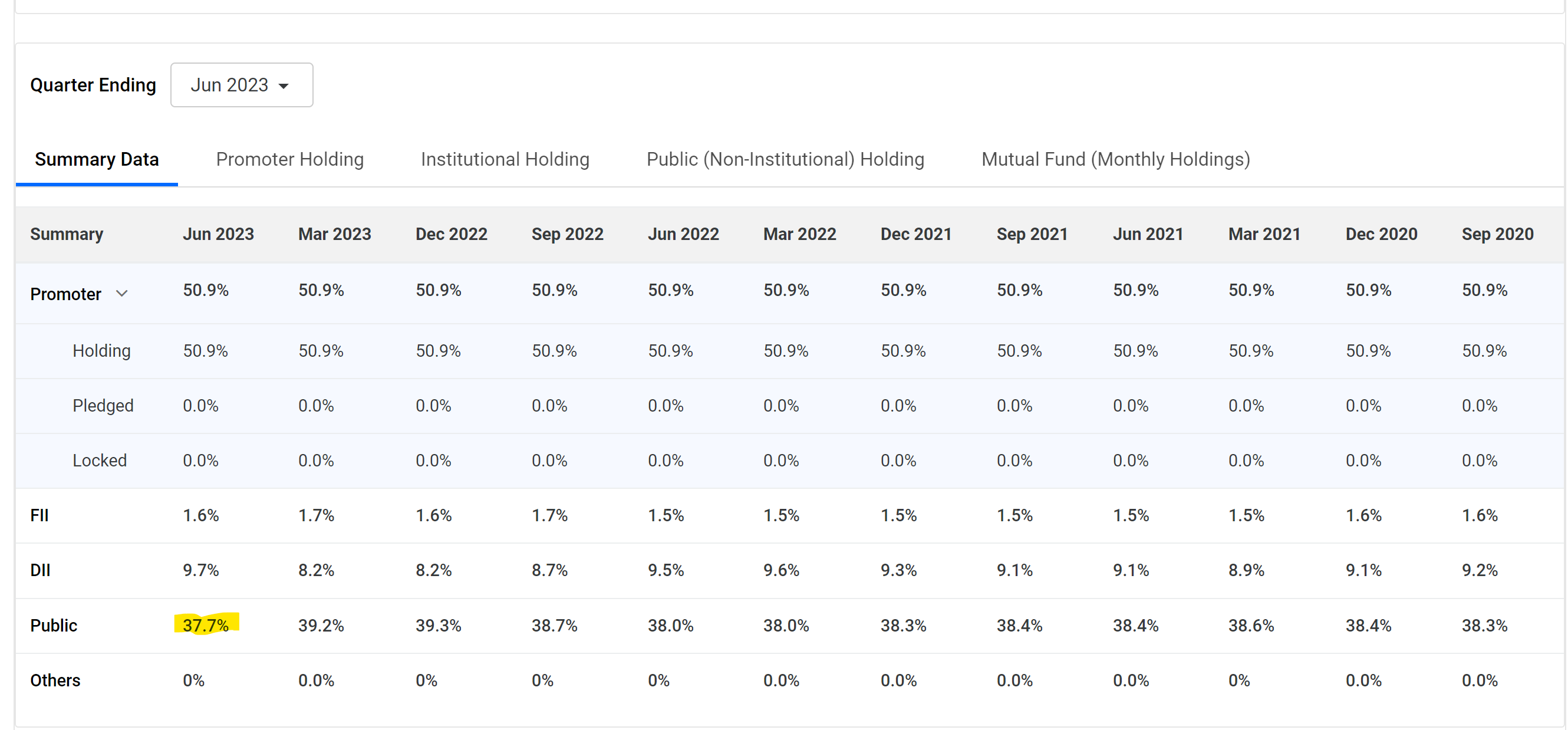

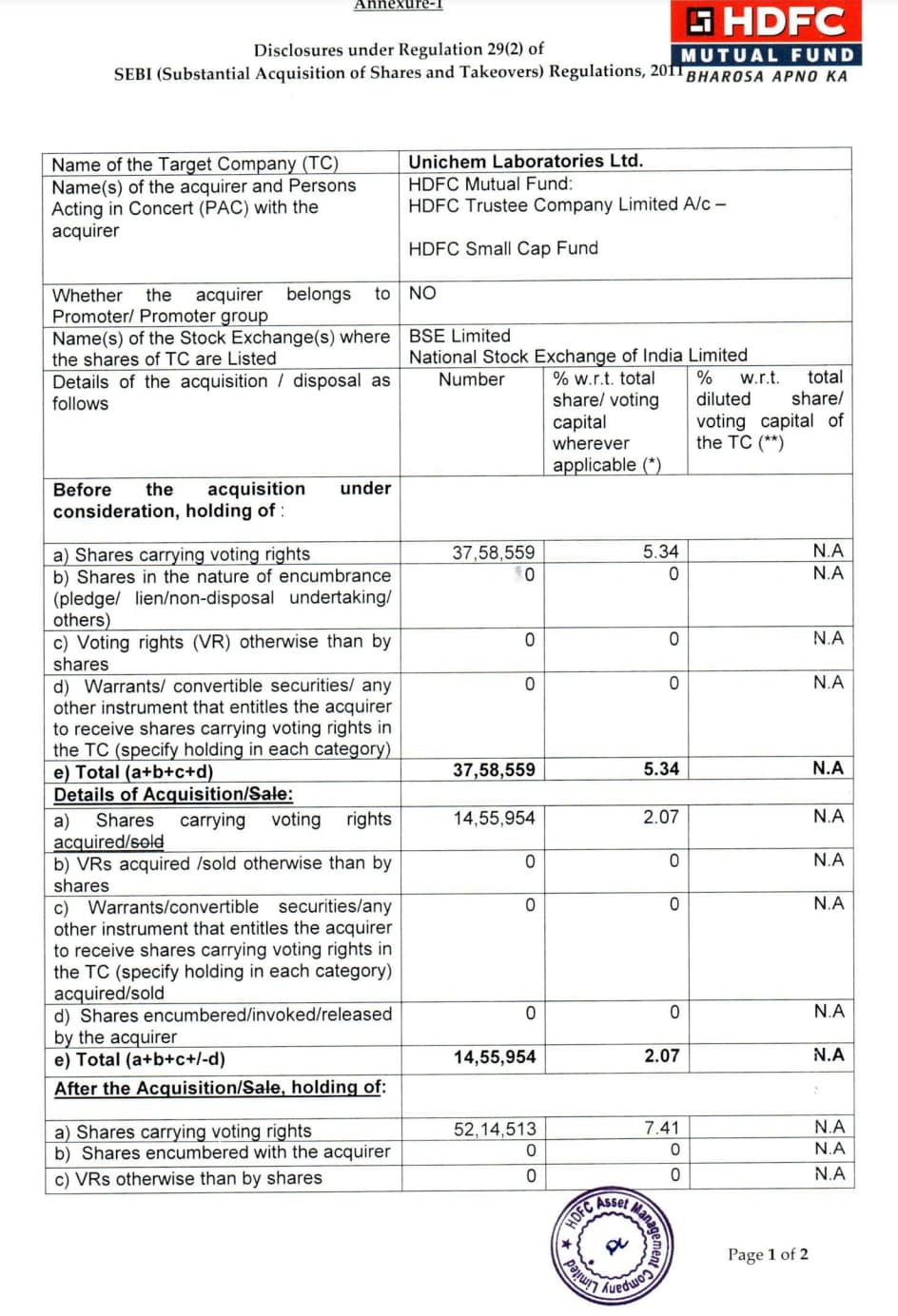

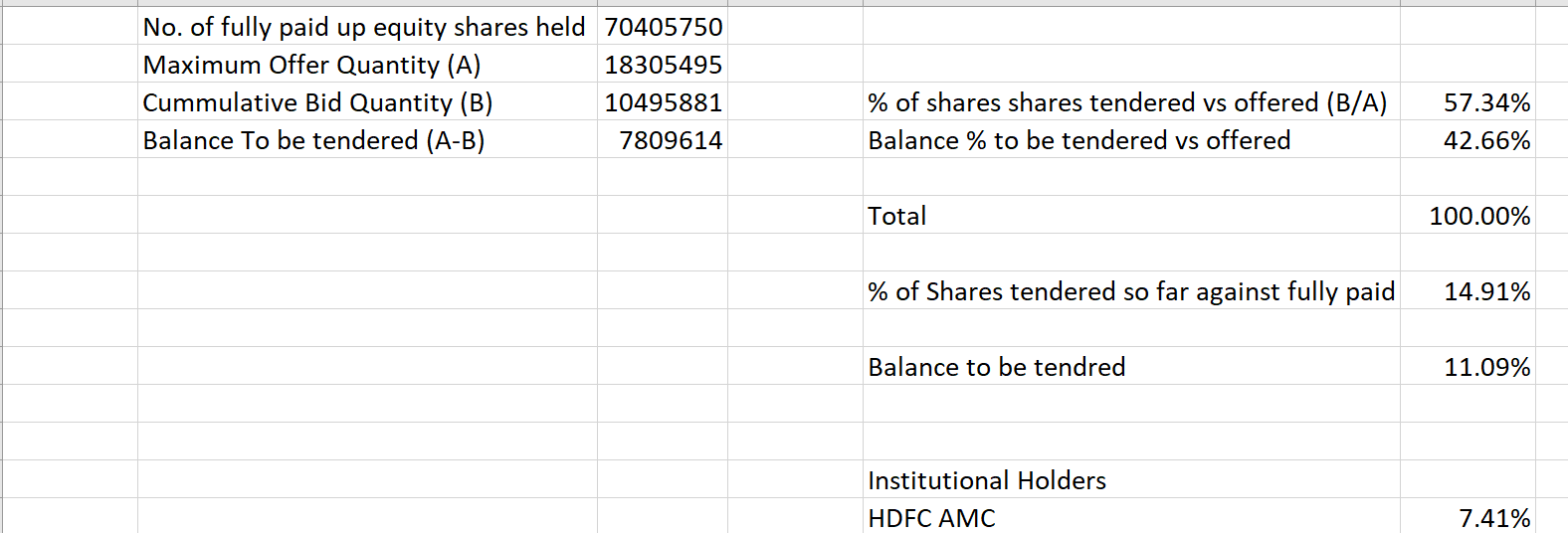

Here is the latest tender details as per BSE Site

Recently HDFC loaded good quanitity

- Pharma cycle is reversing

- Unichem export data appears to be strong

- Tomorrow is the last date to place tenders

Here is the latest tender details as per BSE Site

Recently HDFC loaded good quanitity

My post in Shivalik thread got flagged so trying here.

@dd1474 Since one of the reasons for increasing allocation in Jagran is expecting recovery in Music Discovery & as someone who is invested in both Jagran and Music Broadcast, I want to pick your brains – Don’t you think it would be more prudent investing in MBL. Management has guided about discovery, company is concalls regularly & for Jagran, its has surged almost 50% in a month and there are family disputes as well.

High regards for you sir.

Disclaimer: Invested in both.

Revenues grew by 12% on-year in fiscal 2023 to Rs 566 crore, driven by higher realisations in products like gelatin and di-calcium phosphate (DCP), while volumes continued its modest growth. This, coupled with steady raw material prices led to an all-time high operating profitability of 20.8% for the fiscal as compared to 13.5% in the previous year. This trend continued in the first quarter of fiscal 2024, with the company reporting around 30% operating margins. While margins could soften going forward as the global demand-supply gap eases, supported by improved operating efficiencies, overall profitability is expected to range between 12-14% over the long term. With customers becoming more health conscious, demand prospects for gelatin and other protein-based products is expected to remain comfortable.

