PTC India introduced the concept of Electricity Trading in India and co-promoted IEX.

Later it divested its entire stake in IEX.

Thereafter, It co-promoted another exchange – HPX and we can guess …sooner or later it will divest its stake in it.

No price for guessing who will most likely own the market coupling agency.

What is not good for IEX will also be not good for HPX.

In this great game being played out by PTC India do we know where the real cheese is moving ?

Posts in category Value Pickr

Indian Energy Exchange (IEX) (29-08-2023)

MapMyIndia – The Map Company (29-08-2023)

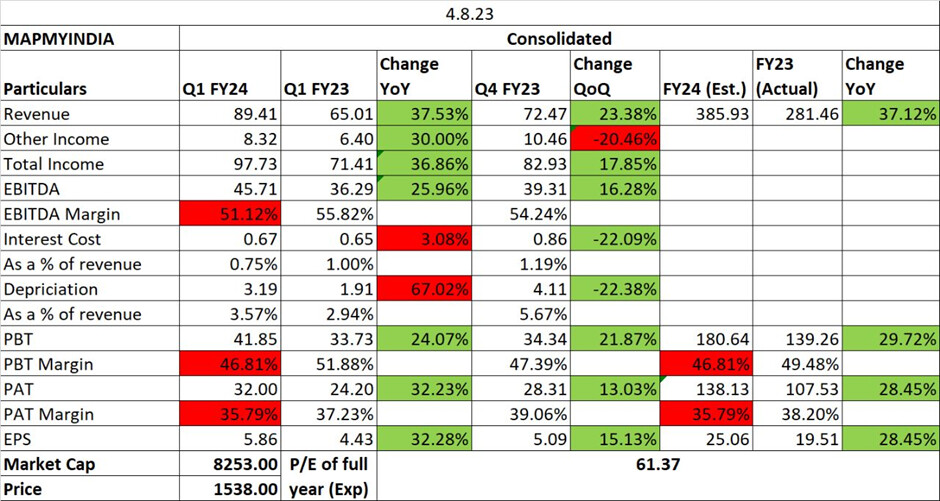

| – | Map-led business EBITDA margin was strong at 54.1%. IoT-led business EBITDA margin continued to expand quarterly and was at 6.3% in Q1FY24 versus 4.0% of Q4FY23, as SaaS income from IoT grew. |

|---|---|

| – | During Q1FY24, we outlined a 5-year vision of a growth roadmap for the company, and are putting in place the requisite foundations that will drive long-term success of the company. We are also delighted with the surge in interest and usage of our consumer-facing Mappls MapmyIndia app amongst users, which resulted in Mappls app becoming the top app in the app store recently. This bodes well for the B2C future of the company, in addition to the B2B and B2B2C where we have been traditionally strong. |

| – | Our strong Q1 YoY revenue growth was broad based with A&M (Automotive & Mobility Tech) up 24% and C&E (Consumer Tech & Enterprise Digital Transformation) up 51% on the market side. On the products side, Map & Data was up 41% and Platform & IoT was up 35%. We’re happy with the large number of customer go lives that occurred during Q1FY24 including many consumer technology companies and startups, corporates across industry sectors, automotive OEMs including EVs and 2- Wheelers, and government and logistics/mobility fleets. This bodes well for our future growth. |

| – | Cash continued to increase in this quarter as well. |

| – | IoT-led business is growing steadily, with expectations of expanding margin with the growth of SaaS income. |

| – | Automotive business is growing faster than industry volume growth, with increasing adoption of MapmyIndia solutions in EVs and ADAS vehicles. |

| – | International business is a focus area for future growth, with efforts to build international maps and expand presence in international markets. |

