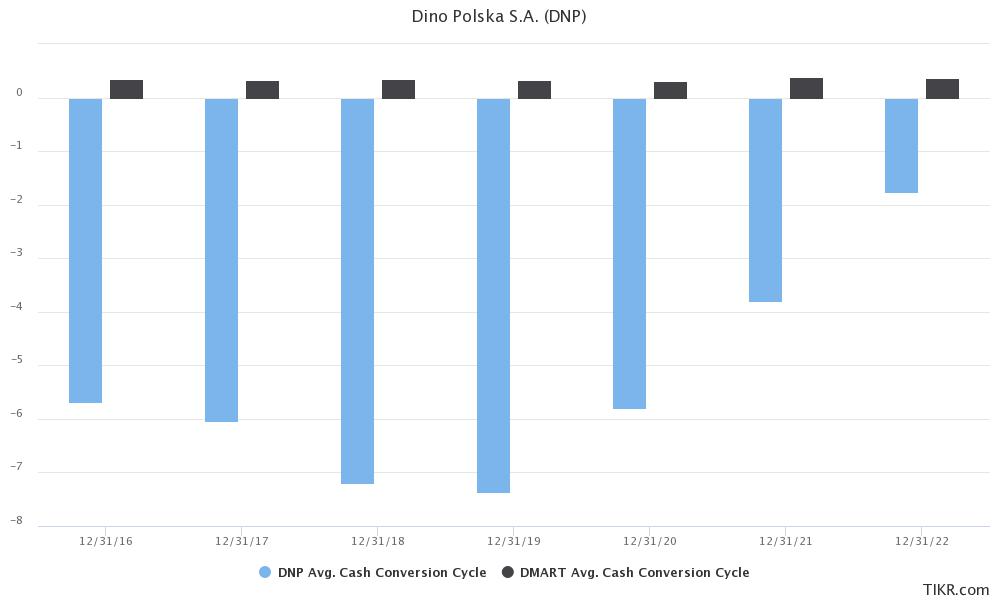

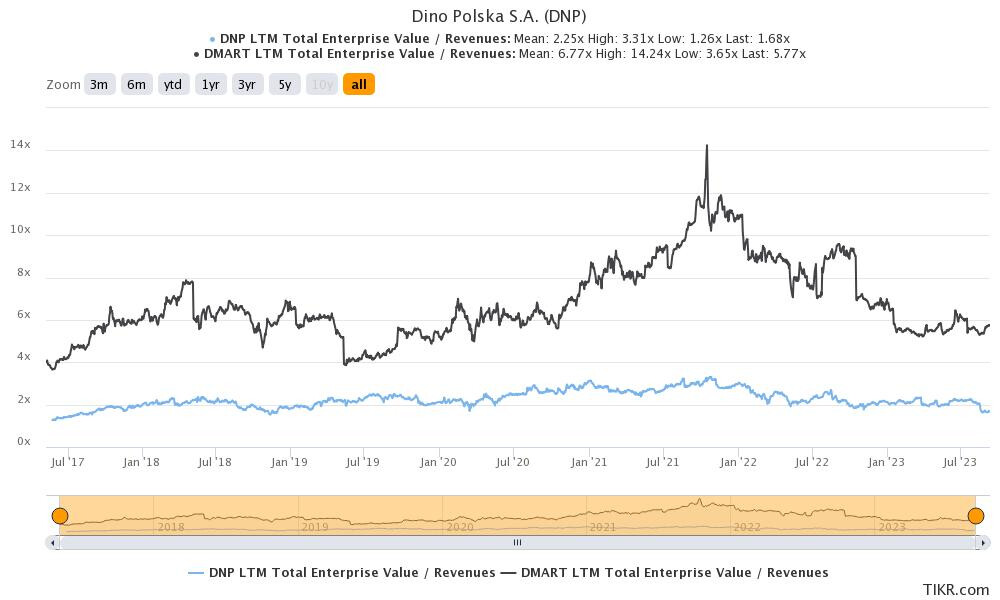

- 5**% position in Dino Polska SA:** The original idea came from our in-house Polish expert @rajanprabu . Dino is a retailer based out of Poland and has done amazingly in past few years. Just to give some context of their scale, I will compare their numbers with Dmart.

Sales growth (since 2016) for Dino has been 33% (vs 21% for Dmart).

Gross margins for Dino has been ~10% higher consistently, which has resulted in higher EBITDA and PAT margins.

All this growth for Dino has come at much higher ROCEs compared to Dmart.

Not only is Dino’s operating model better, even their working capital management is ahead of Dmart (consistently negative working capital).

If Dino was listed in India, I dont know what valuations people might have ascribed as they are superior on every metric vs a Dmart. Actual valuations are half of that of Dmart. So I am getting a superior business model growing faster at less than half the price (thank god for global investing!)