The company budgets to incur ~Rs. 200 crore of capital expenditure over fiscals 2024 and 2025, mainly to undertake capacity expansions in its gelatin and peptide unit. While this could be partly debt-funded, the financial risk profile of the company is nevertheless expected to remain comfortable, supported by annual cash accruals expected of over Rs 50 crore.

The ratings continue to reflect the established position of the NGIL group in the gelatin industry, steady support from joint venture (JV) partner, Nitta Gelatin Inc, Japan (NGI), and the strong financial risk profile. These strengths are partially offset by susceptibility to fluctuations in input prices and foreign exchange (forex) rates, and probability of disruption of operations or sub-optimal capacity utilisation due to pollution concerns.

– Source: CRISIL Ratings, September 01, 2023

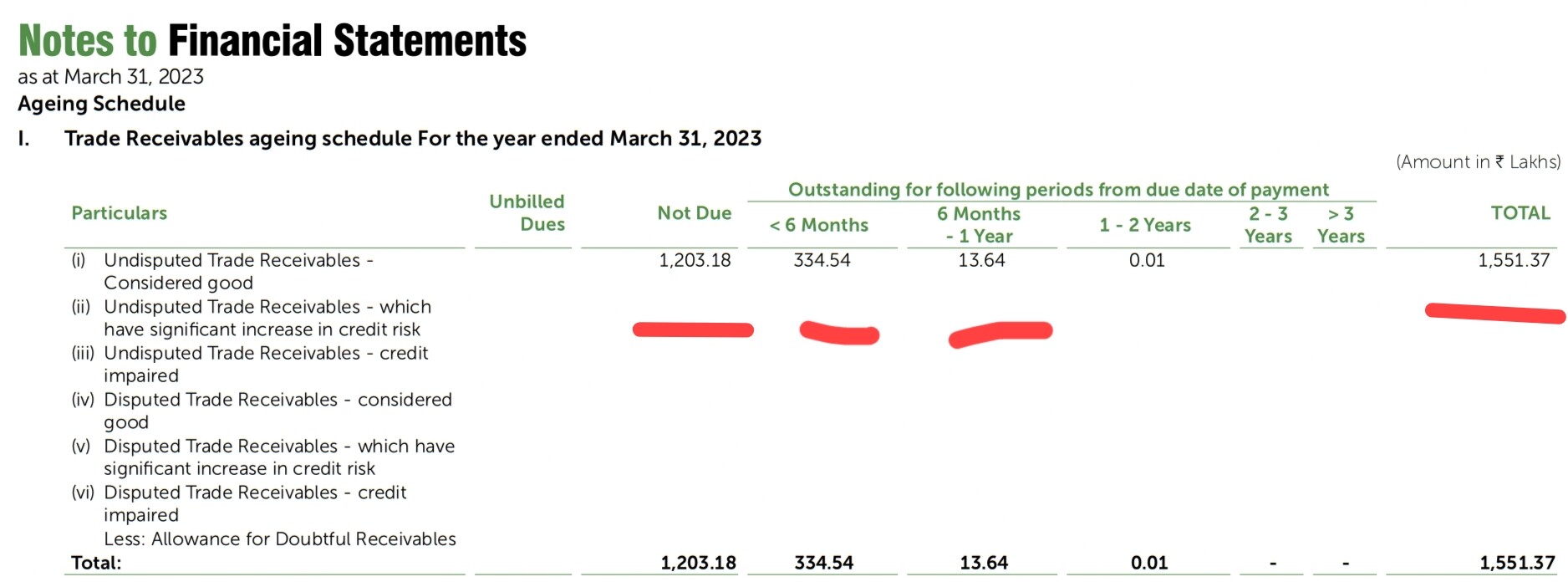

@yrm91 ji – Why are you linking an Investment to Pending receivables… could you share the basis of your assumption that this 17 crore advance amount is an adjustment against the pending Receivables from KJR studios

As per the Annual Report, the total Receivables as on 31st March 23 is only 15.53 crores and this is less than the Investment amount of 17 crores.

