Great! Thank you so much! ![]()

Posts in category Value Pickr

Investing Basics – Feel free to ask the most basic questions (27-08-2023)

KRBL- The King of Basmati rice (27-08-2023)

Avg basmati realisation for KRBL is 98000 (around $1180) per MT from their con-call(11-Aug-2023)

KRBL expectations seem to be there will be higher realisation (5-7%) for Q2.

Prima facie, there might be some impact.

Please correct me if any of this is wrong.

StageInvesting +Elliot Waves (27-08-2023)

sir,

if time permits, could you pls post the charts and share your inputs on vascon, natco, fredun, goodluck & prakash ind.

thanks.

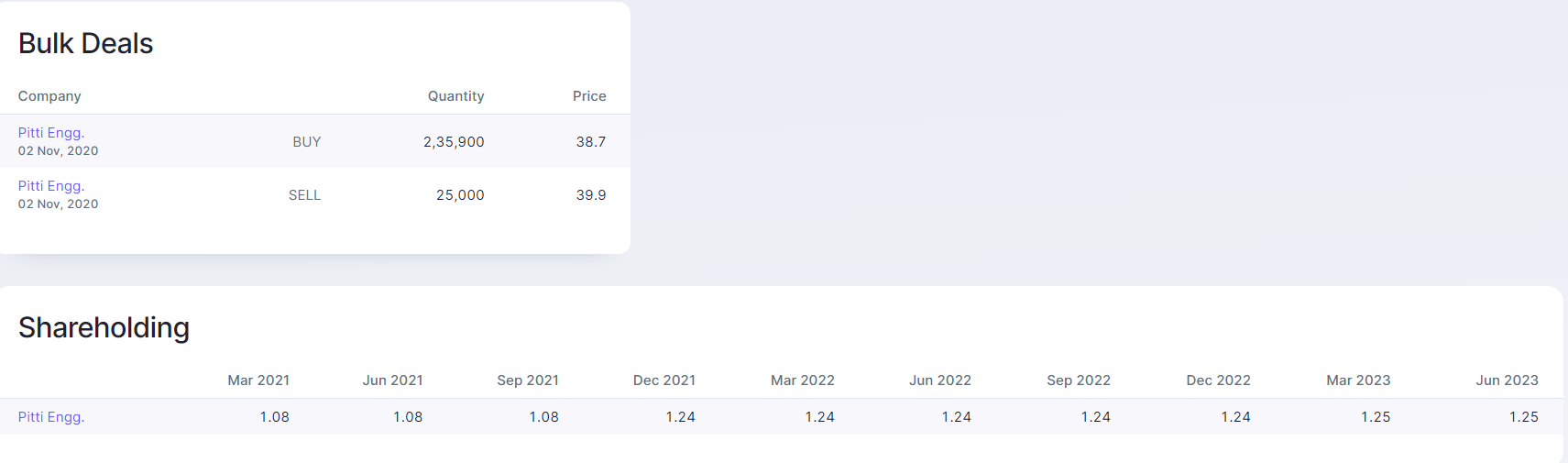

Pitti Engineering Limited: Is it on an inflection point? (27-08-2023)

Hi sir,

Is this you?

Just started tracking from my side and found this in shareholding pattern.

The levels you mentioned in this post and the name and levels in SHP are similar. So asking.

Thanks,

Suresh

H.G. Infra Engineering Ltd : Paving the Path to Success (27-08-2023)

HG Infra looks like an interesting investment opportunity but I am still trying to better understand the sector as whole. Is the high consolidated operating margins of about 20% the industry norm? The Consolidated operating margins of about 20% are higher than the stand alone margins of about 16-17%. Is it correct to presume that margins under HAM business are considerably higher than EPC?

The valuations appear to be low, when one considers that it is a two decade old company, with high promoter holding of about 75% and decent institutional names holding a good amount of the balance. With the ongoing Govt. thrust on the infrastructure sector, there ought to be plenty of opportunities for the Co., so a trailing PE of 11 at the CMP of about 913 seems rather attractive.

I also gather that one of the risks for infrastructure companies is that State govts are at times tardy in making payments, but that should not be the case here as most of the projects are with NHAI or with the private sector. Also, the revenues in the sector are back ended with 60-65% of the business coming in during the second half of the year.

Still in the conviction building stage here and any further inputs would be appreciated.