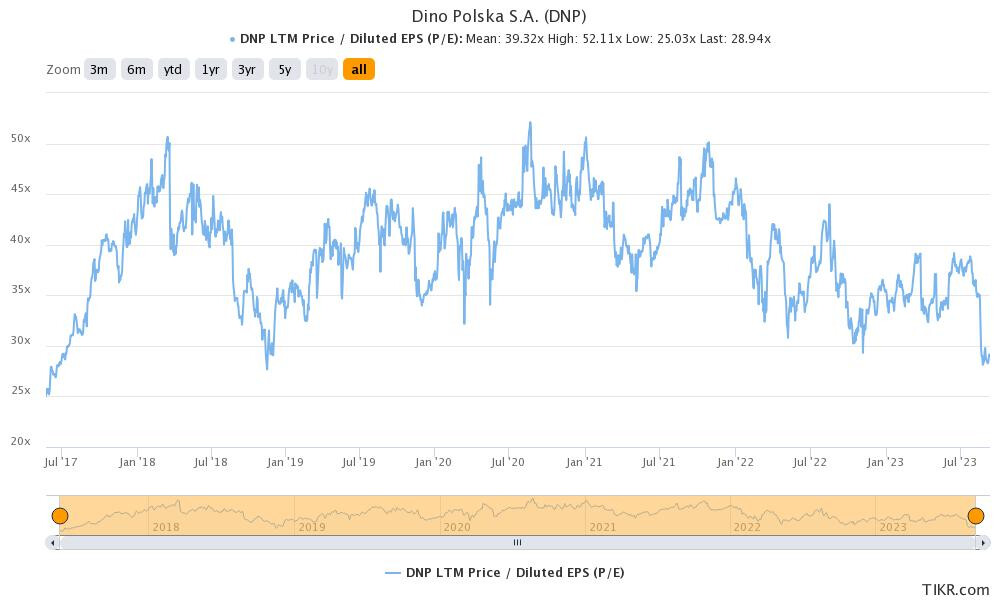

Dino has been consistently been bottoming out at ~25x PE and their current valuation is ~28x, so its towards the lower end of valuations. Lets see how this position works out.