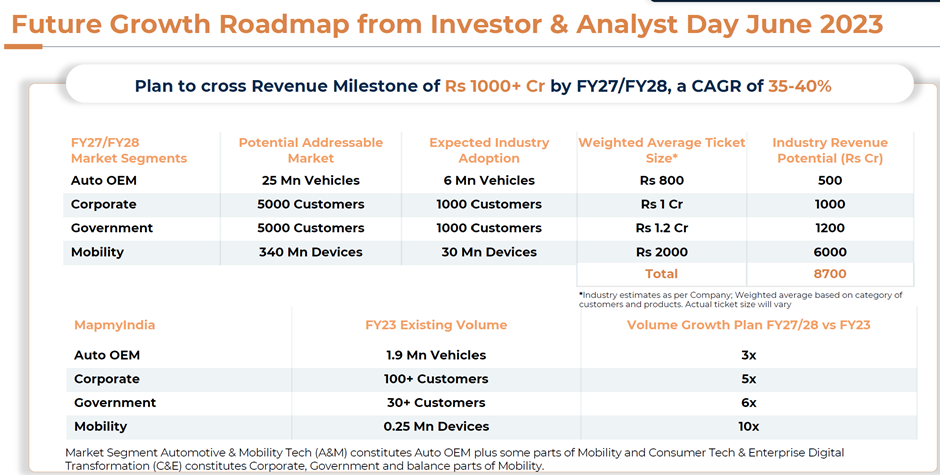

| – | Revenue growth projection of 40%+ for the year is on track. |

| – | Working with defense industry clients and seeing opportu |

Mudit’s Portfolio (Passively Active) (29-08-2023)

I maybe wrong but it seems your top allocation bets have changed significantly since you started the thread… your thoughts must have evolved with time.

Would be nice if you can capture some main points learnt in journey so far which changed your top bets and even the overall portfolio with time…

KPI Green- Turning Sunshine Into Cashflows (29-08-2023)

Which from below could be trade secret that they couldn’t disclose?

Pravin’s Portfolio (29-08-2023)

I don’t follow the company, but from what I can tell, it is tough to make any kind of call when a stock occupies 36% of the PF, if the absolute number is high w.r.t all your investments, which only you know. One can stay put considering the return is only 40%, and growth is visible for the next couple of years, and as such, it can double or even triple from here. Trimming and some profit booking can be done, and depending upon following the business, can add if the price moves up, averaging up at a higher price than the sold price of the trimmed shares. Or can stay put too, if one considers a company to be truly part of a long term PF, then there is no selling, no matter the occupying %, and such companies are rare, as there have to optionalities, future demergers, dividend, management pedigree, not to mention bought at reasonable price. So one can do what suits himself financially and psychologically.

I am still in the process of creating such a long term PF, and I also sell all of my position depending upon the situation, and rebuild my position again, sometimes correct, other times not so, so take my advice with a pinch of salt.

I don’t follow any of the stocks, but looks like the PF is diversified.

Zoom webinar on stage investing (29-08-2023)

Hi, I am interested. Here is my id : chandandatabox@gmail.com

Gokaldas exports — cup and handle/rising channel (29-08-2023)

mp points in the concall.

- Financing of acquisition is done through 40mn of debt and the rest through internal accruals.

- The acquired entity has prod. cap of 40mn with closer to 90% capacity.

- Acquired entity has USD 15mn of wc.

- Bangladesh there is noise of minimum wage hike-if that happens it will benefit Gokaldas.

- 20 mn of revenue is expected to be add in future depending on the market conditions.

- Dec 2025- duty free access to kenya ends.

- The management is confident of duty- free access renewal as kenya has strong ties with US region.

- There is no tax on profit earned by the acquired entity.

- Labour cost in kenya is a little higher but productivity is more efficient.

- There is good revenue visibility of order book for the acquired entity.

- The client of acquired entity is different from Gokaldas barring 1 company.

Zoom webinar on stage investing (29-08-2023)

Intrested sir , please add me.

Websol energy system ltd (29-08-2023)

Phase-2 will be funded by cash flow generated from Phase-1 as per Management comments. So, Phase-2 construction should start rolling from FY25-26 onwards (if Phase-1 generates positive cashflow during FY24 & 25). So, It is a two to three years story from now. One should not forget that Cell capacity of India will be substantial and sufficient to meet the demand by FY26.