I am interested. Please add me.

Posts in category Value Pickr

360 One WAM Ltd (Erstwhile IIFL Wealth) (24-08-2023)

@mahesh_s can you enlighten more about asset and wealth management in terms of what they do, how they manage funds, where do they put money in. Etc etc.

How is this differentiated when it comes to edelweiss/nuvama?

Zoom webinar on stage investing (24-08-2023)

Great ![]() count me in…!!

count me in…!!

Deep Value Portfolio (24-08-2023)

I come across this company through Promoter interview. I was surprise to know this is one fo the fortune 500 company from India.

their margin with very thin as they are in Gold refinening. the positives are

they are in the business for almost 30 years.

positives

very tradingnal family run business with operationally very efficient.(they are lowest gold refiner in the world)

lasty 5-6 yeras they have reduced their debt significantly 8000 cr to 750 Cr

Reservers increased

No capital raised

Negatives

no PR & investor call just focus on business

- very limited information available in public domain

- got selected in PLI scheme of govt (for batter manufacturing – this is positive as well negating (total diversification in no related business) – they have good balancesheet to diversify & if they do this businees as efficiently as they are doing gold refininig then its good marging business than their current business

Over all : available ar the same price of 2015 its long consolidated . I think very minimum downside and good potential upside.

Aarti Pharma Labs (24-08-2023)

Aarti Pharmalab is the company demerged from Aarti Industries and was focusing on mainly 4 areas

1. Caffeine and Xanthine based derivatives: APL is the global leader in caffeine and xanthine derivatives (derived from caffeine) and India’s largest player in xanthine derivatives. Caffeine, one of the more known Xanthine derivative, is used both in pharmaceutical and food and beverages. On Pharmaceutical side xanthine derivatives are used mainly as bronchodilators. APL has 4000 tons per annum capacity. The other larger players are CSPC (China) and Shangdong Xinuha which have larger capacity than APL.

2) API : APL makes high value APIs across therapies related to lifestyle diseases cardiovascular, anti-asthematic, anti-cancer, CNS and other therapies. They focus on regulated markets and US, EU and Japan constitutes 50% plus revenue for API business. According to earlier call transcripts (Aarti Industries) they focus on doing APIs which has value higher than USD 100/Kg. In fact some of the APIs like Salemterol Xinafoate and Mometasone Furoate have value as high as USD 20,000/Kg and USD 11,000/Kg. They have 40 US DMF approved and they have commercialized more than 50 APIs across therapies. Here is the list of APIs that APL is currently producing and in the pipeline. More importantly in many of it’s key APIs it is backward integrated and key intermediates are made inhouse which gives them cost competitiveness versus other global/chinese players.

aarti-pharmalabs-api-product-list.pdf (2.8 MB)

3) Intermdiates: APL manufactures range of intermediates for both generic products as well as for innovator’s patented products. Here is the list of intermediates that APL manufactures – with end API use. As we can see from the list APL manufactures more than 100 intermediates panning across more than 40 API. Not many companies in India have such diverse product basket in terms of intermediate. This shows the R&D strength of the company and it’s manufacturing capabilities. In addition to the below list APL also supplies intermediates to innovators which may be proprietary and part of the CDMO programs.

aarti-pharmalabs-api-intermediates-product-list.pdf (713.1 KB)

4. CDMO: This is the smallest part of the business as of now but very interesting part. APL started doing CRO and CDMO both but over time it realized that their core competence lies in manufacturing products at decent scale and not at very pilot scale. Hence they pivoted their business to do work for Phase 3 and later molecules for innovators. As per earlier ARs, investor presentations and conference calls, APL is working with global innovators and their CDMO partners (like Lonza) to make intermediates for patented products.

Thus if we look at the business in totality, each part of business has some entry barriers

Xanthine & Derivates – scale and cost leadership,

APIs- a large product portfolio of complex and high value- low volume API with domestic and global partners who have APL as source in their filings + very high level of backward integration

CDMO- Ability to manufacture patented product intermediates and supply to global innovators and large CDMO players like Lonza

Evolution of company: APL was part of Aarti Industries till 2023 and hence one has to go back to Aarti Industries AR, presentations and concalls to understand the journey. If we look back, the journey of APL has been nothing but extraordinary. In FY 12- APL (Aarti’s pharma segment) had revenue of 130 Crore and negative EBIT of 6 Crore, while in next 11 years, their revenue in FY 22 was 1300 cr with EBIT of 220 Crore. This clearly shows the management’s execution capability and competence to scale up business.

What makes APL Interesting story: Before we talk about the interesting part of the story, let me put down the turn off!! ![]() Management in latest presentations and conference call has guided for 10-15% EBIDTA growth for FY 24 and 12-17% EBIDTA growth for next 2-3 years. So essentially, they are not talking growth numbers anywhere near to past track record or something that is very exciting then what makes it interesting

Management in latest presentations and conference call has guided for 10-15% EBIDTA growth for FY 24 and 12-17% EBIDTA growth for next 2-3 years. So essentially, they are not talking growth numbers anywhere near to past track record or something that is very exciting then what makes it interesting

- APL has commercialized Tarapur API new block in Q2 FY 23 where validation is going on and total revenue potential is around USD 25-30 million (Aarti Industries FY 22 concall). As per management API facility takes around 2 years to reach optimal utilization – so by H2 FY 25 it can add similar revenue on run-rate basis (around 250 Cr)

- APL’s Atali expansion which is ongoing will come on stream in H2 FY 25 with total capex of 350 Cr. Considering management guidance on asset turns of 1.5-2 , we can assume 550-600 Cr topline in next 3 years

- APL has increased Xanthine capacity from 4000 tons to 5000 tons and full impact of the same will start from H2 FY 24. So there is room to add around 100 Cr from this

- On top of this as per latest AR APL has done capex on hydrogenation and intermediate debottlenecking – of around 100 Cr – which can add 150-200 Cr

- Hence with ongoing capex – Standalone topline can do 2500 Cr plus revenue in 3-4 years.

