Some of the previous bets are still there and in almost same weightage. Like Bajaj Finance, Divis , Asian Paints, LTI, Abbott , PI Industries, Nestle, SRF…

Only thing happened is, some like Polycab,Astral, Apl Apollo grew in size while i tried to remove some duplicacy like instead of 3 banks now only 1 bank. And NBFC also instead of 3 just 2…I had posted my portfolio exactly in sept 2022, 1 year is over, and i have tilted towards large and midcap growth companies more instead of only Stalwart . Thats a major change. Also i have decided to do on my own instead of mutual funds while in small cap space, i will go with mutual funds. Also i am.not locking any funds in Nifty and Nifty Next 50 Index funds

Posts in category Value Pickr

Mudit’s Portfolio (Passively Active) (29-08-2023)

Piramal Enterprises Ltd (29-08-2023)

is there chance PEL to sell insurance business to Jio finance as they had strong plans and capital to invest for long term to build insurance business.

Numbers and Narratives: A Simple Discounted Cash Flow (DCF) Model for Equity Valuation (29-08-2023)

For all companies, Valuation is an outcome of Growth, Risk and Opportunity Cost. It might be difficult to determine these components for some firms more than other (Ex: Banks), but the fact remains true nonetheless.

I’ve written down my thoughts on this topic on my blog. I’d recommend giving it a read.

Pravin’s Portfolio (29-08-2023)

Hi Pravin…looks like a very diversified portfolio containing high growth companies…

Pravin this portfolio you have made is for long term or this is a momentum play with these high growth stocks…

This question has come to my mind observing the high PE of almost all your stocks…most of your stocks are trading at PE greater than 40 and few above 50 as well…

How much convinced are you with the expensive valuation of Aditya Vision, Shivalik Bimetal, Apar Industries and RACL Geartech and till what PE you will be comfortable for holding them for long term…

Pix Transmission – low profile smallcap company (29-08-2023)

Can someone share contribution to revenue from Agri,Textile and Industrial segments? @Harsh_Mulchandani

E2E Networks Ltd – Listed small Cloud computing player (29-08-2023)

I have not read the notification but that’s 0.85cr shares or Rs 308.5cr.

Disclosure: Invested

E2E Networks Ltd – Listed small Cloud computing player (29-08-2023)

Hello,

Did the management disclose their GPU/CPU cloud utilization % anywhere?

On the website, it’s showing Claim your spot on the waitlist for NVIDIA H100 GPUs. Join waitlist? Does it mean that they don’t have enough infra with NVIDIA H100 for now. If not, I don’t think they can get H100 anytime soon considering the huge demand pipeline with Nvidia and pricing power($40K)

Ranvir’s Portfolio (29-08-2023)

Landmark cars Q1 concall highlights –

Sales- 694 vs 800 cr

EBITDA- 44 vs 51 cr ( margins constant @ 6.4 pc )

PAT- 7.3 vs 18 cr

Indian auto Industry grew by 10 pc YoY despite a high base

The company’s OEMs – VW, Honda, Mercedes, Renault, MG did not participate in Q1’s growth

Second Qtr onwards, sales may be pickup due –

1.Launch of Mercedes GLC which has received bookings (>1500 cars) amounting to aprox 1200 cr

2.Launch of Honda Elevate which is seeing very good customer response. Honda sales de-grew 37 pc in Q1 due discontinuation of Jazz, WRV

- Start of MG Motors operations in Q2 at Bhopal and Indore

- Have started receiving BYD cars which were stuck up for over 2 months

- Launch of Jeep’s new 4×2 Diesel version

After sales business continues to be strong

Have started a new business of selling pre owned cars

Avg selling price of new cars at 19.5 vs 15.6 LY

Avg cost of servicing/car is also up 9 pc vs LY

Gross margins @ 15 pc (sales + service + sale of pre owned cars)

Aim to hit 100 cr sales from the sale of pre owned cars this yr

Management believes, they can make money here from sale of 1st car onwards as no new infra / manpower is being employed here

In active conversation with MG Motors for allotment of new locations. Awaiting clarity on selection of their Indian partner before going ahead

Jeep India’s management has changed and they have a renewed focus on India. Jeep’s numbers likely to recover to 800-900 units/month and with Jeep’s avg selling price, that’s a good business

Renault going to launch new models in about 16-18 months

Renault providing financial support to Landmark in the interim

VW opening low cost/small outlets in Gujarat through Landmark to drive incremental sales

Once the company is able to crack the pre-owned car sales business in a profitable way, they can easily & quickly scale up

