I am interested … pls add incognito.2k5@gmail.com

Posts in category Value Pickr

Deepak Fertilizers and Petrochemicals (30-08-2023)

So I see couple of things, now going for the company (Pros):

-

Ammonia prices are going back up (have recent articles price have jumped to near USD 400/ton) which makes things work for the Ammonia Plant. Ammonia downcycle has been playing for a while now and the demand seems to have been picking up. If prices keep rising, there could be a turnaround here in profit margins.

-

An angle still exists to offload a bit of Ammonia in the domestic market to match up some negatives. This was also mentioned in the concall. All other ammonia manufacturers in India are PSUs and consuming it majorly internally.

-

IPA business is expected to perform strong. Fertilizer segment might do good due to the uptick of activity in monsoon season as quoted by Antique Broking. But there are mixed signals here due to some media reports highlighting rainfall deficit.

Cons:

-

Gas prices are going up. The company has dynamic contracts with Brent Index and JKM pricing. If the the uptick is too high then the negative in ammonia might continue. But the management has quoted that they have done some hedging here.

-

If fertiliser subsidy is not adjusted with price rise of ammonia (in case ammonia prices increase), again there could be potential impact like Q1 of FY24.

My thesis why the risk reward is beneficial:

-

Low PE as compared to other chemical companies. I believe the market still values it like it’s peer fertiliser companies which are PSUs. There should be a re-rating story here. Demerger and listing could also be a trigger for this.

-

Company seems innovative in it’s operations so by the time sunset sectors show downward trend, the company should have adjusted it’s product portfolio.

-

If export gates for TAN open which the management mentioned in their commentary government is considering then there is a good opportunity.

Would love to know what others think. I do believe by end of next year (November 2024) the EPS could hit into 130-150 ranges deriving a target price range between 1300-1900.

Disclosure – Deepak Fertiliser and Petrochemicals is a stock in my portfolio.

B C C Fuba India Ltd: PCB Manufacturing Nanocap (30-08-2023)

Thanks @rambaranwal

- I was trying to understand if PCB manufacturing was a completely automated process (i.e. feed the copper clad + design and get the output as assembled pcb) or required human intervention/monitoring at every stage. Another thing was to understand the machinery’s complexity (i.e. is it like a PLC or perhaps way simpler). But I do get your POV and guess there’s no definite answer – and it would depend upon the project complexity

MTAR Technologies – A wager on innovation meeting economies of scale (30-08-2023)

Per AR22-23 pg 39, co expects to fund this through internal accruals and debt. They expect to maintain same debt equity ratio of 0.23

Skipper Ltd., (Power and Water) a moat in making? (30-08-2023)

Have they revelead these details in AR? I couldn’t find.

Garware Technical Fibres (Earlier: Garware Wallropes) (30-08-2023)

The grant will be garnered to areas in technical textiles including agro-textiles, building textiles, geo textiles, home textiles, medical textiles, mobile textiles, packaging textiles, protective textiles and sports textiles.

The startup guidelines (GREAT) is aimed at providing the much needed impetus for the development of technical textiles startup ecosystem in India, especially in niche sub-segments such as bio-degradable and sustainable textiles, high-performance and specialty fibres, smart textiles, among others.

Although this might not help Garware Technical Fibres directly given that it’s not a startup, its great to understand that the government has realized the potential of technical textiles. Such innovation push will surely increase the addressable market size which will ultimately help established companies.

Skipper Ltd., (Power and Water) a moat in making? (30-08-2023)

This is because, interest cost includes capitalised interest, charges for Bank Guarantees/tenders etc.

Genesys International (30-08-2023)

Invested

But below are my observations from SHP

-

GI Engineering is held but the new promoter

Which I believe might be from spin off or de merger sort earlier (assumption) -

GI engineering have sudden bump in income, soon After Malabar entered .

-

G G engineering is another company somewhere linked between all these (could not understand the connection, some shareholders are linked)

—— The Co has tie up with Google and the new Google Map 3D usage will bump up the revenues

Also, searched at BardAI —- infra project , Tata other 2-3 big names are clients .

Do they have some patents , some rights or some niche ???

DHP India Ltd – Regulators and Fittings (30-08-2023)

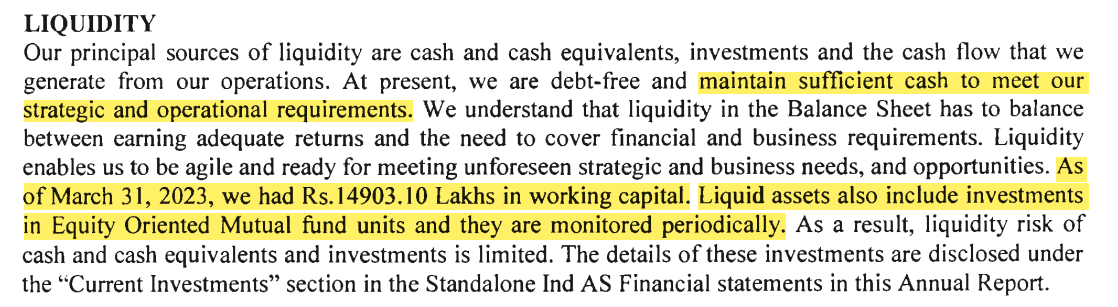

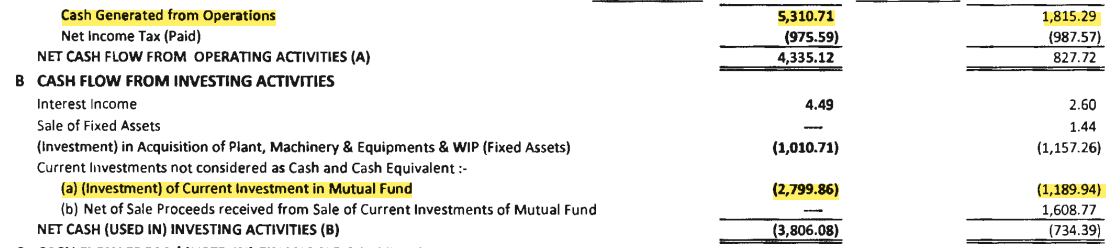

MTM incremental gains for Q2 todate is 11 cr already translating to ~ 140 crores which is 55% of its current market cap and 81% of its equity. Company keeps throwing peanuts to its shareholders each year paying a paltry 1.2 Cr as dividend.

2023 Annual report is no different from its past, without explaining the rationale for exposing so much cash in the business entirely to market risks on which company’s management has no control.

Wonder what kind of strategic and operational requirements are prevailing over last 5 years that forces the company to lock 80% of its equity in mutual funds and not bothering to explain them beyond these few lines.

MDA segment of the annual report is another joke which no one in the company seems bothered to modify over last many years.

Hope the statutory auditors have exercised their full independence in verifying all stated investments and utilization of cash generated from operations, else the minority shareholders can write off their capital as a donation to company management.

No wonder the stock has consistently been derated despite such super strong balance sheet.

Discl: Still holding patiently a large chunk expecting more transparent communications from the company to its minority shareholders.

Sagar Cement – Cyclical Upturn (30-08-2023)

I was holding this from 400 levels pre split and left the bus when it reached 1100 levels. Whole cement sector is a laggard. Valuation of stock looks fair in near term