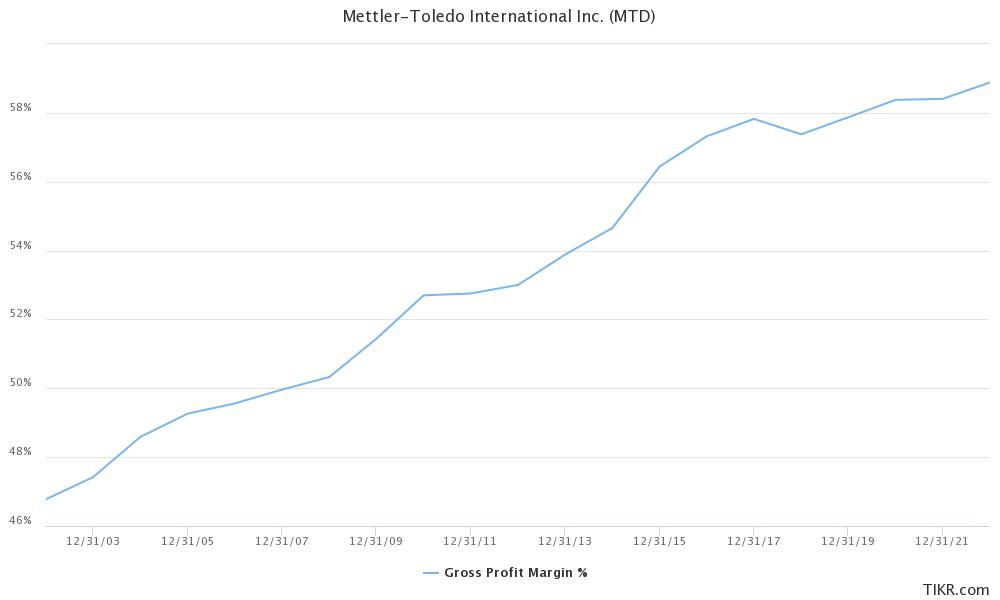

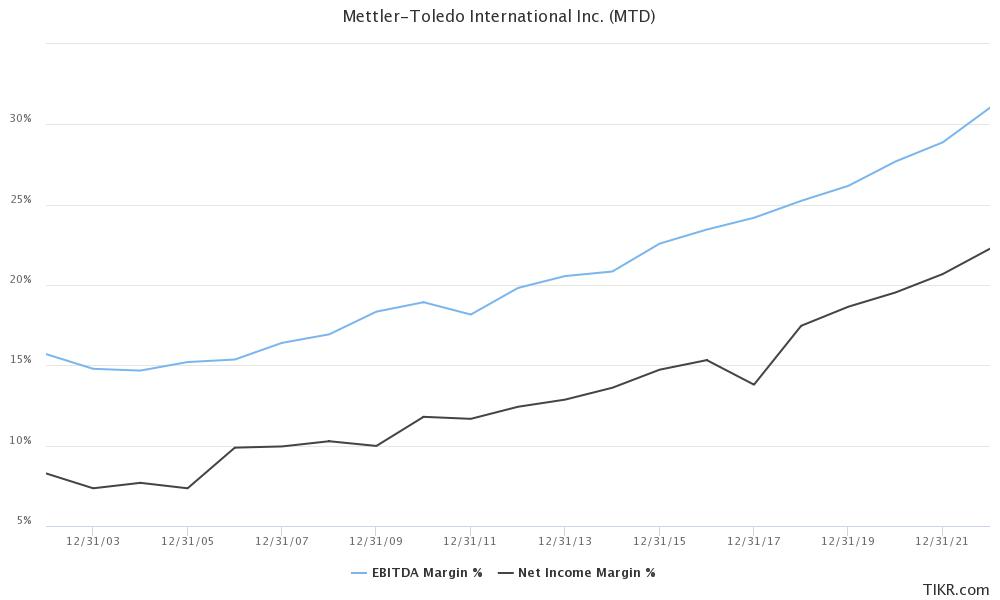

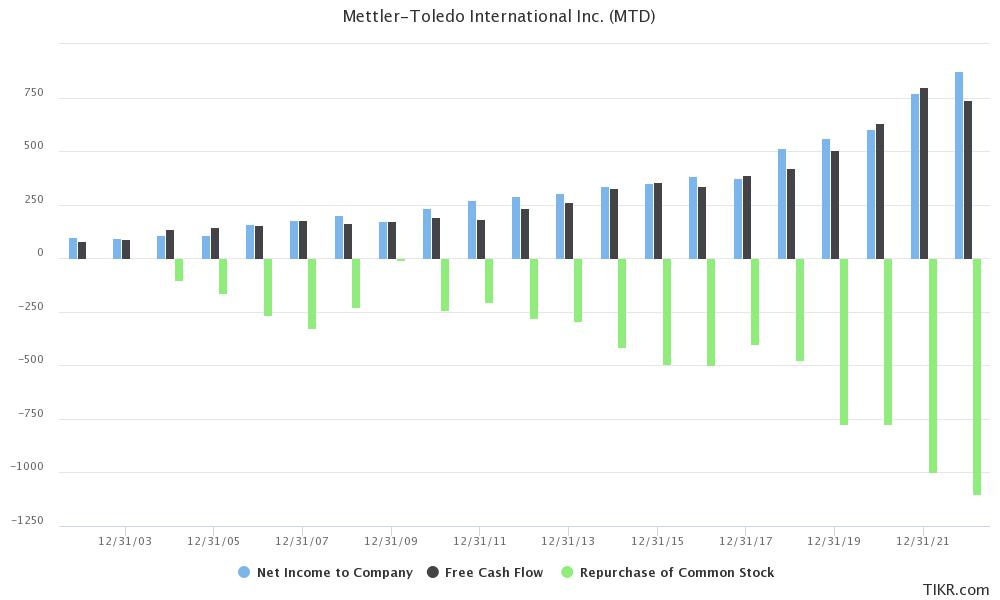

- 2% position in Mettler-Toledo. They manufacture lab instruments and have been industry benchmark for close to a century. I will share few numbers about this business:

Consistently increasing gross margins, leading to improvement in EBITDA and PAT margin over years.