The ageing schedule of these Receivables is given below

12 crores is categorised as not due (probably this is less than 45 days old)

3.34 crores is < 6 months old

13.64 lakhs is > 6 months old

0.01 lakh is above 1 year

It’s Receivables above 6 months and above 1 year are just in lakhs…there is no way a company would try to make an adjustment of 17 crores against few lakhs…Even if we consider the total Receivables and assuming all are pending only from KJR Studios (highly unlikely) this is still around 15.5

Second thing is that, in order to make an adjustment the company has to first classify this receivable as a Default. Which they would do only after a certain period say 1 year or above or basis any other adverse event…further they would initiate a Recovery step and any adjustment agreed between these parties, in my view would be requiring BOD meeting and approval …we would have got intimated had this event ever happened

Third, as on 31st March the movie was in production stage… by this time Phantom would have just completed the pre production work and might be in early stages of post production work.

To my knowledge this movies budget is around 100 crores…this includes Remuneration for Director, Hero, Heroines and other Actors and Technicians plus other production costs like Sets, Properties, Costumes etc;…Given that this is a VFX heavy movie we can assume 50% is the VFX budget which is 50 crores… Out of this there is no way that 17 crores is spent only for pre production

Last, the Annual Report clearly states that this is an “Advance for Distribution Rights”…Given that this is a custom line item where in you can write any meaningful text, they would have mentioned it clearly as “Receivables Adjusted towards Distribution Rights” and not as Advance amount

As I mentioned before this is a situation which Phantom came across and grabbed it as they saw this as an opportunity to get Rights at low cost …a good deal and nothing more than that

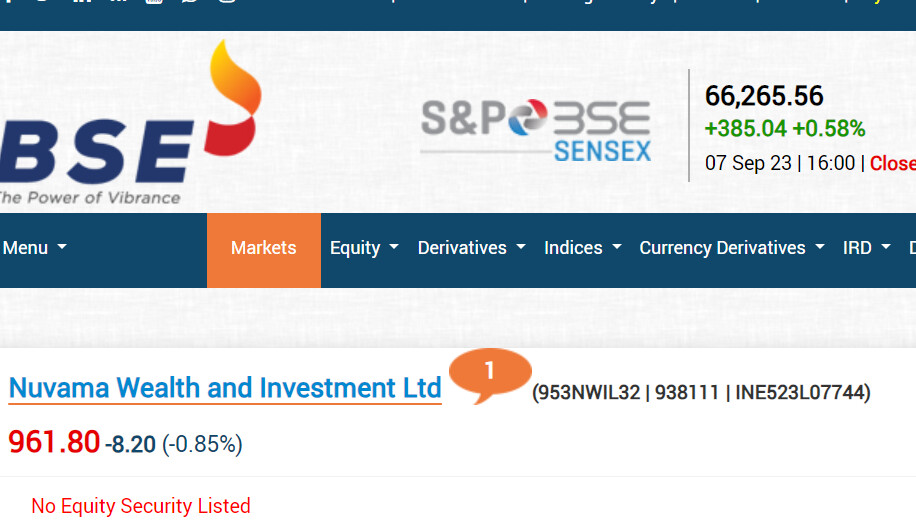

Is the price currently showing on BSE will be the actual price nearly or will be completely different experience people can put their opinions.

When the bull market starts, expect it to last atleast a year. I see no reason to exit small caps so soon. We have probably seen just 1/3rd of the entire up rally. There’s a lot more to go… Also, stocks are not extreme hot. You could still find some small caps that are still value buys.

Disc: my portfolio is 95%smallcap, rest midcap

Hi everyone, as per the latest annual report of Kitex Garments, they are now expecting to commence commercial production from their KMTP Warangal Project which is their first stage expansion only by March 2024. It might or might not be full production level. It seems that the benefits of the first stage of expansion will reflect only in the full year results of the year from April 2024 to March 2025. I am quoting from their latest annual report below.

Blockquote

The first Project at KMTP Waranga is well advanced with the Land fully procured, Buildings getting near completion and types of machinery have started arriving with major LCs opened for procurement of machines. The Company has already contributed a major portion of Promoters Equity. Commercial production is expected to commence in March 2024.