Currently, BYD is allowed to import only 2500 cars / year in CKD format. Even this is a profitable business as the Margins here are high. Company may go ahead with an Indian partner to expand its manufacturing footprint in India

Company is expecting to get advance bookings for 700-800 Elevate car units. That should amount to Aprox 100 cr sales (rough calculation)

Company’s share in various OEM’s India sales –

Mercedes- 16 pc

Honda- 6 pc

Jeep- 26 pc

VW- 10 pc

Renault- 5 pc

New partnerships – BYD, MG, Ashok Leyland

Disc: hold a tracking position

Landmark Cars – Listed premium Car dealership in India (29-08-2023)

Landmark cars Q1 concall highlights –

Sales- 694 vs 800 cr

EBITDA- 44 vs 51 cr ( margins constant @ 6.4 pc )

PAT- 7.3 vs 18 cr

Indian auto Industry grew by 10 pc YoY despite a high base

The company’s OEMs – VW, Honda, Mercedes, Renault, MG did not participate in Q1’s growth

Second Qtr onwards, sales may be pickup due –

1.Launch of Mercedes GLC which has received bookings (>1500 cars) amounting to aprox 1200 cr

2.Launch of Honda Elevate which is seeing very good customer response. Honda sales de-grew 37 pc in Q1 due discontinuation of Jazz, WRV

-

Start of MG Motors operations in Q2 at Bhopal and Indore

-

Have started receiving BYD cars which were stuck up for over 2 months

-

Launch of Jeep’s new 4×2 Diesel version

After sales business continues to be strong

Have started a new business of selling pre owned cars

Avg selling price of new cars at 19.5 vs 15.6 LY

Avg cost of servicing/car is also up 9 pc vs LY

Gross margins @ 15 pc (sales + service + sale of pre owned cars)

Aim to hit 100 cr sales from the sale of pre owned cars this yr

Management believes, they can make money here from sale of 1st car onwards as no new infra / manpower is being employed here

In active conversation with MG Motors for allotment of new locations. Awaiting clarity on selection of their Indian partner before going ahead

Jeep India’s management has changed and they have a renewed focus on India. Jeep’s numbers likely to recover to 800-900 units/month and with Jeep’s avg selling price, that’s a good business

Renault going to launch new models in about 16-18 months

Renault providing financial support to Landmark in the interim

VW opening low cost/small outlets in Gujarat through Landmark to drive incremental sales

Once the company is able to crack the pre-owned car sales business in a profitable way, they can easily & quickly scale up

Currently, BYD is allowed to import only 2500 cars / year in CKD format. Even this is a profitable business as the Margins here are high. Company may go ahead with an Indian partner to expand its manufacturing footprint in India

Company is expecting to get advance bookings for 700-800 Elevate car units. That should amount to Aprox 100 cr sales (rough calculation)

Company’s share in various OEM’s India sales –

Mercedes- 16 pc

Honda- 6 pc

Jeep- 26 pc

VW- 10 pc

Renault- 5 pc

New partnerships – BYD, MG, Ashok Leyland

Disc: hold a tracking position

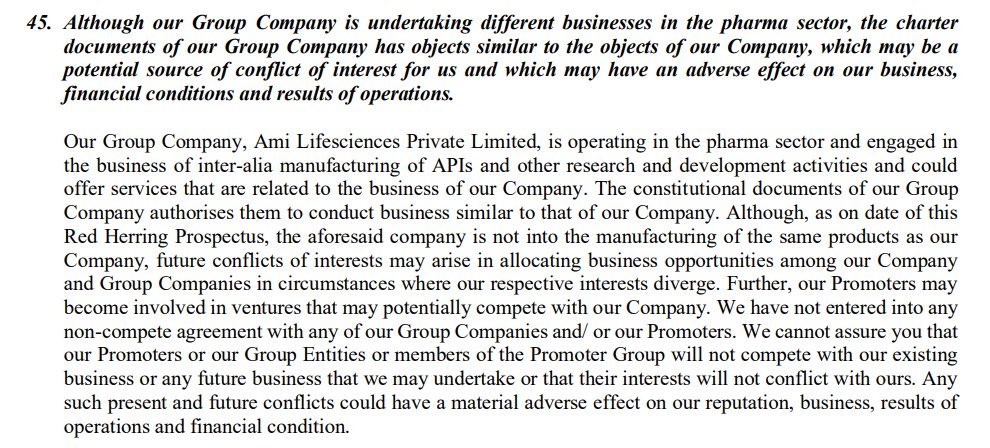

Ami Organics – Pharma Intermediates & Specialty Chemicals (29-08-2023)

Ami lifesciences is their group company (mentioned in RHP)