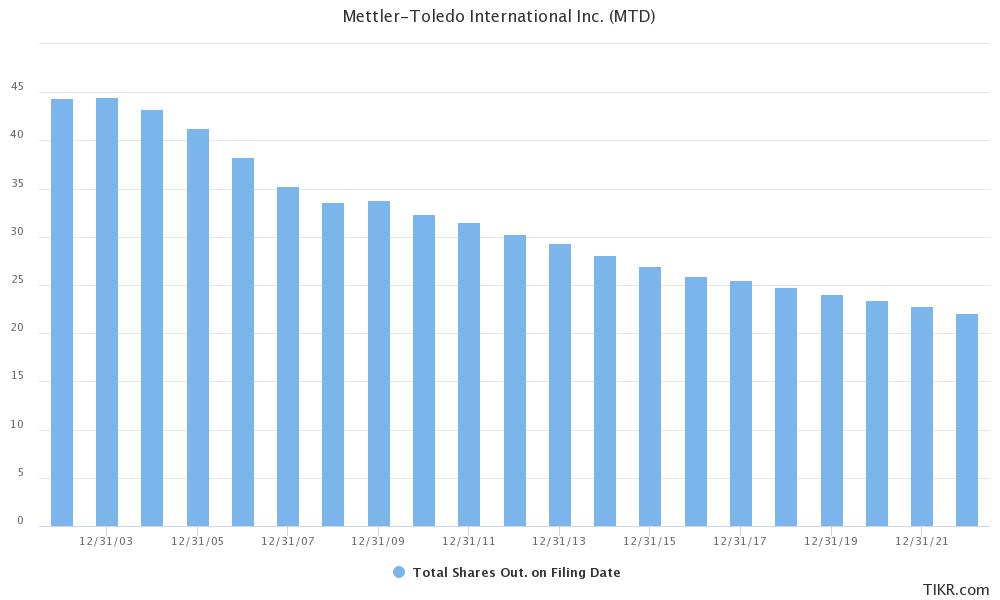

They generate about $800-$1bn in profits and freecashflows, and they use all this to buyback their shares. As a result, their sharecount has kept decreasing over time.

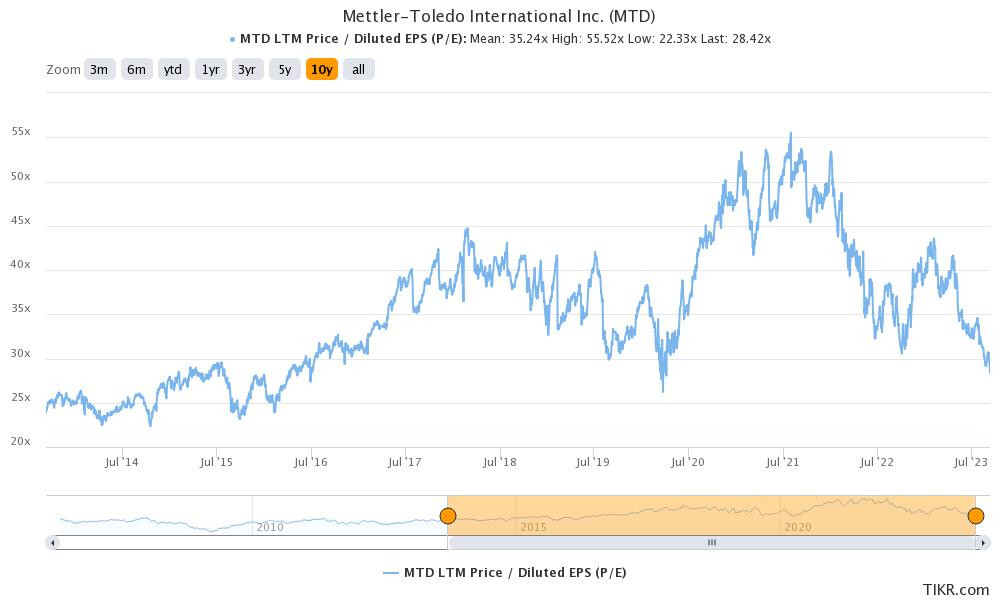

Just to give some context, net profits have grown from $100mn in 2002 to $872mn in 2022 (11% CAGR). But their EPS has grown from 2.21 to 38.41 (15% CAGR) due to consistent buybacks. This is a very high quality and sticky business and they are trading at lower end of their valuation band. This is largely because they saw a large boom in business during COVID which has now normalized and market has derated them. Lets see how this works out.

| Companies | Weightage (cost basis) |

|---|---|

| Berkshire Hathaway | 10.00% |

| Fairfax India Holdings | 10.00% |

| Vanguard Emerging Markets Stock Index Fd | 10.00% |

| AB InBev | 5.00% |

| Disney | 5.00% |

| Markel Corporation | 5.00% |

| UBS ETF CH-SMI | 5.00% |

| Netflix Inc | 5.00% |

| Suzuki Motor | 5.00% |

| Starbucks | 5.00% |

| 5.00% | |

| Dino Polska SA | 5.00% |

| BRITISH AMERICAN TOBACCO | 2.00% |

| Uber Technologies Inc | 2.00% |

| Dropbox Inc | 2.00% |

| Inmode Ltd | 2.00% |

| DWS Group GmbH & Co. KGaA (DWS) | 2.00% |

| VF Corp | 2.00% |

| Mettler-Toledo International Inc | 2.00% |

| Cash | 11.00% |

Natco Pharma: Focusing On Complex Products (11-09-2023)

As per the shared disclosure, number of shares sold are 90,000 i.e. worth ~8.2 Crs, hardly significant keeping in view the market cap of 14k Crs and promoter holding worth ~7k Crs.

Natco Pharma: Focusing On Complex Products (11-09-2023)

As per the shared disclosure, number of shares sold are 90,000 i.e. worth ~8.2 Crs, hardly significant keeping in view the market cap of 14k Crs and promoter holding worth ~7k Crs.