Usha Martin- Coming out of Chaos (27-08-2023)

Usha Martin Q1 concall highlights-

Offers wide range of-

Specialty Wire ropes

High Quality Wires

LRPC wires

Bespoke end fitments, accessories & related services

Consol Q1 outcomes-

Sales- 814 vs 760 cr

EBITDA- 146 vs 117 cr ( margins @ 17.9 vs 15.5 pc )

PAT- 101 vs 82 cr

Segmental revenues –

Wire ropes – 553 vs 481 cr, up 15 pc yoy

Wire and Strands – 65 vs 86 cr, down 24 pc yoy

LRPC – 116 vs 148 cr, down 22 pc yoy

Segment wise sales contribution –

Wire Ropes – 68 vs 67 pc

Wire and Strand – 8 vs 10 pc

LRPC – 14 vs 15 pc

Increase in rope sale in line with company’s strategy to focus on value added products

Volume wise data –

Wire Ropes – 23k vs 21k MT

Wire and Strands – 7k vs 9k MT

LRPC – 14k vs 17k MT

Geographical sales breakdown –

India – 44 pc

Europe – 24 pc

America – 7 pc

Middle East & Africa – 11 pc

Asia Pacific – 14 pc

In Q1, within Wire Ropes the share of speciality ropes ( for cranes, elevators, oil & offshore, mining, fishing ) increased from 65 to 71 pc

Revenues increased in Q1 despite YoY fall in RMs due better mix of value added sales

Exports in Q1 were up 13 pc

Nett Debt down to 99 cr vs 185 in Mar 23 despite 68 cr of Capex spend in Q1 – due very healthy cash flow generation

EBITDA / Ton @ Rs 32230 vs 26470 in FY 23 vs 19625 in FY 22 vs 15880 in FY 21

Committed to maintain > 18 pc EBITDA margins

Intend to improve the margins further as the product mix improves

As wins new international customers, margins can improve significantly. Current guidance is conservative

New wire ropes Capex to be concluded by Q3. Fresh volumes to start flowing in from Q4

Full ramp up to happen in 3-4 Qtrs

LRPC realisations are under pressure due capacity additions from Jindal Group, Tata Steel. Company now focussing on plasticated and galvanised LRPC products to differentiate and to add value

Hope to be Debt free by end of FY 24

Ranchi capex of aprox 350 cr to be completed by Q3. Has the potential to add 800 cr of annual sales at full capacity. Also, the products breakup from this new capex will favour the Higher Margin Speciality business

Chinese are not significant players in the value added segments

Guiding for 13-15 pc volume growth this yr and next yr despite volume contraction in Q1 !!!

Globally, Wire Ropes are growing at aprox 5 pc / yr. Company is gaining mkt share in international Mkts due better pricing vs Intl players and increased efforts towards customer service

Company’s global Mkt share is 5 pc. Intend to take it to 7-8 pc in medium term

Also looking to add value in the Wire segments for both domestic and export Mkts. This is also a huge mkt and can offer a lot of growth opportunities

In 2-3 yrs, EBITDA margins can be upwards of 20 pc due continuous focus on value additions

Disc : holding, biased

Ranvir’s Portfolio (27-08-2023)

Usha Martin Q1 concall highlights-

Offers wide range of-

Specialty Wire ropes

High Quality Wires

LRPC wires

Bespoke end fitments, accessories & related services

Consol Q1 outcomes-

Sales- 814 vs 760 cr

EBITDA- 146 vs 117 cr ( margins @ 17.9 vs 15.5 pc )

PAT- 101 vs 82 cr

Segmental revenues –

Wire ropes – 553 vs 481 cr, up 15 pc yoy

Wire and Strands – 65 vs 86 cr, down 24 pc yoy

LRPC – 116 vs 148 cr, down 22 pc yoy

Segment wise sales contribution –

Wire Ropes – 68 vs 67 pc

Wire and Strand – 8 vs 10 pc

LRPC – 14 vs 15 pc

Increase in rope sale in line with company’s strategy to focus on value added products

Volume wise data –

Wire Ropes – 23k vs 21k MT

Wire and Strands – 7k vs 9k MT

LRPC – 14k vs 17k MT

Geographical sales breakdown –

India – 44 pc

Europe – 24 pc

America – 7 pc

Middle East & Africa – 11 pc

Asia Pacific – 14 pc

In Q1, within Wire Ropes the share of speciality ropes ( for cranes, elevators, oil & offshore, mining, fishing ) increased from 65 to 71 pc

Revenues increased in Q1 despite YoY fall in RMs due better mix of value added sales

Exports in Q1 were up 13 pc

Nett Debt down to 99 cr vs 185 in Mar 23 despite 68 cr of Capex spend in Q1 – due very healthy cash flow generation

EBITDA / Ton @ Rs 32230 vs 26470 in FY 23 vs 19625 in FY 22 vs 15880 in FY 21

Committed to maintain > 18 pc EBITDA margins

Intend to improve the margins further as the product mix improves

As wins new international customers, margins can improve significantly. Current guidance is conservative

New wire ropes Capex to be concluded by Q3. Fresh volumes to start flowing in from Q4

Full ramp up to happen in 3-4 Qtrs

LRPC realisations are under pressure due capacity additions from Jindal Group, Tata Steel. Company now focussing on plasticated and galvanised LRPC products to differentiate and to add value

Hope to be Debt free by end of FY 24

Ranchi capex of aprox 350 cr to be completed by Q3. Has the potential to add 800 cr of annual sales at full capacity. Also, the products breakup from this new capex will favour the Higher Margin Speciality business

Chinese are not significant players in the value added segments

Guiding for 13-15 pc volume growth this yr and next yr despite volume contraction in Q1 !!!