- Management was very confident of increasing CDMO business proportion from 6% higher level. In FY 24 only they want to take it to double digits. Once Atali projects come on stream, there will be significant capacity for CDMO available – which can give headroom for CDMO to grow at higher pace. Currently they have 14 products which are launched or near launch- for global innovators. If some of those products (of innovator) scale up to blockbuster, APL can benefit significantly. In any case, management clearly indicated that CDMO is higher margin business- thus overall margin profile of the company may inch up as it’s contribution grows.

- Intermediate business for APL has done phenomenally well in last 4-5 years. It was 50-60 Cr business in FY 20 and it went to 360-370 Cr in FY 22 (there after separate number is not available). However considering that most pharma companies are trying to de-risk supply chain from China and APL has wide product basket with backward integration in some of these products can help scale up this business further.

All in all APL is a scale company which has established it’s cost competitiveness across segments, has demonstrated track record of execution and growth and is available at reasonable valuation with potential optionality of margin improvement and CDMO scale up.

Key risks:

- Xanthine prices are trending downwards and in current environment we do not know how much further it can fall (considering last 2 years had high base) and hence it may have impact on short term performance considering Xanthine is 50% plus business

- Aarti group may have many private/public listed entities in the same business (Ganesh polychem which is JV is consolidated , Aarti USA which is trading in their as well as Aarti Industries products, Aarti drugs which also makes APIs and is getting into intermediates). However my understanding is that high value-low volume API/intermediates and Xanthine is only done by APL

- Regulatory risk remains as major part of APL’s business is dependent on regulated markets

Discl: Invested with reasonable allocation.

Crompton Greaves Consumer Product: Brand Revival (24-08-2023)

Switch Gears and Switches do sound like natural extensions. Another possible area can be – male and female grooming like – trimmers, dryers, straighteners, shavers etc. Water purifiers can be another target area in my opinion

Wires are a little capital intensive

Getting into electronics – may be a tough nut to crack

Zoom webinar on stage investing (24-08-2023)

Please count me in… very interested

E2E Networks Ltd – Listed small Cloud computing player (24-08-2023)

Thanks but these are not listed I believe

Carysil (earlier Acrysil) – Kitchen sinks (24-08-2023)

Even the Rushil Decor and many comps have talked about the SAP implementation and a soft quarter due to it.

Jio Financial Services (5th largest financial services company) (24-08-2023)

Jio Financial was formed as a result of Demerger of Reliance’s financial companies from RIL.

JFS’s information memorandum showcases its focus on 4 verticals:

- Retail lending – Starting with they’ll probably offer loans on consumer durables (powered by Reliance Digital, Retail), personal loans (Reliance Retail, Jio), MSME lending (Jio Payments Bank) [Source: IIFL, Reliance Earnings]

- AMC – JV with Blackrock for passive funds at low cost

- Insurance broking – Insurance broking for retail customers, SMEs and corporates. Company is also planning to enter Insurance Business (source: IIFL)

- Digital payments – Jio Payments Bank (JV with SBI)

Assets:

- Total Net worth: 28,000 Cr

- Holding (6.1% stake in RIL): 17,000 Cr (cost)

- Core Net worth: 11,000 Cr

Valuation:

-

RIL Holding Valuation:

The market value of its stake in RIL is ~1 lakh Cr. Since, this is a holding company it would get the holding company discount. It can be ~40% looking at other holding companies depending on how they use these shares. Happy to receive some suggestions here -

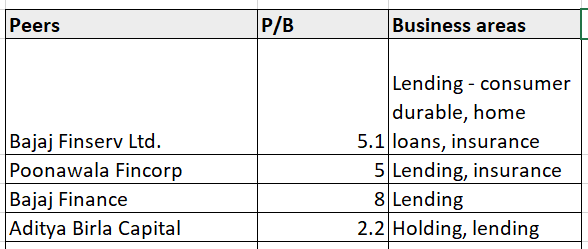

Core Business: Has a networth of 11,000 Cr at present. If it scales as it should, looking at peers, a reasonable multiple would be 5x P/B. Suggestions welcome.

Considering all the above factors, it’s currently trading a premium still but it’s a Reliance venture.

Credit penetration in India is still low, so there’s plenty of room for all players to grow. Also, lower chances of undercutting here considering cost of funds and regulatory strictness in this industry.

Future:

- They need to expand their physical footprint (not sure how to track this) for disbursement, collection

- Hire a bunch of employees (only ~9 on LinkedIn), maybe outsource some work to other companies like Adecco

Disc: Tracking. Would look to add in future