Blockquote

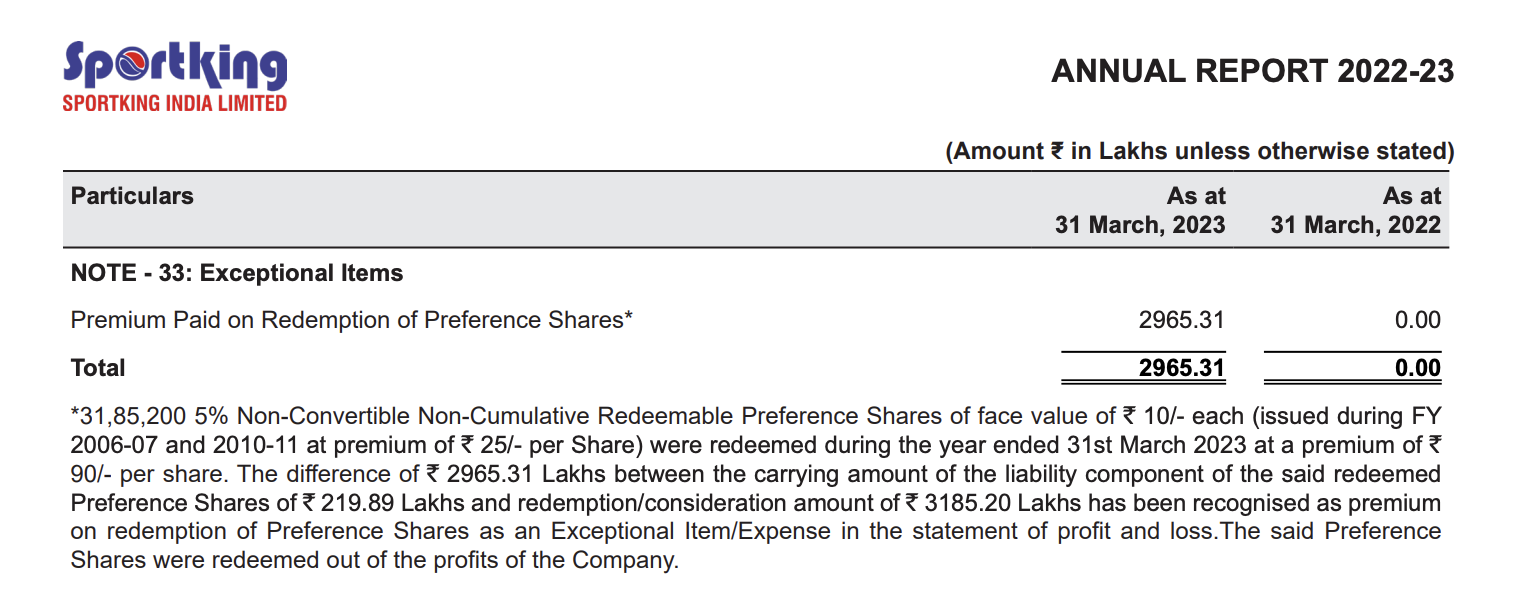

What does Premium Paid on Redemption of Preference Shares mean? Additionally, it says in the footnotes that 5% is Non-convertible Non-cumulative ( What does 5% mean here ? Is it 5% of total preference share). : Source → Annual Report of Sportking (Page : 121)

If a Preference share is redeemed why is preference equity remain the same (page 108)

For example what is stopping a company (in terms of legality) from issuing a truckload of esops?

Promoters had given value of Rs. 160 to TREL. By that parameter it is trading at huge discount. They hold big land bank as shown on their website. The results though not very encouraging the discounting is more in line with real estate companies.

I have recently added to holdings received off demerger. Current investment over 1% of PF.

Its a risky bet, as not much information available on this. This is creating lot of confusion, and they took much more time to list in markets.

No reco. Its a high risk proposition due to lack of information.

I wonder what has happened to money that they got against sale of land bank – it runs into 100s of cr.