Globally, Wire Ropes are growing at aprox 5 pc / yr. Company is gaining mkt share in international Mkts due better pricing vs Intl players and increased efforts towards customer service

Company’s global Mkt share is 5 pc. Intend to take it to 7-8 pc in medium term

Also looking to add value in the Wire segments for both domestic and export Mkts. This is also a huge mkt and can offer a lot of growth opportunities

In 2-3 yrs, EBITDA margins can be upwards of 20 pc due continuous focus on value additions

Disc : holding, biased

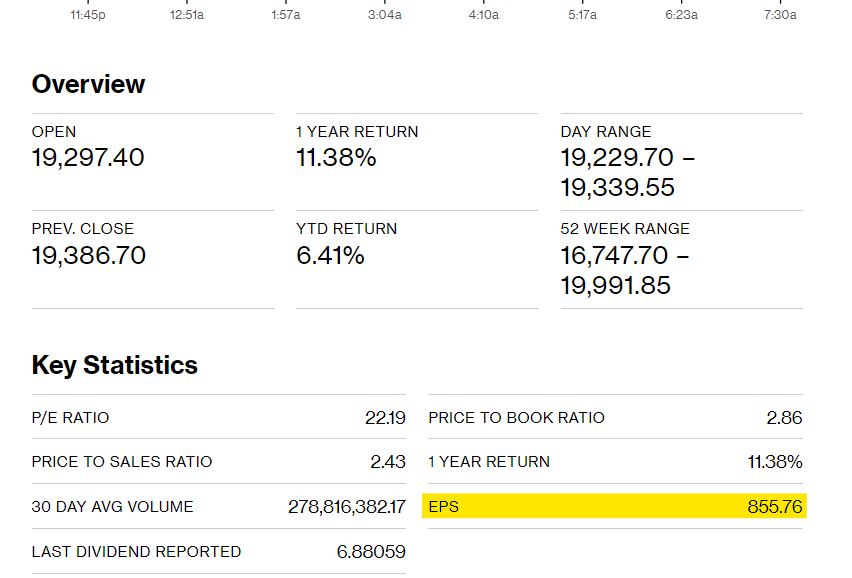

Nifty PE after all earnings have been declared (27-08-2023)

@Gaurav_Agarwal I just eye balled the numbers of stocks comprising the Nifty.

Motilal Oswal figures are (haven’t worked them out) Nifty EPS q-o-q

Trendlyne Nifty EPS that you see is trailing 12 months, y-o-y. So you may be comparing the wrong figures; i.e. q-o-q and y-o-y (and I think both numbers are correct). Now if you want to compare Trendlyne with Motilal, look at Trendlyne EPS on the day when you are sure all results for the previous quarter would have been declared and work out the EPS

Bloomberg (which I believe to be the most accurate) shows Nifty EPS as 855.75

Hope this is helpful

RACL Geartech Limited (27-08-2023)

RACL Geartech Q1FY24 Concall:

Business:

-Revenue grew by 10.88% YoY 89.62 cr vs 80.82 cr

-EBITDA grew by 31.31% YoY 23.19 cr vs 17.66 cr

-PBT grew by 44.18% YoY 11.65 cr vs Rs.8.08 cr

-Usually the first quarter of the company is the lowest for the year, this could have been much higher due to shipping bills being filed late

-EBITDA margins stood at 25%-26% (Increased by 4% vs Q1FY23) driven by higher value addition in the product segment. Moving from lose component manufacturer to highly precisioned oriented manufacturer.

-Working with many sub-assemblies.

-The more complex the part is, the more margin RACL is able to command

-New projects are taking shape towards electric segments, hybrid segments. The customer’s consciousness towards quality and procedure is much higher. The mould is more complex and designs from customers have also been very complex. That is why the gross margins look better.

-The product line is such that the raw material content in the products is very low due to complexity of the products where the value addition is more so that is why the gross margins are higher.

-Recently the new electric scooter launched by TVS a couple of days back which is an extensive scooter, RACL is the single sole supplier for their entire rear axel assembly and many other things. Value addition per vehicle is 10,000

-One more major super bike is being launched maybe in September for which the entire transmission is being supplied by RACL.

-Developing Yokes for motorcycle. The rear wheel will be driven by the propellers instead of a routine chain

-Until FY2020, the company was zero is passenger car vehicle and last year it was 6% and this year it will be more than 10%. RACL is into passenger cars like BMW 7 series, Porsche, Mercedes AMG, BMW X7, Aston Martin. The kind of precautions and stringent requirements are a lot in these segments.

-FY24 guidance maintained at Rs.500 cr

-Capex plans: Until FY267 250 cr & Asset turn guidance: aim is to take it to 2x which right now stands at 1.3x to 1.4x

Management:

-EBITDA Margin sustainability guidance: 20-26%

-OEM customers have one product one supplier (They never use two suppliers)

-Geographical based competition: China, Taiwan, Japan, South Korea.

-Considering to work towards industrial and aerospace segment

Risks:

-Quality issue may lead to loss of customer

-Raw material procurement

Picture of Yoke shared by the management which will be used in Motorcycles:

Disc: no recommendation to buy or sell.